||

Even though most accounting items are standardized between industries, there are different views on what the balance sheet truly communicates. For one, the balance sheet records the capital invested: how much a business has invested in assets that allow for operations to occur. This sheet also measures the current value of a company, as well as the liquidation value – the value if all assets of a firm are liquidated, or sold.

Breaking it Down

The first section of the balance sheet refers to both the fixed and current assets of a company, which has been historically communicated in different ways. The older standard in accounting called each assed at their original cost, net of any depreciation, while the modern standard lists items at their current market value. Following this section, the financial assets of a company communicate holding in securities or partial ownerships of other companies. Holdings of other companies can be classified in two different ways: if the stakeholder owns more than 50% of the company, all subsidiaries of the company are included. In this scenario, the portions not owned by the larger company are labeled as liabilities. This is known as a full consolidation. If the stake is a minority holding, it will usually be deemed a long-term investment.

A unique section of company assets falls in the intangible assets, which classify non-numerical company value; namely, brand-name value, management quality, etc. In general, it is easier for accountants to evaluate smaller intangibles, such as licenses and consumer lists, than other intangibles that lead to large ambiguity. Good will takes the crown for this, being renowned as the most destructive item on the balance sheet. Many call good will a plug variable that signifies little, while others write it as the difference in price in acquisition and the book value of a company. The only reason this discrepancy can stand with such an untamed measurement is because without it, the balance sheet would not be balanced. For the balance sheet to be balanced, the total assets should equal the total of liabilities and shareholders’ equity combined. Here, goodwill will refer to any missing asset-value that would restore this balance. As described, good will holds no real value, and therefore does not have any influence on the stock market.

Now for the liabilities section. The current liabilities cover both interest bearing and non-bearing liabilities. These are mainly supplier credit, short-term debt, and commercial paper (a unique form of interest). They can also be deferred salaries, taxes, and liabilities that are due soon in relation to the release of the statement. The due debt of a company is mostly described in its name. However, there is more than one version of such debt that the balance sheet describes. Corporate bonds (debt raised from the public markets), lease debt, and bank debt (originally borrowed money) are the main three in this category. There are also the footnotes, which include other debts that cannot be characterized as the previous three.

The final major portion of liabilities is shareholder equity. Like many other values in accounting, there is an old and new standard to this liability. The old way calls shareholder equity as the equity that was needed to start a business, and grows with the addition of equity and accumulated earnings. The more modern way of understanding shareholder equity is through MTM accounting (mark to market), which has developed a lot of negative feedback because of its inability to communicate intrinsic value of a company. Shareholder equity is further broken down into company age (total revenue raised and total retained earnings from market value), and buyback effects (dividends and buybacks). The shareholder equity can become negative, but it does not indicate much about the company because it could be a result of a specific business model that the particular company has adopted.

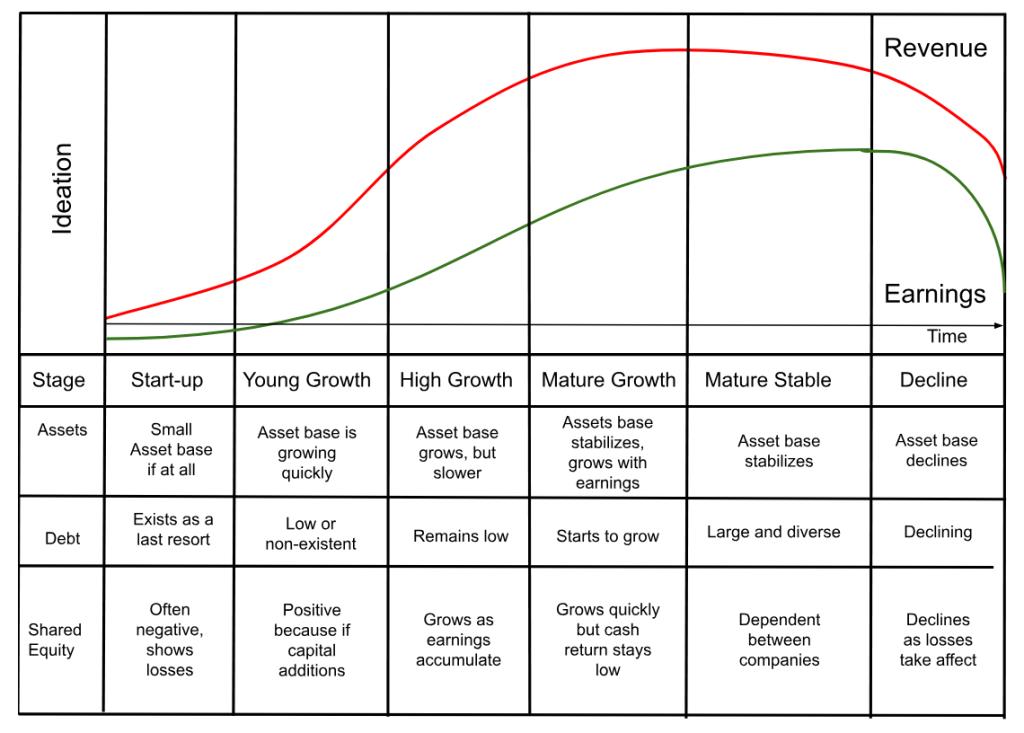

The Balance Sheet vs Company Life-Cycle

In the same way we analyze income statements over company life cycle, we can compare balance sheets.

In a similar system to the company life cycle model considering revenue and profit, we can see how assets, debt, and shareholder equity changes as a business develops. This model can provide effective insight on a company’s balance statement, and we can make a more informed analysis on the future projections of a company’s assets, equity, and debt. We can start looking for the same telltale signs through the same young company, Peloton.

Finding the Signs

Let’s use the same financial report of Peloton in 2019, but highlight the balance sheet. What can we see in this report that reveals Peloton’s status as a company in the startup and young growth stage? Firstly, we can see that the total asset is bare but shows rapid growth from 2017 to 2019. We can also see that the shareholder equity is negative, as they are negative in funds as the company is just starting. We can also see that of their small asset base, the large majority is placed in securities, further proving their stance as a startup with a larger focus on safer assets versus high growth assets.

We can use a similar analytical approach on Netflix’s 2019 report. Their largest liability is in non-current content costs. Understanding that Netflix is constantly curating new media for their customers, they are placing a very large investment into future content’s performance. They also have a very large portion of deferred revenue. If we look at Netflix as a business again, this makes sense, as their main source of revenue is through an SaaS subscription model. In other words, Netflix customers have not paid for the entirety of their yearly subscription yet, and the money they will eventually collect is deferred.

Now a more mature company: Coca Cola. The first thing that catches our eye is the very large asset base. While large, the asset base is not growing much. This is because Coca Cola is in its maturing stage, and will likely not experience much significant growth in the future. Meanwhile, their holdings in other companies take the majority of their company investments, and are not often exercised. A unique item you will see in this 2019 report is deferred tax income. This simply means that they had overpaid taxes in the last year, and are receiving this money back. We can also see that Coca Cola has a large amount of buy-back shares of their stock. This can mean one of two things. This holding can stay as shares outstanding (bought back by the company and held), or shares removed from public holding entirely. Ultimately, we do not know which may be the case. In the footnotes of this balance sheet, you can see Coca Cola breakdown their individual debts, interest rates, and when that debt will return to consumers in their stock dividend. In their intangible assets, we can see that their largest is goodwill, which in this case is simply the difference between the estimated real value of a company and the actual price paid to acquire it.

Lastly, the aging company, Toyota. Here, we can see that their total assets and revenue have been basically frozen, as they are approaching the end of their life as a company. Similar to the return of overpaid taxes in assets for Coca Cola, we can see accrued pension in the liabilities, as severance of underpaid taxes.

Sector Differences

Similar to the differences between sector and industry in the income sheet, there are simple ways to differentiate between industries and compare two different companies in two different industries. Let’s look at examples of balance sheets in different industries as well as how we can read these sheets without any bias.

Let’s take a look back at Total, that French oil company. On their 2019 sheet we can see that the inventory (oil) of the company fluctuates, but not to a high degree. If we compare this to the price-per-barrel during this time, we can see that the net inventory is not hit as hard as the price is. This brings a difference between the income sheet and the balance sheet for commodities. The balance sheet will not be as affected by commodity prices as much as the income sheet will, as the assets of a company will not be thrown away in the event of a significant price change. We can look at the liabilities side of the sheet for more unique information. Here, we can see that there is a currency translation adjustment category, which in other words reflects ForEx transactions. If we remember that Total is a French company that delves in business internationally, this makes a lot of sense. This can be applied to most commodity companies, as they are likely doing business across the world.

Now, let’s take a similar approach to analyzing a financial service company’s balance sheet. Take HSBC’s 2019 report. On the asset side, we can see a very large number of asset categories compared to most companies. This is because banks deal with many parts of the business world, with other companies, and manage their own assets. Noticing a company with a large asset portfolio doesn’t necessarily mean they manage a large volume of assets, rather, they simply have their assets diversified.

Finally, Dr. Reddy’s Labs: a pharmaceutical company. You would initially think that a major pharmaceutical company would list their patents as a major asset, but that is usually incorrect. Pharmaceutical assets usually document assets like this in other places of their report. This again highlights how paying close attention to companies of different sectors can play out in their balance sheet, and how you can mitigate a lack of understanding based on this.

In its essence, a balance sheet effectively communicates the history of a company, through the current values of their assets and liabilities. In the end, because of historical and current accounting standard disputes, the balance sheet is not a truly effective evaluation of company status as a whole, but can reveal important details not found anywhere else.

||

---------------------------

By: Sanjay Mukhyala

Title: Deep Dive into the Balance Sheet

Sourced From: streetfins.com/deep-dive-into-the-balance-sheet/

Published Date: Tue, 01 Aug 2023 01:19:43 +0000

Read More

Did you miss our previous article...

https://peaceofmindinvesting.com/clubs/are-colleges-allowed-to-allow-pets-in-the-dorms-and-on-campus

.png) InvestingStocksToolsClubsVideosPrivacy PolicyTerms And Conditions

InvestingStocksToolsClubsVideosPrivacy PolicyTerms And Conditions