<iframe style="width:120px;height:240px;" marginwidth="0" marginheight="0" scrolling="no" frameborder="0" src="//ws-na.amazon-adsystem.com/widgets/q?ServiceVersion=20070822&OneJS=1&Operation=GetAdHtml&MarketPlace=US&source=ss&ref=as_ss_li_til&ad_type=product_link&tracking_id=peaceinvesting-20&language=en_US&marketplace=amazon®ion=US&placement=0060555661&asins=0060555661&linkId=80f8e3b229e4b6fdde8abb238ddd5f6e&show_border=true&link_opens_in_new_window=true"></iframe>|<iframe style="width:120px;height:240px;" marginwidth="0" marginheight="0" scrolling="no" frameborder="0" src="//ws-na.amazon-adsystem.com/widgets/q?ServiceVersion=20070822&OneJS=1&Operation=GetAdHtml&MarketPlace=US&source=ss&ref=as_ss_li_til&ad_type=product_link&tracking_id=peaceinvesting-20&language=en_US&marketplace=amazon®ion=US&placement=1119404509&asins=1119404509&linkId=0beba130446bb217ea2d9cfdcf3b846b&show_border=true&link_opens_in_new_window=true"></iframe>|<iframe style="width:120px;height:240px;" marginwidth="0" marginheight="0" scrolling="no" frameborder="0" src="//ws-na.amazon-adsystem.com/widgets/q?ServiceVersion=20070822&OneJS=1&Operation=GetAdHtml&MarketPlace=US&source=ss&ref=as_ss_li_til&ad_type=product_link&tracking_id=peaceinvesting-20&language=en_US&marketplace=amazon®ion=US&placement=1119376629&asins=1119376629&linkId=2f1e6ff64e783437104d091faaedfec7&show_border=true&link_opens_in_new_window=true"></iframe>

[Editor's Note: Deadline alert! Today is the last day to enroll in Expert Witness Startup School, where you’ll learn how to launch and build a new source of income that could pay you $500-$900 an hour. As one recent student wrote, “I’ve made more money (~$50,000 in the last eight months) doing this than I ever thought I would.” This four-week CME-eligible course teaches you how to work this side gig on your own schedule by using the skills you already have. And as a bonus, WCI will throw in our 2021 CFE Course (a $699 value) for free. Sign up for Expert Witness Startup School today and begin reaping the benefits.]

By Dr. James M. Dahle, WCI Founder

One of the most enjoyable parts of my week is when Megan Ashriel comes back to work on Monday morning. You may not know Ashriel; she works behind the scenes here at WCI. One of her many tasks is managing the editor (at) whitecoatinvestor.com email box. It's a totally overwhelming job that I was glad to give up a couple of years ago. She forwards emails to the appropriate person on the WCI team to handle them.

Reader and listener questions get sent to me. I get a few every day, but since Megan doesn't work on weekends (Ashriel actually does sometimes but she just recently took over the job after this post was actually written), I get questions from Friday, Saturday, Sunday, and Monday morning all at once when she starts her work week. There's lots of work involved in WCI, and, to be honest, there's a lot of it I don't really like. But I do like answering your questions, and I do like writing blog posts. As I powered through these questions one recent Monday, I thought it would be fun to make a blog post out of them, kind of like the way I take Speakpipe questions on the podcast.

Might as well create some great content at the same time I help out a few people individually, right? So instead of Monday Morning Quarterbacking, today we're going to do a Monday Morning Q&A. I've removed identifying details and shortened a few emails for purposes of anonymity and clarity.

How Can I Minimize Charitable Giving Fees?

Q. “When trying to donate to a charity this month, I tried donating online. Traditionally I have avoided using credit cards because I heard they had a fee associated with them, favoring direct transfers, debit cards, and PayPal instead. However, I'm realizing now with a little research that the latter two may ALSO have fees associated with them (the charity is only getting 98 cents on the dollar donated). Additionally, some charities don't do direct transfers anymore. I'm a resident, so I don't have the good fortune of giving from a Donor Advised Fund (DAF) or donating appreciated shares (offsetting with tax-loss harvesting). What is the most ‘efficient' way to make sure the charity gets every dollar intended for them? Do I have to throw a paper check in the mail, slap a stamp on it, and send it to them? Or just swallow the fees, pay the difference so the charity gets how much I am trying to give them, and roll my eyes at the middle man?”

A. I've done checks in the past. If you don't want to pay/lose 2%, that's pretty much your main option. All a DAF does is send a check.

Should I Transition My Vanguard Mutual Fund Account to a Vanguard Brokerage Account?

Q. “[Forwards an email from Vanguard that says, ‘If you choose to remain on the mutual fund-only platform after September 30, 2022, you'll be charged a $20 annual account service fee for each fund account to offset the costs and complexity of maintaining this system. You'll see a fee of $20.00 in your transaction history. Additionally, your account may lose certain features and functionality over time. However, if you transition your account to the VBA platform, you can avoid paying this account service fee. There's no charge to switch, and in most cases, you can make the change online in a few minutes.']

Now I’m being threatened to not transition.”

A. I transitioned years ago. It's no big deal. Might as well do it. If it really bothers you, you can always move it all to Fidelity or Schwab.

Should I Swap My Student Loans for a Larger Mortgage as I Move?

Q. “Currently, we own a home with approximately $550,000 left on the mortgage with an interest rate of 3.975%. The estimated sale price is $950,000. I owe roughly $360,000 on student loans. I am four years out of residency and make close to $700,000 per year. My wife and I like our current home, but it's not a dream home and we are looking to move. Is it wise, stupid, or financially irresponsible to sell our current home, take the equity and pay off student loans, and then purchase our ‘dream' home where we push the $1 million mortgage using a physician mortgage?”

A. No, that's not crazy. Debt is fungible for the most part—$360,000 in student loans is about the same as an extra $360,000 in mortgage debt. With a $700,000 income, I expect you will wipe out both your student loans and your mortgage relatively quickly.

Additional details I should have added: My guideline for mortgages is no more than 2X gross income. With a $700,000 income, I'd be OK with a mortgage of up to $1.4 million. If you want to buy more than that, save up a down payment. Mortgage interest is also generally deductible (although there are limits, such as the current $750,000 limit), and student loan interest for attendings generally is not. Note that HELOC interest on a loan of up to $100,000 is deductible only if used to buy or improve the home—not to pay off student loans. But in this case, the purpose of the loan would be to buy the new home, so the interest on the first $750,000 would be deductible, lowering the effective interest rate.

Should I Try to Save Money on My Employees' Healthcare Expenses?

Q. “I recently reached out to an independent agent in the town I work because some of my employees are interested in short-term disability coverage. I own a small private general dental office. When she presented options for the short-term disability, she also presented me with a ‘Total Wellness Program,' which is why I am reaching out to you. It seems too good to be true. Essentially from what I can understand, they take advantage of Section 105(b) associated with the Affordable Care Act, and, from my understanding, charge you for the coverage which decreases the taxable income that employees and employer pay taxes on. Then, they are given a credit for taxes paid to make it so everyone saves money. They charge a $30 per month fee. But with the credit back after taxes are removed and savings in taxes paid, they make it sound like with my 10 employees on payroll I could save over $20,000 per year from my own paycheck savings and savings on money not spent on the employer portion of taxes. What do you think?”

A. A “Health and Wellness Program” in the workplace sounds a lot like a Health Reimbursement Account (HRA) or “Cafeteria Plan,” which allow the purchase of healthcare with pre-tax dollars for employees and saves payroll taxes for the employer. As an employee, an HRA plan or this sort of a program basically turns a high deductible plan into a low deductible plan. Glad it's working out well for you. You can submit a guest post in a few months if it ends up being as big of a deal as you hope and share the info with others.

Additional details I should have added: Whether your employees feel they are coming out ahead when you pay them less in order to cover more of their healthcare expenses will be up to them and how well you explain the program to them. If you pay them the same salary and now start paying for their healthcare costs in addition, you're probably not going to come out ahead, even with an extra tax break.

Am I Getting Hosed on My Term Life Insurance?

Q. “I am 45 with multiple lifelong heart issues. I have actually been very lucky in that I was able to compete in sports and actually competed professionally for a while. I’m a new attending making around $300,000. I have disability insurance which is rated and costs $345 per month. I was initially denied for term life, but I asked my cardiologist to write a letter explaining my risk. He actually stated I have less risk and a longer life expectancy than a diabetic. My agent was able to shop me out to several companies, and AIG has the best offer ($100 per month for a 20-year term with $260,000 and 30-year with $100,000 benefit). Not sure if that’s even reasonable or if that $1,200 yearly premium could be placed in a better scenario? Currently maxing out Roth and 401(k), but late to the game in medicine.”

A. Ugh. You're stuck between a rock and a hard place. At least you can get insurance, but man, that's a terrible price. Just to give you a sense of how terrible, if you were a totally healthy 45-year-old male, you could get $350,000 of 30-year level term insurance for $57 a month. A 20-year level term would be $34 a month. You're paying more than double due to your health. You can save some money by having it all be 20-year term if you can hit financial independence by then.

Here's the bigger issue. Is $360,000 really enough? I don't know if I know any physician family for whom that is enough insurance. Would I still buy some insurance? Probably. But I can't imagine you need less than a million if you need insurance.

Should I Reinvest Dividends in Taxable?

Q. “I just started investing in a taxable account after maxing out my tax-deferred accounts. I read on the blog that if we set the dividend to be reinvested, that can create tax pain. Sounds like you receive your dividends, then reinvest them all together along with additional savings from earned income once a month. Could you please elaborate or do a deep dive on this topic and how to avoid the tax pain? I invest in Vanguard ETFs (VTI, VOO, VXUS) and aim to keep things as simple as possible.”

A. It's not THAT painful. You pay the same amount of tax either way, and if you reinvest, the brokerage will keep track of the tax lots. You'll just have a whole bunch of tiny tax lots bought with reinvested dividends to deal with when selling shares or tax-loss harvesting. I also find rebalancing as I go along easier if I'm not reinvesting dividends in taxable. I do reinvest them in tax-protected accounts, though.

This post is for you: 12 Rules for Simplicity in Your Taxable Investing Account

How Can I Estimate My Retirement Nest Egg?

Q. “I really enjoyed the post about your family's spending. Great post! It’s actually really helpful when you share these types of details and open up this way, as it’s helpful to see how others compare and what that could mean financially. The post was very timely as we did the same for our family recently as lifestyle creep is clearly happening within our family, and it looks quite similar to your monthly spending. I calculate between monthly spending and other ongoing expenses today, we have an annual spend of $275,000. I removed the obvious child-related expenses but left in the monthly credit card expenses that include our two kids for simplicity (dining, travel, clothes, etc). Similar to you, we spend a lot on travel and it’s a big bucket.

I’m curious how you would use that number to estimate your retirement nest egg target, assuming you keep the same lifestyle? Would you simply take that number, add taxes, and use 4%? I ask as for me that would be about $10 million, which seems pretty high. We took the Fire Your Financial Advisor online course already for making our own financial plan and, back then, estimated a nest egg of $4 million so I think our target is now completely off and would like to re-estimate it!”

A. Certainly a quick and dirty way to estimate your needed nest egg is to take your spending (including taxes) and divide by 4%—$10 million sounds about right to me!

But you have to also keep in mind the good news of physician retirement. Think of all the expenses that go away when you retire. For example:

- Retirement savings

- College savings

- Kid-related expenses (hopefully)

- Payroll taxes

- A large chunk of your income taxes

- Commuting expenses

- Work expenses

- Disability insurance

- Life insurance

- Mortgage (hopefully)

See what I mean? You're spending a lot of money right now on expenses you won't have in retirement. Now, you may have to add some more back in (travel expenses? health insurance costs?), but most docs who do this exercise in mid-career realize that they only need to replace 25%-50% of their pre-retirement income to maintain their lifestyle.

This post is for you: The Good and Bad News of Physician Retirement

Why Didn't You Include Such and Such in Your Recent Post?

Q. “I have a small and largely off-topic quibble with the prologue of your recent post on insurance.

I suggest you delete the inclusion of annuities in your list. Why not keep the otherwise excellent article just about insurance? Certainly fixed index (aka equity-indexed) annuities and high cost variable annuities (VA) should be avoided, but this is not necessarily true for all annuities. Single premium immediate annuities (SPIA) and multi-year guaranteed annuities (MYGA) can be a useful low-cost option in the withdrawal phase. A 1031 exchange of a bad insurance product into a low cost VA may be preferable to a taxable cash withdrawal. If you feel you want to address the issue, specifically, just add fixed index and variable annuities to the list.

A similar question came in a few days ago, and I actually get them all the time as emails or comments on posts. Not every post, but a large number of them.

Q. “I’m surprised you didn’t mention the PSLF limited waiver that is currently open in your recent post. A mistake I made 13 years ago (and didn’t realize until recently) is that I would be eligible for this program being in academics. I only had $40,000 in loans being an MD/Ph.D., and most of that has been paid off by the NIH LRP. However, I am no longer eligible for that because I take private funding toward my lab (stupid rule IMO). Anyway, I have $14,000 left, and I think this waiver applies to me and others in the wrong payment plan. To quote a recent email from the US Department of Education, ‘The waiver cuts red tape in helpful ways. Any period where you made payments while working in public service will count toward PSLF. Right now, for example, it doesn’t matter whether you were late on a payment or on the wrong repayment plan.'”

This was a comment on a post written years ago (before the limited waiver came out last year) and republished recently with a few updates.

A. I don't have a problem with some uses of whole life or VULs either. But the article isn't about them any more than it is about annuities. As a general rule, all of those are products made to be bought, not sold. But if you go to the links in the article to those words, you'll get more information. If I put “all the information” in every article so that no one ever has a quibble with them, all the articles will be 10,000 words long and no one will ever read any of them.

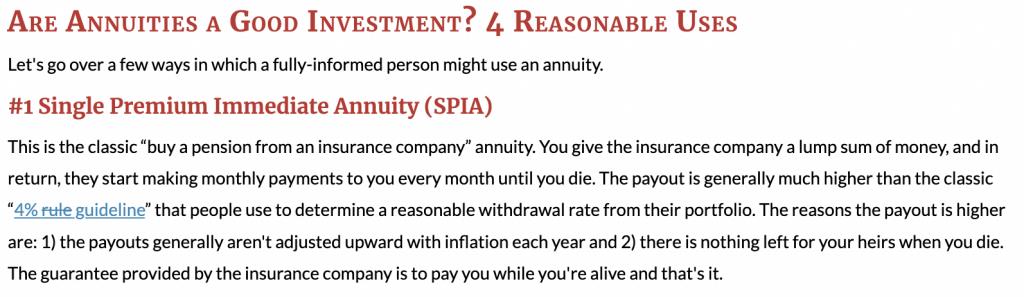

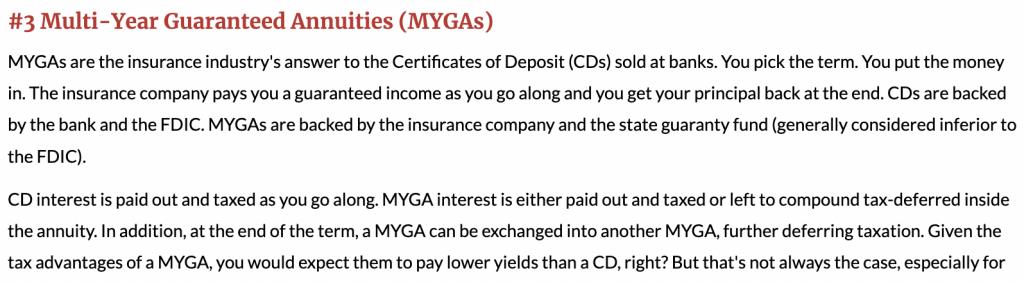

Let me demonstrate how additional information can be found at the links. The word annuities in the article links to my Annuities 101 post, which covers both SPIAs and MYGAs along with some other acceptable uses of annuities. It looks like this:

and . . .

We spend a lot of effort adding links to articles. It does help with Search Engine Optimization (SEO), but mostly I do it to help you, dear reader. If you want more information on a particular topic, try the link! I do appreciate criticism like this, as I do sometimes change an article due to it. But the change is usually to add a link.

For the second question about the limited waiver, I gave this answer.

A. I get that criticism a lot. “Why didn’t you mention such and such in your post?” despite the fact that I have entire posts elsewhere on the website dedicated to such and such. If I included everything in every post, all of the posts on the website would be 10,000+ words long and no one would read any of them.

At any rate, the limited waiver ended on October 31, 2022. One can read more about it in our recent article on the PSLF Limited Waiver. We did add that link to the article in two different places.

Bottom line: Read the links; they're there for a reason. And if you think we should add more info to a post, please let us know. We've probably already published an article providing that info and will add a link in the post.

I hope you enjoyed a Monday morning journey through my new, right-sized email box!

What do you think? Did I get all the answers right? How would you have answered? Comment below!

The post Peering into My Email Inbox on a Monday Morning appeared first on The White Coat Investor - Investing & Personal Finance for Doctors.

||

----------------------------

By: The White Coat Investor

Title: Peering into My Email Inbox on a Monday Morning

Sourced From: www.whitecoatinvestor.com/peering-into-my-email-inbox-on-a-monday-morning/

Published Date: Mon, 30 Jan 2023 07:31:18 +0000

Read More

.png) InvestingStocksToolsClubsVideosPrivacy PolicyTerms And Conditions

InvestingStocksToolsClubsVideosPrivacy PolicyTerms And Conditions