<iframe style="width:120px;height:240px;" marginwidth="0" marginheight="0" scrolling="no" frameborder="0" src="//ws-na.amazon-adsystem.com/widgets/q?ServiceVersion=20070822&OneJS=1&Operation=GetAdHtml&MarketPlace=US&source=ss&ref=as_ss_li_til&ad_type=product_link&tracking_id=peaceinvesting-20&language=en_US&marketplace=amazon®ion=US&placement=0060555661&asins=0060555661&linkId=80f8e3b229e4b6fdde8abb238ddd5f6e&show_border=true&link_opens_in_new_window=true"></iframe>|<iframe style="width:120px;height:240px;" marginwidth="0" marginheight="0" scrolling="no" frameborder="0" src="//ws-na.amazon-adsystem.com/widgets/q?ServiceVersion=20070822&OneJS=1&Operation=GetAdHtml&MarketPlace=US&source=ss&ref=as_ss_li_til&ad_type=product_link&tracking_id=peaceinvesting-20&language=en_US&marketplace=amazon®ion=US&placement=1119404509&asins=1119404509&linkId=0beba130446bb217ea2d9cfdcf3b846b&show_border=true&link_opens_in_new_window=true"></iframe>|<iframe style="width:120px;height:240px;" marginwidth="0" marginheight="0" scrolling="no" frameborder="0" src="//ws-na.amazon-adsystem.com/widgets/q?ServiceVersion=20070822&OneJS=1&Operation=GetAdHtml&MarketPlace=US&source=ss&ref=as_ss_li_til&ad_type=product_link&tracking_id=peaceinvesting-20&language=en_US&marketplace=amazon®ion=US&placement=1119376629&asins=1119376629&linkId=2f1e6ff64e783437104d091faaedfec7&show_border=true&link_opens_in_new_window=true"></iframe>

By Dr. Jim Dahle, WCI Founder

Contribution limits for 401(k)s, 403(b)s, 457(b)s, IRAs, Roth IRAs, HSAs, FSAs, SIMPLE IRAs, and SEP-IRAs are all indexed to inflation. While the retirement contribution limits do not go up every year and while every account does not use the same formula for when there will be an increase, you will generally see an increased contribution every year or two.

Inflation exploded in 2022, all the way up to 9.1% in July, and as a result, the 2023 contribution limits for many of these accounts were increased in a relatively significant way. But inflation has been tamed—at least somewhat—in 2023, and as a result, the increases in those limits for 2024 aren't quite as extravagant. If you know the latest inflation numbers, it is possible to calculate the increase even before the IRS announces it in October or November (in 2022, the IRS officially released those figures in late October).

Note that the Secure Act 2.0 passed in 2022 will eventually change catch-up contributions in significant ways. The 401(k)/403(b) catch-up for those 50+ has always been indexed to inflation. But originally the law stated that, starting in 2024, if you have a Modified Adjusted Gross Income of $145,000+ (indexed to inflation), those catch-up contributions would now have to come on the Roth side. That means tax-deferred catch-up contributions would no longer be allowed for these high earners.

In August 2023, though, the IRS announced that it was pushing back that provision until 2026. That means for the next few years, your catch-up contributions can come either via the traditional method or via Roth.

Also remember that in 2025, catch-up contributions will be increased even more for those who are 60-63 years old (it'll be the larger of $10,000 or 50% more than the regular catch-up contributions).

For now, people can make their own calculations for what the 2024 retirement plan contributions will be (we've made our best guess at the catch-up contributions). We'll update them if they change when the IRS makes it official in the final few months of 2023.

2024 401(k) and 403(b) Employee Contribution Limit

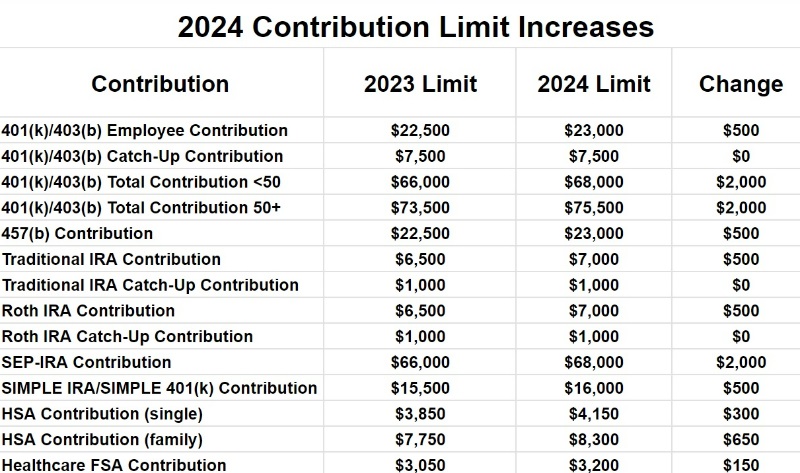

The total employee contribution limit to all 401(k) and 403(b) plans for those under 50 will be going up from $22,500 in 2023 to $23,000 in 2024 (compare that to the $2,000 it increased from 2022 to 2023). The catch-up contribution limit will remain at $7,500, so if you're 50+, your 401(k) employee contribution limit should be $30,500 in 2023.

2024 401(k)/403(b)/401(a) Total Contribution Limit

The total of all employee and employer contributions per employer will increase from $66,000 in 2023 to $68,000 in 2024 for those under 50. Since the catch-up has stayed at $7,500, the total contribution for those 50+ will be $75,500.

Note that the 401(a) limit is separate from the 403(b) limit. So, you could theoretically get $68,000 into each of them.

2024 457(b) Contribution Limit

457(b) contribution limits will increase from $22,500 to $23,000 in 2024. 457(b)s have unique catch-up contribution rules, so consult with your plan administrator if you are interested in putting more in your 457(b).

2024 Traditional and Roth IRA Contribution Limits

IRA contribution limits and catch-up contributions will increase from $6,500 ($7,500 if you're 50+) in 2023 to $7,000 ($8,000 if you're 50+) in 2024.

2024 SEP-IRA Contribution Limits

SEP-IRA contribution limits will increase to $68,000 per year for 2024, up from $66,000 in 2023.

2024 SIMPLE IRA and SIMPLE 401(k) Contribution Limits

The SIMPLE IRA and SIMPLE 401(k) contribution limits will increase from $15,500 in 2023 to $16,000 in 2024.

2024 Health Savings Account (HSA) Contribution Limits

For single people, the HSA contribution limit will increase from $3,850 in 2023 to $4,150 in 2024. Family coverage will increase from $7,750 to $8,300.

2024 Flexible Savings Account (FSA) Contribution Limits

Healthcare FSA contribution limits will increase from $3,050 in 2023 to $3,200 in 2024. Note that there are other types of FSAs (such as dependent care FSAs) with different limits.

Other Interesting Increases

The 401(a) compensation limit (the amount of earned income that can be used to calculate retirement account contributions) will increase from $330,000 in 2023 to $340,000 in 2024. This is always 5X the maximum 401(k) plan total contribution limit.

The deductibility phaseout for IRA contributions for those with a retirement plan at work should increase from $73,000-$83,000 in 2023 for singles to $77,000-$87,000 in 2024, and it'll move from $116,000-$136,00 in 2023 for those Married Filing Jointly to $123,000-$143,000 in 2024.

The Roth IRA Direct Contribution Limit phaseout will increase from $138,000-$153,000 in 2023 for singles to $146,000-$161,000 in 2024 and from $218,000-$228,000 for 2023 for those Married Filing Jointly to $230,000-$240,000 in 2024. If your MAGI is above that, you'll need to contribute indirectly via the Backdoor Roth IRA process.

While Social Security benefits increased by 8.7% for 2023, it's estimated that the bump for 2024 will be much more modest—probably somewhere around 3%. If you were a top earner for your career and qualified for the top benefit level, you received $4,559 per month in 2023 (meaning that if that 3% increase actually happens, you'd earn about $4,696 per month in 2024).

The definition of a highly compensated employee was $150,000 in 2023, but it's unclear exactly what that will be in 2024.

While it feels like all of these are increases, they are really just keeping up with inflation. They're just cost of living increases. On a real (after-inflation) basis, they're basically the same as this year.

What do you think? Are you surprised by any of these? Are you glad they're indexed to inflation? Comment below!

The post The 2024 Retirement Plan Contribution Limits appeared first on The White Coat Investor - Investing & Personal Finance for Doctors.

||

----------------------------

By: Josh Katzowitz

Title: The 2024 Retirement Plan Contribution Limits

Sourced From: www.whitecoatinvestor.com/retirement-plan-contribution-limits/

Published Date: Fri, 15 Sep 2023 06:30:09 +0000

Read More

.png) InvestingStocksToolsClubsVideosPrivacy PolicyTerms And Conditions

InvestingStocksToolsClubsVideosPrivacy PolicyTerms And Conditions