||

Acknowledging the countless unique metrics of macroecnomics and understanding how they can connect to general economic health and prosperity, we need to understand how they unite, as well as the cycles and patterns they prompt together. Over the last century, profound economists have researched and developed models that describe how the different components of an economy interact with each other, and visualized what problems can arise in a specific economy. Through their research, these economists have developed several models that represent how the economy functions as certain metrics rise and fall.

The Classical Model

The first profound macroeconomic model came through the works of Adam Smith – yes, the same Adam Smith who published Wealth of Nations in 1776. Adam Smith’s main ideologies can be summated to the idea that any market will resolve itself left untouched. This belief led to the notion that metrics such as prices, rates, and wages are flexible, being reiterated by several other economists of Smith’s time. Revolutionary economist Jean-Baptiste Say – ironically born in the same year Adam Smith published Wealth of Nations – brought his own developments to current theory with Say’s Law. Say created the law of markets, which argues that the production of any product will create demand for another product, through creating a unique value which can be then exchanged for another product. In simpler terms, production within a market drives demand.

But how is this relevant to the previous claims? Say also stemmed towards the idea that any economy can demand the maximum output that its workers and firms can produce. This economic state, where the economy’s resources are firing on all cylinders reflects the real GDP of that economy – the maximum GDP that the economy can produce. Say’s ideas, combined with the ideas of Adam Smith and flexible metrics, led to the economic theory that the GDP of any economy is always at or near the real GDP, as a lower GDP will prompt an increase in production to drive the GDP back up. Although somewhat loosely constructed, and dependent on natural occurrence of economic restoration, this model has proven to be reliable and maintained value since its creation hundreds of years ago.

The Keynesian Model

Another major economic breakthrough came during the great American depression, which saw widespread unemployment and famine across the United States in the 1930s. During this time, a man named John Maynard Keynes pioneered a belief that counteracted the principle that free markets will constantly provide job opportunity. His belief deemed aggregate demand – the spending of households, firms, and the government – as truly the most powerful economic force, where government intervention and policy leads to stability, rather than free markets. Keynes believed that an inadequate amount of demand would directly lead to lower employment; continually, he argued that demand must stem from one of the four economic output components (government, purchases, investments, and net exports), and during certain economic states will significantly decrease.

Recessions prompt negative consumer sentiment and lower consumer confidence, which make them less likely to spend money on products, goods, and services that they would have no problem with in a regular economic state. A reduction of consumer spending often leads to a decrease in firm investments: a response to a sudden weaker demand. Moving up the power tower, government intervention is then necessary to regulate the economy and bring it back to a healthy state. This process perfectly resembles the Keynesian theory, and shows direct examples of higher power being necessary to maintain the economy through the business cycle.

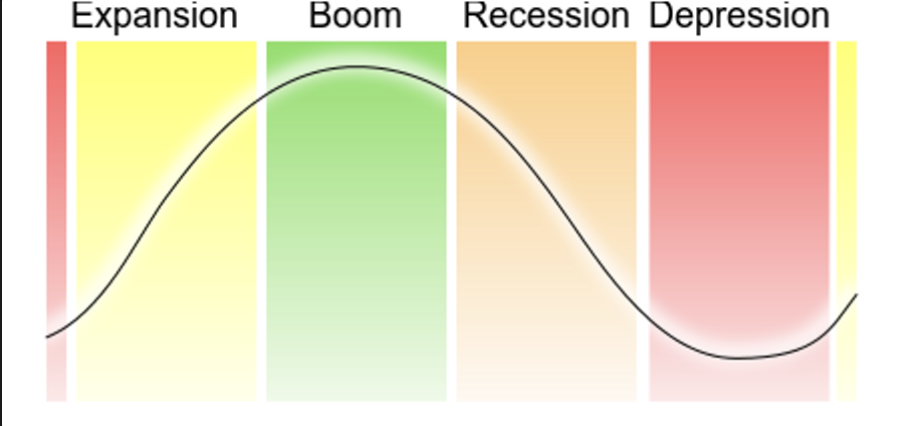

The Business Cycle

The business cycle, along with Keynesian theory, can be described through this chart:

As we can see, economic growth cycles through an upward expansion phase, reaches a parabolic peak in a boom, transitions downward in a recession, and plateaus negatively in a depression. We can see that this cycle is generally separated into two sections: the rise (expansion, boom) and decline (recession, depression). But how can we define each of these phases? The decline, mainly characterized by the recession, refers to a time where income falls, sales fall, production falls, and employment falls; cycling and repeating in that order. This plays directly into Keynesian theory, which calls for government policy and intervention to escape this very quick collapse. Moreover, the pit of the depression is where the policy is created, and as it ages, the economic health rises up. On the other hand, the rise phase is a time where income rises, sales rise, production rises, and employment rises. Generally, this rise phase covers a longer duration, as described government policy takes a longer time to reach full effect. This model is used time and time again, even reflecting economic patterns we have seen in the last hundred years very clearly.

Another prevalent model, the dynamic stochastic general equilibrium, uses macroeconomics to predict comovements (changes in metrics regarding the business cycle) and analyze how creating new policies can shape an economy. The CGE model, New Keynesian model, and many more have built upon the standards set time ago. These are a few of many macroeconomic models that can be used to survey the current economic state and better understand what trends are more likely to occur in the future. As our sense of economics only develops with more knowledge and data, more and more modern economic models will develop.

||

---------------------------

By: Sanjay Mukhyala

Title: Macroeconomic Models

Sourced From: streetfins.com/macroeconomic-models/

Published Date: Sun, 15 Oct 2023 16:15:59 +0000

Read More

Did you miss our previous article...

https://peaceofmindinvesting.com/clubs/does-it-really-make-sense-to-buy-the-new-iphone

.png) InvestingStocksToolsClubsVideosPrivacy PolicyTerms And Conditions

InvestingStocksToolsClubsVideosPrivacy PolicyTerms And Conditions