<iframe style="width:120px;height:240px;" marginwidth="0" marginheight="0" scrolling="no" frameborder="0" src="//ws-na.amazon-adsystem.com/widgets/q?ServiceVersion=20070822&OneJS=1&Operation=GetAdHtml&MarketPlace=US&source=ss&ref=as_ss_li_til&ad_type=product_link&tracking_id=peaceinvesting-20&language=en_US&marketplace=amazon®ion=US&placement=0060555661&asins=0060555661&linkId=80f8e3b229e4b6fdde8abb238ddd5f6e&show_border=true&link_opens_in_new_window=true"></iframe>|<iframe style="width:120px;height:240px;" marginwidth="0" marginheight="0" scrolling="no" frameborder="0" src="//ws-na.amazon-adsystem.com/widgets/q?ServiceVersion=20070822&OneJS=1&Operation=GetAdHtml&MarketPlace=US&source=ss&ref=as_ss_li_til&ad_type=product_link&tracking_id=peaceinvesting-20&language=en_US&marketplace=amazon®ion=US&placement=1119404509&asins=1119404509&linkId=0beba130446bb217ea2d9cfdcf3b846b&show_border=true&link_opens_in_new_window=true"></iframe>|<iframe style="width:120px;height:240px;" marginwidth="0" marginheight="0" scrolling="no" frameborder="0" src="//ws-na.amazon-adsystem.com/widgets/q?ServiceVersion=20070822&OneJS=1&Operation=GetAdHtml&MarketPlace=US&source=ss&ref=as_ss_li_til&ad_type=product_link&tracking_id=peaceinvesting-20&language=en_US&marketplace=amazon®ion=US&placement=1119376629&asins=1119376629&linkId=2f1e6ff64e783437104d091faaedfec7&show_border=true&link_opens_in_new_window=true"></iframe>

[Editor's Note: The Real Estate Masterclass is now officially open, and it’s designed to get you started on your potential journey into real estate. And best of all, it’s free. Think of it as a three-part introduction to our newly released No Hype Real Estate course as Dr. Jim Dahle walks you through these subjects: 1) incorporating real estate into your portfolio; 2) the five most important calculations you need to know; and 3) using real estate to reduce your taxes. Plus, if you register for the Masterclass, you’ll get a $200 discount for the No Hype course. Sign up for the Real Estate Masterclass today, and start a new journey for yourself—for free!]

By Dr. James M. Dahle, WCI Founder

Sometimes I write blog posts that I want to write. Other times, I write blog posts that Josh (our Content Director) and Lauren (our Digital Marketing Director and Search Engine Optimization Guru) want me to write. This is one of the latter. Apparently, lots of people are searching the internet right now for the answer to this question. Here are some possible answers to the question in the title:

- You shouldn't have stopped buying bond funds.

- I didn't stop buying bond funds.

- I'm still buying bond funds.

- Bond funds are more attractive now than they were a year ago but could be even more attractive in another year.

- Yes.

- No.

OK, now that I've done that, I can write what I want.

Bonds Move Inversely with Interest Rates

Perhaps the most important thing to understand about bonds is that when interest rates go down, the value of a bond goes up. The reason why is that your bond that pays interest at that higher rate is now more valuable than a bond that can be purchased today that pays interest at a lower rate. How much more is your bond worth? Precisely the amount that equalizes the yields on the two bonds with different interest rates.

Naturally, when interest rates go up, the value of bonds goes down for exactly the opposite reason. Who wants that old crappy bond paying 2% when I can get a shiny new one paying 4%? I'm not buying your old one unless you sell it to me at a discount.

Bond Funds Own Bonds

A bond mutual fund is simply a convenient, liquid, diversified method of owning bonds. If you choose wisely and select a very low-cost, diversified bond fund—such as those available from Vanguard—you get all of that convenience, liquidity, and diversification for free (along with some professional management.) That's a pretty great deal.

However, a bond fund is not exactly the same thing as owning an individual bond. When you own a high-quality bond, such as a treasury bond, there is a guarantee in place. You are guaranteed to get all of your principal back eventually, plus interest along the way. With a normal treasury bond, your nominal principal is guaranteed. With a TIPS, your real principal is guaranteed. That guarantee doesn't exist with a bond fund. Because a bond fund is a continually replenished group of bonds, it is possible to lose principal in a bond fund. However, in the long run, this really isn't a particularly significant risk. Besides, what do you think you're doing when you are building a portfolio of individual bonds? That's right, you're running a bond fund. Your only real advantage there is that you're not subject to the tax consequences of the actions of the other investors in the fund.

More information here:

I Bonds and TIPS: Which Inflation-Indexed Bond Should You Buy Now?

Higher Interest Rates Are Good for Bond Investors

Here's a principle that too few investors understand. If you're a bond investor, you actually want interest rates to go up. Yes, that means all of your bonds lost value. But it also means that the future expected returns of your bonds are now much higher. In the long run (defined as any period of time longer than the duration of the bond fund or your portfolio of bonds), you will come out ahead. So, if you're not 90 years old with a collection of 10-year bonds (and I hope you're not), quit complaining about interest rates going up. It makes you look dumb. If you're a future net saver and not a future net borrower, all else being equal, higher interest rates are a good thing.

More information here:

Why Bother with Bonds – A Review

You Need an Investing Plan or a Crystal Ball

I learned early on as an investor that my ability to predict the future is not good enough to rely on it for investing decisions. In short, my crystal ball is always cloudy. Chances are yours is, too, but if you're not yet sure of that, I suggest an exercise. Write down all of your predictions in a little $2 journal you can buy at Target. You know, things like what a stock is going to do, what the market will do, what interest rates will do, which asset class will outperform over the next one, two, five, and 10 years, etc. Make these predictions specific. Keep going for a year or two. Chances are you will find out that your crystal ball is just as cloudy as mine. If you find out it is not, then you should consider opening up a hedge fund, managing billions, and charging 2 and 20.

The problem with a question like “Should I Start Buying Bond Funds Again?” is that the answer requires a functioning crystal ball. What you're really asking is, “Are interest rates going to stop going up?” The answer to that is, “I don't know.” Actually, I think a more accurate answer is, “I think they'll probably go up at least one more time, but I have no idea what will happen after that.” The reason I say that is that as I write this on October 28, 2022, I can read the last statement from the Fed Open Market Committee from September 2022. In September 2022, the Fed raised the “effective federal funds rate” to between 3 and 3 1/4. The median view of those on the committee at that time was that by the end of 2023 that rate would be 4.6%. That suggests there will be some more rate hiking ahead of us.

Now, just raising the very short-term federal funds rate doesn't mean that the interest rates that most affect our lives like the 10-year treasury rate and the 30-year mortgage rate are going to go up. The yield curve is currently inverted, suggesting that a possible recession is coming. But it seems more likely than not that rates have at least a little further to rise. However, I don't really think they have to go up much more to get inflation under control. The reason why is that the latest data suggests it already is.

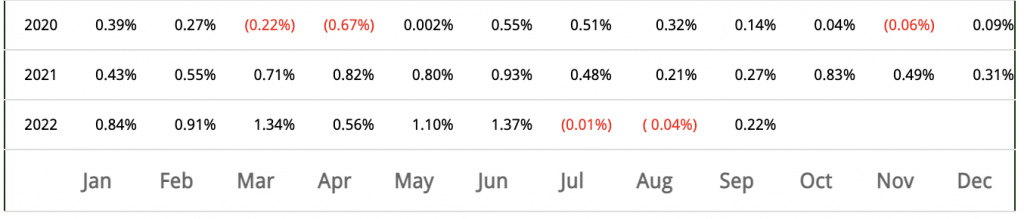

Most people look at year-over-year inflation data. But there is current data being published every month. Here is what it shows right now:

As you can see, we've had some nasty inflation in the last year. Check out those numbers from February, March, May, and June. That's bad. A monthly inflation rate of 1.37% annualizes out to something like 18% inflation. But check out the last three months. There is a negative number for two of them (i.e. deflation), and September's number annualizes out to about 3%, not too far from the Fed's 2% annualized target. That suggests to me that maybe we're starting to get a handle on inflation. Certainly, these higher interest rates have already had a huge effect on housing. In my area, the average house price has already fallen over 7%, and housing prices are notoriously sticky. I just don't think they're going to have to raise rates too much more to get inflation under control, which is the whole goal.

Of course, remember what I told you about my crystal ball. Even though I have an opinion, I'm smart enough not to rely on it for my investing decisions.

Since neither you nor I have a functioning crystal ball, I suggest you do what I have done and develop an investing plan that does not require you to successfully predict the future to be successful. That plan is a static asset allocation. I own 60% stocks, 20% bonds, and 20% real estate. When interest rates are high, I own 60% stocks, 20% bonds, and 20% real estate. When interest rates are low, I own 60% stocks, 20% bonds, and 20% real estate. When interest rates are going up, I own 60% stocks, 20% bonds, and 20% real estate. When interest rates are going down, I own 60% stocks, 20% bonds, and 20% real estate. Get the picture? See how that works? Sometimes my purchase is timed well. Sometimes it's timed poorly. But over the long run, I got rich and I will stay rich.

My own purchases of bonds in the last couple of years took place on:

- 1/25/21

- 2/9/21

- 2/16/21

- 6/1/21

- 7/26/21

- 11/3/21

- 12/13/21

- 1/4/22

- 1/31/22

- 4/18/22

- 4/21/22

- 7/5/22

- 8/9/22

- 10/12/22

Some of those were individual I Bonds or TIPS bought at Treasury Direct, but most were bond fund purchases. I don't buy bonds every month, but it would be an unusual quarter that I didn't buy any bonds. Does that look like the investing record of someone who can predict the future? Or does it look like the investing record of someone that just keeps buying as he earns money? Bingo. You got it. As Nick Maggiulli likes to say (paraphrased):

“‘Just keep buying' is the secret to long-term wealth accumulation.”

Now, you know why I answered the question in the title the way I did.

What do you think? Do you try to time the market when buying bonds, or do you just keep buying? Has increasing interest rates affected your decision to buy individual bonds or bond funds? Comment below!

The post The Fed Keeps Raising Interest Rates; Should You Start Buying Bond Funds Again? appeared first on The White Coat Investor - Investing & Personal Finance for Doctors.

||

----------------------------

By: The White Coat Investor

Title: The Fed Keeps Raising Interest Rates; Should You Start Buying Bond Funds Again?

Sourced From: www.whitecoatinvestor.com/should-you-start-buying-bond-funds/

Published Date: Fri, 18 Nov 2022 07:30:40 +0000

Read More

.png) InvestingStocksToolsClubsVideosPrivacy PolicyTerms And Conditions

InvestingStocksToolsClubsVideosPrivacy PolicyTerms And Conditions