<iframe style="width:120px;height:240px;" marginwidth="0" marginheight="0" scrolling="no" frameborder="0" src="//ws-na.amazon-adsystem.com/widgets/q?ServiceVersion=20070822&OneJS=1&Operation=GetAdHtml&MarketPlace=US&source=ss&ref=as_ss_li_til&ad_type=product_link&tracking_id=peaceinvesting-20&language=en_US&marketplace=amazon®ion=US&placement=0060555661&asins=0060555661&linkId=80f8e3b229e4b6fdde8abb238ddd5f6e&show_border=true&link_opens_in_new_window=true"></iframe>|<iframe style="width:120px;height:240px;" marginwidth="0" marginheight="0" scrolling="no" frameborder="0" src="//ws-na.amazon-adsystem.com/widgets/q?ServiceVersion=20070822&OneJS=1&Operation=GetAdHtml&MarketPlace=US&source=ss&ref=as_ss_li_til&ad_type=product_link&tracking_id=peaceinvesting-20&language=en_US&marketplace=amazon®ion=US&placement=1119404509&asins=1119404509&linkId=0beba130446bb217ea2d9cfdcf3b846b&show_border=true&link_opens_in_new_window=true"></iframe>|<iframe style="width:120px;height:240px;" marginwidth="0" marginheight="0" scrolling="no" frameborder="0" src="//ws-na.amazon-adsystem.com/widgets/q?ServiceVersion=20070822&OneJS=1&Operation=GetAdHtml&MarketPlace=US&source=ss&ref=as_ss_li_til&ad_type=product_link&tracking_id=peaceinvesting-20&language=en_US&marketplace=amazon®ion=US&placement=1119376629&asins=1119376629&linkId=2f1e6ff64e783437104d091faaedfec7&show_border=true&link_opens_in_new_window=true"></iframe>

By Dr. James M. Dahle, WCI Founder

Today's post sprung out of one of those ideas that came to me at 4am in that state between sleep and wakefulness. Now, as I write the actual post in the light of day, the whole idea seems a little silly. Let's go with it anyway and see what we can learn from it. If nothing else, I suspect the exercise will illustrate many of the problems with “investing” in whole life insurance. So, if you've ever considered the idea of investing in real estate vs. whole life insurance, this post is for you.

Investment Returns

Perhaps the biggest difference between these two investments is the returns. Insurance agents will balk at my even calling whole life insurance an investment, and I agree with them. But they're usually talking out of both sides of their mouth on this point. First, they'll say, “It's not an investment,” and a few minutes later, they'll encourage you to use it for your retirement savings. Guess what? That's an investment.

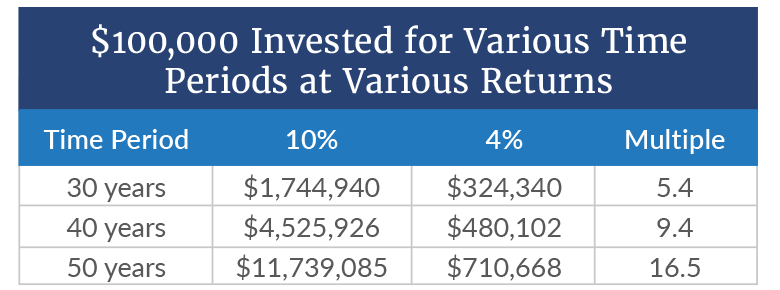

At any rate, expected long-term returns on well-managed real estate investments are usually in the 8%-15% range. Guaranteed returns on a well-designed whole life policy held for decades until death are about 2%, and projected returns are currently about 5%. In my experience, the actual return usually comes in between those numbers, perhaps 3%-4% per year. Obviously, there are bad real estate investments and poorly designed whole life insurance policies that have worse returns, so I'm only comparing good against good here. But what does making 10% vs. making 4% mean over the 40 or 50 years you might own a long-term investment? Let's take a look.

Consider investing $100,000 at 10% vs. 4% over 30-, 40-, and 50-year time periods.

These are not trivial differences. We're not talking about 50% more money. We're talking about having 500% or 1,650% more money! Obviously, you're taking more risk with real estate, but over 50 years, are you really? What are the odds that your return is really going to be less than 4% over 50 years? You'll probably get close to that out of appreciation alone without any leverage or income. There are going to have to be A LOT of other advantages somewhere else to make up for this huge disadvantage.

Both types of investments suffer from poor short-term returns. A typical whole life policy has a -30% return in its first year. Likewise, the high transaction costs on real estate usually result in a negative return if you sell within the first few years.

More information here:

16 Different Ways to Invest in Real Estate

Taxability of Income

Both real estate and whole life insurance can provide income to you. In the early years of a whole life policy, the dividend is usually less than the premiums you are still paying. But eventually, it will hopefully be more than the premiums or you will have the policy paid up such that you are no longer paying premiums. Whole life dividends are technically a return of premium paid, so there is no tax due on them. You can argue whether that's income or not, but it is certainly tax-free.

Rental income is taxed at your ordinary income tax rates. However, with a typical real estate equity investment, at least for the first few years, the rental income is generally covered by depreciation. So, it also comes to you tax-free. When that stops being the case, many real estate investors simply exchange their equity tax-free into a larger property and continue the process. If you ever sell the property, that depreciation is recaptured, but only at a maximum of 25%. You'll still have benefitted from the time value of money during that time period.

Taxability of Exit

If you decide you want out of one of these investments before you die, there can be significant taxes. If you sell your equity real estate investment, all depreciation you've taken will be recaptured at up to 25%, and you will pay long term capital gains rates on any gains. With whole life insurance, you will pay ordinary income tax rates on any cash value that is more than the sum of premiums paid. Any tax losses you may have from tax-loss harvesting can be used to offset capital gains but not gains from the sale of whole life insurance.

More information here:

10 Tax Loopholes for Real Estate Investors

Exchanges

However, you do not have to sell either asset. You can exchange them. A 1031 exchange allows you to swap your real estate for similar real estate (and “similar” has a pretty broad definition) within 60 days of the sale and avoid paying capital gains taxes or depreciation-recapture taxes. A 1035 exchange allows you to swap the cash value of your whole life insurance policy into another cash value life insurance policy, an annuity, or even a long-term care policy, all tax-free.

Tax-Free at Death

Both assets pass to your heirs income tax-free. Real estate passes tax-free by virtue of the step up in basis at death. Whole life insurance passes tax-free by virtue of the fact that life insurance death benefits are not taxable. Remember that with whole life that there is only one pot of money, not two. Whatever cash value you borrowed against the policy is subtracted from the death benefit before it is paid out.

Retirement Accounts

While neither investment is available in most standard retirement accounts, real estate can be placed into self-directed IRAs and 401(k)s with the attendant tax, estate planning, and asset protection benefits. Life insurance cannot.

Ability to Borrow Against the Asset

You can borrow against either asset tax-free but not interest-free. The terms to borrow against your whole life insurance policy are fixed (and guaranteed) when the policy is signed, but they are generally not favorable. The terms to borrow against your real estate are neither fixed nor guaranteed, but you can also generally get better terms. One unique aspect of non-direct recognition whole life insurance policies is that the dividend is not decreased even if you borrow out a large portion of the cash value.

Death Benefit

Whole life insurance provides a death benefit, no matter when you die. Real estate does not. That means that in the event of an early death, the “return” on a whole life insurance policy will be dramatically higher than that of a real estate investment. Of course, this advantage can be relatively offset by using inexpensive term life insurance.

Asset Protection

Some states (about half of them) provide excellent asset protection for the cash value of a whole life insurance policy. In the event of bankruptcy, you often get to keep the entire cash value and stiff your creditors. Real estate, at least real estate outside of retirement accounts (which provide even better asset protection than whole life insurance), has more limited asset protection options. Placing it into a multi-member Limited Liability Company (LLC) will often limit creditors to a charging order and force a settlement, providing some limited external liability protection. Obviously, real estate is a far more toxic asset than life insurance, and it can create its own internal liability. The LLC can help protect your other assets from that, but the entire value of the property (and anything else in that LLC) will be subject to creditors.

Estate Planning

Whole life insurance is a far easier way to pass wealth to the next generation than real estate, although its lower returns usually mean you're passing less wealth to them. Life insurance death benefits do not pass through probate, and the asset is easily placed into an irrevocable trust where any growth is not subject to estate taxes. Real estate can also be put into an irrevocable trust, but there will be more hassle and taxes due. Using a revocable trust, a family-limited partnership, or even an LLC can help avoid probate—just be careful not to lose that valuable step up in basis at death just to avoid probate. Whole life insurance is also obviously a lot more liquid at death, which can help pay any estate taxes that may be due.

Ability to Add Value

Many real estate investors love the fact that their expertise and hard work can boost their returns and add value to their investments. Naturally, if you are lazy and suck at real estate, you can also subtract value. You're not going to add or subtract any value to your whole life insurance policy no matter how hard you work at it.

Hassle Factor

While good systems and good managers can reduce hassle, there's no doubt that real estate investing involves far more hassles than a one-time purchase of a whole life insurance policy. However, do not minimize the difficulty and hassle of managing a whole life insurance policy properly during the withdrawal phase. While much less of an issue with a whole life policy than the various types of universal or variable life policies, you don't want to turn it into a Modified Endowment Contract (MEC) and turn those loans into taxable income.

Hype and Scam Potential

One of the worst parts of both of these investments is the hype that surrounds them. High commissions cause unscrupulous and uneducated insurance agents to push lousy whole life policies for lousy reasons. If they can't sell it to you for asset protection or estate planning, they'll try to sell it to you for retirement income, paying for college, or as a tax-reduction scheme. Many doctors fall prey to these sales tactics. They're not technically a scam (if you read the contract, it'll tell you exactly what's going to happen with this policy), but you might still feel bamboozled.

Real estate investing has almost as much hype surrounding it as multi-level marketing schemes. Books, courses, and seminars are filled with rah-rah-rah motivational material. You should ask yourself why it takes so much motivation to be successful if real estate is such an easy, guaranteed path to wealth. The answer is that it isn't. It's hard work and certainly not guaranteed.

To make matters worse, there are outright scams out there. Real estate education is full of them. One well-known course charges $0 for the first session, $400 for the second session, and $5,000 for the third session. And that's downright cheap compared to many courses and coaching programs. What many beginners don't realize is that all that information is available on the internet and at their public library for free if they're willing to spend the time going to get it. In addition to the education process, there are plenty of downright bad deals out there and incompetent and unethical players in the space. Caveat emptor!

That's why The White Coat Investor's newest course, No Hype Real Estate, is so effective. We're not hyping real estate at all. Instead, we give you the basic knowledge you need to decide whether real estate is the right investment for you. In fact, we've worked so hard on this course that it gives you more than a dozen instructors and 25 hours of content. If you’re interested in real estate investing, you can’t afford to miss the No Hype Real Estate Investing course.

More information here:

Is Whole Life Insurance a Scam?

Summing It Up

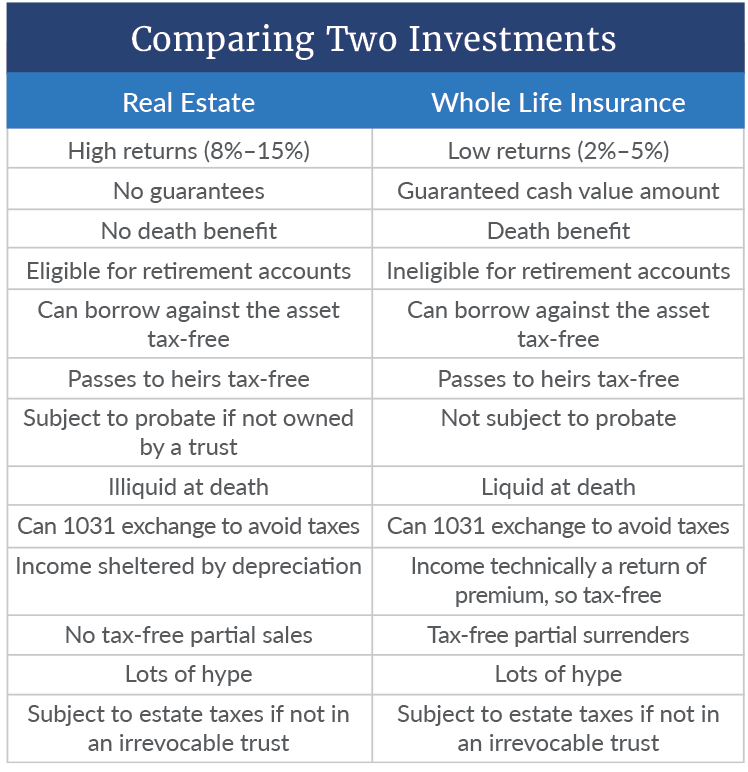

Let's take a look at a summary of the advantages and disadvantages of each of these investments.

As you can see, each asset has its advantages and disadvantages. But over a time horizon of 30-50 years, the advantages of whole life insurance simply cannot overcome the high returns available with a decent real estate investment. That's why 20% of my portfolio is in real estate, and 0% of it is in whole life insurance.

If you would like to learn more about real estate investing opportunities, we recommend you sign up for our free real estate newsletter to learn about various private real estate syndications and funds, including most of those I invest in.

Featured Real Estate Partners

Origin Investments

Type of Offering:

Fund

Primary Focus:

Multi-Family

Minimum Investment:

$50,000

Year Founded:

2007

The Peak Group

Type of Offering:

REIT

Primary Focus:

Single Family

Minimum Investment:

$25,000

Year Founded:

2000

37th Parallel

Type of Offering:

Fund / Syndication

Primary Focus:

Multi-Family

Minimum Investment:

$100,000

Year Founded:

2008

RealtyMogul

Type of Offering:

Platform / REIT

Primary Focus:

Multi-Family

Minimum Investment:

$5,000

Year Founded:

2012

DLP Capital

Type of Offering:

Fund

Primary Focus:

Multi-Family

Minimum Investment:

$200,000

Year Founded:

2008

MLG Capital

Type of Offering:

Fund

Primary Focus:

Multi-Family

Minimum Investment:

$50,000

Year Founded:

1987

JAX Wealth Investments

Type of Offering:

Fund / Turnkey

Primary Focus:

Single Family

Minimum Investment:

$100,000

Year Founded:

2017

Wellings Capital

Type of Offering:

Fund

Primary Focus:

Self-Storage / Mobile Homes

Minimum Investment:

$50,000

Year Founded:

2014

* Please consider this an introduction to these companies and not a recommendation. You should do your own due diligence on any investment before investing. Most of these opportunities require accredited investor status.

What do you think? Do you invest in real estate, whole life insurance, both, or neither and why? Comment below!

The post Should I Invest in Real Estate or Whole Life Insurance? appeared first on The White Coat Investor - Investing & Personal Finance for Doctors.

||

----------------------------

By: The White Coat Investor

Title: Should I Invest in Real Estate or Whole Life Insurance?

Sourced From: www.whitecoatinvestor.com/should-i-invest-in-real-estate-or-whole-life-insurance/

Published Date: Fri, 28 Oct 2022 06:30:38 +0000

Read More

.png) InvestingStocksToolsClubsVideosPrivacy PolicyTerms And Conditions

InvestingStocksToolsClubsVideosPrivacy PolicyTerms And Conditions