<iframe style="width:120px;height:240px;" marginwidth="0" marginheight="0" scrolling="no" frameborder="0" src="//ws-na.amazon-adsystem.com/widgets/q?ServiceVersion=20070822&OneJS=1&Operation=GetAdHtml&MarketPlace=US&source=ss&ref=as_ss_li_til&ad_type=product_link&tracking_id=peaceinvesting-20&language=en_US&marketplace=amazon®ion=US&placement=0060555661&asins=0060555661&linkId=80f8e3b229e4b6fdde8abb238ddd5f6e&show_border=true&link_opens_in_new_window=true"></iframe>|<iframe style="width:120px;height:240px;" marginwidth="0" marginheight="0" scrolling="no" frameborder="0" src="//ws-na.amazon-adsystem.com/widgets/q?ServiceVersion=20070822&OneJS=1&Operation=GetAdHtml&MarketPlace=US&source=ss&ref=as_ss_li_til&ad_type=product_link&tracking_id=peaceinvesting-20&language=en_US&marketplace=amazon®ion=US&placement=1119404509&asins=1119404509&linkId=0beba130446bb217ea2d9cfdcf3b846b&show_border=true&link_opens_in_new_window=true"></iframe>|<iframe style="width:120px;height:240px;" marginwidth="0" marginheight="0" scrolling="no" frameborder="0" src="//ws-na.amazon-adsystem.com/widgets/q?ServiceVersion=20070822&OneJS=1&Operation=GetAdHtml&MarketPlace=US&source=ss&ref=as_ss_li_til&ad_type=product_link&tracking_id=peaceinvesting-20&language=en_US&marketplace=amazon®ion=US&placement=1119376629&asins=1119376629&linkId=2f1e6ff64e783437104d091faaedfec7&show_border=true&link_opens_in_new_window=true"></iframe>

[Editor's Note: Couldn’t make it to WCICON23 this year? You’re in luck! The newest White Coat Investor course, Continuing Financial Education 2023, is now available, and it’s got everything you missed in Phoenix. From keynote speakers Christine Benz and Stacy Taniguchi to sessions on how to vet private real estate deals, more than 55 hours of content are now available in the CFE 2023 course. Even better news: from now until April 17, the course is on sale for $100 off! If you want to continue on the path toward financial literacy, get the CFE 2023 course today!]

By Dr. James M. Dahle, WCI Founder

There's a funny thing about taxes. When you're an employee with a relatively simple financial life, you usually have too much withheld and so you file about the first of February to get your refund ASAP. The self-employed generally end up filing much closer to April 15. As you become a self-employed investor with a complicated financial life, you can't even do that anymore. A few years ago, my financial life finally caught up to me so that I couldn't get my tax return completed by April 15, and I had to file for an extension for the first time.

What happened that caused me to have to do this? It's the usual issue—partnerships not sending me a K-1 before April 15. Although partnerships and S Corporations are required to file their taxes by March 1, they can file an extension themselves and can put off filing their tax return until September 15. C Corporations, like individual taxpayers, don't actually have to file until April 15 (and can extend until October 15). If you get a dozen or more K-1s as I do, the chance of NONE of them filing for an extension is pretty low. And if just one of them does it, well, you're going to have to do it, too.

Taxes, Penalties, and Interest Still Apply

Bear in mind that filing for a tax extension does not relieve you of the burden of paying the taxes due. Those are still due April 15 (or earlier if you didn't stay in the safe harbor). If you fail to pay them, you will pay interest in addition to the taxes due and possibly even a penalty. How can you know how much to pay if you can't even complete the return? The IRS expects you to guess. I mean, estimate. The IRS Form 4868 Instructions say this about it:

“To get the extra time, you must:

- Properly estimate your 2022 tax liability using the information available to you,

- Enter your total tax liability on line 4 of Form 4868, and

- File Form 4868 by the regular due date of your return.

Although you aren’t required to make a payment of the tax you estimate as due, Form 4868 doesn’t extend the time to pay taxes. If you don’t pay the amount due by the regular due date, you’ll owe interest. You may also be charged penalties . . . Any remittance you make with your application for extension will be treated as a payment of tax. You don’t have to explain why you’re asking for the extension . . .

You’ll owe interest on any tax not paid by the regular due date of your return . . . The interest runs until you pay the tax. Even if you had a good reason for not paying on time, you will still owe interest.

The late payment penalty is usually ½ of 1% of any tax (other than estimated tax) not paid by the regular due date of your return, which is April 18, 2023. It’s charged for each month or part of a month the tax is unpaid. The maximum penalty is 25%. The late payment penalty won’t be charged if you can show reasonable cause for not paying on time.

You’re considered to have reasonable cause for the period covered by this automatic extension if both of the following requirements have been met.

- At least 90% of the total tax on your 2022 return is paid on or before the regular due date of your return through withholding, estimated tax payments, or payments made with Form 4868.

- The remaining balance is paid with your return.”

Basically, you have to file Form 4868 and pay any tax due by April 15 (or, in the case of 2022 taxes, by April 18, 2023). If you underpay, you WILL owe interest on the money. If you underpay by a lot, you will also owe a penalty of up to 3% (0.5% x six months). What is the IRS interest rate? It is the federal short-term rate plus 3%, currently a total of 7%.

Of course, those penalties pale in comparison to the failure to file penalty, which increases the penalty from 0.5% a month to 5% a month. Yes, that's right. Five percent a month, and with a minimum of the smaller of $135 or 100% of the unpaid tax. Whatever you do, make sure you either file a tax return or file an extension, whether you can pay the taxes or not.

More information here:

Best Tax Software for 2023

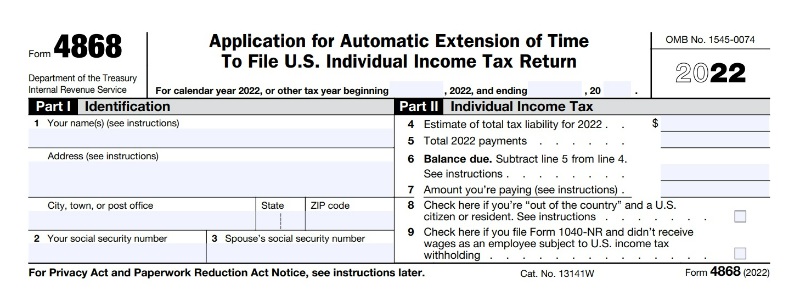

IRS Form 4868

How big of a deal is this form? Let's take a look.

Yup. That's it. Your identifying information plus four lines—how much you owe, how much you've paid, the difference, and the amount on the check you included with this payment. (Hint: Lines 6 and 7 should be the same number.) See, I told you this was super easy.

What About State Tax Returns?

Of course, if you're going to file an extension on your federal returns, you can't very well file your state returns, can you? You will also need to file an extension for each of those. The first time I had to file that extension in 2019, I had to file returns in Utah, Minnesota, and California. Here's what I learned about those particular states.

Utah State Tax Extension

It turns out Utah has the most lenient rules of the three states. In fact, Utah's tax situation is very good compared to those others for many reasons.

First, the maximum tax rate is 4.85% vs. 13.3% in California and 9.85% in Minnesota.

Second, Utahns don't have to make any estimated tax payments. The self-employed can just pay all the tax due on the tax return due date. That gives you use of your tax money for up to an extra 15 months. Employers (including S Corps) do have to withhold taxes for wages, of course.

Third, the interest rate is only 5%, lower than the IRS rate of 7%. That's a pretty good rate. There are even real estate investors and others in need of a short-term loan who prefer to borrow from the Utah State Tax Commission by underpaying their taxes rather than go to a bank or hard money lender.

Fourth, you don't even have to file an extension. You just have to pay the taxes. The extension is automatic. You just send a check in with this coupon.

Fifth, Utah has a clearly defined safe harbor to avoid penalties on late payments. The safe harbor (no penalties due if you meet it) consists of either 90% of what you will owe this year or 100% of what you paid last year. If your tax bill went up dramatically, an extension gives you a six-month, 4% loan on the difference between your tax bills.

Minnesota State Tax Extension

Minnesota has similar rules but a less lenient safe harbor (no option to just pay 100% of last year's tax due). Minnesota charges 5% interest. Like Utah, there's no real form to fill out, just a coupon. Incidentally, Minnesota only requires estimated tax payments if your Minnesota tax liability is more than $500.

California State Tax Extension

You do have to file a form to get an extension in California, but let's be honest: the form is little more than a coupon. It is Form FTB 3519. California requires estimated tax payments if your California Adjusted Gross Income is more than $150,000.

More information here:

Should I Do My Own Taxes or Pay Someone?

Why Not Just Put Off Your Taxes?

Now that you know how easy it is to file an extension, why not just do your taxes in the fall every year? Well, the problem is the estimate. While it is pretty easy to get a good estimate if you are only missing a K-1 or two, it would be very difficult without doing most of your taxes in April anyway. Do as much as you can now and then when your K-1s finally come into your possession, put the finishing touches on your federal and state taxes and send them in.

If you need help with tax preparation or you’re looking for tips on the best tax strategies, hire a WCI-vetted professional to help you figure it out.

What do you think? Have you ever filed an extension? How come? Are you more likely to consider doing so now that you've read this? Comment below!

[This updated post was originally published in 2019.]

The post How to File a Tax Extension appeared first on The White Coat Investor - Investing & Personal Finance for Doctors.

||

----------------------------

By: The White Coat Investor

Title: How to File a Tax Extension

Sourced From: www.whitecoatinvestor.com/how-to-file-a-tax-extension/

Published Date: Mon, 10 Apr 2023 06:30:57 +0000

Read More

Did you miss our previous article...

https://peaceofmindinvesting.com/investing/pickleballs-latest-sensation-is-a-firstyear-medical-student-who-just-came-out-of-nowhere

.png) InvestingStocksToolsClubsVideosPrivacy PolicyTerms And Conditions

InvestingStocksToolsClubsVideosPrivacy PolicyTerms And Conditions