<iframe style="width:120px;height:240px;" marginwidth="0" marginheight="0" scrolling="no" frameborder="0" src="//ws-na.amazon-adsystem.com/widgets/q?ServiceVersion=20070822&OneJS=1&Operation=GetAdHtml&MarketPlace=US&source=ss&ref=as_ss_li_til&ad_type=product_link&tracking_id=peaceinvesting-20&language=en_US&marketplace=amazon®ion=US&placement=0060555661&asins=0060555661&linkId=80f8e3b229e4b6fdde8abb238ddd5f6e&show_border=true&link_opens_in_new_window=true"></iframe>|<iframe style="width:120px;height:240px;" marginwidth="0" marginheight="0" scrolling="no" frameborder="0" src="//ws-na.amazon-adsystem.com/widgets/q?ServiceVersion=20070822&OneJS=1&Operation=GetAdHtml&MarketPlace=US&source=ss&ref=as_ss_li_til&ad_type=product_link&tracking_id=peaceinvesting-20&language=en_US&marketplace=amazon®ion=US&placement=1119404509&asins=1119404509&linkId=0beba130446bb217ea2d9cfdcf3b846b&show_border=true&link_opens_in_new_window=true"></iframe>|<iframe style="width:120px;height:240px;" marginwidth="0" marginheight="0" scrolling="no" frameborder="0" src="//ws-na.amazon-adsystem.com/widgets/q?ServiceVersion=20070822&OneJS=1&Operation=GetAdHtml&MarketPlace=US&source=ss&ref=as_ss_li_til&ad_type=product_link&tracking_id=peaceinvesting-20&language=en_US&marketplace=amazon®ion=US&placement=1119376629&asins=1119376629&linkId=2f1e6ff64e783437104d091faaedfec7&show_border=true&link_opens_in_new_window=true"></iframe>

By Dr. Jim Dahle, WCI Founder

Inherited IRA rules changed a few years ago, but Congress and the IRS did a terrible job of really communicating all of the new rules that occurred as a result of the SECURE Act. This is particularly true with regard to Required Minimum Distributions (RMDs). Two to three years later, the IRS was STILL changing the rules.

Changes with the SECURE Act

When you inherited an IRA prior to 2019, you had to start taking RMDs right away, usually based on your age. That allowed young inheritors to stretch the tax protection of an IRA out for many decades. The SECURE Act implemented the “10-year rule,” which required you to pull all of the money out of an inherited IRA within 10 years of the death of the deceased. However, what it did not specify well was whether you had to take anything out during years 1-9. In fact, there was a pretty good agreement that you did not have to take anything out at all until year 10. This is a big deal, because the penalty for not taking out an RMD is 50% of what you should have taken out—one of the steepest penalties in the entire tax code.

People came up with all kinds of strategies to take advantage of this new Stretch IRA. That usually meant leaving Roth money in there for the full 10 years. It also meant trying to take out tax-deferred money in the most tax-efficient way possible, i.e. in low-income years, spread out over a few years, and delaying withdrawals until late in the 10-year period.

Later Guidance on Required Minimum Distributions

But in February 2022—yes, more than three years after the law went into effect—the IRS clarified the rules in the form of “Proposed Regulations” which took away a few of those planning options.

- If the deceased was already taking RMDs from a tax-deferred IRA upon dying in 2020 or later, the beneficiary must start taking RMDs in the year after the death and continue for nine years before taking everything else out in year 10.

- If the deceased was not taking RMDs from a tax-deferred IRA, the beneficiary could avoid RMDs. They just had to have all of the money out of the account in year 10.

- If the inherited IRA was a Roth IRA, the beneficiary could also avoid RMDs and take all the money out in year 10.

Naturally, a lot of people were not happy about this so they let the IRS know. Imagine those people who didn't take out RMDS in 2020 and 2021 and now had to pay 50% penalties due to the rules changing after the fact.

The IRS relented, and in October 2022, it published IRS Notice 2022-53:

“Final regulations regarding RMDs under section 401(a)(9) of the Code and related provisions will apply no earlier than the 2023 distribution calendar year. IV.

Guidance for Certain RMDs for 2021 and 2022

A. Guidance for defined contribution plans that did not make a specified RMD A defined contribution plan that failed to make a specified RMD (as defined in Section IV.C of this notice) will not be treated as having failed to satisfy section 401(a)(9) merely because it did not make that distribution.

B. Guidance for certain taxpayers who did not take a specified RMD To the extent a taxpayer did not take a specified RMD (as defined in Section IV.C of this notice), the IRS will not assert that an excise tax is due under section 4974. If a taxpayer has already paid an excise tax for a missed RMD in 2021 that constitutes a specified RMD, that taxpayer may request a refund of that excise tax.”

Basically, those who didn't take the RMDs they should have taken in 2020 and 2021 would not be penalized for not doing so. If you had already paid the penalty, you could get a refund of it.

More information here:

At What Age Do You Have to Take RMDs?

Eligible Designated Beneficiaries

The SECURE Act also created Eligible Designated Beneficiaries (EDBs) for whom even those rules don't apply. EDBs are:

- The owner’s surviving spouse

- The owner’s child who is less than 18 years of age

- A disabled individual

- A chronically ill individual

- Any other individual who is not more than 10 years younger than the deceased IRA owner

EDBs can withdraw their money over their own life expectancy, basically like the old Stretch IRA. There are two exceptions, though. The first is for the surviving spouse. The surviving spouse can roll the inherited IRA into their own. They can also continue the first spouse's RMDs. The second exception is for minor children. Once they hit 18, the 10-year rule kicks in.

Also, you should note that the SECURE Act raised the age you must start taking RMDs to 72 (and subsequently, SECURE Act 2.0 raised it to 73 and eventually 75).

More information here:

Understanding Required Minimum Distributions

Best Inheritances

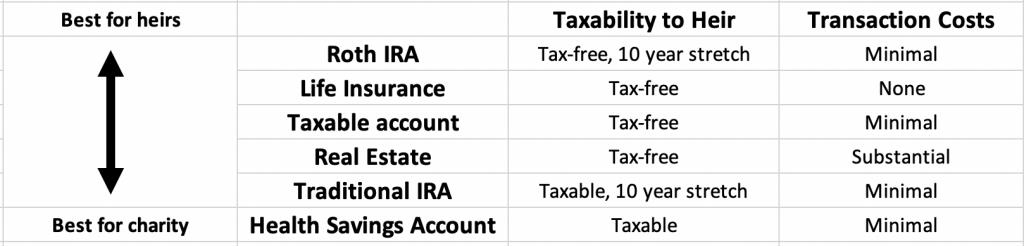

Despite the accelerated RMDs under the New Stretch IRA rules, IRAs and Roth IRAs are still great things to inherit. A Roth IRA may be the best inheritance, and even a traditional IRA is better than an HSA, which is 100% taxable to the heir in the year of death.

Inherited IRAs also do not count toward the pro-rata calculation for the Backdoor Roth IRA.

My condolences if you have an inherited IRA, but if you understand the rules, you can still make the most of your loved one's generosity.

If you need extra help with planning for retirement or have

questions about the best way to save your money in tax-protected accounts, hire a WCI-vetted professional to help you figure it out.

What do you think? Do you have an inherited IRA? What is your plan for it? Comment below!

The post Inherited IRA Required Minimum Distributions (RMDs) appeared first on The White Coat Investor - Investing & Personal Finance for Doctors.

||

----------------------------

By: The White Coat Investor

Title: Inherited IRA Required Minimum Distributions (RMDs)

Sourced From: www.whitecoatinvestor.com/inherited-ira-required-minimum-distributions/

Published Date: Sat, 09 Dec 2023 07:30:10 +0000

Read More

.png) InvestingStocksToolsClubsVideosPrivacy PolicyTerms And Conditions

InvestingStocksToolsClubsVideosPrivacy PolicyTerms And Conditions