<iframe style="width:120px;height:240px;" marginwidth="0" marginheight="0" scrolling="no" frameborder="0" src="//ws-na.amazon-adsystem.com/widgets/q?ServiceVersion=20070822&OneJS=1&Operation=GetAdHtml&MarketPlace=US&source=ss&ref=as_ss_li_til&ad_type=product_link&tracking_id=peaceinvesting-20&language=en_US&marketplace=amazon®ion=US&placement=0060555661&asins=0060555661&linkId=80f8e3b229e4b6fdde8abb238ddd5f6e&show_border=true&link_opens_in_new_window=true"></iframe>|<iframe style="width:120px;height:240px;" marginwidth="0" marginheight="0" scrolling="no" frameborder="0" src="//ws-na.amazon-adsystem.com/widgets/q?ServiceVersion=20070822&OneJS=1&Operation=GetAdHtml&MarketPlace=US&source=ss&ref=as_ss_li_til&ad_type=product_link&tracking_id=peaceinvesting-20&language=en_US&marketplace=amazon®ion=US&placement=1119404509&asins=1119404509&linkId=0beba130446bb217ea2d9cfdcf3b846b&show_border=true&link_opens_in_new_window=true"></iframe>|<iframe style="width:120px;height:240px;" marginwidth="0" marginheight="0" scrolling="no" frameborder="0" src="//ws-na.amazon-adsystem.com/widgets/q?ServiceVersion=20070822&OneJS=1&Operation=GetAdHtml&MarketPlace=US&source=ss&ref=as_ss_li_til&ad_type=product_link&tracking_id=peaceinvesting-20&language=en_US&marketplace=amazon®ion=US&placement=1119376629&asins=1119376629&linkId=2f1e6ff64e783437104d091faaedfec7&show_border=true&link_opens_in_new_window=true"></iframe>

By Dr. Jim Dahle, WCI Founder

Disability insurance protects the most valuable asset of a young physician or dentist—their ability to earn money. Disability insurance is generally sold with numerous riders—some of which are “mandatory,” some of which are optional, and some of which are nonsensical.

For many years, I have recommended that doctors who have not yet reached their peak earning years include a rider that allows them to increase the benefit amount of their disability insurance without having to go through another medical underwriting. This way, even if they develop a new medical condition or take up a risky hobby, they can get a level of insurance that is appropriate for them as attending physicians. I have generally recommended this to medical students, residents, fellows, pre-partners, military docs, and others who expect their income to go up dramatically in the next few years. If they do not develop any new medical conditions, they have the option to exercise this rider or just purchase an additional policy, but if they do develop a new condition, at least they can get some increased coverage.

A typical example might be a resident who buys a policy with a $5,000-$7,500 benefit but with a rider that allows for another $5,000-$22,500 to be purchased once they become an attending with a higher income.

It turns out, however, that not all of these riders are the same. Each company and sometimes multiple policies available from the same company have different available riders. As usual, disability insurance contracts are complicated, and the devil is in the details. You need to understand what you're buying and make sure you're buying the best policy for your age, gender, specialty, state, and medical conditions—including the best combination of riders for your needs.

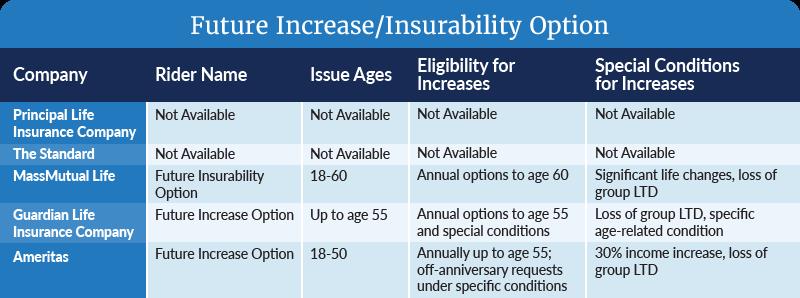

Disability Insurance Future Increase Option

Some companies call this rider a “Future Increase Option” or “Future Insurability Option” (FIO). FIO is always a rider for which you pay extra. It allows you to increase your benefit amount EVERY year up to a certain limit. You are in control of whether you exercise this option. It doesn't go away and just because you didn't use it at all last year doesn't mean you can't purchase the maximum amount of coverage this year, assuming your income justifies it. There is usually a minimum increase (maybe a $1,000 per month increase) in benefit if you want to exercise the rider at all, but that's rarely seen as any sort of a limitation by the docs exercising these options.

Another key benefit of a FIO rider is that even if you change professions to something that is riskier (a change from psychiatry to surgery, for instance), you can still exercise the rider and the entire policy will protect your surgeon's income.

The main downside of FIO riders is that they are an expense. You have to pay for them. That means if you never use them, you were paying for insurance you never needed. Some insurance companies don't offer these riders either.

More information here:

People Aren’t Buying Disability Insurance, But They Should

How Much Disability Insurance Should You Buy?

A Pain in the Butt – My Dental Disability Story

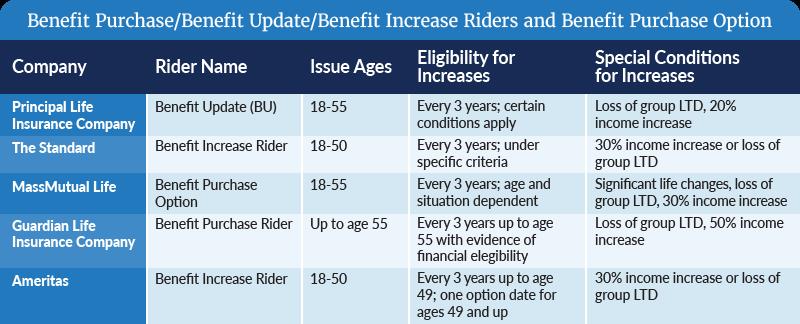

Disability Insurance Benefit Update Rider

Other companies offer a similar rider called a Benefit Update Rider (BUR), Benefit Purchase Rider (BPR), or a Benefit Purchase Option (BPO). These riders are generally offered for free as part of your policy, but like most things in life, you get what you pay for. BUR/BPR/BPO riders are generally not as good for you as an FIO rider.

Just like with an FIO rider, you can exercise these riders without undergoing medical underwriting, but that's where the similarity ends. Instead of having the ability to exercise these riders at your convenience as frequently as every year, you MUST exercise them on the company's schedule—typically every three years—or you lose the ability to exercise them at all. Even if you forget to “check in” with the company by doing the paperwork (application and financial information) and even if those financials wouldn't have allowed you to get an increase at that time, you lose the ability to do an increase in three more years. And if you don't accept an offered increase, you may lose the rider entirely. This is a serious risk. Over time, most of these riders “fall off” the policies as the busy doctors forget about them and the agents fail to remind the doctors or can't get in touch with them.

In addition, BUR/BPR/BPO riders may require you to go through underwriting. Not health underwriting, but occupational underwriting. If you've changed occupations or they've changed the occupation class for your specialty since you bought your policy three years ago, you may find yourself facing a large increase in the cost of the policy. The insurance bought with any of these riders is going to be more expensive than the original policy because you're older, but with the FIO rider, at least the insurance company will still look at you as being in your original occupation.

While details like these change frequently (so double-check with your agent), Guardian, Mass Mutual, and Standard are the companies most likely to do occupational underwriting. If you change specialties after taking out a DI policy and you have a Benefit Purchase Rider (or one like it) with MassMutual, Guardian, and Standard, your occupation class on the increase could change for better or worse depending on the current carrier occupation guidelines. However, if you have the Future Increase or Insurability Option with MassMutual or Guardian or the Benefit Update rider with Ameritas or Principal, your occupation class won’t get any worse.

The main benefit of a BUR/BPR/BPO rider is the lower cost, i.e. no additional cost. But you truly get what you pay for. Just to keep things complicated, however, there are a couple of minor advantages to BUR/BPR/BPO riders over FIO riders. Some companies allow a graduating resident or fellow to immediately exercise this option upon graduation rather than waiting for the three-year mark. That's pretty nice since that's the main time these riders need to be used. The total amount of possible increased coverage may also be higher. Rather than being limited to just another $5,000 or $15,000, you can generally eventually increase the amount to as high as that insurance company will allow. This could be a higher potential increase than under an FIO rider.

As a general rule, if you're buying a policy as a resident or fellow (as you should), you definitely want to buy a policy with one of these types of riders. Both will allow you to increase your coverage as your income increases. However, there are significant differences between the two which should be considered when comparing and contrasting all of the features of all available policies.

As a general rule, a FIO rider is going to be more flexible but cost more. A BUR/BPR/BPO rider is going to be much less flexible and require more effort on your part, but it will be cheaper and it may even permit a greater increase in coverage. Choose wisely, and if you go with a policy with a BUR/BPR/BPO, make sure you set a reminder in your phone to actually exercise it.

What do you think? Which type of rider does your policy have? Would you choose differently if you had to do it again? Have you exercised an increase rider? How did it go? Comment below!

The post Disability Insurance Increase Riders: What’s the Difference? appeared first on The White Coat Investor - Investing & Personal Finance for Doctors.

||

----------------------------

By: The White Coat Investor

Title: Disability Insurance Increase Riders: What’s the Difference?

Sourced From: www.whitecoatinvestor.com/disability-insurance-increase-riders/

Published Date: Sat, 16 Mar 2024 06:30:53 +0000

Read More

Did you miss our previous article...

https://peaceofmindinvesting.com/investing/what-its-like-to-be-a-military-doctor-and-is-it-the-right-path-for-you

.png) InvestingStocksToolsClubsVideosPrivacy PolicyTerms And Conditions

InvestingStocksToolsClubsVideosPrivacy PolicyTerms And Conditions