<iframe style="width:120px;height:240px;" marginwidth="0" marginheight="0" scrolling="no" frameborder="0" src="//ws-na.amazon-adsystem.com/widgets/q?ServiceVersion=20070822&OneJS=1&Operation=GetAdHtml&MarketPlace=US&source=ss&ref=as_ss_li_til&ad_type=product_link&tracking_id=peaceinvesting-20&language=en_US&marketplace=amazon®ion=US&placement=0060555661&asins=0060555661&linkId=80f8e3b229e4b6fdde8abb238ddd5f6e&show_border=true&link_opens_in_new_window=true"></iframe>|<iframe style="width:120px;height:240px;" marginwidth="0" marginheight="0" scrolling="no" frameborder="0" src="//ws-na.amazon-adsystem.com/widgets/q?ServiceVersion=20070822&OneJS=1&Operation=GetAdHtml&MarketPlace=US&source=ss&ref=as_ss_li_til&ad_type=product_link&tracking_id=peaceinvesting-20&language=en_US&marketplace=amazon®ion=US&placement=1119404509&asins=1119404509&linkId=0beba130446bb217ea2d9cfdcf3b846b&show_border=true&link_opens_in_new_window=true"></iframe>|<iframe style="width:120px;height:240px;" marginwidth="0" marginheight="0" scrolling="no" frameborder="0" src="//ws-na.amazon-adsystem.com/widgets/q?ServiceVersion=20070822&OneJS=1&Operation=GetAdHtml&MarketPlace=US&source=ss&ref=as_ss_li_til&ad_type=product_link&tracking_id=peaceinvesting-20&language=en_US&marketplace=amazon®ion=US&placement=1119376629&asins=1119376629&linkId=2f1e6ff64e783437104d091faaedfec7&show_border=true&link_opens_in_new_window=true"></iframe>

By Francis Bayes, WCI Columnist

For many reasons, 2022 was not kind to the wallet and the retirement prospects of average Americans. But this website is for healthcare professionals, other high-income professionals, and trainees who will most likely have (or currently have) above-national-average household incomes. The audience of this website (i.e., you) is not made up of average Americans. For you, 2022 might have been an opportunity or a relief because of your high savings rate or your large margin of safety.

Even if 2022 was a missed opportunity, we cannot change the past. Some of us were unlucky to start investing during the bubble. We can only control our financial plan at this moment. Is your financial plan prepared for another 2022? In fact, would your financial plan want 2022 rather than 2021?

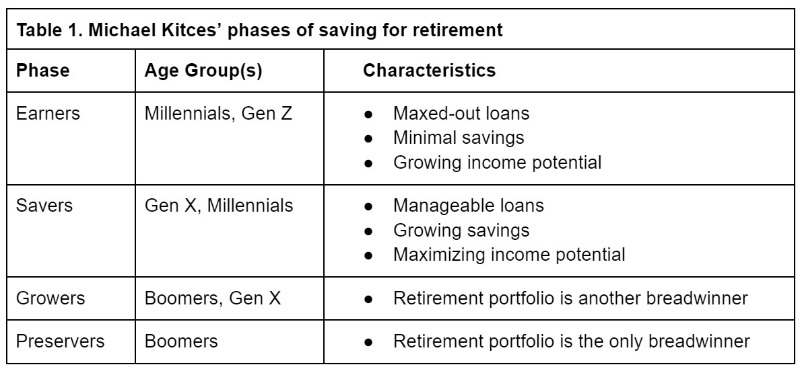

This column is my hot take for 2023: whether one is an earner, a saver, a grower, or a preserver–as per Michael Kitces’ framework (Table 1)–those who follow the basic principles of the WCI community should wish that financial markets in 2023 are like they were in 2022, not 2021.

(To be clear, I do not want inflation to rise again, another war, or even the long-expected recession. I'm talking about the markets for stocks, bonds, housing, etc. For example, we should want another 10%-20% decline in the stock market. But I would rather have the markets of 2021 if it means that inflation goes back to 2% and the war in Ukraine ends.)

For Earners and Savers: You Can Keep Buying Stocks on Sale

I can claim to be a part of both “Earners” and “Savers” thanks to my wife, who is the primary breadwinner and works as a consultant. On the surface, my wife and I lost a lot of money in 2022. In January, we lump-sum contributed to our Roth IRAs and bought broad-market stock index funds (instead of “dollar-cost averaging”). Throughout the year, we kept buying Bitcoin and Ether, although their price fell too fast for us to allocate up to 2% of our portfolio (OK, I was responsible for her losing money).

Our portfolio is 98% stocks, but we would not have fared much better even if we owned bonds. Our YTD money-weighted return was about -9% (it helped to overweight small-cap value!) The YTD return of Vanguard Target 2055 Fund, which has 91% stocks and 9% bonds, was about -14%. Nonetheless, 2022 was a great year for us because we kept buying socks on sale.

Sorry, I meant stocks. Turns out Jason Zweig is right. It sounds better if I say socks on sale.

These stonks socks stocks (i.e., broad-market index funds) should be held for at least 20 years because stocks have not had a negative return over any 20-year period. As Cullen Roche argues, when we buy stocks in our retirement accounts, we should think that we are buying a bond that matures in 20 years—i.e., a loan that will not be repaid to you for 20 years. Just like we can sell bonds on the secondary market, we can sell our stocks in our retirement accounts. But we should understand that the penalty is excessive, because the moment we sell, we are forfeiting the historical guarantee of a positive return.

If you are 30 like I am, we should not worry about the stocks that we buy today until we are 50. Of course, anything can happen, and the stock market’s undefeated streak over 20-year periods might end at one point. If our stocks are worth less than expected after 20 years, our future selves might need to worry a little. But the likelihood of such a scenario is lower if the stocks are cheaper today (i.e., valuations are lower) because lower valuations are associated with greater future returns. This means that our future selves are less likely to worry about the stocks that we bought in 2022 than those in 2021. If 2023 is like 2022 and the stocks become even cheaper, the likelihood of our future worries will further decrease.

If the stock market declines in 2023, remember that we should worry less now because we will worry less in the future.

For Savers and Growers: You Can Be Greedy While Others Are Fearful

For most people, maintaining their asset allocation throughout another year of a bear market will not be easy. If the current uptrend (as of this writing) is another “bear market rally,” their belief in stocks will further erode. The interest rates in their high-yield savings account and bond funds will be too attractive. Sales pitches about alternative investments will grow louder. But if the prices of stocks do not increase at the rate of earnings growth (i.e., valuations decrease), savers and growers might want to consider increasing their allocation to stocks.

Is this sacrilegious? In his book Rational Expectations, Dr. William Bernstein suggests that strategic asset allocation might be appropriate during bubbles and market crashes. He defines strategic asset allocation as “small, infrequent changes in allocation opposite large changes in valuation.” One does not need to change their asset allocation every year, but 2022-2023 could be a historic opportunity. In December 2022, for example, professional investors were most overweight with bonds vs. stocks since March 2009. When others are too conservative, long-term savers should be more daring with their allocation to 20-year bond-like assets such as stocks. Discussion of strategic asset allocation is beyond the scope of this column (though WCI now has a book about it), but if 2023 is more like 2022 than 2021, savers and growers can take their time to learn more about it and implement it.

For Growers and Preservers: You Can Better Match Your Liability

Dr. Anthony Ellis may disagree with me . . . but how much luckier can the Boomers get? They experienced a historic bull market (technically, we are still in a “secular bull market”) during their peak earning years. Depending on where they live, the value of their house likely soared as well. They could have ridden both waves and rectified any of their earlier mistakes.

I do not wish the inflation rate to increase again, because inflation can be devastating for “preservers.” However, preservers can now buy nominal Treasury bills and notes (not bonds!) at 4% and TIPS with positive real yields. One can buy enough Treasury bills, notes, and TIPS to survive any sequence-of-returns risk AND withdraw from their portfolio at a 4% real rate. Allan Roth demonstrates how one can create a 30-year TIPS ladder, and Big ERN declares the 4% withdrawal (guide, not rule!) to be back.

Although I do not plan on having Treasuries in my retirement portfolio for a while, I have a bit of skin in the game as my parents are near retirement. Their TreasuryDirect accounts do not own only I Bonds anymore. For their sake, I want the interest rates to continue to be higher than the rates in 2021.

Even if one wants to leave some money for their heirs (or charities), one’s strategy to match their short-term liability can be more versatile in 2022 than in 2021 because of the current interest rates. They can protect themselves from another year of unexpected inflation and still have income. They can buy three-month Treasury bills, which have higher rates than 10-year Treasury notes as of this writing; and depending on the change in interest rates, they can roll them over at higher rates or reinvest their principals in Treasuries with higher rates and longer duration.

For example, one might want to live on $100,000 in 2022 dollars (their desired liability), but in the worst-case scenario, they need only $60,000 (their true liability). They can buy a mix of TIPS and Treasuries with $100,000 in 2022 dollars. Five years later, they will want more than $100,000 in nominal value (i.e., in 2027 dollars) because of inflation. If the total return on their mix of TIPS and Treasuries is less than the difference between $100,000 in 2027 dollars and $100,000 in 2022 dollars, they might need to live on less or sell some stocks.

Either way, they would sacrifice less income or stocks by matching their liability at the end of 2022 rather than 2021. The likelihood that they would have less than $60,000 in 2022 dollars is lower as well. This is because current bond yields predict future returns. For one’s liabilities in the future, they should want the yields at the end of 2023 to be similar to the yields today.

‘Don’t Do Something, Just Stand There' . . . Unless You Don’t Have a Good Plan

Saint Jack Bogle is right, but only if your financial plan upholds his principles. In reality, such readers do not have to wish for 2023 to be like any year. Even 2019. You are prepared for any market because you will stick to your plan.

For those for whom standing still in 2022 was painful, give yourself a pass, especially if you are an earner or saver. The past three years were a unique period in the financial markets for many of us. To err is human! Myriad individuals have shared how they overcame their mistakes and achieved financial milestones in WCI blogs, forums, and podcasts. As the OG WCI says, “a physician income covers a multitude of mistakes.”

While others are still licking their wounds, you can create a good financial plan to take advantage of whatever happens next—not only in 2023 but also for your next phase in saving for financial independence.

Would you rather 2023 be like 2022, or do you want a repeat of 2021? If the bear market continues, will you buy stocks that are on sale? Can or should you be greedy if others are fearful? Comment below!

The post If You Want More Money, You Should Root for 2023 to Be Just Like 2022 appeared first on The White Coat Investor - Investing & Personal Finance for Doctors.

||

----------------------------

By: Josh Katzowitz

Title: If You Want More Money, You Should Root for 2023 to Be Just Like 2022

Sourced From: www.whitecoatinvestor.com/if-you-want-more-money-you-should-root-for-2023-to-be-just-like-2022/

Published Date: Sat, 31 Dec 2022 07:30:22 +0000

Read More

Did you miss our previous article...

https://peaceofmindinvesting.com/investing/a-career-in-the-pharmaceutical-industry-can-make-physicians-a-huge-salary

.png) InvestingStocksToolsClubsVideosPrivacy PolicyTerms And Conditions

InvestingStocksToolsClubsVideosPrivacy PolicyTerms And Conditions