||

Company Overview

Qualcomm Incorporated ($QCOM) is a wireless technology company focused on the semiconductor, software, and service industries, operating with three main segments: Qualcomm CDMA Technologies (QCT), Qualcomm Technology Licensing (QTL), and Qualcomm Strategic Initiatives (QSI). The QCT segment utilizes a fabless model to develop and supply integrated circuits and software based on 3G, 4G, and 5G technologies used in mobile phones, wireless networks, consumer electronics, and, most recently, automotive systems. The QTL segment relies on the intellectual property portfolio to grant licenses and provide rights regarding the manufacturing or development of wireless devices to serve as the secondary revenue driver. Finally, the QSI segment generates revenue from strategic investments in newer, growth companies. The company is headquartered in San Diego, California, with around 45,000 employees and global revenue of $33.566 billion in the fiscal year 2021.

Sales by Geography

- China + Hong Kong: 67.07%

- South Korea: 7.05%

- United States: 4.19%

- Ireland: 3.46%

- Other: 18.23%

Company Statistics

Market Cap ($ Bn): $128.7 (as of 10/10/2022)

Enterprise Value ($ Bn): $137.4

52-Week Range: $112.92 – $193.58

Dividend Yield: 2.62%

Free Cash Flow Yield (2021): 11.03%

P/E (Current): 10.15x

P/E (Forward): 9.27x

EV/EBIT: 9.45x

ROE: 106.18%

CDP Score: B

Market Position + Share

QCOM is a strong leader in the segments in which it operates. Within the QCT segment itself, there are many industries to dissect:

- With a position in 5G in terms of their products and licensing/patenting portfolio, they remain highly relevant and continue to excel in this growing space. In terms of the smartphone application processor industry — one that focuses on selling Snapdragon products and consumer devices — Qualcomm places second, with a market share of 29%, falling short of MediaTek. However, the demand for premium-tier chipsets will allow them to drive better results and recapture some of the positions that slipped from their hands in the past years.

- In the global baseband processor market, Qualcomm has proven its dominance with a 55.70% share over other companies in the Annual Year 2021 and 23.5% in the smartphone RFFE market for Q1 2022. With Apple’s use of Qualcomm’s RFFE 5G Baseband technology and other premium Android devices, they have kept their modem and radio frequency business solid and relevant.

- Regarding the global cellular IoT chipset market, which encompasses automotive, router, asset tracking, and industrial IoT, to name a few, Qualcomm retained the highest market share of 38%. To combat the increasing competition from foreign vendors, Qualcomm has begun to target new verticals, enhance IoT demand, and excel as a company.

Not to mention, Qualcomm has also been utilizing its acquisitions to develop a market share in industries they had already visited or is growing. Two notable ones include:

- Nuvia, which would allow them to re-enter the server market. Despite Nuvia not selling any products, the SoC manufacturing that the company could do would allow them to expand its business to a newer range of consumers.

- Arriver, which, with Snapdragon, could open up a range of possibilities for automotive automation.

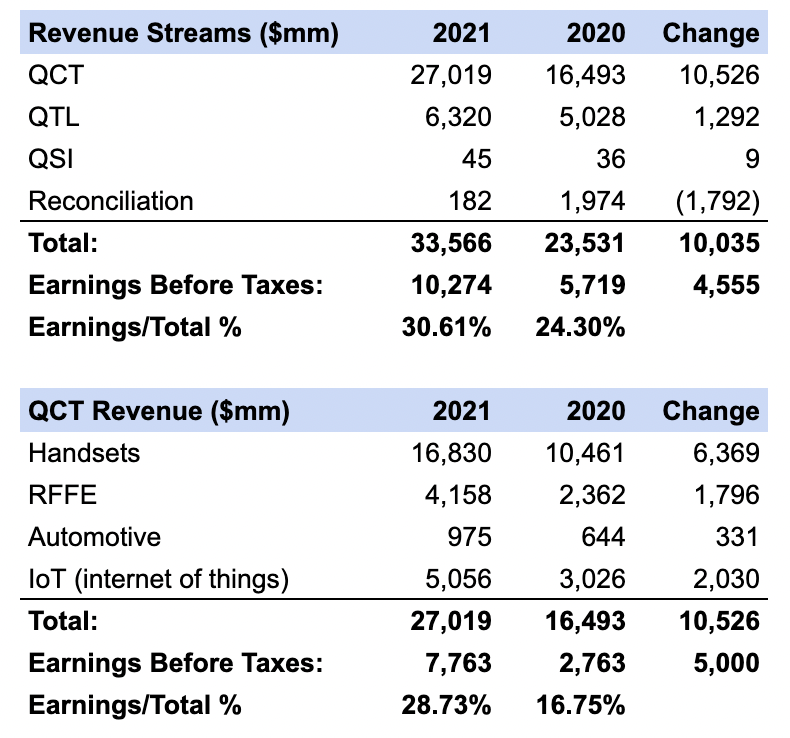

Revenue Streams + Drivers

As mentioned in the company overview, the three notable revenue streams for Qualcomm include QCT (CDMA Technologies), QTL (Licensing), and QSI (Investments).

Due to their fabless manufacturing model — a model in which they do not manufacture the chips — QCT solely encompasses the company’s design, development, and supply of integrated circuits and system software based on earlier 3G, 4G, and the most recent 5G technologies. Consumer devices — including handsets —radio frequency front-end to promote inter-device communication, automotive systems, and IoT (the internet of things – the network of physical products) utilize these technologies. One key highlight of their development is Snapdragon: a platform and set of products that provide an integrated system for advanced graphics, application processing, and AI development. This technology is being translated to the automotive sphere, with their chassis as the central point of discussion in their 2022 Automotive Investor Day.

Qualcomm’s second revenue stream — QTL — grants licenses and provides rights, in exchange for royalties, for their vast intellectual property and patent portfolio (140,000+ achieved and pending patents in the 3G/4G/5G industries). Since the company’s founding in 1985, over $75 billion and 20% of the revenues in the past decade have been invested towards R&D, promoting patent licensing to encourage growth, and leading to Qualcomm having created multi-year 5G patent license agreements with every major handset OEM (original equipment manufacturer).

Finally, the newer, more corporate development-focused revenue stream is Qualcomm’s Strategic Investments (QSI), primarily functioning through Qualcomm Ventures: an arm that focuses on early-stage investment to open up new opportunities for Qualcomm themselves. Whether in 5G, enterprise, or any other sector, the venture group invests in similar-minded and path companies like Jio, Matterport, Cruise, FitBit, Ring, Waze, Zoom, and August.

The main catalysts for growth tie in with the investment thesis and are: automation with Snapdragon, CPU emergence, continued 5G dominance.

Industry Analysis + Growth

Semiconductor Market: The semiconductor industry — with demand from smart electric cards to IoT devices — has continued to grow, despite the lost revenue in the two pandemic-ridden years, with the global market hitting an all-time high revenue of $556 billion in 2021 and expectations to be over $600 billion in 2022. Although the supply chain shortage has drained the demand and revenue streams and may continue to do so in coming years, financial strength, higher operational expectations, and new opportunities for wireless communications continue to instill confidence in the companies in the industry.

As KPMG notes, while IoT and wireless communications were considered to be the #1 revenue drivers for semiconductors for the past few years (and into the future), wireless communication took #1, with automotive at #2 and IoT at #3. Although the automotive sector of semiconductors remains only 10-11% of the industry’s total revenue, the more extended design in cycles and taxing processes have changed over COVID, and this niche market for automotive vehicles will reach over $200 billion in the next two decades.

The industry is estimated to have a 10% CAGR until 2026, with varied estimations (7%-12% after + valuations at over a trillion dollars by 2030 for the market); however, it’s important to note that the market does not remain limited to the smartphone industry. 5G and emerging technology applications are much past the mature smartphone industry: towards new sectors to improve overall efficiency and wireless communications. For now, the ascension of 5G, the prevalence of semiconductors in automotive safety, industrial automation, and autonomous capabilities are the primary revenue drivers of the semiconductor industry: three of the four on what Qualcomm has its eyes to develop and which they plan to secure a market share within.

Qualcomm is well positioned for this market, with its innovation, M&As, and R&D geared toward the automotive industry and its continual improvement of the Snapdragon chip to be implemented for 5G and RFFE purposes. As a result, their products remain extremely well in demand, as their market share reflects this, with baseband processors and smartphone application processor sectors at first and second place positions, respectively, in terms of revenue.

Autonomous Vehicles: Talks about autonomous vehicles have been circulating since 2016, when CEOs began promising completely self-dependent cars to drive them to and from work daily, along with longer rides. Although reality struck and full automation has not been accomplished, the software has been in progress as companies continue to improve Levels 1 and 2 — basic driver assistance programs — to achieve Levels 3, 4, and 5, as several companies work on these technologies. The different applications, propulsion types, vehicle types, regions, and breakdown of the vehicles are critical in opening up several opportunities to the market.

While the market was valued at $76.13 billion in 2020, the expected CAGR is projected to surpass $2.2 trillion by 2030, mainly due to several sectors’ dependence on these innovations to improve productivity and workforce efficiency. Although North America dominates in revenue, the Asia-Pacific region is expected to grow significantly during the forecast period. Moreover, with Qualcomm’s strong position among Chinese and Asian developers, they will also heavily benefit from the increased demand.

Overall, the globe is shifting over to significant growth in the autonomous automotive sector: promoting significant growth in recent years, rapidly advancing technology, and collaboration between tech firms like Qualcomm and vehicle manufacturers. This also shows the partnerships that allow autonomous cruise vehicles to exist on the roads between the government and these companies, as seen in Dubai and upcoming/in-works in other countries: an embrace of these newly developing technologies.

Due to how the market is tied to improving safety, reducing traffic congestion, and growing cloud and connection infrastructure, the industry’s growth continues to grow. While there are several divisions to this autonomous vehicle market, Qualcomm’s ability to dominate the sector in which they plan on operating with their digital chassis — the foundation for a plethora of car manufacturers for development — will be the reason for their success in the years to come.

The company itself believes automotive technology — specific to car-to-cloud connectivity, the digital cockpit’s increasing complexity, and ADAS systems — will reach a TAM of $100B by 2030 as an underestimate, with Qualcomm retaining a substantial portion of those customers, while competing for its spot with companies like Nvidia.

Financial Health

When it comes to the financial health of the company, due to the services being a mix of tangible and intangible assets, it’s challenging to use the book value to verify the company’s well-being. However, looking at the liquidity health of the company, the Quick Ratio — 0.9 — and the Current Ratio — 1.61 — tell us that the company is pretty liquid, yet many of its assets lie in inventory, mainly due to in which industry they exist. Looking at their leveraging, their debt-to-equity ratio — 0.97 — helps the shareholders understand that they utilize debt and equity pretty equally, with around 97 cents to every dollar raised from equity. Looking at Return on Equity — 106.18% — the company generates just above $1.06 for $1 of equity invested, which means they are efficiently using the capital they have been provided. With operating margins at 35.70%, it’s clear that Qualcomm is efficiently minimizing operating expenses to ensure they can effectively distribute their net income to shareholders and continue growing their business through investments.

Current Events/Reasons to Invest in QCOM

Analysis concludes that there are three reasons why Qualcomm is rated as a buy: their recent push into automation, their continued dominance in 5G, and their emergence in the CPU sector.

#1: The centerpiece of Qualcomm’s appearance and push in the automation sector is the Snapdragon Digital Chassis. This cloud-based automotive platform integrates all the essential automation technologies into a single, centralized unit: an idea that has not been done before. QCOM’s pipeline from this grew to $30 billion last quarter, up $19 billion from the previous $11 billion, which already emphasizes their exponential growth and dedication to this sector. Their figures suggest a $100 billion TAM by 2031, the company’s revenue at $9 billion for this sector (a gross underestimate in many analysts’ opinions), and a prevalent position in the market and among consumers. Qualcomm has partnered with Volkswagen on future automated driving efforts, BMW for Tier 3 Autonomous Driving Technology, and finalizing deals with General Motors (with whom they already have a long-standing partnership) and Mercedes Benz to integrate the Snapdragon Digital Chassis into their technologies. This new technology, comprising of a cockpit, ride, auto connectivity, and car-to-cloud platforms, has already attracted consumers including Acura, Audi, Buick, Ford, Mini, Hyundai, and Jaguar (large names in the automotive business), to serve as the platform on top of which they plan on developing their businesses. More importantly, Qualcomm’s technology extends beyond cars; the Snapdragon Digital Chassis can also be applied to two-wheelers and e-bikes, opening up their runway to growth and new opportunities in the future.

#2: Qualcomm’s prevalence in 5G is no question. How consumers gain access to 5G internet capability runs through Qualcomm; they were the first company to introduce a 5G modern with their Snapdragon X70. However, Qualcomm didn’t only enable the beginning of this industry; instead, they remain dominant in this sector. The Snapdragon X65 has been announced to be used in the upcoming iPhone 14 and Samsung Galaxy S23; the X70 will be implemented in forthcoming Sangam and Apple generations through at least the end of 2030 (when current contracts expire). Qualcomm has remained on top and dominant in a highly competitive market, cleverly acquiring companies and extending agreements to secure solid partnerships for 5G and, shockingly, future 6G market share. Not to mention, they plan on utilizing these 5G licenses to generate revenue from an autonomous vehicle viewpoint, meaning they are not restricting themselves to the technologies. Overall, however, with 5G connections expected to pass 1 billion by the end of 2022 and 2 billion by 2025, Qualcomm’s large market share in their industry will pay dividends to all shareholders in the near term and for years to come.

#3: The final and symbolic reason lies in Qualcomm’s emergence in CPU (ARM-based). QCOM recently acquired Nuvia (server chip maker) in 2021 to increase Nuvia’s chip’s peak performance, a surprising move as it meant their entrance into the CPU market, competing against companies like AMD and Intel. While the industry is infamous for its competitiveness, Qualcomm has been working with Amazon Web Services to break into the market. The significance of this is that there has been a considerable growth in demand for ARM-based servers. The market is projected to reach $16.7 billion in 2022, with a CAGR of 12.4% through 2032. This means if Qualcomm can establish itself as a player in the CPU market, it could significantly increase its revenue and profit looking to the future. This push towards a new market indicates how the change in governance has pushed the company to dominate many markets and become indispensable to cellular, automotive, and IoT products rather than the one market they had once conquered.

Investment Risks

There are two big categories in which the risks may be a part of: General and Business Specific.

When it comes to general risks, the main ones include:

- COVID-19: Not only did this pandemic have an impact on supply chain management, but the change of environment resulted in an impact on consumer trends. Although COVID is not as bad as it was when it started — quarantine, masking, and limited mobility — it still had a prominent and prevalent effect on the operation of businesses too.

- The life cycle of the economy: This factor can never be predicted but it is one that, with every division in the life cycle, will bring different types of swings in the economy and businesses.

- Supply-chain shortages

- Debt-related risks

- and IT breaches, especially with the cybersecurity threats and risks that prevail today.

From a semiconductor/business specific perspective, the risks include:

- Customers vertically integrating their business to reduce possible revenue, as Qualcomm’s functional model is based on small number of consumers, with high volume and high revenue

- Geopolitical tensions, especially the US/China trade as 67% of revenue for Qualcomm is concentrated in China

- The usage of the fabless production model, which, although may have its perks, also means not owning their own foundry to regulate and execute “supply strategies” that provide assurance to consumers.

- Efforts by some OEMs to not pay fair royalties, which would mean dedicating financial and time resources to making decisions, thus taking away from other opportunities (QTL focused)

- The competitiveness: 5G is an industry that has brought upon a lot of competition with a lot of changes too, requiring companies like Qualcomm to always be on their toes

- Semiconductor industry: just like the business cycle going through its ups and downs, the semiconductor industry is one of the most cyclical industries in the world.

Cash and Short-Term Investments Growth

Acquisitions

Some of Qualcomm’s 2022 acquisitions give investors insight into how they are positioning themselves for accelerated market growth in their focus areas.

One of the most notable and essential acquisitions supporting their integration into the automotive industry is Veoneer, with SSW Partners, which closed in April 2022. By funding the cash for the acquisition, they plan to incorporate the Arriver business to further their Snapdragon’s automotive utility. With the computer vision, drive policy, and driver assistance technologies in Snapdragon’s automotive platform to create an SoC ADAS platform for several manufacturers, this acquisition is in line with their future goals, as seen by the $30 billion updated R&D pipeline for the automotive development within QCT. Not to mention, Qualcomm will receive a portion of the sale of the non-Arriver arms of Veoneer’s business, nearly equivalent to the money they had spent.

Another notable acquisition is Nuvia, completed in March 2021. While the company has not sold any physical products, QCT products can integrate its in-process technology designs for CPUs, processors, and SoCs. With this acquisition, Qualcomm decided, in mid-August, to return to the server chip market, with Amazon Web Services as one of the first companies to take a look at their designs and offerings. While the competition will mainly be Intel, Apple, and AMD, the company’s usage of Nuvia technology — which derives itself from company ARM’s architecture, the source of Qualcomm’s legal server market controversy — would, without a doubt, enable the company to secure a strong market position in this niche sector. Even though Qualcomm owns licensing in the CPU space, their lack of focus on CPU, eliminating their advantage, and the prevalence of companies self-producing their chips would mean Nuvia has to develop better products than other competitors to prevail to be utilized in technologies in “late 2023”.

However, they continue to achieve their goal of becoming a dominant player in the sectors they join through smaller acquisitions. In June 2022, Qualcomm recently acquired Cellwize Wireless Technologies to accelerate its position in the 5G Radio Access Networks innovation and adoption, as well as automation and management software platforms. Cellwize could provide new infrastructure solutions to the growing 5G market to fuel not just the adoption of these technologies but a transformation of the entire industry.

Another notable acquisition was Augmented Pixels Inc., which, unlike any other acquisitions, expanded its development of AR/VR, the metaverse, and, specifically, geolocation and crowdsourcing technologies. This technology would have applications for AR navigation and 3D mapping for mobile phones, drones, and robots, thus indicative of their expansion to conquer every arm of the industries they join.

Qualcomm has become more active with acquisitions in recent years. They continue to expand through companies and innovative technologies that will expand their dominance in the market through customer base and product versatility.

Porter’s Five Forces

The analysis of Porter’s Five Forces covers, not only the company’s shortcomings or advantages, but also the landscape of the industry. The five analyses and their ratings are:

- Threat of New Entrants: The threat of new entrants is low. Chip-making requires years of research and development, and there are high upfront costs associated with breaking into the industry; after this, it still takes decades for a new corporation to build up trust and establish itself. Moreover, there is already high brand recognition among the existing players (Intel, Qualcomm, etc.).

- Threat of Substitutes: The threat of substitutes is moderate. Very few firms offer the same products in the market as Qualcomm, which would qualify as substitutes. Regardless, there are high switching costs for a business/consumer in the computer chip industry due to compatibility and dependency issues. Additionally, the recent semiconductor shortage has decreased the threat of substitutes as there are very few readily available products to switch to compared to the technologies of Qualcomm. That being said, some firms provide chips that can perform the same tasks as Qualcomm.

- Bargaining Power of Customers: The bargaining power of consumers is low. In the semiconductor space, there is substantial hardware and software dependency which makes switching to another product incredibly time-consuming and costly for the consumer. This inability to change products quickly reduces their bargaining power. Additionally, the lack of many players in the industry hurts consumers’ bargaining power because they lack various options.

- Bargaining Power of Suppliers: The bargaining power of suppliers is low. The raw materials necessary for production are readily available from several suppliers. Additionally, the corporations which act as suppliers are often medium-sized, meaning Qualcomm, a much larger corporation, is at a natural advantage. Also, the lack of product differentiation among the goods being supplied (as they are natural resources) means switching suppliers for Qualcomm is easy, reducing supplier bargaining power.

- Competitive Rivalry: Competitive rivalry among existing firms is very high. Consumers expect yearly updates and upgrades from Qualcomm and competitors’ technologies, meaning there exists a necessity for innovation. Economies of scale also serve as significant factors in the semiconductor industry, making price wars, in which rivals reduce costs and improve products to increase market share, common. Thus, the competitors can reduce costs through economies of scale. Finally, to be an established firm in this space requires heavy investments meaning the firms are “all in”; this increases competitive rivalry.

Moat Analysis

While having a considerable share in several markets, Qualcomm has a somewhat wide-moat, resulting from the mixture of narrow-moat qualities, due to the industry in which they develop their products, with some strong wide-moat attributes. Whether in 5G, automation, or CPUs, the markets they participate in are incredibly competitive. With most of their revenue coming from chip supply and design and the market requiring continual improvement, at any time, technologies from competitors like Broadcom, Intel, Nokia, Texas Instruments, and more can chip away at their market share.

However, the company can have specific wide-moat attributes that make them indispensable, even in perpetuity. Their Intellectual Patent Portfolio is much more vast than any other company in the market, with licensing on technology ranging from 3G/4G/5G services to automation and even the recently entered CPU market. Thus, Qualcomm’s diversity of market participation and hyper-aggressive licensing (to the extent to which companies need their patents to sell a phone) enable them to squeeze out several competitors, keeping them distinguishable and their business in continual demand.

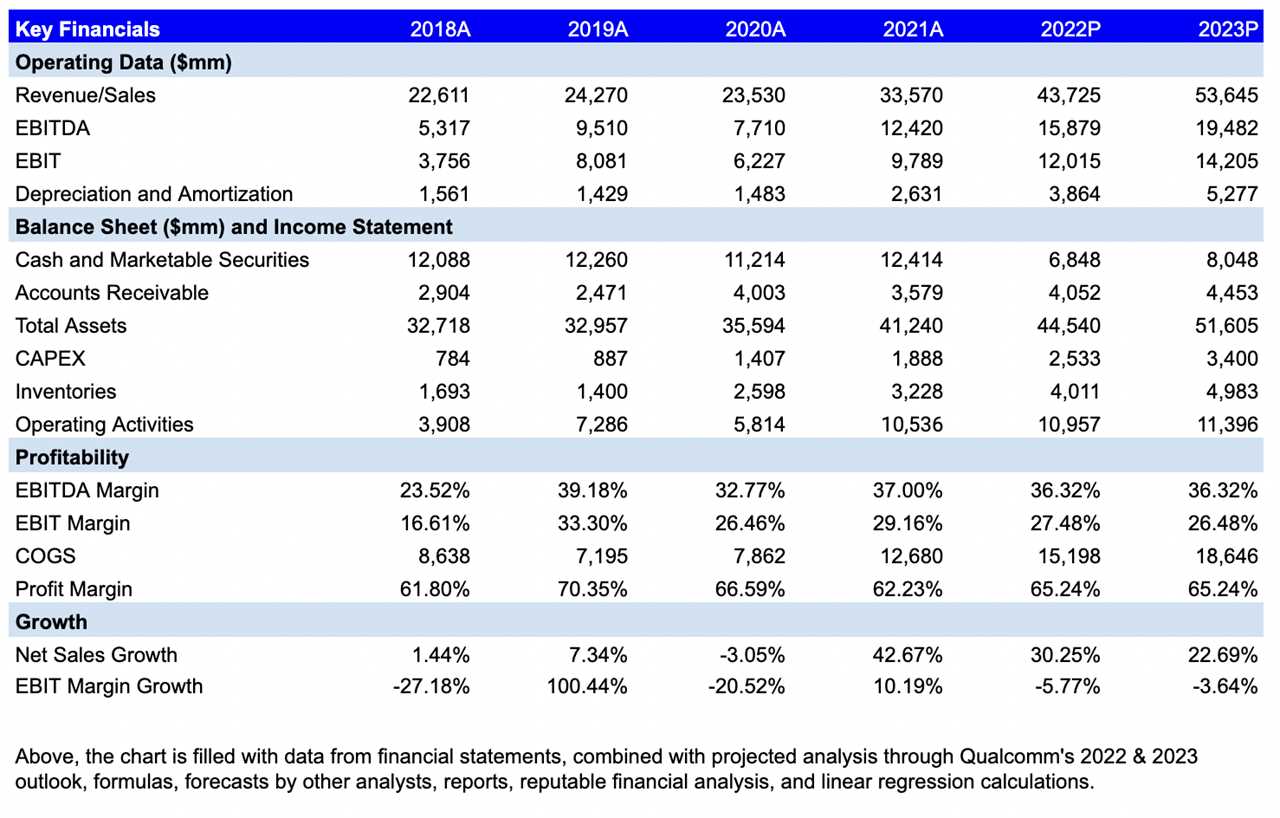

Key Financials Chart

DCF Calculation + Considerations

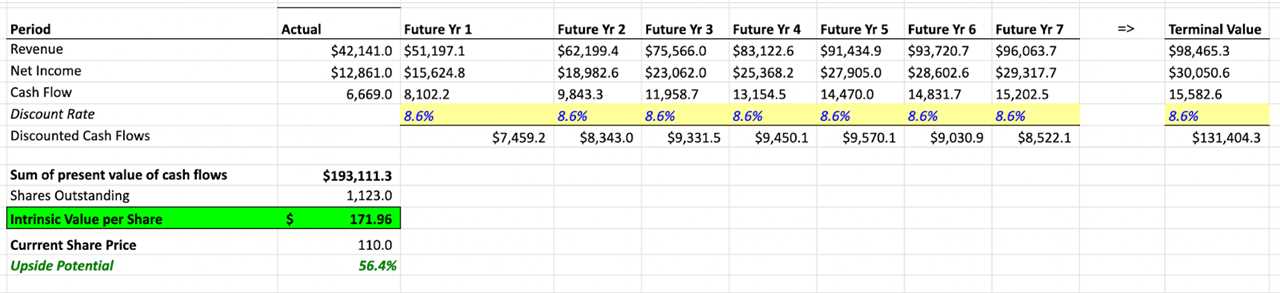

Simplified:

For the simplified calculation, revenue was based on an estimated CAGR, for the next five years, of around 21.5%, as forward looking due to the 5G expansion and autonomous automotive industries, with a terminal rate of 2.5%. Using the previous margins for Cash Flow and Net Income, along with a discount rate derived from “FinBox”, we were able to develop an intrinsic value per share of $171.96, relative to the current share price at around $110.

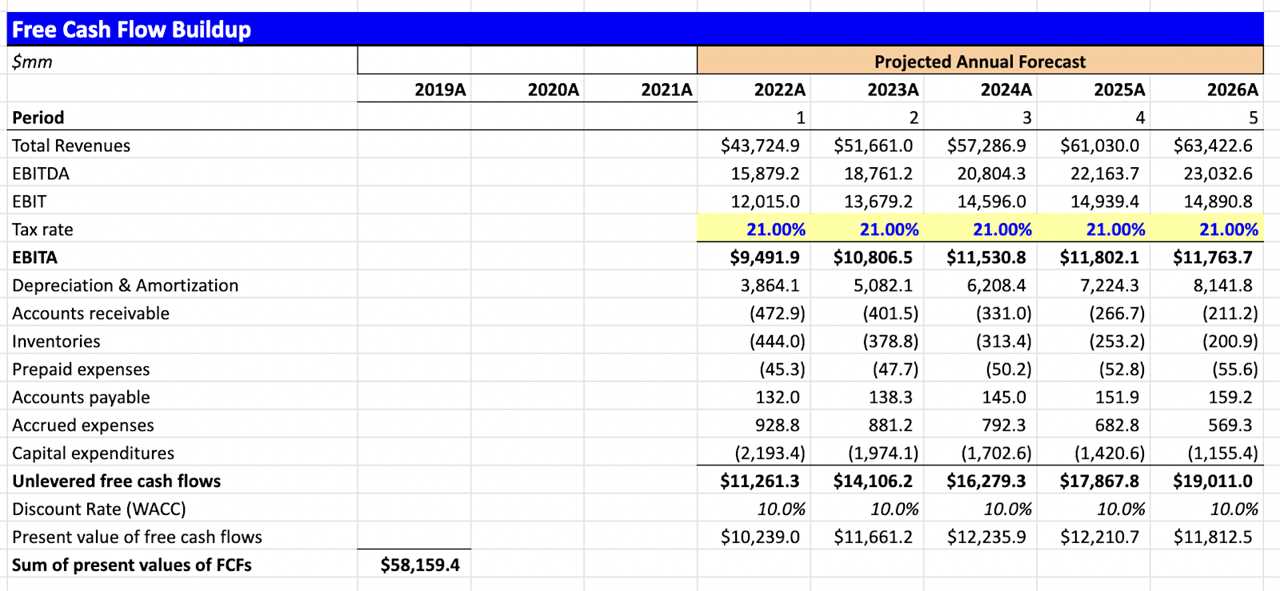

Detailed, but also with many more subjective variables:

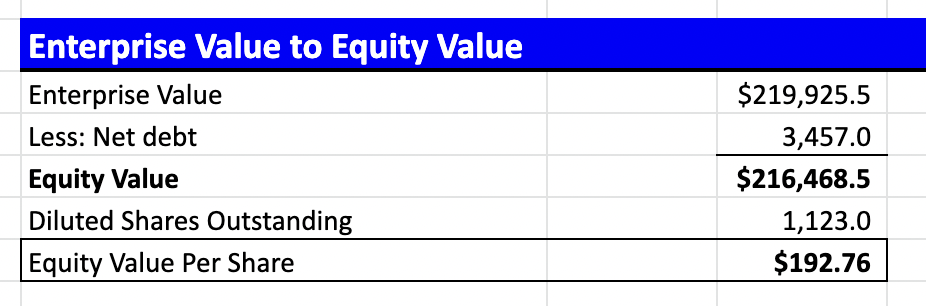

Although there were many more variables and subjective decisions that went into the DCF calculation, the main ones were near-sighted projections based on general industry and market growth as well as rationalized increases (decreases) in growth rates of certain parts of the company’s balance sheet. At the end, with a 21% corporate tax rate along with a WACC derived from GuruFocus’s calculations, we arrived at a value of $192.76, which, with a margin of safety of 5% can be considered as $183.12.

Management & Governance

- About the CEO: Cristiano R. Amon has been the President and CEO of Qualcomm Incorporated since June 2021. He joined Qualcomm in 1995 as an engineer, holding a B.S in Electrical Engineering and an honorary doctorate from UNICAMP, the state University of Campinas, Brazil. During his time at Qualcomm, he served as head of various subsidiaries at Qualcomm including QCT and QTI and was involved in the early stage development of the Qualcomm Snapdragon platforms.

- Top Institutional Shareholders: Vanguard Group; BlackRock; State Street Corporation; FMR, LLC; AllianceBernstein, L.P.; Geode Capital Management, LLC; Morgan Stanley; Bank of America, Price (T.Rowe) Associates; Northern Trust Corporation

Conclusion

Qualcomm Incorporated ($QCOM) is a wireless technology company with revenue from three segments: CDMA Technologies (QCT), Technology Licensing (QTL), and Strategic Initiatives (QSI). While participating in a market known for its ups and downs and with sales concentrated in Asia, Qualcomm’s continued dominance in 5G, emergence into the CPU sector, and push into automation are critical to its success as a business. In addition, their licensing technologies branch is essential to establishing their relevance and continued profits today, generating the second most revenue for their company. Keeping these factors in mind, along with the indication from Porter’s Five Forces that competitive rivalry is the most significant factor in play — continually demanding product innovation and excellence — we could estimate Qualcomm’s intrinsic equity value at $171.96 (simplified) and $183.12 (expanded). While their push towards innovation in the expanding automotive and CPU sphere has no reference point as to its projection, we have attempted to include the expected revenue from automotive and 5G into the 2026 Revenue, along with that of the continually expanding 5G market. Overall, with its acquisitions and CEO, whose qualities emphasize diversity and dedication to the company, the company has justified the valuation calculated.

||

---------------------------

By: Prateek Vyas, David Dettelbach and Kenan Pala

Title: Qualcomm: Stock Report

Sourced From: streetfins.com/qualcomm-stock-report/

Published Date: Fri, 04 Nov 2022 17:04:42 +0000

Read More

Did you miss our previous article...

https://peaceofmindinvesting.com/clubs/the-best-payday-advance-apps

.png) InvestingStocksToolsClubsVideosPrivacy PolicyTerms And Conditions

InvestingStocksToolsClubsVideosPrivacy PolicyTerms And Conditions