<iframe style="width:120px;height:240px;" marginwidth="0" marginheight="0" scrolling="no" frameborder="0" src="//ws-na.amazon-adsystem.com/widgets/q?ServiceVersion=20070822&OneJS=1&Operation=GetAdHtml&MarketPlace=US&source=ss&ref=as_ss_li_til&ad_type=product_link&tracking_id=peaceinvesting-20&language=en_US&marketplace=amazon®ion=US&placement=0060555661&asins=0060555661&linkId=80f8e3b229e4b6fdde8abb238ddd5f6e&show_border=true&link_opens_in_new_window=true"></iframe>|<iframe style="width:120px;height:240px;" marginwidth="0" marginheight="0" scrolling="no" frameborder="0" src="//ws-na.amazon-adsystem.com/widgets/q?ServiceVersion=20070822&OneJS=1&Operation=GetAdHtml&MarketPlace=US&source=ss&ref=as_ss_li_til&ad_type=product_link&tracking_id=peaceinvesting-20&language=en_US&marketplace=amazon®ion=US&placement=1119404509&asins=1119404509&linkId=0beba130446bb217ea2d9cfdcf3b846b&show_border=true&link_opens_in_new_window=true"></iframe>|<iframe style="width:120px;height:240px;" marginwidth="0" marginheight="0" scrolling="no" frameborder="0" src="//ws-na.amazon-adsystem.com/widgets/q?ServiceVersion=20070822&OneJS=1&Operation=GetAdHtml&MarketPlace=US&source=ss&ref=as_ss_li_til&ad_type=product_link&tracking_id=peaceinvesting-20&language=en_US&marketplace=amazon®ion=US&placement=1119376629&asins=1119376629&linkId=2f1e6ff64e783437104d091faaedfec7&show_border=true&link_opens_in_new_window=true"></iframe>

[Editor's Note: In exactly 28 days, registration for the 2023 Physician Wellness and Financial Literacy Conference (WCICON23) will officially open. Yes, it’s that time of year again! It’s time to plan to take a break in sunny Phoenix from March 1-4, 2023 so you can continue down the path of financial literacy while also connecting with like-minded white coat investors. Registration for WCICON23 will open on October 10 at 7pm MT. We expect registration to fill up fast, so make sure to mark your calendar now!]

By Dr. James M. Dahle, WCI Founder

It is no secret that I think “front-loading” your savings is a good idea. The four most important words a medical student or resident can hear are “Live Like a Resident.” In order to front-load your savings and to get all the benefits that would provide, though, you must have a high savings rate early in your career.

6 Reasons Why You Should Have a HIGH Early Savings Rate

#1 Choices, Choices, Choices

Perhaps the most important reason to save early is to allow for more choices later. By getting a good-sized nest egg in place early, you will have the option to cut back on work or even fully retire early. You may wish to change careers or choose a less lucrative practice option. These are all options someone who waits to save does not have. It affects your investments as well. If you start saving early, you can choose whether to be aggressive or conservative in your investments. If you start too late, you may no longer have that option.

College savings is similar to retirement savings. If you start early, your kid will have additional options that might not have been affordable if you started late. That doesn't mean you have to send the kid to the fancy-pants school, but at least it's an option.

More information here:

7 Ways to Increase Your Savings Rate

#2 Less Hedonic Adaptation

It is no secret that, behaviorally speaking, it is far easier to avoid growing into your income than to cut back on your standard of living. Hedonic adaptation means that you are not any happier just because you spend more money. Studies suggest that there is little additional happiness to be had once income hits a reasonable living standard, about $75,000 per year in the US (up to $120,000 in expensive areas like Manhattan and the Bay Area.)

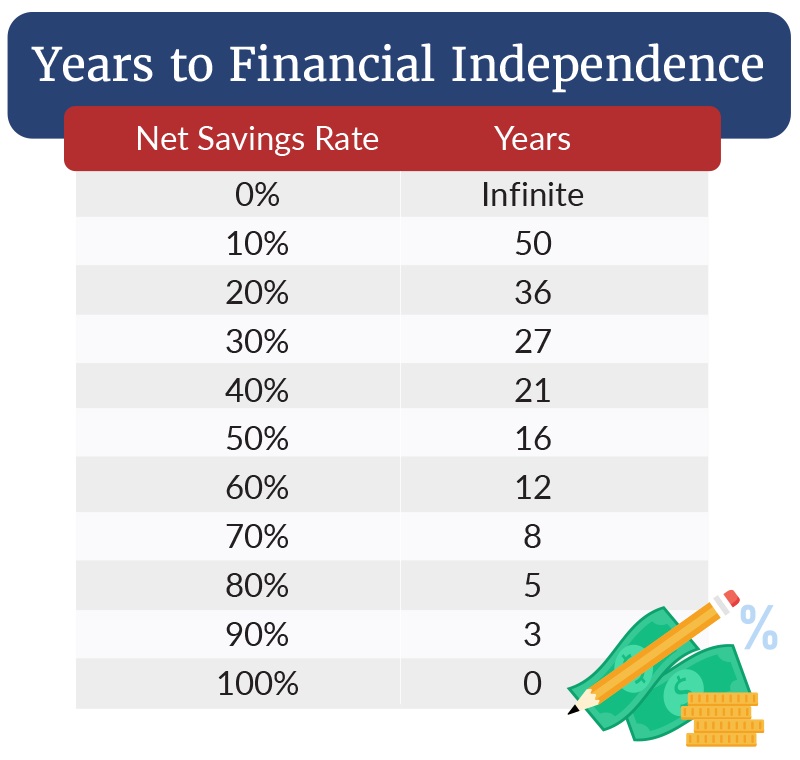

If you start off saving a big chunk of your money, you may NEVER reach the highest levels of hedonic adaptation. That allows you to accumulate a larger nest egg, and it also lowers the size of the nest egg that you need. This is easily seen in this chart:

This is a very simplistic calculation. I used a “net savings rate,” which means how much you save, adjusted for taxes (so using some theoretical discounted rate for tax-deferred accounts), divided by your after-tax income. But the point of the chart (and the calculation behind it) is clear—when you spend less, you save more and your need to save drops. You're burning the candle (years of working/saving) at both ends, so it gets short very quickly.

#3 Much Cheaper Insurance Costs

Despite what insurance agents would like you to believe, insurance costs, on average, are a net drag on your financial life. Since insurance is unlikely to make you particularly happy (kind of like utility bills), it seems silly to spend more than you need to on it. The key factors in determining your life and disability insurance costs are how long you will need it and the size of your expenses.

Agents like to sell you as much disability insurance as you qualify for. But if you're living on 40%-50% of your income, you hardly need to insure it at all. Plus, if you can become financially independent early in life, you can take advantage of “deals” like graded premiums, where your premium is low early and high later. Since you're financially independent, you simply surrender the policy before the premiums ever get high. Term life insurance is similar. It is ridiculously cheap for someone who doesn't need it after age 50, and you never even have to consider expensive permanent insurance.

#4 The Portfolio Does More Lifting

Even if becoming financially independent or retiring early isn't your goal, you give your portfolio the chance to do more of the heavy lifting if you start early. Less of your eventual nest egg will have to come from brute force savings.

Most readers of personal finance books have seen the example that shows if you save $10,000 a year for 10 years ($100,000 total) and then allow that money to compound for another 20 years without additional contributions, you will end up with the same amount of money as someone who waits 10 years to start and then saves $15,000 a year for 20 years ($300,000 total.) The examples are a little misleading since most authors don't make any adjustments for inflation. If you actually do that, a better example would be saving $10,000 in inflation-adjusted dollars a year for the first 10 years ($100,000 total in today's dollars) vs. saving $10,000 in inflation-adjusted dollars a year for the last 20 years ($200,000 total in today's dollars). Still, it's better than a kick in the teeth.

More information here:

From Fourth Year to the Real World (part 1) (part 2)

In slot canyons, just like with finances, you're often stuck between a rock and a hard place

#5 Avoid Hard Choices

Many investors struggle with deciding which types of accounts they should use to save. Others struggle with the pay off debt vs, invest decision. However, if you're saving a ton, you can just do everything at once. That's the whole point of “living like a resident” for 2-5 years after residency. You don't have to choose between paying off your loans, maxing out your retirement accounts, and saving for a down payment. You can do it all at once.

#6 Acquire Important Knowledge Earlier

The sooner you learn about how to manage your finances properly, the longer you can reap the benefits of that knowledge. I once chatted with a doc who came out of residency about the same time as me. He was frustrated with the underperformance and fees of his 401(k). We talked about how mutual funds, advisory fees, and investment costs work. It was all new information to him. It's great that he is learning it while he is still in his late 30s. But imagine if he had learned about that stuff in his early 30s—he might have twice the net worth, and over time, that knowledge could be worth $1 million or more.

It's yet another reason why you should have a high savings rate as early as possible.

What do you think? Do you think it is worthwhile to try to front-load your retirement and college savings? Why or why not? What other benefits or drawbacks exist to having a high early savings rate? Comment below!

[This updated post was originally published in 2015.]

The post 6 Reasons to Have a High Early Savings Rate appeared first on The White Coat Investor - Investing & Personal Finance for Doctors.

||

----------------------------

By: The White Coat Investor

Title: 6 Reasons to Have a High Early Savings Rate

Sourced From: www.whitecoatinvestor.com/6-reasons-to-have-a-high-early-savings-rate/

Published Date: Mon, 12 Sep 2022 06:30:17 +0000

Read More

.png) InvestingStocksToolsClubsVideosPrivacy PolicyTerms And Conditions

InvestingStocksToolsClubsVideosPrivacy PolicyTerms And Conditions