<iframe style="width:120px;height:240px;" marginwidth="0" marginheight="0" scrolling="no" frameborder="0" src="//ws-na.amazon-adsystem.com/widgets/q?ServiceVersion=20070822&OneJS=1&Operation=GetAdHtml&MarketPlace=US&source=ss&ref=as_ss_li_til&ad_type=product_link&tracking_id=peaceinvesting-20&language=en_US&marketplace=amazon®ion=US&placement=0060555661&asins=0060555661&linkId=80f8e3b229e4b6fdde8abb238ddd5f6e&show_border=true&link_opens_in_new_window=true"></iframe>|<iframe style="width:120px;height:240px;" marginwidth="0" marginheight="0" scrolling="no" frameborder="0" src="//ws-na.amazon-adsystem.com/widgets/q?ServiceVersion=20070822&OneJS=1&Operation=GetAdHtml&MarketPlace=US&source=ss&ref=as_ss_li_til&ad_type=product_link&tracking_id=peaceinvesting-20&language=en_US&marketplace=amazon®ion=US&placement=1119404509&asins=1119404509&linkId=0beba130446bb217ea2d9cfdcf3b846b&show_border=true&link_opens_in_new_window=true"></iframe>|<iframe style="width:120px;height:240px;" marginwidth="0" marginheight="0" scrolling="no" frameborder="0" src="//ws-na.amazon-adsystem.com/widgets/q?ServiceVersion=20070822&OneJS=1&Operation=GetAdHtml&MarketPlace=US&source=ss&ref=as_ss_li_til&ad_type=product_link&tracking_id=peaceinvesting-20&language=en_US&marketplace=amazon®ion=US&placement=1119376629&asins=1119376629&linkId=2f1e6ff64e783437104d091faaedfec7&show_border=true&link_opens_in_new_window=true"></iframe>

By Andrew Paulson, CSLP, Lead Student Loan Consultant and Co-Founder of our partner site StudentLoanAdvice.com

The Department of Education has proposed changes to the existing income driven repayment programs (IDR) for those who have student loans. We thought the department was going to add a brand new plan so we would have had five IDR options, which could have further complicated how to select your repayment plan. Instead, the ED chose to simplify the existing repayment options and improve the REPAYE plan. The new REPAYE plan will be rolled out in late 2023. We anticipate borrowers to become eligible for new REPAYE after student loan payments resume in September 2023 (if they actually do).

The REPAYE or Revised Pay As You Earn plan was created in 2016. The old REPAYE plan had its pros and cons. Most of the cons have gone away with the new REPAYE plan. There are a couple of changes that are basically holdovers from the PSLF and IDR waivers you need to be aware of, as well.

Here’s what you need to know about the changes:

#1 Old REPAYE Becomes New REPAYE

Borrowers will be eligible for the new REPAYE program. Those with direct loans, regardless of when they borrowed or their current income, will be eligible for the new REPAYE program. If you have FFEL loans, you’ll need to consolidate those to enroll in REPAYE.

If you’re already in REPAYE, we don’t think you’ll need to do anything to change from the old to the new plan.

#2 Switching from REPAYE to IBR

The old rule for switching from REPAYE to IBR or REPAYE to PAYE was that the borrower had to qualify for a partial financial hardship (PFH). A PFH is when your monthly payment as calculated in IBR or PAYE is less than what the payment would be in the standard 10-year repayment plan. As long as the borrower qualified for a PFH, they could change repayment plans at any time.

The new rule requires a PFH, and it won’t let a borrower switch from REPAYE to IBR if they already have made 120 monthly payments.

More information here:

REPAYE vs. Refinancing Student Loans as a Resident

#3 Monthly Payments Become More Affordable

Historically, monthly payments in REPAYE were 10% of discretionary income (more on this later) for undergrad, graduate, and professional degrees. The new REPAYE will calculate payments at 5% for undergrad loans and 10% for graduate and professional loans. If you have a mix, a weighted average will be calculated to determine the percentage you’ll pay on a monthly basis. I suspect most of your loans are from your graduate program, so I don’t foresee the monthly payment changing much.

Here's a quick example to see how this would change for a doctor:

A single doctor makes $200,000 per year with a loan balance of $220,000 ($200,000 at 6% interest rate from medical school and 20,000 at 6% interest rate from undergrad).

Old REPAYE = 10%

New REPAYE = 9.55% (weighted average)

This would result in a lower monthly payment for this doctor. These percentages would not be recalculated unless the borrower takes on additional loans.

Now, let’s also talk about discretionary income. Discretionary income calculations are changing from 150% of the federal poverty guidelines to 225%. The federal poverty guidelines are set by the Department of Health and Human Services each year. For single borrowers, the poverty guideline is $13,590. The guideline increases by $4,720 for every person in your household. Here’s an example of how payments can change for a borrower using the prior example.

- Discretionary income is lowered by $10,193 due to 225% of the poverty guideline.

- Monthly payments drop $149 per month as a result of lower discretionary income and lower monthly calculation (9.55%).

- On an annual basis, this borrower saves $1,789 in student loan payments.

The numbers look better if you have a greater percentage of undergrad loans as compared to graduate loans. We will show more case studies at the end of this post.

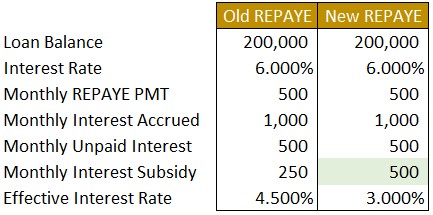

#4 Unpaid Interest Subsidy Is Increased

In old REPAYE, if your monthly payment was less than the interest accrual (or interest charged), half of the interest would be waived. This was commonly referred to as the interest subsidy and was a huge benefit when selecting REPAYE over PAYE/IBR. With new REPAYE, all the unpaid interest would be waived. This appears to be particularly beneficial to those who are (or will be soon) in training or who have a high debt-to-income ratio. Now, your loans will no longer enter negative amortization—or when your monthly payment isn’t sufficient to cover the monthly interest.

The interest subsidy now waives all the unpaid interest monthly and drops the effective interest rate on the loans when your monthly payment isn’t sufficient to cover monthly interest accrual. Interest is ONLY waived in the REPAYE plan.

#5 Shortened Time Frame for Receiving Loan Forgiveness

This probably isn’t applicable to 99% of you, but if you borrowed $12,000 or less, you would receive loan forgiveness after a decade of payments in IDR. The loan forgiveness we are discussing here is taxable loan forgiveness. The loan balance is taxed as if it were income when you reach forgiveness, unlike PSLF which is not federally taxable.

For every additional $1,000 you borrow above $12,000, you add one additional year of monthly payments. Basically, if you borrow $27,000 or more, you would have 25 years until you reached forgiveness.

Please note: if you reach taxable forgiveness prior to 2026, there is no federal income tax on the loan balance forgiven. This reverts back to taxable in 2026 going forward.

More information here:

6 Tricks Medical Students Can Use for Their Student Loans

#6 Receive Forgiveness Credit for Certain Deferments and Forbearances

Since October 2021, we have had a number of waivers that temporarily granted borrowers forgiveness credit for deferments and forbearances like we’ve never seen before. But due to the temporary nature of these waivers, most of these benefits would expire. The PSLF waiver expired October 31, 2022, and the IDR waiver is set to expire on May 1, 2023. This recent proposal will extend a couple of benefits from the waivers:

- Economic hardship deferment and Peace Corps service deferments.

- 12 months of consecutive forbearance or a minimum of 36 months of cumulative forbearance. Does this incentivize you to enter forbearance? It seems like it does. We assume the ED will tamper down on what it allows as forbearance.

- Cancer treatment deferments, military service deferments, national service forbearances, National Guard duty forbearances, post-active-duty deferments, Department of Defense loan repayment program forbearances.

- Certain administrative forbearances—we think this is your classification for when you switch repayment programs or consolidate your loans.

- Rehabilitation training deferments and unemployment deferments.

- Catch-up payments for borrowers in deferments or forbearances wherein a borrower would have a $0 monthly payment—our initial thinking is this may also include those who left their loans in a grace period right after graduation.

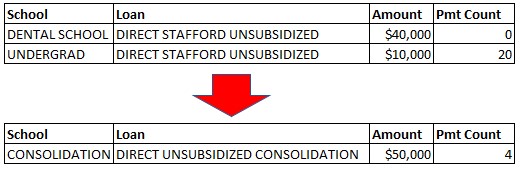

#7 Payment Count Is Not Reset After Consolidation

Typically, when you consolidated your federal loans, any previous repayment history was erased. This was done because the consolidation actually issues a brand new loan in place of the old two or more loans you included in the consolidation.

Instead of resetting your payment history, a weighted average of your existing accounts will be applied to the consolidation loan beginning July 1, 2023.

Please note: if you consolidate loans with differing payment counts before May 1, 2023, you would be eligible to take the loan with the highest payment count. Just make sure that if you’re doing PSLF, to resend your PSLF forms post-consolidation to your servicer.

#8 Help for Delinquent Borrowers

When a borrower misses a payment and they don’t call their servicer to put them into forbearance or deferment, their account becomes delinquent. After 270 days of delinquency, their loans will go into default.

Now, borrowers will be automatically enrolled into the IDR plan with the lowest monthly payment if they are 75 days behind on payments. Also, borrowers’ options can become quite limited when they enter default. They must choose to pay the loan off, consolidate, or complete a rehabilitation process. The new proposal will give borrowers the ability to access an IDR plan to allow for lower monthly payments and an easier exit from default back to good standing.

#9 Phaseout Income-Contingent Repayment (ICR) and Pay As You Earn (PAYE)

To simplify repayment options, borrowers will no longer be able to enter the ICR or PAYE plan. But, borrowers who are already in these plans can stay in them, and they won’t be kicked out. If you are trying to get into either plan, make sure you switch repayment plans before this passes.

REPAYE and IBR will be the only repayment options available to new borrowers. Only Parent Plus Loans borrowers will be able to enroll into ICR after a direct federal consolidation.

More information here:

10 Reasons You Should Pay Off Student Loans Quickly

#10 Ability to Exclude Spousal Income Through Married Filing Separately in REPAYE

A common strategy for married borrowers is to file taxes married filing separately to exclude spousal income to lower monthly payments. This strategy was only available in the IBR, ICR, and PAYE plans. In new REPAYE, you can also exclude spousal income if you file taxes married filing separately (MFS).

This is a huge change for many of you trying to decide which repayment plan is best. Most people, if they were married to another earner and doing loan forgiveness, would avoid REPAYE because of the requirement to include spousal income regardless of how taxes were filed. It was an easy decision to pick PAYE over REPAYE to minimize payments. If they weren’t eligible for PAYE, it came down to running the numbers between IBR or REPAYE—which, if you were making more than you owed, favored IBR.

One other point of emphasis: IBR and PAYE, aside from the past ability to exclude spousal income through MFS, have a payment cap. This payment cap is based on what your monthly payment would be if you were in the standard 10-year repayment plan.

This ceiling does not exist with old REPAYE or new REPAYE. That means there is no payment cap in the REPAYE plan. Further, this may end up being a more costly option than IBR or PAYE in the long run if you do loan forgiveness.

Here are a few scenarios:

New REPAYE beats PAYE

A dual-earning doctor and dentist with no kids. The doc makes $200,000, and the dentist makes $300,000. The doc borrowed $200,000 for med school and $25,000 for undergrad for a total of $225,000 at a 6% interest rate. The dentist paid off their loans already. They file married filing separately.

REPAYE saves the doc $2,096 per year.

PAYE beats new REPAYE

The same fact pattern as above except the doc now makes $400,000.

PAYE saves the doc $4,940 per year. The difference is the payment ceiling that PAYE has that borrowers will run into if they make more than they owe.

IBR beats new REPAYE

Same fact pattern as about except the doc now makes $375,000.

IBR saves the doc $2,554 per year. IBR also has the payment ceiling.

In summary, if you make more than you owe and are currently on track to loan forgiveness, you might be better off staying put in IBR or PAYE. If you make less than you owe, REPAYE would probably be the superior IDR plan.

For those who aren’t graduating until 2024, it is unlikely you’ll be eligible for PAYE. You’ll have to decide between REPAYE and IBR.

This is another huge shakeup for income-driven plans and is helpful to some borrowers. As more details become available, we will continue to update you on changes. The ED's proposal is trying to simplify repayment options for borrowers, and it may sound great on paper. But we see this as another variable that may further complicate your current plan (or potential plan).

Rest assured, we will continue to provide you with relevant information and up-to-date commentary to save you money on your loans. If you need help interpreting these changes, contact our Student Loan Advice team today!

Are you impacted by these changes? Do you plan on switching repayment plans? Does the new proposal make your decision easier or more complicated? Comment below!

The post 10 Changes to Know About IDR Plans for Your Student Loans appeared first on The White Coat Investor - Investing & Personal Finance for Doctors.

||

----------------------------

By: Andrew StudentLoanAdvice

Title: 10 Changes to Know About IDR Plans for Your Student Loans

Sourced From: www.whitecoatinvestor.com/changes-idr-plans-student-loans/

Published Date: Fri, 13 Jan 2023 07:30:09 +0000

Read More

.png) InvestingStocksToolsClubsVideosPrivacy PolicyTerms And Conditions

InvestingStocksToolsClubsVideosPrivacy PolicyTerms And Conditions