<iframe style="width:120px;height:240px;" marginwidth="0" marginheight="0" scrolling="no" frameborder="0" src="//ws-na.amazon-adsystem.com/widgets/q?ServiceVersion=20070822&OneJS=1&Operation=GetAdHtml&MarketPlace=US&source=ss&ref=as_ss_li_til&ad_type=product_link&tracking_id=peaceinvesting-20&language=en_US&marketplace=amazon®ion=US&placement=0060555661&asins=0060555661&linkId=80f8e3b229e4b6fdde8abb238ddd5f6e&show_border=true&link_opens_in_new_window=true"></iframe>|<iframe style="width:120px;height:240px;" marginwidth="0" marginheight="0" scrolling="no" frameborder="0" src="//ws-na.amazon-adsystem.com/widgets/q?ServiceVersion=20070822&OneJS=1&Operation=GetAdHtml&MarketPlace=US&source=ss&ref=as_ss_li_til&ad_type=product_link&tracking_id=peaceinvesting-20&language=en_US&marketplace=amazon®ion=US&placement=1119404509&asins=1119404509&linkId=0beba130446bb217ea2d9cfdcf3b846b&show_border=true&link_opens_in_new_window=true"></iframe>|<iframe style="width:120px;height:240px;" marginwidth="0" marginheight="0" scrolling="no" frameborder="0" src="//ws-na.amazon-adsystem.com/widgets/q?ServiceVersion=20070822&OneJS=1&Operation=GetAdHtml&MarketPlace=US&source=ss&ref=as_ss_li_til&ad_type=product_link&tracking_id=peaceinvesting-20&language=en_US&marketplace=amazon®ion=US&placement=1119376629&asins=1119376629&linkId=2f1e6ff64e783437104d091faaedfec7&show_border=true&link_opens_in_new_window=true"></iframe>

By Dr. James M. Dahle, WCI Founder

It's no secret that we're no fans of personal loans. In fact, we're no fans of credit card loans, car loans, student loans, or mortgage loans either. We would love for no white coat investor to ever have to borrow money ever again. However, that's just not realistic. So, like with any other financial service, we want to make sure that when you do have to borrow money, you borrow as little as possible for as short a time period as possible from the best companies in the industry. As a for-profit company, if we can also generate income from the activity, even better. Thus, every link to a lender or platform in this post is an affiliate link, i.e., if you get a loan after clicking on these links, it doesn't cost you any more but it does help support the site since the company pays us a referral fee (which also naturally introduces a conflict of interest).

What Is a Personal Loan?

A personal loan is simply an unsecured loan used for various purposes. Typically, it is a relatively small amount of money ($5,000-$100,000) and for a relatively short period of time (3 months-7 years). It is generally a little harder to get than a credit card. But it generally provides a lower interest rate—usually fixed—and amortizes so the loan eventually goes away, even if you only pay the minimum payment (unlike credit card debt.) There is usually no pre-payment penalty (but always read the fine print) and only sometimes an origination fee (again, read the fine print). For doctors, personal loans are generally used to solve cash flow problems. The doctor will have the money soon but does not have the money now. Some very reasonable uses for these loans are residency/job interviews and relocation expenses.

Best Physician Personal Loan Companies

In today's post, we'll be talking about seven companies, all of which are partners with The White Coat Investor. We have been working with most of these companies for many years, but others are relatively new to us. If we needed a personal loan or a reader asked us for a referral to a company for a personal loan, these are the companies we would consider.

- Laurel Road

- Splash Financial

- SoFi

- Credible

- Doc2Doc

- First Republic

What Can You Use Personal Loans For?

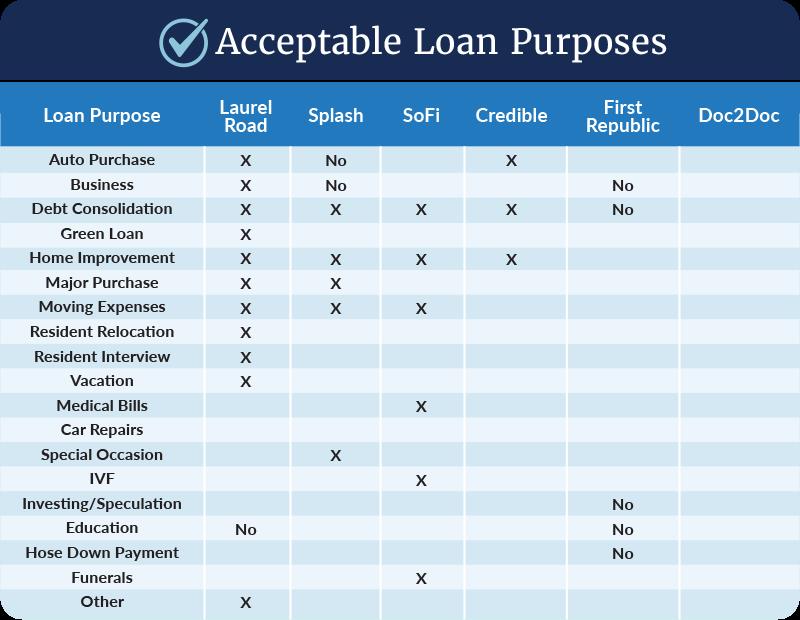

Having never had a personal loan before, I was surprised as I began to research this space. Although personal loans are far more flexible than student loans, car loans, and mortgages, these companies actually want you to tell them what you are going to use the loan for. And if you answer the question wrong, they may not loan you the money. I found this mildly hilarious since money is fungible. If you use your earned income for home improvements and then use the borrowed money for groceries, it's not like it's a grocery loan instead of a home improvement loan. But in the contracts you sign, it does specify the reason for the loan, and you're only supposed to use the loan money for that purpose. Interestingly enough, not every lender will lend you money for every purpose. Here is what I discovered were acceptable loan purposes for each of the companies.

The Xs in the chart are for uses the company has specifically said are fine. The No's in the chart are for uses the company has specifically said are not fine. The blank boxes are presumably fine, but there's no guarantee. The main exclusions to watch out for are business loans, auto loans, student loans, investing loans, and credit card consolidation loans. While personal loans have a lot fewer restrictions than other types of loans, there are obviously some restrictions.

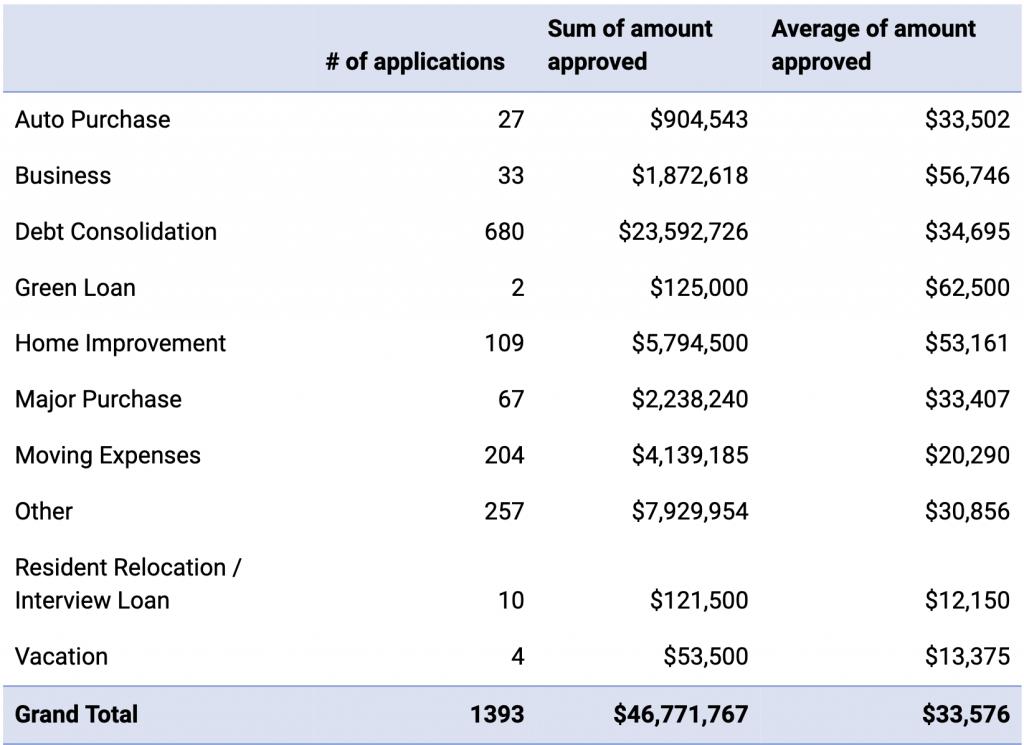

What do doctors actually use these loans for? I don't have this information for all companies, but Laurel Road shared this data:

Not sure what all falls into the “other” category, but the big surprise to me was how few resident relocation/interview loans there were. I would have expected this to be a much bigger piece of the pie. I wasn't surprised that moving expenses were a big category, but I was surprised to see so many auto and home improvement loans. The biggest category was debt consolidation, which I find a bit disturbing now that I know what kind of interest rates doctors get for these loans. That means the loans they consolidated from presumably had even higher interest rates!

Your Location Matters When Getting a Personal Loan

Another interesting aspect of the personal loan market is that every lender does not lend in every state. Some severely restrict where they lend, others exclude just a few states, and some lend in every state.

Laurel Road, SoFi, and Credible work with all states. Splash could help those in all states except Maryland and Vermont. Doc2Doc excluded just Iowa and West Virginia. First Republic only works with those in certain areas of Washington, Oregon, California, Wyoming, Florida, Massachusetts, Connecticut, and New York. In addition, minimum loan amounts are higher for some states, particularly Ohio, New Mexico, New Hampshire, and Massachusetts.

Some Companies Are Lenders; Others Are Platforms

Some of these companies are banks or direct lenders. Others, however, are middlemen, essentially online lending platforms that connect you with dozens of other lenders. The platforms are Credible and Splash. It's fine to use a platform. Just recognize that your eventual loan may end up coming from some bank or credit union you've never heard of before.

My Experience with Personal Loans

I decided to actually apply for loans with each of these companies myself. However, I ran into a few issues doing it (primarily that I had to upload a ridiculous amount of paperwork for a $5,000 loan, given my varied, self-employed sources of income.) I got a rate/offer with most companies in less than five minutes, but when I had to upload two years of tax returns, two years of business tax returns, and a Year to Date Profit and Loss statement, I decided it was no longer worth it just for this blog post.

However, I went as far as I could with each of the lenders without actually uploading documents. If all you had to upload was a driver's license plus either proof of attendance or a paystub (which is the case for most students or docs who actually need one of these loans), it really wouldn't be that big of a deal.

There was an occasional funny question (How much do you have in your checking and savings accounts right now?” and “What monthly payment works with your budget?”), but mostly it was what you would expect on a loan application—name, address, phone number, annual income, whether you own your house, mortgage/rent payment, employer name, etc.

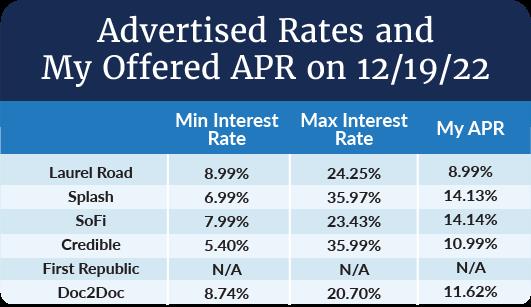

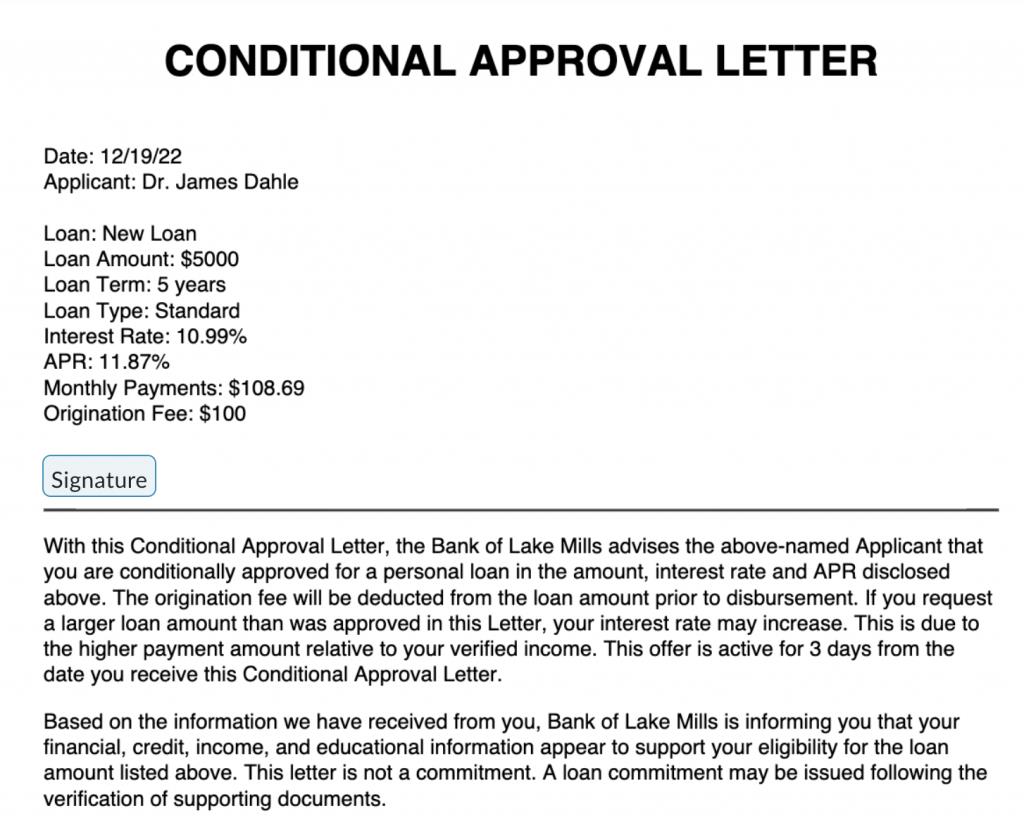

In order to standardize the offers, I only looked at five-year loans of $5,000 and let them each do a soft credit pull. I checked my credit reports before I started. One company told me that my FICO score was 796, certainly high enough to qualify for their best offer on the day I applied (December 19, 2022). Here are the APRs I was offered:

- Laurel Road: 8.99%

- Splash: 14.13%

- SoFi: 14.14%

- Credible: 10.99%

- Doc2Doc: 11.62% (not instantaneous, but within a few hours I knew)

- First Republic doesn't lend to Utah residents.

Does that mean that everyone reading this who needs a personal loan should run out to Laurel Road and get a loan? No, of course not. I'm not kidding when I said it takes less than five minutes to check your rate with these companies. With most of them, I did it in less than three minutes. You might as well check them all and then apply with the one offering the best rate for the terms you need. Rates change over time, and they are different for different debt-to-income ratios and credit scores.

Advertised Interest Rates Are Bunk

Each of these companies advertises a wide range of interest rates on their websites. On the day I applied, this is what they were advertising:

Now, I applied for a five-year loan, not a two- or three-year loan, but if I can't get the best rates with a fantastic debt-to-income ratio and an excellent credit score, who actually gets those low rates? Only Laurel Road got even close to the lowest advertised rate when I applied (and, in fact, offered me 7.99% for a three-year loan, a rate lower than the lowest listed on their site). Maybe it would have offered me a better rate if I borrowed more. Lesson? Ignore the published rates. They have nothing to do with the rate you will be offered. They let you check your rate in just a few minutes with only a soft credit pull (no effect on your credit score). You just need to go do that.

Beware the Origination Fees

Note that the interest rates above are actually APRs. An APR is an Annual Percentage Rate. It includes the interest rate on the loan and any fees, such as origination fees, assuming you keep the loan for the full term. If there are no fees, the APR is the interest rate. If there are fees, the APR is higher than the interest rate. If you pay off a loan with an origination fee early, your actual cost of the loan is higher than even the APR was. Origination fees just matter a lot more when you're not spreading them out over the full term of the loan. If you're going to pay off your five-year loan in six months, even a small origination fee dramatically increases the cost of your borrowing. Of the four companies that gave me instant quotes (including Splash's chosen lender “Upgrade” and Credible's chosen lender “Lightstream”), only one (Upgrade) had an origination fee. Here's what to expect for origination fees.

- Laurel Road: None

- Sofi: None

- Splash: 0%-8%

- Credible: Varies

- Doc2Doc: 2%

- First Republic: None

Prepayment fees are rare. None of the lenders I looked at charged any, but keep in mind that the lending platforms use multiple lenders, so always read the fine print.

Citizenship Matters for Personal Loans

If you're a US citizen or permanent resident, you can apply with any company. If you are on an O-1 or H-1B visa, we recommend either Doc2Doc or Splash. If you are on a J-1 visa, Doc2Doc is your best bet.

Things I Learned Applying for Personal Loans

There were a few other things I learned during the process:

- You can get lower rates by taking shorter terms. Several lenders offered terms as short as 2-3 years with a correspondingly lower interest rate.

- Most companies offer a 0.25% rate discount for setting automatic payments. I included that in the rates above. There were other discounts available that you could get by setting up bank accounts and direct deposit into those bank accounts. I did not include those in the rates above.

- None of these rates are what I would call super attractive. These are unsecured loans, after all. Your comparison should be credit cards, not mortgages or margin loans. These rates make even graduate student loans look downright cheap. Thus, personal loans are only for things that are true necessities, and paying them rapidly should be a major financial priority for you. While 15% is a terrible interest rate, it's not so bad if you only have to pay it for six months.

- It is not hard to apply for these loans. Even the extensive paperwork I was asked to provide to prove my self-employed income, I could have provided in another 10 minutes. I just didn't want to reveal all that. But I'm also not desperate enough for cash to take out a double-digit loan.

- Students are better off taking out extra student loans (or spending less of the loans they do take out) if possible in order to cover residency interviews and relocation expenses. The rates will be lower, and terms (IDRs, PSLF) will be better.

- If you're buying a car, you're probably better off getting a specific car loan. The presence of collateral (the car) will allow you to get a lower interest rate. If you're doing a home improvement, I'd suggest getting a home equity line of credit. Again, the collateral will allow you to get a better interest rate than you will get with a personal loan.

- Most of the companies required a credit score of at least 580-680. If your credit score is in that range or worse, you can certainly apply. But don't be surprised if you are turned down by most or all of the companies.

- None of the companies seemed to be offering variable interest rates, for better or for worse.

- Minimum loan amounts are generally $5,000, but the lending platforms must have at least one lender willing to do a loan of as little as $600. Maximum loan amounts were highly variable and ranged from $25,000-$100,000.

Comments About Specific Lenders

I think all of these companies are OK to use, with the caveat that you should not apply to just one and that you should think long and hard before taking out a personal loan of any kind. Again, take out as little as possible and pay it off as quickly as possible.

Laurel Road

Laurel Road, under one name or another, has been partnering with The White Coat Investor since 2013. This is a company we know well and like. It offers all kinds of doctor-specific products and deals. I was not surprised to see Laurel Road come out on top when I went rate shopping.

Its maximum loan term is 60 months, and its minimum loan amount is $5,000. Its maximum loan amount varies by purpose, profession, and training status. It can be anywhere from $30,000-$80,000. Laurel Road loans only to citizens and permanent residents, requires a minimum credit score of 660, and loans in every state. The only stated exclusion is that you can't use the loan for education. Otherwise, it seems very flexible.

Perhaps the most unique thing about Laurel Road is that it has a reduced payment option for trainees (similar to one of its student loan refinancing products.) Low interest rates and a real understanding of the financial lives of doctors . . . what's not to like?

Check Your Rate with Laurel Road in Less Than Five Minutes

Splash is another long-term WCI partner, and it has been very supportive of our mission for many years. Like Laurel Road and SoFi, many WCIers have refinanced their student loans through Splash over the years. Splash is a lending platform; it will not be your final lender. Despite this, I found the application process to be extremely fast, well-oiled, and intuitive.

Splash can offer the lowest possible minimum loan ($600) with the lowest possible credit score (580) and a loan term of up to 84 months. The maximum loan amount is $100,000. It also loans to H-1B and O-1 visa holders in addition to citizens and residents. If you live in Maryland or Vermont, don't use Splash, but other states should be fine (although Ohio, New Mexico, and Massachusetts require higher minimum loan amounts of $5,000-$6,000). Splash specifically excludes auto and business loans. The lender that Splash connected me with (Upstream) did have a 5% origination fee.

Check Your Rate with Splash Financial in Less Than Five Minutes

SoFi

SoFi is a well-known brand that has grown up alongside WCI. We've been working with them for almost as long as Laurel Road. There are few companies whose C-suite I have physically sat down with and lobbied on your behalf for better physician-specific products. Laurel Road and SoFi are two of them. I'm proud to have helped convince them to offer student loan refinancing products that are appropriate for typical interns and residents to use mostly for their private loans. SoFi also offers lots of other great banking and investment products.

SoFi offers loans in the range of $5,000-$100,000 to citizens and residents in every state (although a few states have a higher minimum loan amount.) It has a relatively high minimum FICO score of 680. Let's be honest, though. It is not that hard to get a credit score above 680 if you actually pay your bills for a reasonable period of time. There are no origination or pre-payment fees—or really fees of any kind. SoFi does not specifically exclude any particular use of the loans. As a very techy company, it has a slick and efficient user interface. I had my quote in about two minutes. It might take you three if you type slowly.

Check Your Rate with SoFi in Less Than Five Minutes!

Credible

Credible, like Splash, is a lending platform that will automatically pair you up with lenders, including companies like SoFi. We've also been working with Credible for many years.

Credible lenders offer loans from $600-$100,000 to citizens and permanent residents with FICO scores of at least 640 in every state. When I applied, the lender I was paired with (Lightstream) did charge an origination fee, but even so, it had one of the lower interest rates I was offered.

Check Your Rate with Credible in Less Than Five Minutes!

Doc2Doc

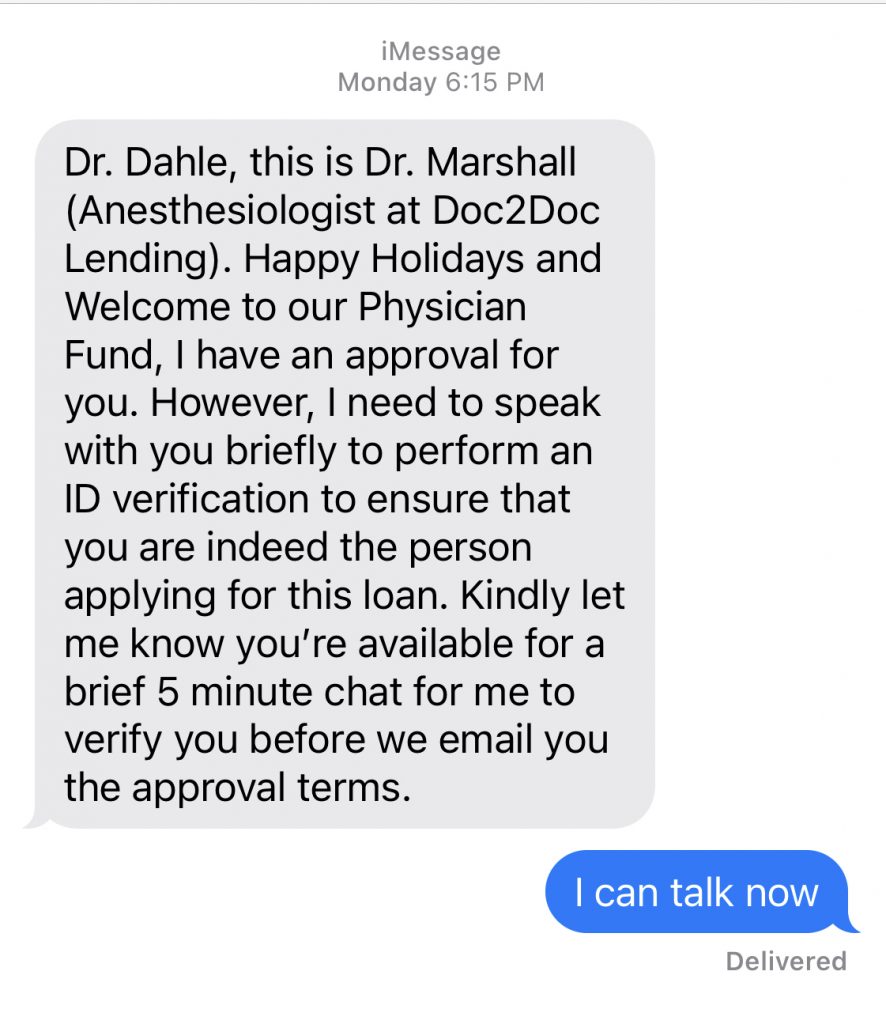

Doc2Doc Lending is the most unique company on this list and a new partner here at The White Coat Investor. Doc2Doc requires its borrowers to be fourth-year students or have already graduated with an MD, DO, or DDS. This physician-owned company does not give you a quote in less than five minutes like the ones listed above. However, it was the only one where a doctor actually texted me a few minutes after I applied and asked if we could chat.

I thought that was pretty cool. I thought Dr. Marshall would recognize my name, but he didn't seem to, so I think I got the standard schpiel where he asked me a few identity verification questions (from my credit report) and outlined the terms of the loan (no prepayment fee). By the time we talked, it must have been after 8pm here in Utah, but I think it's located in the Pacific Time Zone. It felt like Doc2Doc went above and beyond to get me my money quickly. This email was in my inbox a few minutes later:

While you don't get an instantaneous quote, it was still pretty fast, and I felt like I was going to get great service there.

Doc2Doc had the lowest maximum listed interest rate (20.7% on the date I applied) and one of the best interest rates I was offered. It has three- to five-year loan terms and loans from $5,000-$100,000 (less in training). It also seemed to be the only company that would lend to someone on a J-1 visa. Doc2Doc does charge a 2% origination fee, so be aware of that. Like most of the companies, it offers a 0.25% discount for automatic ACH payments. It does not lend in Iowa or West Virginia, and it has higher minimum loan amounts ($7,000-$11,000) in Massachusetts and New Hampshire.

Some companies “get” docs pretty well, but I doubt any of them understand physician financial lives like Doc2Doc does.

Check Your Rate with Doc2Doc!

First Republic

First Republic is another company we have worked with for many years. It's most famous for its low-interest rates. The main problem is that it's not a nationwide company. It wants to build a long-term banking relationship with you, not just a one-off personal loan. So, First Republic wants you to live close to one of its branches, open an account, and talk to a personal banker. While I could not get a loan with First Republic because I live in Utah, it would not have surprised me if it offered me a loan at a much lower rate than the other companies. It did that for a long time when refinancing student loans, even before rates plummeted in 2018-2020. First Republic refinanced student loans into what is essentially a personal loan product. That had downsides (you could no longer deduct interest or refinance the loans with other student loan refinancing companies), but the low rates generally made up for it.

It does have an origination fee, but it will lend for up to 15 years, much longer than any of the other companies. You really do have to live close to a branch, though. Don't bother applying if you don't live in Washington, Oregon, California, Wyoming, Florida, Massachusetts, Connecticut, or New York.

Check Your Rate with First Republic in Less Than Five Minutes!

Personal loans can be used for many purposes. They offer fixed rates, and unlike credit cards, they do eventually go away if you just make the minimum payments. However, because the interest rates on personal loans are relatively high, we recommend you borrow as little as possible and pay it back as quickly as possible. If you do need one of these loans, we recommend checking your rates with these lenders today.

What do you think? Have you used one of these lenders for a personal loan? What was your experience like? Comment below!

The post Best Personal Loan Companies for Doctors appeared first on The White Coat Investor - Investing & Personal Finance for Doctors.

||

----------------------------

By: The White Coat Investor

Title: Best Personal Loan Companies for Doctors

Sourced From: www.whitecoatinvestor.com/best-personal-loan-companies-for-doctors/

Published Date: Mon, 24 Apr 2023 06:30:12 +0000

Read More

.png) InvestingStocksToolsClubsVideosPrivacy PolicyTerms And Conditions

InvestingStocksToolsClubsVideosPrivacy PolicyTerms And Conditions