<iframe style="width:120px;height:240px;" marginwidth="0" marginheight="0" scrolling="no" frameborder="0" src="//ws-na.amazon-adsystem.com/widgets/q?ServiceVersion=20070822&OneJS=1&Operation=GetAdHtml&MarketPlace=US&source=ss&ref=as_ss_li_til&ad_type=product_link&tracking_id=peaceinvesting-20&language=en_US&marketplace=amazon®ion=US&placement=0060555661&asins=0060555661&linkId=80f8e3b229e4b6fdde8abb238ddd5f6e&show_border=true&link_opens_in_new_window=true"></iframe>|<iframe style="width:120px;height:240px;" marginwidth="0" marginheight="0" scrolling="no" frameborder="0" src="//ws-na.amazon-adsystem.com/widgets/q?ServiceVersion=20070822&OneJS=1&Operation=GetAdHtml&MarketPlace=US&source=ss&ref=as_ss_li_til&ad_type=product_link&tracking_id=peaceinvesting-20&language=en_US&marketplace=amazon®ion=US&placement=1119404509&asins=1119404509&linkId=0beba130446bb217ea2d9cfdcf3b846b&show_border=true&link_opens_in_new_window=true"></iframe>|<iframe style="width:120px;height:240px;" marginwidth="0" marginheight="0" scrolling="no" frameborder="0" src="//ws-na.amazon-adsystem.com/widgets/q?ServiceVersion=20070822&OneJS=1&Operation=GetAdHtml&MarketPlace=US&source=ss&ref=as_ss_li_til&ad_type=product_link&tracking_id=peaceinvesting-20&language=en_US&marketplace=amazon®ion=US&placement=1119376629&asins=1119376629&linkId=2f1e6ff64e783437104d091faaedfec7&show_border=true&link_opens_in_new_window=true"></iframe>

Key Takeaways

- 2022 continues to be challenging for investors. The third quarter was a tale of two halves. In July and early August, stocks and bonds rallied on speculation for a potential Fed “pivot” back toward more accommodative policy. The tide shifted abruptly with the August consumer inflation report.

- GDP has declined two quarters in a row. Like most economists and market participants, we suspect the economy will worsen before it gets better, though we view the timing and outcome as far less certain than many suggest.

- Staying committed to a diversified strategy and periodically rebalancing provides one of the best chances for success. It also reduces the odds of a debilitating behavioral mistake. Every bear market feels awful and scary, and all of them come to an end.

- Global stocks cost 25% less than they did at the beginning of the year. We are deep into this bear. The final phases tend to be dramatic, but so are the recoveries and you don’t want to miss them. .

Inflation paired with falling stock and bond prices continue to make 2022 a historically challenging year for investors. The third quarter was a tale of two halves. In July and early August, stocks and bonds rallied on speculation for a potential Fed “pivot” back toward more accommodative policy. Investors eagerly scooped up positions at lower prices than they were accustomed to.

The tide shifted abruptly with the August consumer inflation report, which delivered an 8.3% headline number. Though only modestly ahead of expectations, the result dashed hopes that inflation was already in decline and prompted more aggressive rhetoric from the Fed and other central banks.

Market fixation on the Fed and other central banks leaves us in a period where good news for the economy is bad news for stocks, and vice versa. The Fed raised short rates by 0.75% in September and indicated more to come at the next meeting in early November. Chairman Powell indicated several times that some “pain” in the economy would likely be required to tame inflation. After more than a decade of the Fed coming to the rescue at seemingly any sign of market weakness, inflation has truly and dramatically changed the approach.

For the quarter, U.S. stocks lost 4.9% and international stocks were down 11.2%, largely due to a surging dollar. The U.S. aggregate bond market surrendered another 5.1%.

We appreciate how discomforting bear markets are. Market returns impact wealth and lifestyle. For better or worse, conditions are likely to remain volatile.

Economic Slowdown

GDP has already declined two quarters in a row, but like most economists and market participants, we believe the economy will worsen before it gets better. We also think the outcome is far less certain than many suggest. People and economies tend to be more resilient than often given credit for. Interestingly, the job market remains relatively strong, although there are increasing signs of cracks. A softer jobs market may slow consumer demand but should help support corporate profit margins overall. Most bear markets start to recover only after there has been an increase in unemployment.

The usual narrative for economic slowdown points to high inflation and falling asset prices causing households to reduce spending. The tone from corporate America has also become decidedly less enthusiastic. Home values are just beginning to tip, with prices falling nationally for the last two months. Mortgage rates are now roughly double from the start of the year (currently 6.7% according to Freddie Mac), so further price declines should be expected. We do not expect the magnitude to be anywhere near that of the subprime crisis when mass foreclosures flooded the market. This cycle features higher credit quality as well as a much greater prevalence of fixed rate mortgages. Still, higher mortgage rates and general uncertainty are causing a sharp drop in home sale volume, which is a great source of economic activity touching many sectors.

Overseas, things are not much brighter. China is navigating a potential real estate crisis, Europe faces a likely energy crisis, and the ongoing war in Ukraine adds uncertainty and even the potential for the use of nuclear weapons.

Why Stay Invested?

Given the rather bleak global backdrop, where it seems almost everyone “knows” things are going to get worse, many are asking, “Why should I be invested now?” In our view, the answer is simple. Staying committed to a diversified strategy and periodically rebalancing provides one of the best chances for success. It also reduces the odds of making debilitating behavioral mistakes.

Every bear market feels awful and scary. And all of them come to an end. The best opportunities often surface when pessimism is widespread. Inflation is a serious issue, but we believe the macro environment now is significantly less perilous than the Covid shutdowns in 2020, the financial crisis in 2008, and several other times of crisis before that. Global stocks cost about 25% less than they did at the beginning of the year. Meanwhile, most of the money printed during the pandemic is still sloshing around and can help support higher asset prices.

Bear markets come in many shapes and sizes. The average bear since 1950 declined roughly 35% from peak to trough, lasting about a year and a half. Some have been shorter and less severe, others longer and stronger. No one should be surprised if either there are more down months ahead, or if a recovery begins soon. No matter how you look at it, we are deep into this bear. The final phases tend to be dramatic, but so are the recoveries and you don’t want to miss them. One of the biggest risks for long-term investors has always been selling low when the going gets rough.

Recessions and bear markets surface in most decades, often more than once. They should be expected. But the natural state of the economy, population, money supply, earnings, and stock prices are growth. Despite the disappointing state of the world in many regards, we don’t see any reason why these fundamental conditions have changed.

Barring emotional mistakes, one year does not make or break a thoughtful plan.

Worried about this bear market’s impact on your long-term plans? Get perspective with our Retirement Planner by visualizing the impact of historic market downturns.

Sticking with a strategic asset allocation doesn’t mean doing nothing. Volatility presents increased opportunities to benefit from rebalancing and tax-loss harvesting. Benefits from these tactics can feel incremental in years when there are big market moves, but they compound over time to generate a very tangible difference in ultimate results.

Bonds

Fed funds (a measure of short-term interest rates) sits at a little over 3% and is expected to climb to somewhere in the 4%-4.5% range over the next six months. This does not mean bonds will necessarily fall further in price. Short to intermediate Treasuries already reflect aggressive Fed moves still to come. For example, if rates increase by 1% over the coming year and then remain flat, a two-year Treasury bond owned now will both increase in price AND pay over 4% a year in yield along the way.

Bonds with long maturities are less reactive to Fed moves, but prices have greater sensitivity when longer-term interest rates change. If short rates shoot past 4%, the implication is that either long bonds endure declines, or the yield curve becomes quite inverted. Longer term bonds may be a better hedge to significant economic slowdown, but they come with more risk. Personal Capital managed bond portfolios have exposure across the yield curve while remaining more heavily weighted to short and intermediate term bonds. This year, that has helped.

The bond mix in managed portfolios currently offers a similar or higher yield than the aggregate bond market, while taking less interest rate risk. This is achieved in part through more credit risk, however.

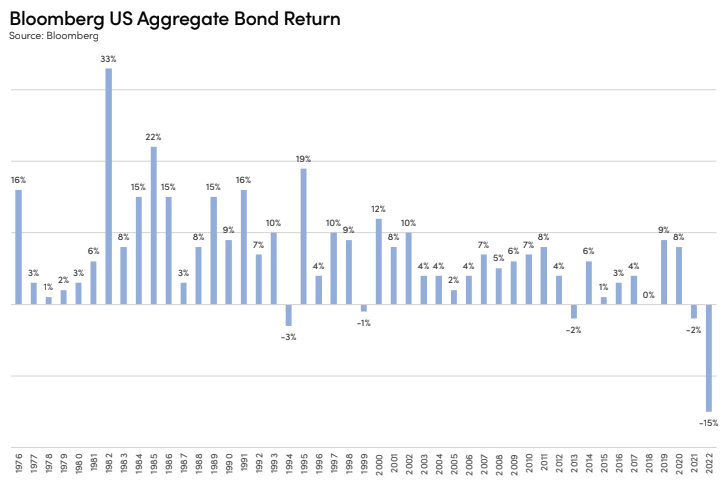

Like almost everyone, we have been surprised by the swiftness of rising interest rates. Bonds have been less volatile than stocks this year, but losses in the U.S. Aggregate bond market are five times greater than any year since 1976. With a strengthening dollar, international bonds are doing even worse.

It is very rare for bonds to deliver a negative absolute return over three-year periods, but it appears it will take at least that long to recoup losses from this year. Still, for those with a longer-term view, a historically awful 2022 may be an important silver lining. Higher interest rates should translate to better absolute returns for years to come, making retirement planning easier along the way. Ultra-low interest rates were like steroids for stocks, but they created unnatural behavior in many regards, causing significant challenges for many.

The return to more normal rate levels does not preclude strong returns from stocks. For example, interest rates for most of the 1990s were higher than we see now, and it was one of the most prolific decades for equities of all time.

Where are we headed now?

Recent trends in stock prices tell us relatively little about which direction they will head next. Volatility, on the other hand, does tend to beget more volatility, and we should expect significant moves in both directions to persist.

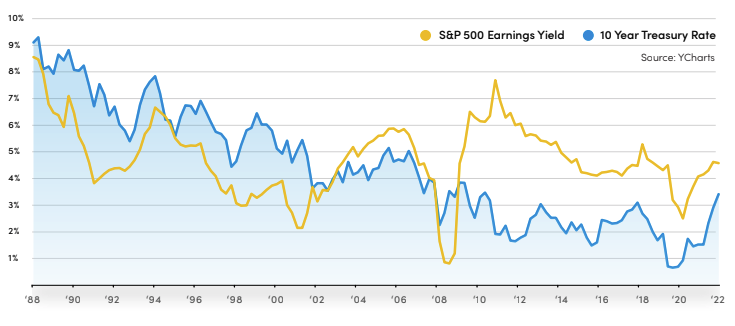

Equities are considerably cheaper than they were at the beginning of the year, with prices down even as earnings are climbing. At the end of Q3, the trailing PE of the MSCI All Country World index was 15.5, implying an earnings yield of 6.5%. Compared to bond yields in the 3-4% range, this is relatively attractive. International stocks trade at just 12.5x earnings.

For much of the last 30 years, 10 Year Treasury yields were higher than the S&P 500 earnings yield (the trailing PE ratio flipped on its head). That meant you could get a higher immediate yield with lower risk bonds. Currently, stocks provide a significantly higher yield, even more so if you use forward looking earnings. While not a good short-term indicator, this is generally bullish, especially because earnings should continue to grow over time while bond coupons generally do not.

Valuations should provide some comfort to those with a long-term view, especially for global investors, but they tell us little about the next six months. Just as investors can become irrationally exuberant around bull market peaks, extreme pessimism can push valuations to irrational lows.

Until recently, extreme valuations in growth stocks created an overhang for the U.S. equity market. This has now largely corrected itself already. Nine months ago, it was hard to find a growth stock that felt approachable but now many do. Even so, the momentum swing toward value could easily persist.

Sentiment is a contrarian indicator in our view. At the start of the year, complacency was a red flag. Now, pessimism pervades, making sentiment a bullish indicator to us. We still lack the despair and mass-capitulation like that felt at the bottoms in 2003 and 2009, but it feels closer.

Headlines and risks

Inflation, interest rates and earnings should continue to be the main drivers of asset prices, but there are a host of other issues making headlines and stoking fear. The following are brief summaries on some of them:

Russia and Ukraine

Russia’s war on Ukraine drags into its eighth month, upending millions of lives, creating commodity shortages, and adding uncertainty to the global geopolitical situation. While capital markets appear to have little concern for the day-to-day evolution of the war, Ukraine’s surprising and impressive resiliency increases the likelihood that Russia will resort to exacerbating energy shortages in Europe this winter. It also raises the possibility of the use of nuclear weapons.

In Europe, gas prices have reached record highs and supplies are running low. Several EU states have created emergency plans that may lead to blackouts and energy rationing this winter. The problems are multi-faceted. Higher energy costs create general inflation pressures as well as energy poverty for millions of households who must choose between cold homes and other necessities. Some energy intensive manufacturing activity is being curtailed.

The region has been stockpiling reserves and developing other energy supplies, so the worst may be avoided. Much will depend on the severity of the weather. All this creates uncertainty for commodity markets and will likely push Europe deeper into recession. However, it is also all very well-known, widely discussed and expected. This leaves equity markets roughly equally likely to be disappointed or pleasantly surprised with the outcome, in our view.

Unfortunately, based on Putin’s actions and words, it is clear he views the U.S. and the West as a threat and adversary. The “peace dividend” of the supposed end to the Cold War may have to be repaid. Russia’s ability to align with China ideologically will be important and is yet another great unknown.

The U.S. dollar

Times of stress have often sparked a flight to the safety of the U.S. dollar, and we are seeing it again this year. More aggressive interest rate hikes in the U.S. is also stoking demand for dollars. The ICE U.S. Dollar Index ended Q3 up 17% for the year and the Euro dipped below parity with the dollar for the first time since 2002.

A stronger dollar has several implications. Among them are:

- It limits inflation in the U.S. while fueling it overseas.

- For most U.S. companies with international sales, it reduces earnings. This hits some sectors harder than others, especially technology.

- The value of international assets is proportionally reduced in dollar terms. The MSCI All Country ex U.S. Index is down 26.5% in dollars, but only 16.2% in local currency.

- It constrains commodity prices (as quoted in dollars).

Currencies can be as difficult to predict as economic cycles or stocks, but in our view the best indicator is purchasing parity. As it stands, the dollar goes quite far overseas, suggesting it may have become somewhat overextended. For international equities, in addition to being cheaper on a price to earnings basis, we suspect the currency headwind may soon shift to a currency tailwind

Midterm elections

The upcoming elections are proving to be more interesting than expected with both houses of Congress now up for grabs. Whichever party controls the White House typically loses seats in midterms, but Republican momentum lost steam following the reversal of Roe v. Wade. According to FiveThirtyEight.com, Republicans are favored to regain control of the House while Democrats are moderately favored to keep the senate (which is currently divided 50-50 with the tie-breaking vote going to the Vice President). In each case, whichever party wins will likely do so narrowly.

As it relates to asset prices, elections and which political party is in power tends to matter less than most people believe. Historically, stocks happily marched higher at a similar pace regardless. Divided government is often a good backdrop for stocks because it leads to less legislation and less likely change or uncertainty. While suspenseful for those interested, we don’t expect these midterms to have much impact on markets. The Presidential election in two years may be a different story if it drives the nation to become further divided and acrimonious.

The Inflation Protection Act

This legislation is a slimmed-down version of the original Build Back Better bill. We don’t expect it will reduce inflation overall, as the name suggests, though it will help some people with health care costs. Some meaningful provisions include:

- Continued subsidies for health insurance created under the Affordable Care Act

- It allows Medicare to negotiate the price of certain prescription drugs

- Corporations with at least $1 billion in income will have a minimum 15% tax rate

- $80 billion to the IRS to enforce tax payments

- Numerous investments in climate protection, clean energy production and carbon reduction.

Ultimately, the bill feels more appropriate than the original massive spending proposal. The Congressional Budget Office estimates it will reduce the deficit by about $100 billion over the next decade. It is a win for the environment. We don’t see much impact on capital markets one way or another.

Inflation

Inflation can be more damaging than bear markets. CPI reports in June and September were disheartening because many expected to see inflation start to decline. We take inflation risk very seriously but urge people not to panic. Looking beyond 2022, we concur with the Fed outlook that price increases should moderate. There are several factors supporting this:

- The Fed is prioritizing price stability above growth.

- There is a high chance we are or will soon be in a recessionary environment.

- Higher mortgage rates are beginning to impact home prices, which should lead to lower rental costs as well.

- Supply chain issues should abate over time and are likely already improving.

- The temptation for U.S. shale companies to drill more should eventually prove irresistible.

- Innovation and technology continue to drive efficiencies.

- The five-year breakeven rate for TIPS is just 2.4%, which is the lowest since late February.

Many high-priced growth stocks have been decimated in recent quarters, and those concentrated in this area remain at higher risk in our view. Earnings expected far in the future are generally worth less now if interest rates and inflation rise.

While markets are likely to remain volatile and unpredictable, cash is losing value to inflation. This makes it more important to properly evaluate extra cash beyond typical emergency fund levels. One of the best places for cash that isn’t expected to be used for many years is generally in a properly diversified long-term growth portfolio.

For short term cash, yields have moved away from zero and it has again become worthwhile to manage appropriately. The biggest national banks often have some of the worst interest rates on checking and saving accounts.

Tip: Get 2.60% APY1 on Personal Capital Cash

, a flexible cash account.

*As of October 2022

This communication and all data are for informational purposes only and do not constitute a recommendation to buy or sell securities. Third party data is obtained from sources believed to be reliable. However, PCAC cannot guarantee that data’s currency, accuracy, timeliness, completeness or fitness for any particular purpose. Certain sections of this commentary may contain forward-looking statements that are based on our reasonable expectations, estimate, projections and assumptions. Forward-looking statements are not guarantees of future performance and involve certain risks and uncertainties, which are difficult to predict. Past performance is not a guarantee of future return, nor is it necessarily indicative of future performance. Keep in mind investing involves risk. The value of your investment will fluctuate over time and you may gain or lose money.

The content contained in this blog post is intended for general informational purposes only and is not meant to constitute legal, tax, accounting or investment advice. You should consult a qualified legal or tax professional regarding your specific situation. Keep in mind that investing involves risk. The value of your investment will fluctuate over time and you may gain or lose money.

Any reference to the advisory services refers to Personal Capital Advisors Corporation, a subsidiary of Personal Capital. Personal Capital Advisors Corporation is an investment adviser registered with the Securities and Exchange Commission (SEC). Registration does not imply a certain level of skill or training nor does it imply endorsement by the SEC.

1 Personal Capital Cash is offered through Personal Capital Services Corporation (Personal Capital). Personal Capital is not a bank. Bank deposit products provided by UMB Bank n.a., Member FDIC. To participate in the program, you must open an account at UMB Bank, through which your funds will be placed in accounts at participating program banks. The advertised interest rates are paid by participating program banks, not by UMB. Your funds will be FDIC insured up to applicable limits while in transit through UMB Bank. Personal Capital receives a fee from each Program Bank in connection with the Program that is based on the aggregate daily closing balance of deposits held in Program Accounts by such Program Bank. The fee may vary from Program Bank to Program Bank and will generally increase as the aggregate amount of funds held in Program Accounts with the Program Bank increases. The Personal Capital Cash

Annual Percentage Yield (APY) as of 9/28/22 is 2.60% APY (2.570% interest rate). The calculation for APY is rounded to the nearest basis point. For Personal Capital advisory clients, the APY is 2.70% (2.667% interest rate). Both the interest rate and APY are variable and subject to change at our discretion at any time without notice.

||

----------------------------

By: Craig Birk, CFP®

Title: Market Review & Outlook: U.S. Investors Brace for Market Swings

Sourced From: www.personalcapital.com/blog/investing-markets/market-review-outlook-q3-2022/

Published Date: Tue, 01 Nov 2022 00:04:24 +0000

Read More

Did you miss our previous article...

https://peaceofmindinvesting.com/investing/how-to-add-adventure-to-your-life

.png) InvestingStocksToolsClubsVideosPrivacy PolicyTerms And Conditions

InvestingStocksToolsClubsVideosPrivacy PolicyTerms And Conditions