<iframe style="width:120px;height:240px;" marginwidth="0" marginheight="0" scrolling="no" frameborder="0" src="//ws-na.amazon-adsystem.com/widgets/q?ServiceVersion=20070822&OneJS=1&Operation=GetAdHtml&MarketPlace=US&source=ss&ref=as_ss_li_til&ad_type=product_link&tracking_id=peaceinvesting-20&language=en_US&marketplace=amazon®ion=US&placement=0060555661&asins=0060555661&linkId=80f8e3b229e4b6fdde8abb238ddd5f6e&show_border=true&link_opens_in_new_window=true"></iframe>|<iframe style="width:120px;height:240px;" marginwidth="0" marginheight="0" scrolling="no" frameborder="0" src="//ws-na.amazon-adsystem.com/widgets/q?ServiceVersion=20070822&OneJS=1&Operation=GetAdHtml&MarketPlace=US&source=ss&ref=as_ss_li_til&ad_type=product_link&tracking_id=peaceinvesting-20&language=en_US&marketplace=amazon®ion=US&placement=1119404509&asins=1119404509&linkId=0beba130446bb217ea2d9cfdcf3b846b&show_border=true&link_opens_in_new_window=true"></iframe>|<iframe style="width:120px;height:240px;" marginwidth="0" marginheight="0" scrolling="no" frameborder="0" src="//ws-na.amazon-adsystem.com/widgets/q?ServiceVersion=20070822&OneJS=1&Operation=GetAdHtml&MarketPlace=US&source=ss&ref=as_ss_li_til&ad_type=product_link&tracking_id=peaceinvesting-20&language=en_US&marketplace=amazon®ion=US&placement=1119376629&asins=1119376629&linkId=2f1e6ff64e783437104d091faaedfec7&show_border=true&link_opens_in_new_window=true"></iframe>

[It's FIRE week here at WCI, where we celebrate all things Financial Independence, Retire Early! Every post this week is going to be about topics relevant to the FIRE community. Enjoy!]

By Dr. James M. Dahle, WCI Founder

How much money does a doctor need to retire? There are a lot of short answers that are reasonably accurate, such as:

- It depends.

- More than you might think.

- Less than people who just learned about the 4% rule think.

The long answer, of course, is going to take an entire blog post to explain.

First, though, let's explain the short answers.

Retirement Isn't an Age; It's a Number

The most important concept to understand is that retirement is not an age, such as 65. Retirement (aka financial independence) is a number, either expressed as income or as a gross sum of money. It really doesn't matter how you express it since those two things are fungible. You can convert income into a sum of money, and you can convert a sum of money into income. The most important number, however, is the one that determines how large that income or that lump sum must be. It's the wizard behind the curtain. That number? How much you spend. It's actually how much you will spend in retirement, but that's typically pretty closely related to what you spend just before retirement. When I say “it depends,” what it depends on is your spending. If you spend $50,000 a year, you don't need that much money to retire. There's a good chance you already have enough. On the other hand, if you spend $400,000 a year, you're going to need a much larger nest egg.

The Bad News of Retirement

Three decades ago, financial advisors would tell their clients that if their portfolio made 8%-10% a year, they could spend 8%-10% per year. It turns out that was not true. The problem is something called Sequence of Returns Risk (SORR). When your portfolio makes 8% and you spend 8%, no problem. But what happens the next year when your portfolio loses 20%? You can't spend negative 20%. Are you going to spend another 8% that year? Now, your portfolio has dropped by 28% in a single year. That's not good. If you have a bunch of these bad years early in retirement, you'll run out of money rapidly, even if the returns throughout your retirement average 8%. That's sequence of returns risk.

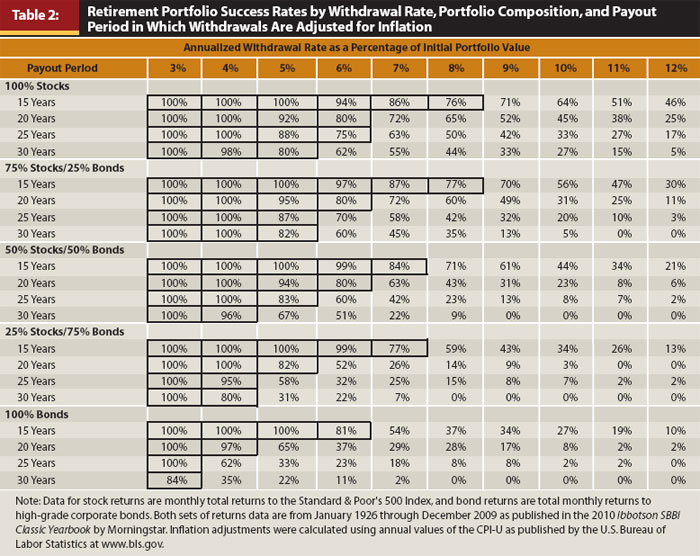

To counter that, you have to spend less than the average rate of return of the portfolio. How much less? Well, that's exactly the question that researchers at Trinity University wanted to answer back in the '90s. Here's the most important table from an updated version of their study:

This table is worth studying. Down the Y axis are various asset allocations from 100% stocks (US large cap) to 100% bonds (US corporate) and various lengths of retirement from 15 years to 30 years. Across the X axis are withdrawal rates. These are a percentage of the initial portfolio value adjusted up with inflation each year. The figures in the table represent the percentage of all of the rolling 30-year periods since 1927 in which the portfolio did not run out of money during retirement.

Given that it is historical data and that the history is pretty short (about four independent 30-year periods), it has some limitations. But it's still pretty useful. As you can see, a 3% withdrawal rate is bulletproof, and most people consider 4% as good enough. Five percent starts introducing some significant risk (runs out of money one-third of the time in a 30-year retirement with 50% stocks). It's a 50/50 proposition at 6%, and by 8%, you would have run out of money 90% of the time. This is why you hear about the “4% rule” (really it's more of a 4% guideline).

The 4% rule isn't really a great withdrawal/spending method in retirement, but it's pretty useful as a rule of thumb to determine how much you need to retire. You just have to reverse-engineer it. If you can spend 4% a year, then you need 25X what you spend. That's a lot of money. At least a million, and for many doctors, $5 million-$10 million dollars. This is the bad news of physician retirement.

More information here:

What Income Do You Want to Retire At?

The Good News of Retirement

If that was the first time you've ever heard that, I'm sorry. Saving for retirement is the greatest financial challenge of your life. For most people, even doctors, it will take your entire career to save up a nest egg large enough to provide your desired level of comfort in retirement. However, there are two pieces of good news. The first is that you only need to replace what you spend, not what you earned prior to retirement. Think of all those expenses that go away in retirement.

- You'll pay dramatically less in income tax

- You won't pay payroll taxes at all

- You no longer have to save for retirement

- No disability and life insurance premiums

- You no longer have to save for college

- Your child-related expenses should be much lower (if not zero)

- Your work-related expenses should go away

The bottom line for most docs is that they only need to replace 25%-50% of their pre-retirement earnings to maintain the same standard of living.

The second piece of good news is that Social Security will replace some of that income. A physician, especially one married to another high earner, is likely to receive the equivalent of $40,000-$60,000 in today's dollars from Social Security each year for the last couple of decades of their life. If they retire anywhere near traditional retirement age, that knocks $1 million or more from the amount they must save up as a retirement nest egg. Some people say:

“But Social Security is running out of money!”

What do you mean by running out of money? You mean it'll only pay 77% of promised benefits? Because that's what the government means when it says Social Security is running out of money. Besides, that's an easy thing to fix. It can be fixed by raising the Social Security age, increasing the Social Security tax rate, raising the Social Security wage limit, decreasing the inflation adjustment, means testing the benefit, or increasing the taxability of Social Security. Most likely it would be a combination of those changes. What it's NOT going to do, though, is go away. Think I'm wrong? List the names of 60 senators who will vote against it. Go ahead, I'll wait.

Did you stall out at about five? Me too. The fact remains that Social Security is perhaps the most popular of all government programs. It would be political suicide to vote against it. I think we can all agree that Social Security will pay you something, barring a complete societal collapse, in which case we're all hosed anyway.

More information here:

8 Things to Do with Financial Independence Besides Retire Early

Is Passive Income the Answer?

OK, enough with the short answer. If you've made it this far into the post, you will at least have the basics down. Now, let's head off into the weeds a bit and start talking about the long answer.

Some people—let's call them the “passive income folks” (most of whom have a large percentage of their portfolio invested in either real estate or high dividend stocks)—will tell you that once you have enough passive income to replace your earned income, you are now financially independent and you can retire. There are two problems with this philosophy. The first is that income is not definite. Rents can disappear with vacancies, and dividends can be cut. The higher the yield on an investment, the less secure it becomes. If all you're looking at is yield, you can often get into investments that aren't wise. Consider junk bonds or, worse, peer-to-peer loans. Yes, these investments offer a high yield, but in the meantime, the value of your principal is dropping. It's really not all income; some of it is really your principal. As long as you're aware of this and don't construct an outlandish portfolio, it's not too big of a deal.

The second, much more significant problem with the income philosophy is that it simply causes you to oversave/underspend. If you only ever spend the income, you're right that you'll never run out of money. It's a very, very safe withdrawal plan. So safe that I'd love to be your heir, because you're going to leave dramatically more behind than you retired with. The value of your investments, whether stocks or real estate, is going to continue to grow, and only a fraction of their return is going to come to you as income. The rest is just going to compound for the rest of your life.

You're not immortal. You will not live forever. It's OK to spend some principal. You just have to be careful how much of it you spend. That's why a plan based on a percentage of retirement assets is generally superior to one based solely on income.

People Say a 4% Withdrawal Rate Is Too Aggressive, Even Cavalier

“I read somewhere that 4% really isn't safe, that I should use 3% or even 2%. What do you think?”

You really know what I think? I think those people are bonkers. But it's important to understand their arguments. The argument is three-fold.

Part 1 basically says, “I looked at the chart for a 50/50 portfolio and 30 years, and I'm not OK with only a 96% rate of success. That means I could run out of money 1 out of 25 times. So, I'm going to cut back to 3% and get a 100% rate of historical success.” The answer to this argument is simply that the rate of the whole country (world?) going to hell in a handbasket over the next 30 years is higher than 4%. Think about all those unstable politicians with their fingers hovering over nuclear buttons. Plus, consider how long the typical world empire lasts. Maybe a few hundred years, if you're lucky. Then, it all blows up. Things can change, and they can change very quickly. Facing that sort of true risk, a 4% risk of running out of money using data from just the last 100 years seems perfectly acceptable. An even better answer is that nobody actually uses a 4% withdrawal method like the Trinity Study did. They adjust as they go. If SORR shows up, they spend less. But more on that later. The bottom line is that this argument can be dismissed off-hand.

Part 2 says, “Valuations are higher now than they have been historically, so you cannot expect as high of returns from your portfolio and, thus, must spend less.” This argument has a little more substance to it but not much. The answer is that the data in the Trinity Study included a lot of really terrible periods of market returns—the Great Depression, the Global Financial Crisis, the Stagflation of the 1970s, a World War, a Cold War, the tech meltdown. It still worked just fine through the COVID pandemic. When you make this argument, you're saying, “I need to have a plan that accounts for a time period even worse than the Great Depression.” That's awfully conservative. But if this is really a big concern for you, then sure, adjust down a bit. Maybe 3.75% or even 3.5%. If you're super nutso, you can go all the way down to 3%. But the folks adjusting down to 2% or less? They're up in the night. Think about it. Imagine your portfolio just barely kept up with inflation, and you had a long-term real return of 0% for decades. And you're spending 2% of it a year. How long will it last? Fifty years. How long are you going to live again?

Part 3 says, “I want to retire early. I could be retired for 40 or even 50 years, and the Trinity Study only looked at 30-year periods so I'll have to spend much less.” Two comments on this. First, I know very few early retirees who never make another dollar. Many of them go back to work after a while or have a side gig that pays something. It might not be anywhere near what they were making before, but even a little bit of income dramatically extends how long a nest egg can last. Second, the difference between lasting 30 years and lasting indefinitely is minimal. If you're really worried about this, then dial it back a bit to 3.75% or 3.5% (or 3% if you're really, really worried and lying awake at night worrying about it). The truth is that most people can withdraw 5% and still be fine. Six percent is 50/50 at 30 years. So, 4% is already very conservative. And you're talking about reducing it even further.

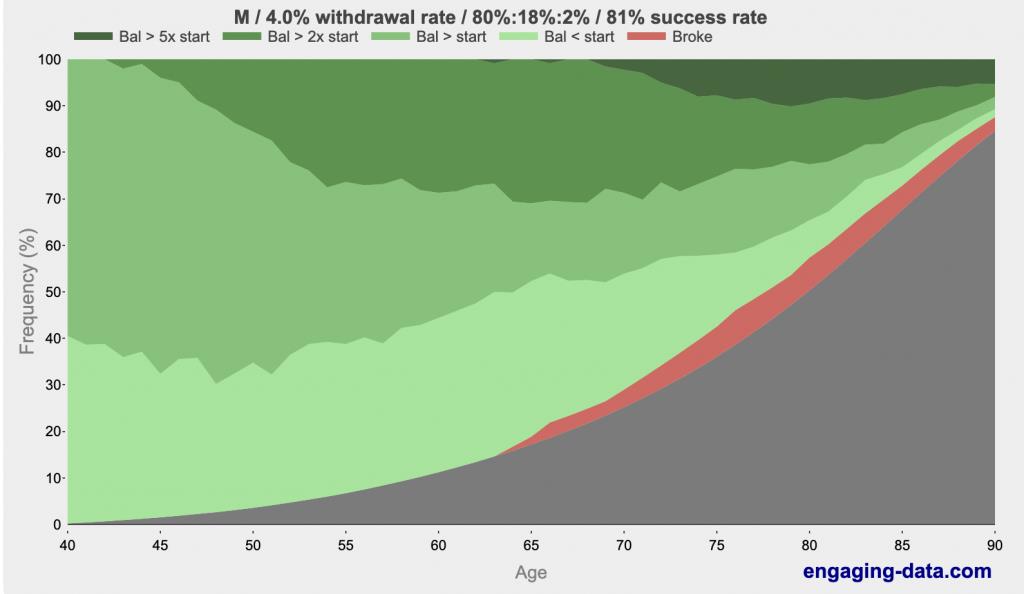

No, 4% is not “too aggressive” or “cavalier.” It's conservative, and it'll be fine. And if it isn't, you'll know long before you run out of money and you can adjust. Besides, you'll probably be dead anyway. Using the catchy phrase “Rich, Broke, or Dead,” Engagingdata.com has demonstrated that you're far more likely to be dead in your 80s or 90s than to run out of money. Check it out:

See the darker greens? That's rich. See the black? That's dead. See the red? That's broke. What are the real issues at 80 or 90 if you retire at 40 using a 4% withdrawal rate? Well, there's the issue of having so much money that you'll ruin your heirs. On average, using the 4% rule you'll die with 2.7X what you retired with. But by age 90, you've got an 85% chance of being dead. And if you think that's a big risk at 90, wait until 100.

More information here:

How to Spend in Retirement

Doctors Aren't Special

This blog post has doctors in the title, as though doctors have some special consideration when it comes to how much is needed for retirement. There are a few unique things about doctors in personal finance. A late start. Large student loans. A high-earned income accompanied by a high marginal tax rate. Some asset protection considerations due to malpractice. Complicated retirement account situations. That's about it. The whole “how much do I need in retirement” thing is not unique for doctors—other than that most doctors spend more than the average American, so, of course, they'll need more saved for retirement to pay for that lifestyle.

Doctors Don't Save

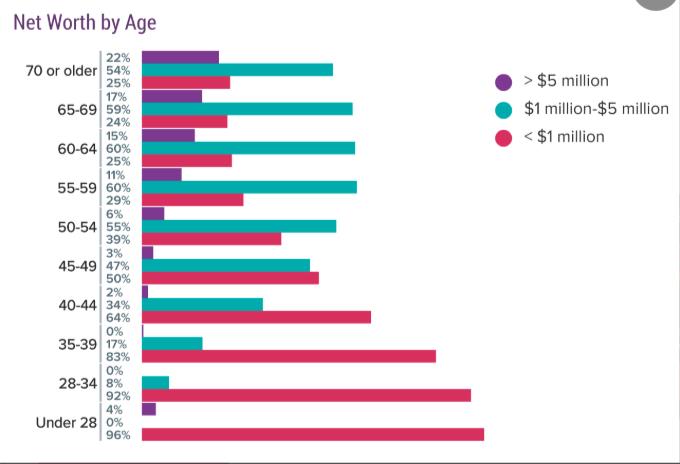

The bigger problem is that doctors, like everyone else, don't accumulate enough money to pay for their desired retirement. Check out this survey from Medscape where doctors were asked about their net worth. Remember that this is everything they have, not just their retirement nest egg. It includes their home(s), car(s), and all of their other stuff. So, their nest egg isn't even this large.

As you can see, one-quarter of doctors in their 60s aren't even millionaires, and only about 1 in 6 have $5 million or more. Doctors might say, “I need $5 million (or $10 million) to retire,” but almost none of them have it. Which is probably fine. You can have an awfully nice retirement even if you spend a lot less than $200,000-$400,000 per year.

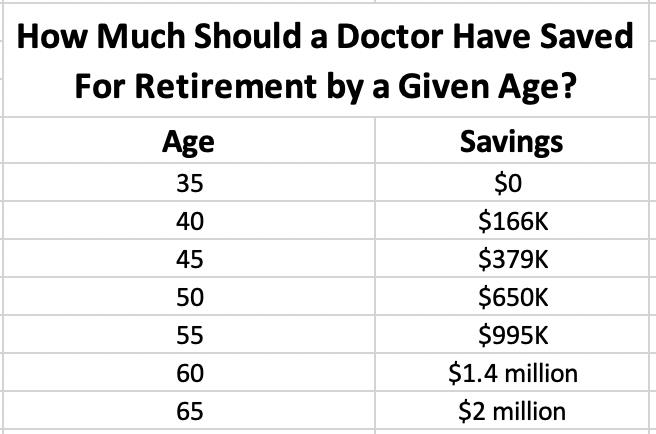

How Much Should You Have Saved for Retirement at Any Given Age?

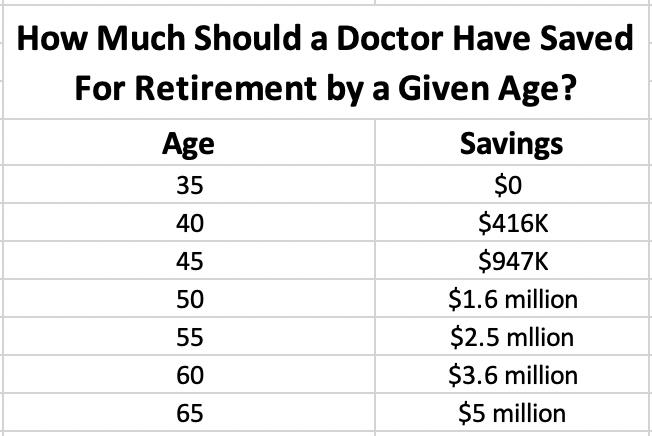

But let's say you have decided you need $5 million to retire at age 65. How much should you have saved at any given age? Since you're a doctor, we'll assume you don't even start until age 35. Even if you finish training before then, you'll have other serious needs for savings in your early 30s, such as house down payments and student loans.

Note that this is adjusted for inflation. The assumption used is a 5% after-inflation (real) return, so we're talking about getting to $5 million in today's dollars. If you need $5 million and you're 45 and you have $1.4 million, you're already way ahead of schedule. If you have $600,000, you're behind.

What if you've realized that you only need $2 million to retire? We can dial it all back a bit. Same assumptions.

I hope you find those charts helpful, whether they make you feel good or make you anxious. Keep in mind that like any calculation, this one is garbage in/garbage out.

The Truth About Retirement Spending

If you hang out on retirement, early retirement, or even general investing forums such as the Bogleheads, you will notice people having long, extensive discussions about safe withdrawal rates and retirement withdrawal/spending plans. They go on for hundreds and hundreds of posts over weeks debating back and forth what to do. I find it all hilarious, especially the amount of precision that the engineer types start using. Former US Treasury Secretary William E. Simon shared a joke that has been quoted many times since:

“Q. How do you tell economists have a sense of humor?

A. They use decimal points.”

There are so many variables and assumptions in any of these equations that when someone tells you the ideal withdrawal percentage is 3.82%, feel free to roll your eyes.

That's not really why I think it's so funny, though. It's funny because if you actually ask reasonably wealthy multi-millionaire retirees what their withdrawal method is, they all tell you the same thing:

“Ad hoc. We just sell shares when we need money without regard to budgets, SORR, and whatever.”

Why is that? It's because there are three categories of retirees, and this method works great for all of them.

#1 People Who Have Far More Than They Need

When these people calculate their withdrawal percentage, it comes out to 1%-2% or even less. It's not because they're paranoid they'll run out of money. They just have a lot of it, more than they'll need. They may have estate tax problems. They certainly have decisions to make about how much to leave to heirs and how much to leave to charity. As an anxious near retiree, you can't really have a serious discussion about withdrawal rates with these folks. The truth is that MOST multi-millionaire retirees are in this category. Almost nobody retires JUST as soon as they hit their number. They get one more year syndrome and work another year or two or three and boost up that nest egg. Or they became wealthy before they were really done working and worked another five or 10 or 20 years. They might even still be earning money in retirement.

#2 People Who Have Enough to Retire

There are a few people who are careful and reasonable but who just hate their jobs. As soon as they had enough money, they punched out. They're the ones trying to have serious discussions about withdrawal rates and plans. There just aren't very many of these folks. They can also just start with a withdrawal rate of around 4% and adjust as they go.

#3 People Who Don't Have Enough

These people are essentially just trying to spend as little as possible in retirement. There are a lot of these people, but few of them are multimillionaire physicians. They basically do the best they can, and if they're still alive when the money runs out, they live off of Social Security and charity. Safe withdrawal rate and technique studies don't matter to these folks any more than they matter to those with far more than they need.

More information here:

How I Went from a Negative Net Worth in My 30s to Early Retirement

Calculating How Much You Need for Retirement

All right, with that little bit of cynicism out of the way, let's talk about how to calculate your number. The easy back of the napkin number is just multiplying your spending by 25. But let's get into the weeds a bit more.

Calculating Spending

Step 1 is to figure out what you are actually going to spend in retirement. Start by figuring out what you spend now. This is easy for those who live on a budget or otherwise track their spending. If you have never done this, this is as good a reason as any. Log in to your financial accounts—including your bank accounts, credit card accounts, Venmo, and PayPal. Add up everything you spent money on in the last three months. You can put it into categories if you want, but you don't have to for this exercise. Then divide by three. That gives you a monthly amount. You can multiply that by 12 to get an annual amount. This tells you what you're actually spending now.

Step 2 is the tricky part, which is adjusting your current spending for what your spending will look like in retirement. Many of your expenses will go away completely (who needs to save for retirement when you're already retired?) Many of your expenses will go down when you stop working (commuting costs) and get the kids through college (college savings, child-related expenses). But others might go up, such as healthcare and hobby- or travel-related expenses. You'll need a real categorized budget at this point to really get this all sorted out. Make sure you include the categories most likely to change as you move into retirement. These include:

- Payroll taxes (go away completely)

- Income taxes (usually go down dramatically)

- Disability insurance premiums (disappear)

- Life insurance premiums (disappear)

- Work expenses (disappear)

- Commuting/auto expenses (decrease)

- Retirement savings (disappear)

- College savings (disappear)

- Child-related expenses (disappear [hopefully])

- Hobbies (probably go up as you have more time to do them)

- Healthcare (may go up if your employer has been covering it but could fall at 65 as you become eligible for Medicare)

- Travel expenses (likely to go up, at least in the first few years of retirement)

Write down the amount you're spending now and an estimate of what you will spend in retirement. Once you have this amount, you're ready to move on to the next step. Keep in mind that you need to adjust for inflation. There are two ways to do this. You can simply use real (after-inflation) rates of return in your calculations, or you can adjust the end amounts. Either way is fine, just be consistent so inflation will be properly accounted for.

Choosing a Withdrawal Percentage

Once you've got a spending number, you need a withdrawal percentage to divide it by. What should you choose? If you choose 5%, you'll be done saving a lot sooner than if you choose 3%, but is it safe? Well, there are three factors to consider:

- Asset allocation

- Length of retirement

- Comfort with shortfall

The more aggressively you plan to invest in retirement, the shorter the retirement length, and the more comfortable you are with the risk of coming up short, the higher your percentage can be. Conversely, if you will have the majority of your assets in safe investments, if you expect 40-50 years in retirement (due to early retirement or a much younger spouse), or if you lie awake at night worrying about running out of money, then you'll be using a much lower percentage. If most expenses are fixed, you might need to have a lower percentage. If most expenses are optional and they can be eliminated in the event of poor investment performance, you can start with a higher percentage.

The bottom line is that if you're choosing something greater than 5%, you're probably being too cavalier, and if you're using something less than 3%, you're being ridiculously conservative. There are some resources you can use to run numbers and decide exactly how much you're comfortable withdrawing (and thus how small your nest egg can be.) These include:

- FIRECalc

- EngagingData.com

- Big ERNs Safe Withdrawal Rate series

Adjusting for Income

Now, you have both pieces of the equation. You simply divide your annual spending by your chosen withdrawal percentage. If you plan to spend $125,000 per year and you are comfortable with a 3.75% withdrawal rate, then you will need $125,000/3.75% = $3.33 million. But what about if there are other sources of income? It really depends on when those sources of income start and just how guaranteed they are. For example, if you are retiring at 45, I would completely ignore Social Security when it comes to making any sort of income adjustment. You're at least 17 years away from receiving it and perhaps as many as 25 years away. Plus, you won't be paying into it nearly as much as someone who works longer. You know it's out there somewhere, so perhaps you can be a little more aggressive on your retirement withdrawal percentage. But that's it. On the other hand, if I was retiring at 68, I would add the entire amount to the amount I could spend each year.

Some sources of income are more guaranteed than others. Social Security is backed by the government. I would also consider a pension to be pretty guaranteed, as long as the company standing behind it is financially strong. Single Premium Immediate Annuities (SPIAs) are also pretty guaranteed. However, there are plenty of sources of income that are not guaranteed. These include stock dividends, rents from rental properties, and income from small businesses. The safest thing to do with these sources of income is to ignore them and just include the value of the investment in the portfolio. However, if you want to hold those assets out of your portfolio and just add the income to your spending amount, then I would at least discount it in some manner (at least 25%, more for a particularly risky business).

Here's an example. Let's say you have $1.3 million in mutual funds and have a rental property that produces $30,000 a year of income, and you are comfortable with a 4.25% withdrawal rate. You plan to retire at 66 and expect $45,000 from Social Security. How much can you spend? I'd discount the rental property by 25%, take 4.25% from the mutual funds, and count all of the Social Security income.

That's $1.3 million * 4.25% + $30,000 * 75% + $45,000 = $122,750 in retirement income per year

You can reverse-engineer all of this as well. Let's say you want $225,000 in retirement income and have the same Social Security and rental property. How much do you need to save?

($225,000 – $45,000 – 75% * $30,000)/4.25% = $3.5 million

Spending in Retirement

Let's say you're now heading into retirement. How much can and should you spend? Well, it depends. Remember those three categories above? Place yourself into one of them.

#1 More Than You Need

Spend whatever you like as needed, and be sure to have a solid estate plan in place.

#2 Just Enough

Start at 4% and adjust as you go. If SORR doesn't show up in the first few years, you can adjust up a bit. If it does, you can dial it back some. Alternatively, work a little longer and get yourself into category No. 1.

#3 Nowhere Near Enough

Help your heirs to realize they won't be getting anything. Consider buying a SPIA with some of your money. Work longer if you can. Delay Social Security to 70 if at all possible. Plan on investing aggressively with everything you won't be spending in the next 2-3 years and hope for the best.

What’s your number? At what age do you think you could achieve it? Do you anticipate retiring then, or will you continue to work to leave a legacy, for the benefit or charity, or simply because you love your job?

[This updated post was originally published in 2019]

The post How Much Money Does a Doctor Need to Retire? appeared first on The White Coat Investor - Investing & Personal Finance for Doctors.

||

----------------------------

By: The White Coat Investor

Title: How Much Money Does a Doctor Need to Retire?

Sourced From: www.whitecoatinvestor.com/how-much-money-to-retire/

Published Date: Mon, 01 May 2023 06:30:38 +0000

Read More

Did you miss our previous article...

https://peaceofmindinvesting.com/investing/mutual-fund-return-calculator-dividends-reinvested

.png) InvestingStocksToolsClubsVideosPrivacy PolicyTerms And Conditions

InvestingStocksToolsClubsVideosPrivacy PolicyTerms And Conditions