<iframe style="width:120px;height:240px;" marginwidth="0" marginheight="0" scrolling="no" frameborder="0" src="//ws-na.amazon-adsystem.com/widgets/q?ServiceVersion=20070822&OneJS=1&Operation=GetAdHtml&MarketPlace=US&source=ss&ref=as_ss_li_til&ad_type=product_link&tracking_id=peaceinvesting-20&language=en_US&marketplace=amazon®ion=US&placement=0060555661&asins=0060555661&linkId=80f8e3b229e4b6fdde8abb238ddd5f6e&show_border=true&link_opens_in_new_window=true"></iframe>|<iframe style="width:120px;height:240px;" marginwidth="0" marginheight="0" scrolling="no" frameborder="0" src="//ws-na.amazon-adsystem.com/widgets/q?ServiceVersion=20070822&OneJS=1&Operation=GetAdHtml&MarketPlace=US&source=ss&ref=as_ss_li_til&ad_type=product_link&tracking_id=peaceinvesting-20&language=en_US&marketplace=amazon®ion=US&placement=1119404509&asins=1119404509&linkId=0beba130446bb217ea2d9cfdcf3b846b&show_border=true&link_opens_in_new_window=true"></iframe>|<iframe style="width:120px;height:240px;" marginwidth="0" marginheight="0" scrolling="no" frameborder="0" src="//ws-na.amazon-adsystem.com/widgets/q?ServiceVersion=20070822&OneJS=1&Operation=GetAdHtml&MarketPlace=US&source=ss&ref=as_ss_li_til&ad_type=product_link&tracking_id=peaceinvesting-20&language=en_US&marketplace=amazon®ion=US&placement=1119376629&asins=1119376629&linkId=2f1e6ff64e783437104d091faaedfec7&show_border=true&link_opens_in_new_window=true"></iframe>

By Dr. Daniel Smith, WCI Columnist

I’m going to ask a blunt question. How much has your income risen over the last five years? Was it at least 21%? I’ll tell you that the rents from my rentals and home values certainly have; however, my physician income per patient has most certainly not. I’m asking because that’s how much inflation has risen over the same time period. In fact, if I could go back five years ago, I’d have bought another eight rentals at the outset.

Even with the COVID eviction moratorium, the income from my rentals actually increased slightly more than inflation—about 23%. The best part I haven’t mentioned yet is the principal paydown of another ~9% and the home value increase of nearly 40% over the same time period! Even by leaving out mortgage principal paydown and property value appreciation, my rental income beat inflation, as any investor worth their salt is looking to do.

But let’s contrast that with physician-owner situations. I’d bet that if you own your practice, your staffing costs increased by at least 21%, not to mention prices for consumables, rent, utilities, and other back-office expenditures. If you’re an employed physician, have you noticed your employer or hospital cutting back on spending and scrutinizing costs with an increasingly jaundiced eye? The reason, which we all can guess, is due to inflation. But why should physicians accept lower and lower relative incomes when just about everything else is becoming more costly?

Why Care About Inflation?

Inflation is simply the increase in costs for goods and services over time. However, for the physician, inflation is the carbon monoxide of fixed wages, a slow and seditious denigration of your financial health. It’s one of Bill Bernstein’s big four threats to your wealth: inflation, deflation, devastation, and confiscation.

Confiscation by the government or another entity is uncommon in America because our legislation is predicated upon English Common Law, which holds the ownership of property as a citizen’s right. Devastation is certainly possible for those whose incomes are subject to natural and man-made disasters, like the Dust Bowl of the 1930s which decimated farmers and those upon whom they relied or the financial crisis of 2008 which relied upon the stability of mortgage payments. Deflation in America is also uncommon with the most recent example being the Great Depression where prices dropped 7%-10% per year from 1930-1933.

Inflation in small doses, according to many economists, has a neutral to positive effect on an economy: making exports cheaper to foreign buyers, making debt “cheapen” as time passes (i.e. your one dollar you owe your bank is worth 21 cents less in purchasing power now than five years ago), and encouraging companies to borrow to build new things and create more jobs. Inflation that gets readers’ attention tends to be that of countries in financial stress: Venezuela (at nearly 10,000%!), Zimbabwe, and Iran, for example.

High inflation erodes purchasing power and, thus, public confidence that tomorrow’s needs might not be met with tomorrow’s dollars. Panic-buying ensues, which pushes inflation higher. Fortunately, we don’t have runaway inflation thanks to the Federal Reserve mandate of low, stable inflation (monetary policy like raising interest rates or the sale of securities on its balance sheet) and a previous history of good financial policy and prudence on the legislative side. Then, why the concern with our low to moderate inflation?

It's because . . .

Physician incomes lag inflation . . . considerably.

The 21% figure I quoted above came from the Consumer Price Index (CPI), as measured from February 2021-February 2023. The federal government measures the CPI to help it determine what the inflation rate is and has been. The CPI guides our central bank’s decisions about monetary policy (federal discount rate, bond purchasing, and reserve requirements) and our legislators regarding fiscal policy (tax and spend; i.e. the budget). The CPI also drives inflation-adjusted rates on Social Security benefits, federal workers’ pay, and elective deferral limits for qualified retirement plans. Conspicuously absent from the list of inflation-adjusted federal expenditures is Medicare pay rates for physicians.

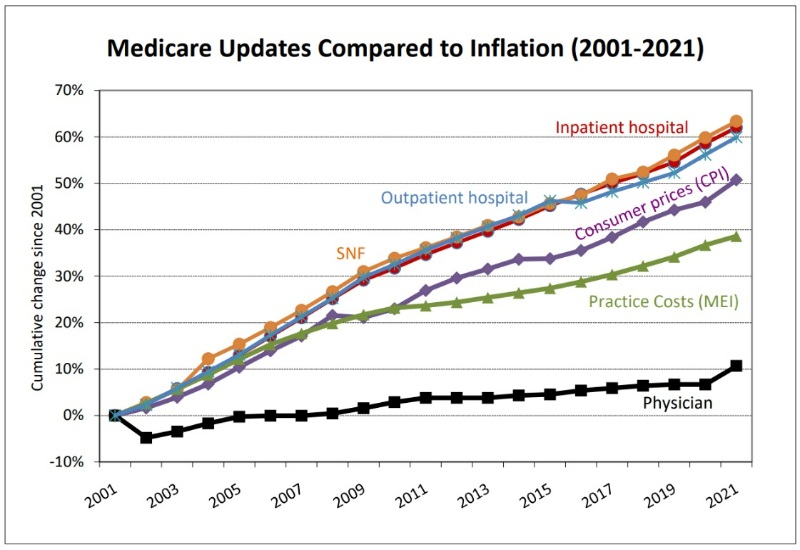

Inflation concerns are not new, however. In 2021, the AMA released this graph of the CPI compared against pay increases for acute-care hospitals, skilled nursing facilities, and outpatient hospitals. Trundling along at the bottom is physician pay—which, from 2001-2021, increased a marginal 10.5% while the CPI increased 50%. This means that over the course of that 20-year span, physician incomes dropped by 39.5% in after-inflation dollars. Further, the cost of just running physician practices increased by nearly 40% nominally.

Why is this happening? Originally, CMS (Center for Medicare and Medicaid Services) was tasked to measure increases in expenditures. It anticipated future growth by compiling the Medicare Economic Index (MEI, seen above in green) and projecting the sustainable growth rate (SGR) by which physician pay raises were determined annually. In 2015, a Republican legislature and a Democratic president (so that everyone can be equally incensed) signed into law MACRA, which changed physician reimbursement from the SGR to a collection of metrics presented as a way to move physicians to value-based care.

For anyone grousing about how Congress is made up of career politicians who don’t have a clue about the sector they’re legislating, this bill was sponsored by a retired OB-GYN from Texas. For the record, Congresspeople vote themselves their own pay increases.

More information here:

You Can’t Hedge Against Inflation in the Short Term

What to Do About Physician Incomes During High Inflation?

#1 You Could Do Nothing

Physician incomes, by any measure, are far above average, and far be it from me to suggest you spend more of your precious time doing anything other than what you value highly. No doubt that as inflation increases, your nominal, though not your real, earnings will increase with time. If you are content to have less purchasing power over time, then feel free to skip the rest of this column and spend your morning how you please. If I were near retirement or was part of a high-income DINK (Double Income, No Kids) couple, I’d probably feel this way too.

#2 You Could Spend Less and Save More

Rarely a bad idea, unless you’re already a miser anyhow, and one that probably most of us could use a bit more of. The problem with spending less and saving more is that it’s an uphill battle. I can’t continue to spend commensurately less as inflation erodes my purchasing power just to keep up with what I am making.

#3 You Could Make More Money

Now there’s my kind of idea. Granted, most docs work plenty of hours, and for most of us, working only plenty of hours would be an improvement in our work schedule. Instead, I’m lobbying for leveraging your most valuable asset—your medical degree and future earning potential—for producing income that keeps up with inflation.

A Call to Action for Side Hustles

Ben Franklin is quoted as having said, “If you fail to plan, you plan to fail.” So, the first step after recognizing the problem with physician pay is to make a plan. Some of this is going to sound a little unconventional, but stay with me.

Figure Out Which Debt to Carry and Which Debt to Erase

We know that good debt is usually fixed rate, non-callable, and low interest—and for a good reason. Credit card debt is bad because it’s high-interest rate. Margin loans are bad because they’re callable (if your speculative asset drops in value, you’re getting a call from your broker for cash) and usually not low interest. Loans for cars are generally foolish; let’s all admit you just bought too much car. Josh Katzowitz, I’m talking to you here.

Home mortgages tend to be good for all four reasons above. Loans for practice improvement, expansion, and purchase can be good, given they improve revenue streams and are on reasonable terms. Carrying some low-interest, consolidated student loan debt can also be good debt to carry because it frees up cash for you to invest or to use for your financial benefit.

Figure Out What Your Side Hustle Will Be

Most of us possess arguably the most difficult professional credential to obtain in the United States. It is a gateway for multiple kinds of side hustles: medical directorships, IV fluids bars, medical spas, locums physicians, urgent care, professorships, research opportunities, consulting, concierge medicine, chart review for attorneys or insurance companies, sideline sports coverage, those surveys Rikki Racela made so much money on. The list is far longer than any of these, but these are the ones that come quickly to mind. For those who say that jobs where physicians practice medicine are subject to the same pay problem, that’s correct. However, because it is a side hustle, you have leverage in that you have the freedom to negotiate. If the pay isn’t high enough, do something else!

If medically oriented side hustles aren’t your preference, then by all means do something completely unrelated. WCI readers are go-getters, or you wouldn’t have gotten into medicine. Find an unmet need that you believe you can fill, and do it. If you have a passion for wine, open a bar specializing in Spanish vintages. If you’re excellent with computers, try to contract with some local practices to be their impromptu IT guy on a case-by-case basis. If you aren’t already well-versed in some prosaic skill or trade, read up on a new one!

Doctors are lifelong students by nature and by necessity. Transfer some of that ability to learning a new skill or getting a new degree. A colleague of mine just finished his MBA, and he was amazed at the new world of possibilities open to him. Maybe you start a small blog on physician finance that becomes a huge success to the degree that it overshadows your physician income (I think, though, that niche might have already been taken).

On the investment side, your large incomes all mean that you are or will be accredited investors, opening up riskier but potentially more lucrative investments available only to you. While it’s not as active as some other hustles, it’s also something that is out of reach for many people because of the requirements. Maybe you buy a timber farm (an aspirational investment of mine) which is mostly passive, or rental real estate or vacation homes, etc. There’s an ENT in my town who derives the majority of his income from passive investments in mixed-use commercial and residential buildings rather than his income as a surgeon solely because he had the capital and borrowing capacity to make it work.

For my part, I have a few rentals (which have done well given higher rents and fixed debt), write for this blog (by the way, how about a cost of living adjustment??), and have a couple more buckets under the sluice which I’m hoping will pan out. If those do work out, I’ll be sure to write about them.

More information here:

The List of Physician Side Hustles

From Medicine to Entrepreneurship: How Side Hustles Are Changing the Physician Landscape

The Bottom Line

Physicians have a real (income) problem with inflation. We are at the blackjack table, and Medicare is dealing. Outside of a permanent Medicare fix (debt? What debt?), our best option is to create one or more income streams that are free to rise as inflation does. If you’ve got a great inflation-hedging side hustle, I’d love to hear about it.

As a doc, you have valuable knowledge and information. Various companies want that knowledge and are willing to pay you for it. If you're interested in starting a side hustle as a paid survey-taker while also making a difference in the medical field, check out our favorite physician survey companies today!

Are you using a side hustle as an inflation hedge? What is it? How well is it working? Is all of this worth your time? Comment below!

The post Side Hustles: The Real Inflation Hedge appeared first on The White Coat Investor - Investing & Personal Finance for Doctors.

||

----------------------------

By: Josh Katzowitz

Title: Side Hustles: The Real Inflation Hedge

Sourced From: www.whitecoatinvestor.com/side-hustles-the-real-inflation-hedge/

Published Date: Mon, 11 Sep 2023 06:30:56 +0000

Read More

Did you miss our previous article...

https://peaceofmindinvesting.com/investing/this-is-what-i-learned-on-my-trip-to-israel

.png) InvestingStocksToolsClubsVideosPrivacy PolicyTerms And Conditions

InvestingStocksToolsClubsVideosPrivacy PolicyTerms And Conditions