<iframe style="width:120px;height:240px;" marginwidth="0" marginheight="0" scrolling="no" frameborder="0" src="//ws-na.amazon-adsystem.com/widgets/q?ServiceVersion=20070822&OneJS=1&Operation=GetAdHtml&MarketPlace=US&source=ss&ref=as_ss_li_til&ad_type=product_link&tracking_id=peaceinvesting-20&language=en_US&marketplace=amazon®ion=US&placement=0060555661&asins=0060555661&linkId=80f8e3b229e4b6fdde8abb238ddd5f6e&show_border=true&link_opens_in_new_window=true"></iframe>|<iframe style="width:120px;height:240px;" marginwidth="0" marginheight="0" scrolling="no" frameborder="0" src="//ws-na.amazon-adsystem.com/widgets/q?ServiceVersion=20070822&OneJS=1&Operation=GetAdHtml&MarketPlace=US&source=ss&ref=as_ss_li_til&ad_type=product_link&tracking_id=peaceinvesting-20&language=en_US&marketplace=amazon®ion=US&placement=1119404509&asins=1119404509&linkId=0beba130446bb217ea2d9cfdcf3b846b&show_border=true&link_opens_in_new_window=true"></iframe>|<iframe style="width:120px;height:240px;" marginwidth="0" marginheight="0" scrolling="no" frameborder="0" src="//ws-na.amazon-adsystem.com/widgets/q?ServiceVersion=20070822&OneJS=1&Operation=GetAdHtml&MarketPlace=US&source=ss&ref=as_ss_li_til&ad_type=product_link&tracking_id=peaceinvesting-20&language=en_US&marketplace=amazon®ion=US&placement=1119376629&asins=1119376629&linkId=2f1e6ff64e783437104d091faaedfec7&show_border=true&link_opens_in_new_window=true"></iframe>

By Josh Katzowitz, WCI Content Director

Located between the L’Artisan des Glaces gelato shop and the L’Esprit de la Provence store, my daughter spotted her next purchase. She stepped into the Les Halles boutique/patisserie and made her choice. It was June 2022. We were hot and sweaty and running all over the World Showcase at Epcot in Orlando. It was a $43 shirt with French sayings and renderings of the Eiffel Tower and the Arc de Triomphe sprinkled across the material, and it featured tiny, subtle Mickey Mouse ears all around. She thought it was gorgeous. And for the first time in her life, my 12-year-old daughter pulled out her Greenlight debit card and made her own purchase.

She probably won’t remember the moment (unless she reads this column), but it was still a turning point. In essence, she took another baby step on her journey to learning about finances.

“The Greenlight Card is nice because you don’t have to carry around a bunch of cash,” she told me as we power-walked from France to Mexico. “It teaches you to be responsible for your money by keeping it and then paying with it.”

Her twin brother chimed in: “I like my card, because it has a picture of me on it playing piano.”

My kids have never been good at asking for their allowance. They hardly spend any of their money, and they seem content to wait for their birthdays or for Hannukah to receive their Lego sets and their Yu-Gi-Oh! cards and their trendy new clothes.

Me? I don’t understand it. Every Sunday afternoon when I was growing up, I was asking my parents for my $5 allowance and dreaming of all the baseball cards that I could buy and all the Blockbuster videos I could rent. My kids would let months go by without mentioning the cash we owed them.

As a parent of pre-teens, we’ve been teaching our kids about money and finance and talking about subjects like budgeting, mortgages, interest, retirement accounts, and whether we should buy a new car. Several months ago, my wife ordered Greenlight debit cards for the kids, joining the 4 million other families who have done so.

Here’s what you should know about the Greenlight card and if it’s a good way to teach your children about finance and money management.

[Disclaimer: The White Coat Investor has no financial relationship with Greenlight, and I have not been compensated in any way by Greenlight.]

What Is the Greenlight Card?

Greenlight is a debit card for kids that allows them to earn, save, and invest their money. The company says its mission is to “shine a light on the world of money for families and empower parents to raise financially smart kids.”

It gives kids and teens a secured card of their own so you, as the parent, aren’t carrying around wads of their cash to spend while trying to keep track of how much change you owe each kid. Do I want to carry $60 worth of cash for each of my kids at Disney World and then remember that I owe my daughter $17 after her Mickey shirt purchase? Not really. This is much easier since the Greenlight card is taken anywhere that Mastercard is accepted.

When I was a kid, my parents opened a checking account for me at a C&S bank. I would have to ride my bike a couple of miles over to the local branch to deposit my money. Greenlight is the 2022 version of that (and this way, you don’t have to wait in line for a bank teller).

Getting an Allowance Through the Greenlight Card

Kids no longer have to remember to ask for allowance. Now, it can automatically show up in their Greenlight account, which they can keep track of online, and if you have a teenager who has a part-time job, you can tie a direct deposit to their account.

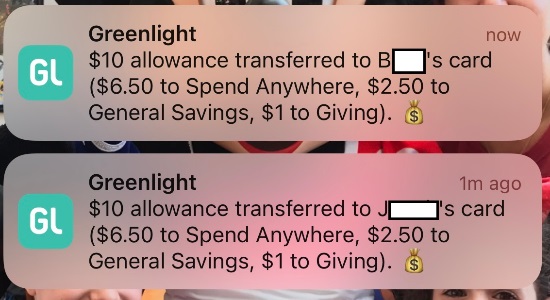

The parents also get plenty of control over their kids' accounts and get notifications on their phones for when deposits are made or when money is transferred out. For instance, I get this message every week.

Based on the settings we’ve decided on, they’re automatically saving 25% of their income and setting aside 10% for charitable giving. As I’m writing this, I just asked my kids if they know how to get into their Greenlight account to check their savings and spending. In unison, they said, “No!”

Obviously, we still have more educational work to do.

How Much Does the Greenlight Card Cost?

There are three price tiers for the Greenlight Card.

For $4.99 per month, you get the debit card, access to the app, parental controls, and 1% back on savings (this is similar to the interest a bank would pay you). For $7.98, you get all of that and the ability for the parents to invest their own money. For $9.98 per month, you get everything previously mentioned, plus 1% cash back, 2% on savings, and a variety of protection plans (identify theft, cell phone, etc.).

Whatever price tier you pick, it's a good way to teach your children about the effects of compound interest.

Learning to Save and Invest with the Greenlight Card

This was the $43 shirt bought with my daughter's Greenlight card.

Through the app, parents can still control and see how their children are spending and saving their money.

On the $7.98 and $9.98 monthly tiers, your kids can also begin investing. All they need is $1, and they can begin buying fractional shares in ETFs. After all, it’s never too early to teach your kids about the power of the stock market.

Also worth noting: the balance in the account is FDIC-insured up to $250,000, and your kids can pick their own photos to be displayed on the card.

We’ve enjoyed our experience with Greenlight so far, and even though there are a few cons (the monthly fee, the fact that the kids are using a debit card and not building any kind of credit score, and the fact you can’t use Venmo or PayPal to fund the account), our kids have learned a little more about finance since they received their own cards.

They still don’t mention receiving their allowances; I’m sure it almost never crosses their minds. But it was fun to watch my daughter pull out her debit card at Epcot, stick it into the credit card machine, and watch her pay for her own purchase (even if she did look slightly nervous while doing it).

As she said afterward, “You have to learn someday.”

A Quick Note on My Last Column

In case you missed it, I wrote late last month about buying a new Tesla and how and why we did it. A couple of extra notes.

- I got plenty of pushback on financing $50,000 of the car with some readers saying I can’t really afford it if I can’t buy it in cash. That’s fine. It still doesn’t change my opinion that this was the best decision for us, especially since we plan to pay it off much quicker than the 60-month loan dictates. It’s that age-old question of, can we earn more on our portfolio than we pay in car loans at 2.94% interest? I think we’ll be fine.

- I ended up selling my 2010 Mazda CX-9 for $8,500. That was slightly more than I expected. So, that’s a solid win.

- Apparently, we could currently sell our 2022 Model Y for somewhere in the $75,000 range, even though we just bought it for $58,000. My wife said maybe we should think about getting rid of the Tesla after only having it for a month. I’m not sure if she was serious.

What I’m Reading This Week

The Pushover Landlord vs. One Who’s Compassionate

This was an interesting story on Humble Dollar about how landlords should treat their tenants and about whether the author’s father’s mantra of, “Don’t be a wimpy landlord,” was worthwhile.

The author, psychologist Steve Abramowitz, took that advice, and, well, he just kind of ignored it. As he wrote,

“I never wanted to be a pushover for my tenants, but I also never wanted to pulverize the lives of people who, in some sense, were in my care.

Folks who rent worry about their safety, their comfort, and their budget, just like homeowners do. Pride of ownership is fine as far as it goes. But what about pride of partnering? Of course, there’s an inherent conflict of interest and a hierarchical relationship between owners and renters, but I believe there’s also a common thread. Both want a living space that’s functional and presentable.

Partnering doesn’t only help the renter. We once had a scheduling snafu and couldn’t arrive in time to meet a prospective tenant at the property. The vacating person offered to show her around the apartment on his own time. I like to think he was returning the respect he received during his stay with us.”

It’s nice to treat people with compassion and kindness even when you’re frustrated and angry and feel like your tenants might be trying to take advantage of you. It’s also not always the best idea to try to take advantage of your tenants by raising the rent to extraordinarily high levels. After all, finding a good tenant isn’t always so easy. It’s probably best to hold on to the good ones for as long as you can.

What Gen Z Needs from Physicians

What does Gen Z want from their doctors? According to one new study, they want to be asked if they have enough food and housing.

In a poll of more than 1,200 people between the ages of 14-24, the vast majority of them (81%) said healthcare providers should ask patients if they have access to food and safe housing and if they have experienced discrimination.

“It seems obvious that addressing social needs, like food and housing, in clinical settings would benefit patients,” Claire Chang, a University of Michigan Medical School student and the lead author of the poll, said, via The Hill. “But we actually know very little about whether and how patients would want to receive this kind of assistance. Youth in our study told us that they do want to talk about social determinants of health with their providers. It is important for us to understand these preferences and desires as social/medical care integration efforts spread across the country.”

To read all the poll findings, it’s available on the Journal of Adolescent Health.

The ESG Backlash

A few years ago, Dr. Jim Dahle wrote about ESG investments and whether Environmental, Social, and Governance investing is actually good for your portfolio. He seemed pretty skeptical about the whole idea, and as FT Adviser writes, there’s been plenty of backlash against ESG investing in 2022 with critics claiming fraudulent activity and virtue-signaling.

But author Nigel Green says “ESG backlash is misguided and shallow” and claims that those who disagree with the idea of ESG investments are on the wrong side of history.

Let’s reconvene in 50 years and see who was right.

Money Song of the Week

Those who are into musical theater already know Lin-Manuel Miranda doesn’t mind penning numbers about finance and the power that money has and can wield.

I’ve written about Hamilton before, but now that I recently saw a summer stock performance of Miranda’s In the Heights, let’s explore the song “96,000,” when the play’s characters dream about what they would do if they won $96,000 in the lottery.

As is common for those listening to a Miranda musical for the first time, there’s almost too much going on, and it’s difficult to parse out all the applicable lyrics. But here are a few fun ones.

“Imagine how it would feel going real slow/Down the highway of life/With no regrets/And no breaking your neck for respect or a paycheck/For real, though/I'll take a break from the wheel and we'll throw/ the biggest block party, everybody here/It's a weekend when we can breathe/Take it easy.”

And . . .

“Yo, with 96,000, I'd finally fix housing/Give the barrio computers and wireless web browsing/Your kids are living without a good edumacation/Change the station.”

And maybe the best (and harshest) answer:

“If I win the lottery/You'll never see me again.”

As for the official WCI advice? Put that $96,000 in low-cost index funds and check back in 20 years to see how much your investment has grown.

Tweet of the Week

Remember, sometimes even financial advisors can’t avoid financially ruining themselves. Lessons can be learned from this Twitter thread.

Have you tried the Greenlight card? Have you used other kid-friendly debit cards? How else do you like to teach your children about finances? What would you do with an extra $96,000? Comment below!

[Editor's Note: For comments, complaints, suggestions, or plaudits, email Josh Katzowitz at [email protected].]

The post Is Greenlight the Best Debit Card to Help Your Kids Learn Finance? appeared first on The White Coat Investor - Investing & Personal Finance for Doctors.

||

----------------------------

By: Josh Katzowitz

Title: Is Greenlight the Best Debit Card to Help Your Kids Learn Finance?

Sourced From: www.whitecoatinvestor.com/greenlight-card-for-kids/

Published Date: Sun, 14 Aug 2022 06:30:40 +0000

Read More

Did you miss our previous article...

https://peaceofmindinvesting.com/investing/rates-are-rising-how-to-navigate-buying-a-home-in-todays-market

.png) InvestingStocksToolsClubsVideosPrivacy PolicyTerms And Conditions

InvestingStocksToolsClubsVideosPrivacy PolicyTerms And Conditions