<iframe style="width:120px;height:240px;" marginwidth="0" marginheight="0" scrolling="no" frameborder="0" src="//ws-na.amazon-adsystem.com/widgets/q?ServiceVersion=20070822&OneJS=1&Operation=GetAdHtml&MarketPlace=US&source=ss&ref=as_ss_li_til&ad_type=product_link&tracking_id=peaceinvesting-20&language=en_US&marketplace=amazon®ion=US&placement=0060555661&asins=0060555661&linkId=80f8e3b229e4b6fdde8abb238ddd5f6e&show_border=true&link_opens_in_new_window=true"></iframe>|<iframe style="width:120px;height:240px;" marginwidth="0" marginheight="0" scrolling="no" frameborder="0" src="//ws-na.amazon-adsystem.com/widgets/q?ServiceVersion=20070822&OneJS=1&Operation=GetAdHtml&MarketPlace=US&source=ss&ref=as_ss_li_til&ad_type=product_link&tracking_id=peaceinvesting-20&language=en_US&marketplace=amazon®ion=US&placement=1119404509&asins=1119404509&linkId=0beba130446bb217ea2d9cfdcf3b846b&show_border=true&link_opens_in_new_window=true"></iframe>|<iframe style="width:120px;height:240px;" marginwidth="0" marginheight="0" scrolling="no" frameborder="0" src="//ws-na.amazon-adsystem.com/widgets/q?ServiceVersion=20070822&OneJS=1&Operation=GetAdHtml&MarketPlace=US&source=ss&ref=as_ss_li_til&ad_type=product_link&tracking_id=peaceinvesting-20&language=en_US&marketplace=amazon®ion=US&placement=1119376629&asins=1119376629&linkId=2f1e6ff64e783437104d091faaedfec7&show_border=true&link_opens_in_new_window=true"></iframe>

By Dr. James M. Dahle, WCI Founder

I have written before about how to tax-loss harvest. I've shown you screenshots for tax-loss harvesting at Vanguard and at Fidelity. I've explained why you might not want to tax-loss harvest. I've been tax-loss harvesting for a long time, and I've learned a lot of practical tips beyond the basics over the years. Today, I'm going to give you some guidance for those with substantial taxable accounts that will make things much more hassle-free.

#1 Have a Purpose for the Losses

When you first start a taxable account and then hit your first bear market, you get all excited about tax-loss harvesting. The primary goal there is to get up to that $3,000 amount of losses that you can use as a deduction against your ordinary income. However, once you've been tax-loss harvesting for a while and have a six- or seven-figure taxable account, getting $3,000 in losses is no longer really the goal. By this point, you already have tens of thousands or hundreds of thousands of dollars in losses you've been collecting over the years.

Imagine you have a $2 million taxable account, and the market drops 20%. You tax-loss harvest as much as you can. You might now have $100,000, $200,000, or perhaps even $300,000 in losses. That's 33-100 years' worth of $3,000 losses—more than you'll probably ever use up just taking that $3,000 per year deduction. If you're going to bother continuing to tax-loss harvest, there had better be a good reason to do so. Here are some potential reasons:

- You have a small business, practice, or center (surgical, radiological, dialysis, etc.) that you will sell at some point for a big gain

- You have a house you may sell during your lifetime that has a gain that will be much higher than the $250,000-$500,000 capital gains exclusion

- You have real estate investments that will be sold prior to death

- You are likely to sell a fair amount of your taxable account to pay for retirement spending (if you sell only high basis shares with a little bit in losses, that provides A LOT of tax-free retirement spending since most of what is sold will be basis)

Most people with large taxable accounts will have one or more of these situations apply to them. At least two of them and possibly all four of them apply to us. So, we continue to tax-loss harvest.

#2 Have a Simple Portfolio in the First Place

I sometimes have people write in and ask me how to tax-loss harvest their Amazon shares or something similar. The problem is that there is no other investment out there with a 0.99+ correlation with Amazon shares. So, you're stuck picking something else (QQQ? S&P 500? Another retailer stock? A tech stock?) or waiting 30 days to buy it back to prevent a wash sale—and running the risk that you're selling low and then buying high. If you just stick to a handful of boring index funds, this works much better.

There are a dozen or more awesome tax-loss harvesting partners for a total stock market index fund. Simplicity has lots of benefits. It is also much simpler to manage a taxable account if there are just a few investments in it. The majority of our portfolio is now in a taxable account, so most of our asset classes are now in taxable. But what's in there? Just this:

- US Stocks via a Total Stock Market Fund

- International Stocks via a Total International Stock Market Fund

- Small Value Stocks via a Small Value Stock Index Fund

- Small International Stocks via a Small International Stock Index Fund

- Municipal Bonds via an Intermediate-Term Municipal Bond Fund

That's it. Super simple. Yes, we have some real estate investments and some I Bonds and individual TIPS at Treasury Direct, but tax-loss harvesting those doesn't really work due to transaction costs and hassle.

#3 Use Specific Share ID

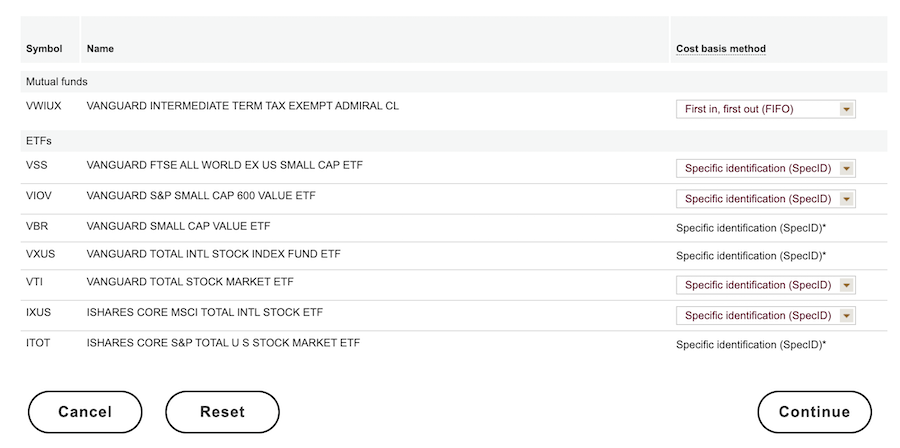

Whenever you buy a new investment in the taxable account, be sure to set it to use “specific identification” as your cost basis tracking method. This is done at Vanguard by going to the “My Accounts” tab and then the “Cost Basis” page, which is labeled “Cost Basis Summary” at the top. Select your taxable account from the drop-down menu. Near the upper right is a link called “View/Change Cost Basis Method.” Click that.

Once you click that link, you'll see a page like this that shows all of your holdings and the method each is using for keeping track of your cost basis.

There are four choices in the drop-down menu:

- Average Cost (AvgCost)

- First In, First Out (FIFO)

- Highest In, First Out (HIFO)

- Specific Identification (SpecID)

I have no idea why anyone would ever want to use anything other than SpecID, and I don't understand why that is not just set as a default option. As you can see, when I went in to take this screenshot, there was one holding that had not yet been set to SpecID, so I fixed that while I was in there. I checked all of the accounts and found some holdings in my kids' UTMA accounts where a method had not been chosen yet and fixed those too. If you haven't looked at this in a while, you probably should.

By using Specific Identification, you can sell only the tax lots with losses, which is precisely what you want to do. Maximize your control over your tax situation by always doing this.

#4 Don't Bother for Small Amounts

When you're just trying to get your $3,000 in losses, you may be willing to tax-loss harvest for a loss of just a few hundred dollars. When you already have six figures in tax losses, you don't need to do that anymore. Don't worry, there will probably be a market correction or bear market along soon, and you can get just as much in losses all at once as you could have by doing small amounts all along the way. At this point, I NEVER tax-loss harvest for less than a high five- or six-figure loss. Maybe I miss out on a few losses here and there that I could have gotten if I had checked my account every single day, but at a certain point, I have more important stuff to do in my life. The amount of a loss worth going after for you might be larger or smaller than mine, but over time, that amount is likely to increase.

#5 Tax-Loss Harvest No More Frequently Than Once Every 2-3 Months

Despite robo-advisors out there trying to convince you of the value of daily tax-loss harvesting (so you will pay them advisory fees to do it for you), I think there are four very good reasons to only do it once a quarter or so.

The first is the simple hassle factor. You have better things to do.

The second is to ensure your qualified dividends stay qualified. If you don't own shares for at least 60 days in the period around (counting both before and after) the ex-dividend date, dividends that would have otherwise been eligible for the lower qualified dividend tax rate become ordinary dividends—and they are subject to your ordinary income tax rates. In my case, that means going from a 20% to a 37% federal tax rate. Doing that completely eliminates the benefit of tax-loss harvesting. If you never tax-loss harvest more frequently than every 60 days, that will never happen to you.

The third is to avoid the 30-day wash sale rule. Again, if you buy or sell more frequently than every 60 days, you'll never have a wash sale. Avoid reinvesting dividends automatically in your taxable account and watch that IRA/Roth IRA to make sure you don't have the same holding there as your taxable account. I know putting everything on auto-pilot sure is convenient, but tax-loss harvesting and automatic investing don't play together well. If you're buying all of your funds every two weeks when you get paid, you're going to have some wash sales. It's not the end of the world, but I think you're better off just pooling all of your money from all of your sources of income and investing it all together manually once a month or once a quarter. That also allows you to rebalance as you go along with new money just by directing investments at lagging asset classes.

The fourth is so you don't ever have more than two investment holdings per asset class. If you're trying to tax-loss harvest every week, you might need three or four partners for each asset class. That introduces a lot of complexity to the portfolio.

#6 Have Only 2 Options

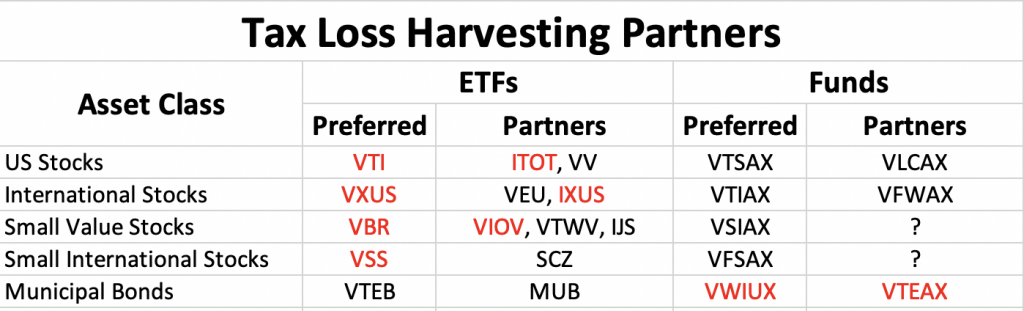

As mentioned above, just have two good options for each asset class you own. Make sure they are investments you are willing to hold for the rest of your life, because you might just have to do so (unless you're willing to pay capital gains taxes to change or you donate a lot to charity.) Here are some of the specific investments I use, along with tax-loss harvesting partners that I would be willing to hold long-term and that are available to purchase at Vanguard. The ones marked in red are the ones I have actually owned recently.

As you can see, finding ETF partners at Vanguard is easier than finding fund partners most, but not all, of the time. For small value and small international, I very much prefer the ETFs. For muni bonds, Vanguard only has one ETF so I very much prefer the fund. For my main taxable holdings, TSM and TISM, both ETFs and traditional mutual funds work just fine.

#7 Donate Appreciated Shares Held for at Least a Year

Do you have charitable inclinations? Then, I suggest donating appreciated shares from your taxable account via a Donor Advised Fund (DAF) instead of donating cash to your favorite charities. The DAF allows for convenience and anonymity, and you can keep the fees very low by not leaving money in there long-term. The overall effect is to flush capital gains out of your portfolio; continually raising the cost basis of the portfolio; and ensuring a larger percentage of it is likely to have a taxable loss, allowing for more tax-loss harvesting. This is a really great strategy to harvest the losers and donate the winners. I've never actually realized a gain in the index funds in my taxable account. Just losses. Yet the basis in that account is over 90% of its value. Why? Because I keep raising it by donating the most appreciated shares. Be sure to hold on to those appreciated shares for at least one year before donating them or you won't get the full charitable donation deduction. You'll only be able to deduct the cost basis, not the full value.

#8 Use 2-3 Tabs in Your Browser

It's important to keep everything straight as you go through this process, especially when using ETFs. I find it best to have three tabs open, all at Vanguard.com. The first one is the Cost Basis page. This allows me to see exactly which holdings and which shares I want to sell. The second one is the Order Status page. This tells me when the sell order goes through so I can then put in the corresponding buy order. The third one is where I actually put in the orders.

#9 Move Quickly When Using ETFs

When tax-loss harvesting large amounts, you really don't want the market to move in between selling one security and buying the partner security. You want to move quickly. Yes, the price could drop in between the transactions and you could have a nice little bonus, but Murphy's Law being what it is, the market always seems to move against me while I am out of it for a minute or two putting in the buy order. Having multiple tabs open helps with this. Using market orders also helps with this.

I have found Vanguard ETF market order transactions to be essentially instantaneous, and I get fair pricing despite using a market order. With limit orders, I often found myself chasing my tail and putting in continually higher buy orders every couple of minutes as the market climbed away from me. It's much easier to avoid buying high and selling low by using market orders in this case. As soon as you see the sell order has gone through, put in a buy order.

If you are doing a very large transaction (six to seven figures), I find it helps if you do one (or perhaps both) of two things. The first is to keep a few thousand dollars of cash in your settlement fund. That way if the share price goes up a few cents right as you buy, you've still got the money to cover the transaction. The second is to actually put in two buy transactions. The first is a very large transaction for most but not all of the shares. That way if the price rises just as you put in the order, you still have the cash to cover it. Then, you do a “clean-up” buy for the remaining shares. Let me show you how this works.

Let's say you are selling VTI and buying ITOT. You sell $1.5 million of VTI. You see that ITOT is selling for $86.76 a share. And $1.5 million divided by $86.76 is 17,289 shares. So, maybe you put in a transaction for 17,200 shares and wait until that goes through. Let's say the market rose on you and you ended up paying $86.80 per share. Instead of buying 17,200 x $86.76 = $1,492,272 worth of ITOT, you actually bought 17,200 x 86.80 = $1,492,960 of ITOT, or $688 dollars more, with that first transaction. Now you only have $7,040 left to buy instead of $7,728. So, you put in an order to buy 81 shares instead of the 89 you would have bought. If you had instead bought all 17,289 shares at once, you would have bought an extra $685 that maybe you didn't have. You can solve this problem either by having some extra cash in the settlement fund or by doing two transactions, one large and one small.

#10 When Using Funds, Put Your Transaction in Near the End of the Day

Tax-loss harvesting traditional mutual funds is way simpler than tax-loss harvesting ETF shares. It all takes place at the Net Asset Value (NAV) at the end of the day. You simply put in an exchange order and voila! It just happens. Very convenient. However, sometimes markets really change during the day. You might have thought you were going to have a loss at 10 in the morning, but by 4pm, it was actually a gain! I recommend you don't put that order in until closer to 4pm ET to make sure you actually still have a loss. To check, just google the corresponding ETF share class ticker and see where it sits on the day. If you had a loss on the fund as of the prior day and the ETF share is down again (or not up much), then you are probably still going to have a significant loss at the end of the day.

You don't have to tax-loss harvest. But if you choose to do so, save yourself some trouble by following these rules, at least once you have a six- or seven-figure taxable portfolio.

As you accumulate wealth, you need a way to protect your assets. WCI’s newest book is The White Coat Investor's Guide to Asset Protection, and it provides the techniques you can use to safeguard your money AND the most comprehensive list of state-specific asset protection laws ever published. Pick up the Amazon best-selling book today and protect your wealth!

What do you think? Do you tax-loss harvest? Why or why not? How do you do it to keep it simple? Any other tips? Comment below!

The post 10 Things to Know When Tax-Loss Harvesting a Large Taxable Account appeared first on The White Coat Investor - Investing & Personal Finance for Doctors.

||

----------------------------

By: The White Coat Investor

Title: 10 Things to Know When Tax-Loss Harvesting a Large Taxable Account

Sourced From: www.whitecoatinvestor.com/how-to-tax-loss-harvest-a-large-taxable-account/

Published Date: Fri, 02 Sep 2022 06:30:07 +0000

Read More

Did you miss our previous article...

https://peaceofmindinvesting.com/investing/the-myths-that-hold-us-back-about-women-and-money

.png) InvestingStocksToolsClubsVideosPrivacy PolicyTerms And Conditions

InvestingStocksToolsClubsVideosPrivacy PolicyTerms And Conditions