<iframe style="width:120px;height:240px;" marginwidth="0" marginheight="0" scrolling="no" frameborder="0" src="//ws-na.amazon-adsystem.com/widgets/q?ServiceVersion=20070822&OneJS=1&Operation=GetAdHtml&MarketPlace=US&source=ss&ref=as_ss_li_til&ad_type=product_link&tracking_id=peaceinvesting-20&language=en_US&marketplace=amazon®ion=US&placement=0060555661&asins=0060555661&linkId=80f8e3b229e4b6fdde8abb238ddd5f6e&show_border=true&link_opens_in_new_window=true"></iframe>|<iframe style="width:120px;height:240px;" marginwidth="0" marginheight="0" scrolling="no" frameborder="0" src="//ws-na.amazon-adsystem.com/widgets/q?ServiceVersion=20070822&OneJS=1&Operation=GetAdHtml&MarketPlace=US&source=ss&ref=as_ss_li_til&ad_type=product_link&tracking_id=peaceinvesting-20&language=en_US&marketplace=amazon®ion=US&placement=1119404509&asins=1119404509&linkId=0beba130446bb217ea2d9cfdcf3b846b&show_border=true&link_opens_in_new_window=true"></iframe>|<iframe style="width:120px;height:240px;" marginwidth="0" marginheight="0" scrolling="no" frameborder="0" src="//ws-na.amazon-adsystem.com/widgets/q?ServiceVersion=20070822&OneJS=1&Operation=GetAdHtml&MarketPlace=US&source=ss&ref=as_ss_li_til&ad_type=product_link&tracking_id=peaceinvesting-20&language=en_US&marketplace=amazon®ion=US&placement=1119376629&asins=1119376629&linkId=2f1e6ff64e783437104d091faaedfec7&show_border=true&link_opens_in_new_window=true"></iframe>

By Dr. James M. Dahle, WCI Founder

There is an investment truism out there that says every investment will get its day in the sun. As you build a portfolio (i.e. your investments), you want to ensure your portfolio will allow you to reach your financial goals under a wide variety of potential future outcomes. The best way to do that is to include a variety of asset classes that perform differently in various potential economic circumstances and then rebalance the portfolio periodically. This is basic Portfolio Construction 101.

When you do that, it generally means you will have at least one asset class doing well at any given time and you will have at least one asset class doing poorly at any given time. Low correlation is not the same thing as inverse correlation, as many have learned in the first half of 2022 as both their stocks and bonds cratered. Sometimes, most or all of your asset classes do go down together. But diversification between asset classes (and sub-asset classes) can help minimize the damage most of the time, decreasing volatility and increasing long-term returns.

The G Fund Gets Its Day

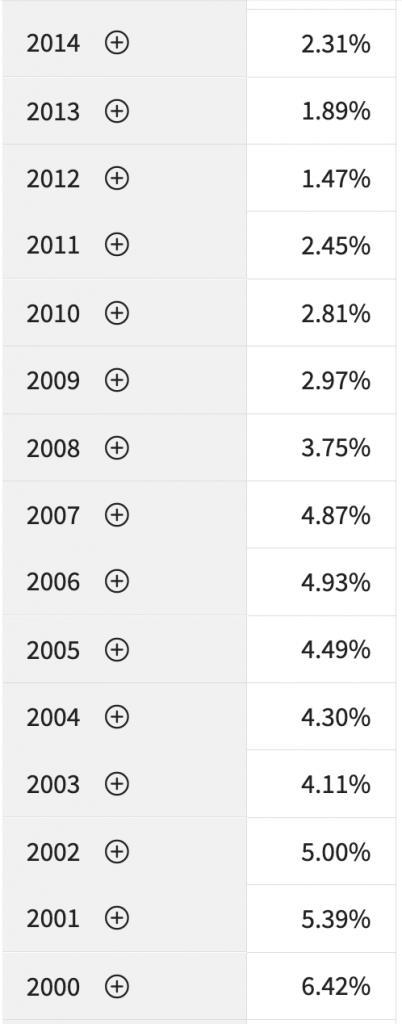

Since I went on active duty in 2006, I have had money in the G Fund of the Thrift Savings Plan (TSP). The TSP is the military/government 401(k). It has changed a bit over the years but has generally been a very good deal with low expenses and broadly diversified index funds. One of its most unique holdings is the G Fund, which provides treasury bond yields with money market risk. The yield on the G fund is an interest rate calculated once a month from the average yield of all (nominal) US treasury securities with four or more years to maturity. However, the value of the principal never goes down, so it is a very safe investment. You can't lose money with it, at least on a nominal basis.

However, since I started investing in it in 2006, it has been a pretty lousy investment. Why is that? Simply because it has not yet had its day in the sun. Low-interest rates equal low returns for the G Fund. To make matters worse, falling interest rates do not boost the value of the G Fund like they do for typical nominal bonds. In the last decade and a half, as interest rates have fallen and markets have generally performed well, the G Fund has looked pretty terrible. Take a look and you'll see what I mean:

Pretty crummy last decade, right?

But now, conditions are perfect. It's Wednesday night . . . there's nothing good on TV, and I'm wearing my business socks, etc. No, not those conditions. I'm talking about a general economic downturn combined with rising interest rates. THOSE are the conditions for which the G Fund was made. Almost everything else has done poorly in 2022. Look at the returns from the first half of 2022:

- US Stocks: -21.38%

- International Stocks: -18.16%

- Small Value Stocks: -15.48%

- REITs: -20.51%

- Long Bonds: -21.62%

- Short Bonds: -4.52%

- TIPS: -3.01%

- Gold: -1.46%

- Bitcoin: -58.81%

That's a lot of red. There's not much with positive returns in 2022. Commodities have done well. Cash has held its value (at least nominally). Real estate debt funds seem to be maintaining their yields without dramatic increases of defaults (yet.) But just about everything in your portfolio is not doing great. While private real estate seems to be hanging in there, it tends to be a bit of a lagging asset due to its illiquidity—and its day is probably coming.

But you know what's doing great? The G Fund. Not only is it in the green (+2.65%) but its yield is now up to 3.875% (while money market funds are paying about 3.5%) and is likely to rise even further as the Fed continues to raise interest rates to combat inflation.

Now, I admit it's hard to get excited about an investment like this. It's definitely not exciting. Nobody goes to cocktail parties and brags about owning shares of the G Fund. But it performs well when nothing else does. And now is that time. If you're a G Fund owner, enjoy it!

More information here:

The Thrift Savings Plan (TSP) Gets a New Look—and I Don’t Love It

Investments and Sunshine

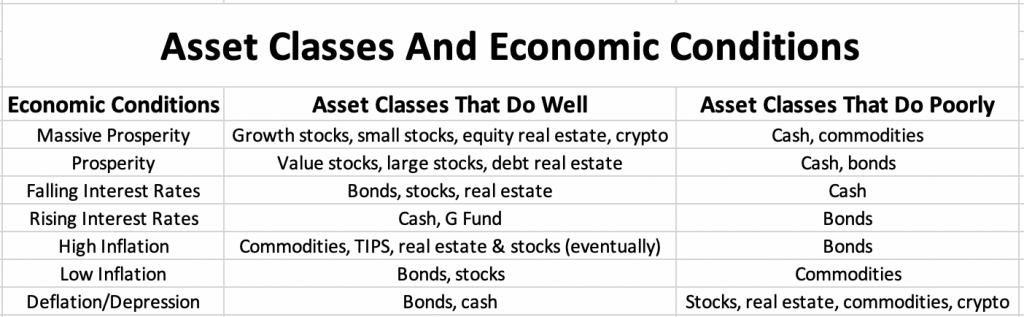

Under what types of economic conditions do the various asset classes tend to do well compared to other asset classes? Let's talk about it.

US Stocks

US stocks do best during prosperous times, especially when the dollar is strengthening. Falling/low interest rates make fixed-income investments less attractive. Thus, riskier assets, like stocks, become more attractive. Companies can also grow using borrowed money when interest rates are low.

International Stocks

International stocks also perform well in prosperous times, especially with low and/or falling interest rates. However, they do better than US stocks when the dollar is weakening. International stocks also tend to be more value-y than US stocks, so in conditions that favor value stocks over growth stocks, they also tend to do better than US stocks.

Growth, Value, Small Stocks

As a general rule, growth and small stocks do better in prosperous times, and value and large stocks do better in less prosperous (but still prosperous) times. Lots of exceptions there, though.

Equity Real Estate

Equity real estate, like stocks, benefits from prosperous times and low-interest rates. It tends to do a little bit better during inflationary times as well, especially with shorter-term tenant contracts. Owners raise rents with inflation, the value of the property increases with inflation, and the cost of its leverage (at least if it's fixed) also decreases. Equity real estate tends to do poorly with rising/high interest rates and general economic downturns as people have less money to pay rent (or to buy a property) and vacancies rise as households combine. Private real estate tends to do a little better than publicly traded real estate when the stock market is doing poorly and vice versa.

Debt Real Estate

Debt real estate is a little bit safer than equity real estate. Debt real estate seems to do best comparatively when times are OK but not awesome. The debt holder in first lien position does just fine even when the owners aren't doing that great. However, in a really terrible real estate environment, debt real estate investors become equity real estate investors as they foreclose on the properties whose loans are in default. Even if they don't foreclose, they may end up with significantly lower income as they strike deals with the owners.

Precious Metals

Gold tends to keep up with inflation in the long run, but it generally does so through sharp rises in value every few decades rather than any sort of steady rise. Meanwhile, it exhibits profound volatility. If gold isn't volatile enough for you, try silver. Historically, there are times when precious metals have done well as a “flight to safety” asset during bad economic times, but that is hardly a guarantee. We certainly haven't seen that in 2022 or 2008, although gold did great in those opening months of the pandemic in 2020.

Nominal Bonds

Bonds do particularly well in times of falling interest rates. They also often do well when stocks are doing poorly, but the correlation there is 0, not 1, so there are times when stocks and bonds go up or go down together. They are particularly good in deflationary times, such as the Great Depression. The longer the term of the bond, the better they do with falling interest rates and vice versa.

Inflation-Indexed Bonds

Inflation-indexed bonds, such as Treasury Inflation Protected Securities (TIPS), do well in times of unexpected inflation, but like all bonds, they're hurt by rising interest rates. 2022 has been an interesting case study in these interesting investments. The unexpected inflation has helped them to do much better than nominal bonds, but that hasn't been enough to overcome the effect of rapidly rising interest rates so their 2022 return has actually been negative.

Cash

Cash does particularly well in terrible economic times. It preserves its (nominal) value to cover your living expenses, and it provides the ability to purchase stocks, real estate, and other assets at a discount.

Cryptoassets

Nobody really knows when or why the value of cryptoassets goes up or down. It has been proposed that Bitcoin is digital gold, but it seems to act more like a really volatile tech stock. Low-interest rates and prosperous times do seem to lead to more people speculating in these assets, but they're really too new to say much more than that. In the past, people have argued they would do well when the dollar weakens or when inflation is high, but neither of those really turned out to be true. Their value seemed to rise just fine as the dollar was strengthening, but their performance in the first real episode of inflation in decades has been underwhelming at best.

Commodities

Commodities do best with high inflation but do not have very good long-term returns. Like gold, you expect commodities to match inflation in the long run.

More information here:

How to Build an Investment Portfolio for Long-Term Success

The Bottom Line

Let's sum up what we've learned, shall we?

As you can see, nothing does well (or poorly) in all conditions. So, make sure you include multiple asset classes (3-10) in your portfolio. For those new to the blog, you may find it useful to see our asset allocation. It's 60% stocks, 20% bonds, and 20% real estate.

- US Stocks: 25%

- Small value stocks: 15%

- International stocks: 15%

- Small international stocks: 5%

- Nominal bonds (muni bonds and the G Fund): 10%

- Inflation-linked bonds (TIPS and I Bonds): 10%

- Publicly traded REITs: 5%

- Equity real estate (private): 10%

- Debt real estate (private): 5%

Stocks, bonds, and real estate. Depending on how you count them, somewhere between 3-9 asset classes. As you can see, you don't have to invest in everything to be successful, but it's still wise to include a handful of asset classes in your portfolio. Pick something reasonable and stick with it for the long term. Eventually, every asset class in your portfolio will have its day in the sun, but you might have to wait for a while—just like I did with the G Fund.

Need to get your own financial plan in place? Check out the Fire Your Financial Advisor course! It's a step-by-step guide to creating your own path to financial freedom. Try it risk-free today!

What do you think? What asset classes are in your portfolio and why? Has 2022 given any of your asset classes their day in the sun? Comment below!

The post The G Fund (Finally) Gets Its Day in the Sun appeared first on The White Coat Investor - Investing & Personal Finance for Doctors.

||

----------------------------

By: The White Coat Investor

Title: The G Fund (Finally) Gets Its Day in the Sun

Sourced From: www.whitecoatinvestor.com/the-g-fund-finally-gets-its-day-in-the-sun/

Published Date: Fri, 09 Dec 2022 07:30:04 +0000

Read More

Did you miss our previous article...

https://peaceofmindinvesting.com/investing/how-to-hack-a-zerobased-budget-as-a-highincome-professional

.png) InvestingStocksToolsClubsVideosPrivacy PolicyTerms And Conditions

InvestingStocksToolsClubsVideosPrivacy PolicyTerms And Conditions