<iframe style="width:120px;height:240px;" marginwidth="0" marginheight="0" scrolling="no" frameborder="0" src="//ws-na.amazon-adsystem.com/widgets/q?ServiceVersion=20070822&OneJS=1&Operation=GetAdHtml&MarketPlace=US&source=ss&ref=as_ss_li_til&ad_type=product_link&tracking_id=peaceinvesting-20&language=en_US&marketplace=amazon®ion=US&placement=0060555661&asins=0060555661&linkId=80f8e3b229e4b6fdde8abb238ddd5f6e&show_border=true&link_opens_in_new_window=true"></iframe>|<iframe style="width:120px;height:240px;" marginwidth="0" marginheight="0" scrolling="no" frameborder="0" src="//ws-na.amazon-adsystem.com/widgets/q?ServiceVersion=20070822&OneJS=1&Operation=GetAdHtml&MarketPlace=US&source=ss&ref=as_ss_li_til&ad_type=product_link&tracking_id=peaceinvesting-20&language=en_US&marketplace=amazon®ion=US&placement=1119404509&asins=1119404509&linkId=0beba130446bb217ea2d9cfdcf3b846b&show_border=true&link_opens_in_new_window=true"></iframe>|<iframe style="width:120px;height:240px;" marginwidth="0" marginheight="0" scrolling="no" frameborder="0" src="//ws-na.amazon-adsystem.com/widgets/q?ServiceVersion=20070822&OneJS=1&Operation=GetAdHtml&MarketPlace=US&source=ss&ref=as_ss_li_til&ad_type=product_link&tracking_id=peaceinvesting-20&language=en_US&marketplace=amazon®ion=US&placement=1119376629&asins=1119376629&linkId=2f1e6ff64e783437104d091faaedfec7&show_border=true&link_opens_in_new_window=true"></iframe>

Each quarter, our investment team comments on the markets and economy over the past quarter and looks forward at what the next period might bring.

Executive Summary

- Inflation forced the Fed and other central banks to raise interest rates and tighten liquidity in 2022. The results have been unpleasant, but in many regards market and economic activity this year has been logical. Unsustainable froth in some of the most speculative assets has been washed away, and equity prices overall probably better reflect the new interest rate reality. Persistent inflation and deeper recession remain risks, but we believe macro conditions have significantly progressed toward a healthier state to support sustained growth.

- The biggest driver for the Q4 bounce was probably lower than expected inflation reports. Official US inflation peaked at over 9% in June and was 7.1% in November. A slowing inflation rate adds credibility to the hope that the central bank will eventually begin reversing rate hikes.

- Equity gains in Q4 were concentrated in value stocks. The situation remained grim for most investors concentrated in the trendy high-flyers from 2020-2021.

- We believe inflation will continue to moderate in the coming year, while staying well above the Fed’s 2% target, but there is no way to have high confidence. If we are right, there is a path for rates to stabilize and demand for stocks to increase. However, the fact that our outlook is widely shared means risk may be skewed to the downside if inflation and interest rates stay higher longer.

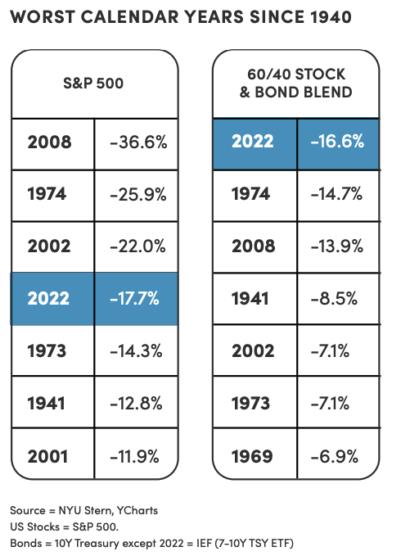

- Bonds had the worst year in modern times. Sentiment toward them is very low. Many people simply don’t want to own fixed income. We think this is a mistake and strongly believe bonds should remain an important allocation in most portfolios. Higher yields create losses in the short term but can drive higher return over time.

- Bear market fatigue is real. This bear market is nearing the average length but remains shallow in terms of average peak to trough drop. Many investors end up giving up on stocks at close to the worst time. Every bear market feels awful and scary. And all of them come to an end. The best opportunities often surface when pessimism is widespread.

Download report as a PDF

In the wake of the initial Covid shutdowns, an unexpected phenomenon occurred: extreme investor enthusiasm. The world didn’t suddenly get better, but by late 2020 ultra-low interest rates, fiscal stimulus, and quarantines combined to create rapidly rising home prices, a meme-stock craze, Bored Apes, skyrocketing crypto prices, and tech stocks partying like it was 1999.

Inflation then began knocking on the door in mid-2021 and spiked higher in early 2022. This quickly changed the market dynamic by forcing the Fed and other central banks to raise interest rates and tighten liquidity. The results have been unpleasant, but in many regards market and economic activity this year has been logical. Investment decisions at the corporate and individual level have generally become more measured. Unsustainable froth in some of the most speculative assets has been washed away, and equity prices overall probably better reflect the new interest rate reality. Persistent inflation and deeper recession remain risks, but we believe macro conditions have significantly progressed toward a healthier state to support sustained growth.

For the full year, US stocks lost 19.5%. International stocks, which feature less tech and lower valuations, fared better, down 15.6%. Global bond prices declined sharply. 7-10 Year Treasuries (IEF) fell 15.1%, the most ever based on our data series, which begins in 1928.

In contrast to the full year, and with little fanfare, capital markets rallied in the fourth quarter. US Stocks gained 7.0% in the period. Rebounding currencies propelled international stocks, which surged 14.4%. US Bonds added 1.6% despite the Fed raising short rates by 0.75% in November and 0.5% in December. Yield on the US Aggregate bond market is currently around 4%. Stocks and bonds both rose in October and November, while December was down.

The biggest driver for the Q4 bounce was probably lower than expected inflation reports. Official US inflation peaked at over 9% in June. August and September were lower but still exceeded expectations. Readings of 7.8% in October and 7.1% in November, however, were well received. (source: YCharts, BLS). While still far above the Fed’s target of 2%, a slowing inflation rate adds credibility to the hope that the central bank will eventually begin reversing rate hikes. The tone from the Fed was stern, but the shift from 0.75% hikes to 0.50% also comforted investors’ anticipation of a “pivot” back to more accommodative policy.

S&P 500 year-over-year earnings declined 2.8% in the fourth quarter. This is generally considered a bad result, but it proved to be good enough because many were expecting a more dire scenario. Corporate revenues continue to expand, suggesting companies are facing inflation pressures as well.

Unemployment ticked up modestly to 3.7%. This remains low by historical standards but increasing layoff announcements have helped balance power between workers and employers. Most notable in the quarter were Meta Platforms cutting 10,000 jobs and Amazon slashing 11,000. Some slack in the labor market is a positive for companies seeking to maintain historically high profit margins.

The midterm elections also gave stocks a boost, partly because fears of contested elections and process breakdowns were removed. Republicans regained control of the House but failed to take the Senate. Both houses of Congress are nearly balanced. This type of divided government can be a constructive backdrop for stocks because it leads to less legislation and therefore more stability.

Equity gains during the quarter were concentrated in value stocks. The situation remained grim for most investors concentrated in the trendy high-flyers from 2020-2021. Richly priced growth companies continued to fall from grace. QQQ, the popular Nasdaq 100 ETF, was down almost 33% this year. A more extreme example is the formerly loved ARKK Innovation ETF, which lost over two-thirds of its value this year and is now down 80% off its 2021 peak value.

In this cycle, as in the dotcom bust, losses first appeared in the most speculative growth stocks, then spread to bigger more stable companies, including mega tech.

The seven most valuable companies at the start of the year (Apple, Microsoft, Alphabet, Amazon, Meta Platforms, Tesla and Nvidia) each fell more than the S&P 500 in 2022. The big losers from this list in Q4 were Tesla and Amazon. Single stock and single sector concentration can bring impressive gains, but they always come with risk. Smart Weighting in Personal Capital client portfolios limits exposure to any one company, which helped this year. Apple and Microsoft, the two biggest companies, have held up best within the group, leaving open the question if they may be the next shoe to fall.

Our investment approach is a process. It is designed to give our clients the best chances for success over time. It requires oversight, but it is not based on market predictions. We focus first on customized strategy selection, or asset allocation. Then we look to enhance diversification and seek out opportunities to benefit from efficiencies through actions like rebalancing and tax management. Our job is to follow the process, avoid distractions, and seek new technologies or tools to drive better outcomes.

Investing is a long game where success comes from consistency with results compounding over time. Despite this, we appreciate how discomforting bear markets can be.

Outlook

As always, several bullish and bearish factors are simultaneously doing battle. We think it is equally likely that stocks advance in Q1 and never look back, or that this bear will shake more people out with another sharp down move. Either way, when a new bull market arrives there is often considerable upside to be had in the early months and it is important to be there to capture it. Uncertainty remains somewhat elevated, in our view, but not to such a degree we would consider veering from strategic allocations.

Continued fixation on the Fed and other central banks leaves us in a period where good news for the economy is often bad news for stocks, and vice versa. Said another way, interest rate expectations currently have more impact on stock prices than the earnings outlook.

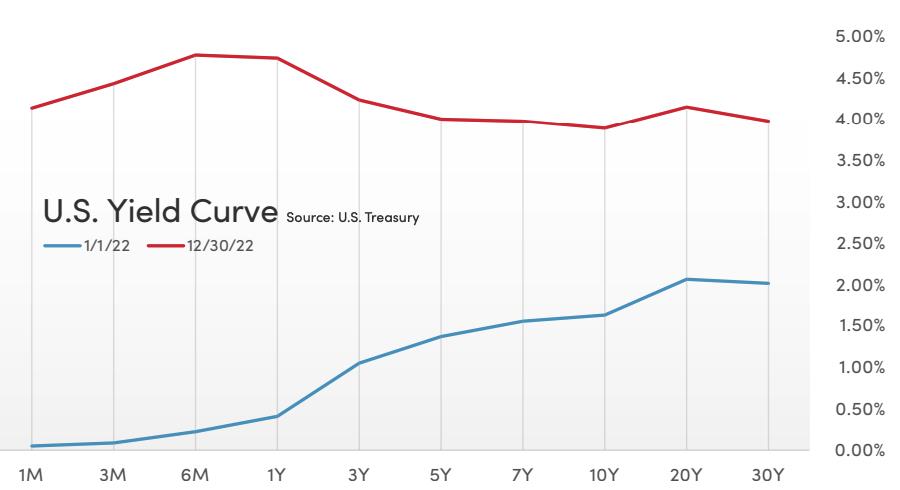

While further rate increases are almost universally anticipated, a disconnect has formed between what the Fed is saying and what the market seems to be expecting. Chairman Powell suggested we should expect short rates to surpass 5% and persist there for some time. However, at year-end, the peak of the US Treasury yield curve was a 4.67% at the six-month maturity mark. From there it is inverted, suggesting many market participants expect rates to peak in the first half of 2023 and start to decline before year-end or early in 2024.

We believe inflation will continue to moderate in the coming year, while staying well above the Fed’s 2% target, but there is no way to have high confidence. If we are right, there is a path for rates to stabilize and demand for stocks to increase. However, the fact that our outlook is widely shared means risk may be skewed to the downside if inflation and interest rates stay higher longer.

Regardless of the short-term outlook, it is highly likely that most of the rate hiking cycle is behind us. Stocks will not necessarily wait for an actual rate cut to show their enthusiasm.

Moving on from inflation and interest rates, the collapse in cryptocurrency prices and implosion of FTX is bullish in our view. Not because any positive comes from it, but because these events did not spread to the mainstream financial system. There was no reason to believe major banks were leveraged to crypto, but when two trillion dollars of perceived wealth evaporates and hedge funds start failing, contagion is a possibility. That risk is now greatly reduced. Also, crypto was probably the biggest posterchild of the froth and exuberance of 2020-2021. For this bear to ultimately be laid to rest and a new cycle to begin, a reset in crypto prices felt like a needed milestone. Regardless of whether crypto rebounds or shrinks further, that box is now checked.

This is not to say all is clear in terms of bank balance sheets or debt defaults. Leveraged loans have ballooned in recent years. Many companies which were struggling to stay afloat with low rates may sink under the burden of higher interest costs. Collateralized loan obligations (a more general term for mortgage-backed securities), a major villain of the subprime crisis, are also back again. Overall, bank stress models seem to be holding up well, though in this regard, bad news for the economy really would be bad news for banks.

On that note, US GDP growth was revised upward to 3.2% in the third quarter after declining in the first half of the year. One quarter does not tell the whole story, but the strong result means a shallow recession and rapid recovery remains quite possible. While stocks dropped the day of this announcement, another contraction would have been more concerning in our view. Inflation is currently job number one for the Fed, but people and economies are resilient.

The housing market poses a significant headwind for growth. Home values have declined four months in a row, albeit only moderately. With mortgage rates now roughly double from the start of the year, that trend is likely to continue. The market is in an unusual state of low demand and low supply, which creates a fragile equilibrium and makes it difficult to tell which direction prices may move. Falling prices lower confidence and reduce spending, but the bigger risk may come directly from a slowdown in home transaction volume. New and existing home sales create a flurry of economic activity.

Existing home sales were down by about a third in November compared to a year ago. It is likely home prices and volumes continue to fall, but we do not expect the magnitude or impact to be anywhere near that of the subprime crisis when mass foreclosures flooded the market. This cycle features higher credit quality and more fixed rate mortgages. A likely silver lining to modest home price declines, which are correlated to rent, is progress on containing inflation.

Valuation and Sentiment

With US bond yields in the 4% range, this is relatively attractive as there have been many periods when bond yields were higher than equity earnings yields. International stocks are more attractive by this measure,

Stocks are cheaper now than they were at the beginning of the year. Prices are down and earnings are up. Until recently, extreme valuations in growth stocks presented an overhang for the US equity market. This has now largely corrected itself.

Relative valuations should provide some comfort to those with a long-term view, especially global investors, but tell us little about the next six months. Just as investors can be irrationally exuberant around bull market peaks, extreme pessimism can push valuations to irrational lows.

Related, we view sentiment as a contrarian indicator. At the start of the year, widespread complacency was a red flag. Now, mild pessimism pervades, but we have not seen despair or mass-capitulation.

Bottom line: Neither valuations nor sentiment are making a compelling bullish or bearish case right now.

Bonds

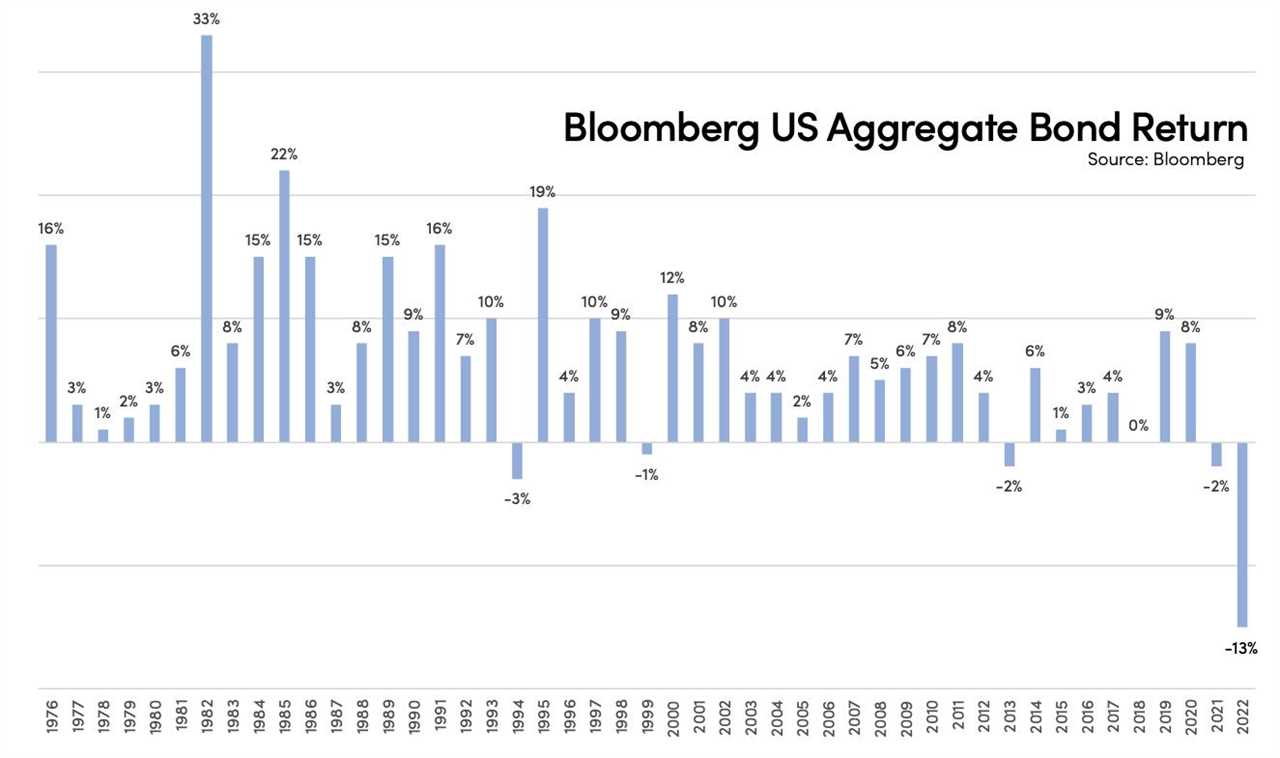

While bonds can lose value in any given year, we frequently maintain that they are highly unlikely to underperform cash over three-year periods. That just happened. Meanwhile, bonds are supposed to be negatively correlated with stocks, providing ballast in bear markets. This year, bonds fell less than stocks, but declined largely in tandem.

Said bluntly, bonds just had the worst year in modern times. Understandably, sentiment toward them is very low. Many people simply don’t want to own fixed income. We think this is a mistake and strongly believe bonds should remain an important allocation in most portfolios.

Bond prices rise when interest rates fall, and drop when interest rates rise. This made 2022 very difficult, but the long-term impact is more complex.

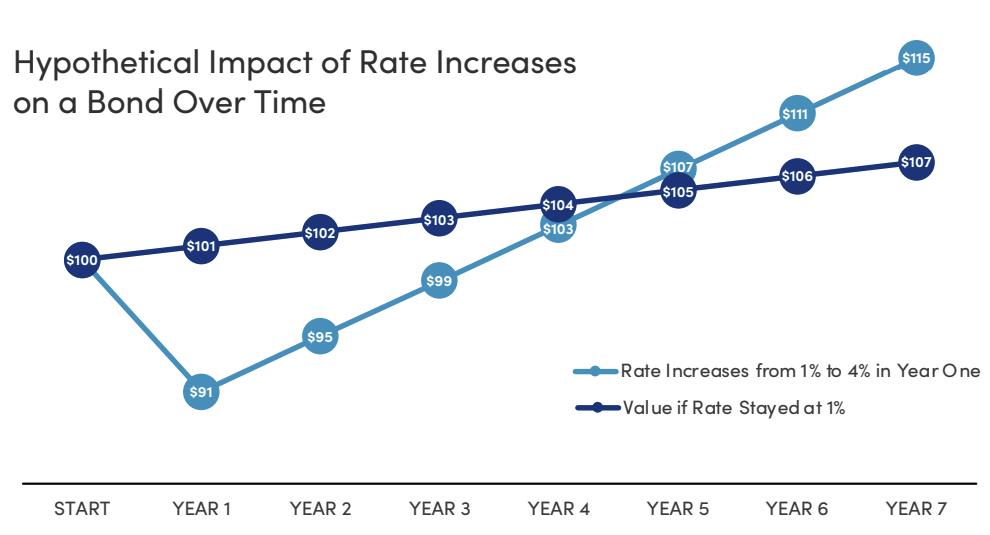

Let’s consider a very simplified example of bond type with a duration of 4.

Duration is a measure of sensitivity that roughly shows the price impact of a 1% move in interest rates. Let’s assume interest rates climb from 1% to 4% over the course of a year. In this example, we can expect the bond price to drop roughly (4%-1%) = 3% x 4 = 12%. Along the way about 2% interest would be paid, so the loss in year one is about 10% (not far from the US aggregate bond market this year).

Next, let’s assume rates then hold steady at 4%. It will take 2.5 additional years to earn enough interest to get back to breakeven. Around 3.5 years into this example, we start to surpass the original 1% rate scenario. And with a higher yield now in place, it typically doesn’t take long for bonds to leave cash in the dust. At around six years from the starting point, the investor will have more dollars than if rates had never risen in the first place.

All of this makes sense. Cash has almost no volatility, or risk. Bonds have much lower volatility than stocks, but more than cash. Investors are compensated over time for taking that risk. Ultimately, a move away from ultra-low interest rates is probably healthy. Aside from creating excessive risk taking in some cases, rates near zero created significant challenges for not only retirees, but pension funds, insurance companies and others.

Right now, the Fed Funds target range is 4.25%-4.50%, and it is expected to climb above 5% in the coming months. This does not mean bonds will necessarily fall further in price. Shorter term Treasuries already reflect additional Fed moves still to come. However, it is important to note that the yield curve is inverted, meaning longer maturity bonds pay lower rates. This suggests investors expect the Fed to pivot back to rate cuts before long.

One final note: A return to more normal rate levels does not preclude strong returns from stocks. Interest rates for most of the 1990s were higher than we see now, and it was one of the most prolific decades for equities of all time.

Bear Market Fatigue

In life the years seem to fly by. But from an investing perspective, 2022 seemed long. Bear markets wear investors down through both magnitude and duration. It is normal to grow tired of seeing account balances linger below highs while hearing the same advice.

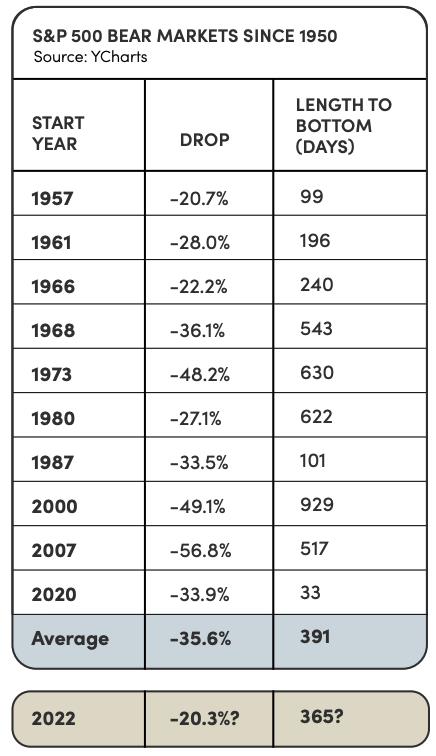

September may have been the bottom of this bear market. If not, it will have now reached the one-year mark for duration. In terms of magnitude, the US stock market is down around 20%. The average bear market since 1950 (excluding the current bear) featured a roughly 36% total decline with a duration of about 13 months. However, there was extreme variability in those outcomes. The shortest was the 2020 Covid panic, lasting just over a month. The longest was the dotcom collapse which unfolded over more than two and a half years, encompassing 9/11.

This bear market is nearing the average length but remains shallow in terms of average peak to trough drop. There are plenty of reasons this bear market may end up having less bite than average, but no one should be surprised if the hardest days still lie ahead.

Bear market fatigue is real. Many investors give up on stocks at close to the worst time. Others manage to hold on but find themselves emotionally impacted when usually they may not give much thought to markets. It is common for a significant portion of losses to be backend loaded into the final months of a bear market, just when patience is already running low. This pattern contributes to the type of behavioral challenges we are here to help clients avoid.

Despite rising prices in Q4, many people seem to “know” things are going to get worse. This raises the question “Why be invested now?” In our view, the answer is simple. Staying committed to a diversified strategy and periodically rebalancing provides the best chances for success. It reduces the odds of making debilitating behavioral mistakes and is a powerful tool in combating the long-term impact inflation can have on spending power.

Every bear market feels awful and scary. And all previous ones have eventually come to an end. The best opportunities often surface when pessimism is widespread.

Cognitively, most people understand the power of compound growth, the statistical disadvantages of market timing, and the logic of a diversified long-term approach. But we are all human. Talking about it can help, even if it feels repetitive or like a similar conversation you’ve had in the past. We appreciate the opportunity, so please don’t hesitate to reach out to your advisor.

Sticking with a strategic asset allocation doesn’t mean doing nothing. Volatility presents increased opportunities to benefit from rebalancing and tax loss harvesting. We continue to engage in each as the year progresses. Rebalancing involves periodically selling what has done better and buying what has become cheaper.

Inflation

Depending on your age, this is either the first or second time you have experienced a period of elevated inflation. Inflation is a serious issue. Day to day, it is disturbing to feel higher prices and the concept of accumulated wealth losing purchasing power can be quite disorienting. That is why the Fed is willing to send the economy into recession, increase unemployment, and exacerbate the national debt costs if needed to reduce it.

Fortunately, headline inflation has been in decline. It June and was reported at 7.1% in November. Unfortunately, inflation has a somewhat permanent nature. Even if it returns to around 2%, higher prices from this year will generally be baked in.

Inflation is impossible to predict, but we concur with the Fed outlook that it should continue to moderate in 2023. There are several factors supporting this:

- The Fed is prioritizing price stability above growth, pushing through the fastest rate hike regime in our lifetimes. Higher interest rates reduce general demand and therefore pricing pressure.

- The labor market is still strong but has softened.

- Higher mortgage rates are impacting home prices and should lead to lower rental costs.

- Covid created supply chain issues should abate over time.

- Energy companies greatly reduced exploration and drilling activities. Ability to increase supply should keep a lid on oil prices.

- Innovation and technology continue to drive efficiencies.

- Markets also agree. The five-year breakeven rate for TIPS is just 2.3%. This is the difference in yield between inflation-protected bonds and standard Treasuries for the same maturity range, which represents the expected inflation rate.

What should I do now?

While there is much commentary about inflation and its possible path, there is a shortage of information on what individuals should do about it. Here are four suggestions:

1. Consider inflation risk in investment portfolio construction.

Allocations to TIPS (inflation protected bonds); hard assets like real estate, gold and commodities; a diversified sector exposure including materials, utilities and consumer goods; and a global approach — none of these can hedge inflation perfectly but all of them can help. Although dormant until last year, inflation risk has always been a part of our allocation decisions. Bitcoin may someday prove to be a reasonable hedge against inflation. For now, we believe its massive volatility and speculative nature outweigh its ability to play this role effectively.

Inflation also plays a big part in overall asset allocation. In a world with no inflation, if you have a million dollars and want to spend $50,000 for 20 years, you could keep your money in cash and be fine. That is not reality. Growth from equities and bonds is usually needed to combat inflation. Owning real estate also reduces risk.

2. Understand your spending.

It is hard to know how inflation is impacting your financial goals if you don’t have a decent understanding of how much you spend and what the trend is. Inflation can show up very differently in individual spending habits. Monthly budgets are great for some people, and don’t work well for others. If you know you are still saving adequately, or that your withdrawal rate is still on target if retired, that is a great start. Regardless, it is good practice to see where your money is going. The cash flow and budgeting tools on our free financial dashboard are designed especially for this purpose.

3. Have a plan.

Once you have realistic spending goals you can see how likely you are able to maintain them or what adjustments can be made to achieve them. This is where our Retirement Planner tool comes into play. It helps us identify the right allocation for your investments and it should help you with general planning. The default for inflation in the tool is 3.5%. This is about the average since 1950 and is greater than we have seen for most of this century. But of course, this year inflation has been higher. We continue to believe it is a reasonable setting in a long-term tool. As mentioned, TIPS markets are pricing in for expectations of just 2.3% over the next five years.

In the assumptions section of Retirement Planner, you can adjust the inflation rate and create a “what-if” scenario to model the impact of higher inflation. This can be informative, but we advise against too much consideration of significantly higher inflation numbers because that scenario is unlikely.

4. Don’t panic.

The purpose of money is first to provide for needs and then to help enjoy life. We don’t want to stop either of those because of moderate inflation. A year of higher inflation may impact lifetime spending power similarly to a moderate decline in stocks. We shouldn’t overreact to either. Your monthly cash flow will tell you if immediate spending changes are required. If not, we don’t want to stop living. However, the unfortunate reality is that for many 2022 was a bad combination of down markets and high inflation, which may necessitate some changes. We may not be able to consume as much as we did before.

Cutting back can be difficult but those who understand their situation will be able to do so with confidence in the moves they are making. On the investment side, it is important not to get scared out of a good long-term allocation. Now that one can get a higher interest rate holding cash, it can be tempting to stick our heads in the sand and prioritize safety. The problem is even at higher rates, cash is losing value to inflation. Inflation is not necessarily good for stock prices, but stocks prices still tend to rise in inflationary periods when growth becomes even more important to protect purchasing power.

||

----------------------------

By: Craig Birk, CFP®

Title: Markets: Investment Insights on Braving the Bear

Sourced From: www.personalcapital.com/blog/investing-markets/market-commentary-q4-2022/

Published Date: Mon, 09 Jan 2023 18:15:56 +0000

Read More

Did you miss our previous article...

https://peaceofmindinvesting.com/investing/although-people-arent-buying-disability-insurance-they-should

.png) InvestingStocksToolsClubsVideosPrivacy PolicyTerms And Conditions

InvestingStocksToolsClubsVideosPrivacy PolicyTerms And Conditions