<iframe style="width:120px;height:240px;" marginwidth="0" marginheight="0" scrolling="no" frameborder="0" src="//ws-na.amazon-adsystem.com/widgets/q?ServiceVersion=20070822&OneJS=1&Operation=GetAdHtml&MarketPlace=US&source=ss&ref=as_ss_li_til&ad_type=product_link&tracking_id=peaceinvesting-20&language=en_US&marketplace=amazon®ion=US&placement=0060555661&asins=0060555661&linkId=80f8e3b229e4b6fdde8abb238ddd5f6e&show_border=true&link_opens_in_new_window=true"></iframe>|<iframe style="width:120px;height:240px;" marginwidth="0" marginheight="0" scrolling="no" frameborder="0" src="//ws-na.amazon-adsystem.com/widgets/q?ServiceVersion=20070822&OneJS=1&Operation=GetAdHtml&MarketPlace=US&source=ss&ref=as_ss_li_til&ad_type=product_link&tracking_id=peaceinvesting-20&language=en_US&marketplace=amazon®ion=US&placement=1119404509&asins=1119404509&linkId=0beba130446bb217ea2d9cfdcf3b846b&show_border=true&link_opens_in_new_window=true"></iframe>|<iframe style="width:120px;height:240px;" marginwidth="0" marginheight="0" scrolling="no" frameborder="0" src="//ws-na.amazon-adsystem.com/widgets/q?ServiceVersion=20070822&OneJS=1&Operation=GetAdHtml&MarketPlace=US&source=ss&ref=as_ss_li_til&ad_type=product_link&tracking_id=peaceinvesting-20&language=en_US&marketplace=amazon®ion=US&placement=1119376629&asins=1119376629&linkId=2f1e6ff64e783437104d091faaedfec7&show_border=true&link_opens_in_new_window=true"></iframe>

[Editor's Note: There are only a few weeks left to register for one of the top medical conferences of 2022. It’s PIMD’s Financial Freedom Through Real Estate Conference, and it’s happening September 23-25 in Los Angeles (and virtually). With several prominent speakers (like Peter Kim and WCI’s own Jim Dahle), you can learn how to pursue financial freedom through real estate investing. It’s an event created by doctors for doctors and other high-income professionals who want to learn the high-yield information and techniques that will allow them to invest with confidence. Sign up for PIMDCON today and begin your journey to the life you’ve always wanted!]

By Andrew Paulson, CSLP, Lead Student Loan Consultant and Co-Founder of our partner site StudentLoanAdvice.com

The long-awaited day has finally arrived for the seventh student loan payment holiday and the announcement of $10,000 of student loan forgiveness. On August 24, President Biden announced that student loan payments have been extended again and will now begin in January 2022. This means status quo for an additional four months—no payments and no interest. Also, the administration passed $10,000 of student loan forgiveness to borrowers making less than $125,000. This will be met with a legal battle, and it certainly will take some time to roll out.

The application is not out yet but you can subscribe to receive a notification for when it does here. Another income-driven repayment option will be released as well.

Here's everything you need to know about the last student loan holiday extension and everything that was announced by the administration.

Student Loan Payment Pause Extended

Federal student loans have been paused since March 2020, and when this most recent extension is completed, it will be close to three years of no payments or interest on your student loans. The president said this is the FINAL pause, but we’ve seen this movie before and I want to see a January 31 payment date before I start to believe it.

Hopefully, you’ve been collecting payment counts for Public Service Loan Forgiveness (PSLF) or have been saving money to throw into your loans if you’re planning to privately refinance. If you haven’t enrolled into auto-pay yet, make sure you log into your servicer’s site and opt in.

Income certification for income-driven repayment (IDR) plans was set to begin in March 2023 but will surely be moved to later in the year. If the past is any indication of the future, the income certification dates will be required six months (at the earliest) after payments resume.

More information here:

How to Ensure Student Loan Forgiveness Through the PSLF Program

Widespread Student Loan Forgiveness

President Biden is using his executive authority under the HEROES Act to forgive student loan debt. The HEROES Act was passed after 9/11 to expand the presidential powers in times of national emergency. COVID-19, categorized as a national emergency, was the catalyst to use the HEROES Act to forgive student loans. In 2021, the Trump administration looked into the Act and concluded in a memo that it didn’t provide the ability to discharge student loan debt.

It’s clear Congress has the ability to cancel student debt but lacks general consensus to do so. This is why the Biden Administration looked into the HEROES Act and concluded in this legal memo it does have the ability to forgive student debt. The executive action will likely be challenged in court.

Borrowers with an annual income during the pandemic of below $125,000 for individuals or below $250,000 for couples who received a Pell grant in college will be eligible for up to $20,000 in forgiveness on their existing federal student loans. If you weren’t eligible for Pell grants, you’re eligible for up to $10,000 of relief. Some households will be eligible for forgiveness of up to $40,000. The amount of loans forgiven won’t be taxed federally as income. However, there may be state taxes levied on this forgiveness for those in a few states. You should consult a tax advisor for your particular state.

The income to be used when you apply for forgiveness is what you’ve submitted on your most recent IDR form. Due to the pandemic, most borrowers haven’t certified their income since 2019 or 2020. If you haven’t enrolled into an IDR plan yet, you will have to report income on a simple application. Reading the tea leaves, I'd assume it's your tax return from 2020 or 2021, because the government has alluded to income during the pandemic. Whatever would be the lower of the two is what you could submit.

Federal student loans eligible for forgiveness are Direct Stafford subsidized/unsubsidized, Direct Consolidation, Direct PLUS Graduate, Parent PLUS, and potentially some Family Federal Education Loans (FFEL). Perkins Loans and private student loans will not be eligible.

The application to sign up for widespread loan forgiveness hasn’t opened yet, but it will in the coming days. Here’s the link to be notified when the application is available.

Here are a few questions I still have (feel free to drop your questions in the comments, and I’ll answer them as best I can):

- What if a borrower is married and makes below $125,000 but has a high-earning spouse that would push them above the $250,000 income threshold as a household and they file taxes Married Filing Separately? If the government follows the pattern for most IDR plans when couples file taxes MFS, it only takes the adjusted gross income of the spouse who has student loans. Therefore, this borrower would qualify because they have income under $125,000.

- Will I be eligible for loan forgiveness while I’m still in school? There isn’t an employment requirement to receive this forgiveness. All it requires is income below the threshold I mentioned earlier and outstanding federal student loans.

- If I borrow loans now, will I be eligible to have those forgiven? Probably not. The cutoff will probably be sometime this summer, like June 30. There are people out there who will try to game the system. Don't be surprised if IRS auditors try to track down those people.

- Are Family Federal Education Loans (FFEL) eligible? I think those that are commercially held won’t qualify and those held by the Department of Education (ED) will. Commercially held FFEL loans would require a direct federal consolidation to be eligible.

- Can this forgiveness be targeted toward my higher interest rate loans? Honestly, I have no idea at this point. We will update when we get more direction.

There are lots of unknowns about how long implementation will take and for some of the nitty-gritty details. As these become available, I'll continue to update this post. However, most of you should not stress over this and change your overall student loan paydown plan. If you haven’t made a plan yet, be sure to check out WCI’s student loan 101 guide or schedule a time with one of our student loan pros.

More information here:

Student Loan Management When Both Spouses Work

New Income-Driven Repayment Plan

The new income-driven repayment plan is still in a proposal state, and it will request public comment. Implementation wouldn’t likely be until the middle to end of 2023. This would now create the sixth IDR option for borrowers which could further complicate repayment plan selection. But it does seem to be particularly beneficial for undergraduate borrowers. Here’s what’s been proposed:

- Monthly payments will be calculated as 5% of discretionary income on undergraduate loans and 10% on graduate loans. Borrowers with both undergraduate and graduate loans will have a prorated payment percentage based upon the percentage of their outstanding debt of undergraduate vs. graduate.

- The poverty line deduction used to calculate discretionary income will be raised from 150% of the federal poverty level to 225%. A household size of 1 deduction (in the lower 48 states) would increase from $20,385 to $30,578.

- Forgiveness will occur after 10 years of payments if you have loan balances of $12,000 or less.

- If monthly interest isn’t covered by your monthly payment, it will be covered by the government. Loan balances will not increase while in this IDR plan when payments are less than interest. This applies to undergraduate loans and I'm not certain if graduates will receive the same treatment. If they do this could be huge for residents.

There is no mention of how spousal income will be treated, if there will be a payment cap, or if you have to qualify for a partial financial hardship to enroll in it. After the proposal process, some of the details could change for this program. I'll update this article as I know more.

What About the PSLF Waiver and IDR Waiver?

The Biden administration and the ED were pretty mum on the PSLF waiver and made no mention of the IDR waiver. The PSLF waiver is set to expire on October 31, 2022, so you need to get your paperwork done before then if you’d like to be considered under the relaxed rules. There have been proposals to implement pieces of the PSLF waiver into actual PSLF law. This consists of counting late payments, partial payments, deferments, and forbearances as PSLF credit.

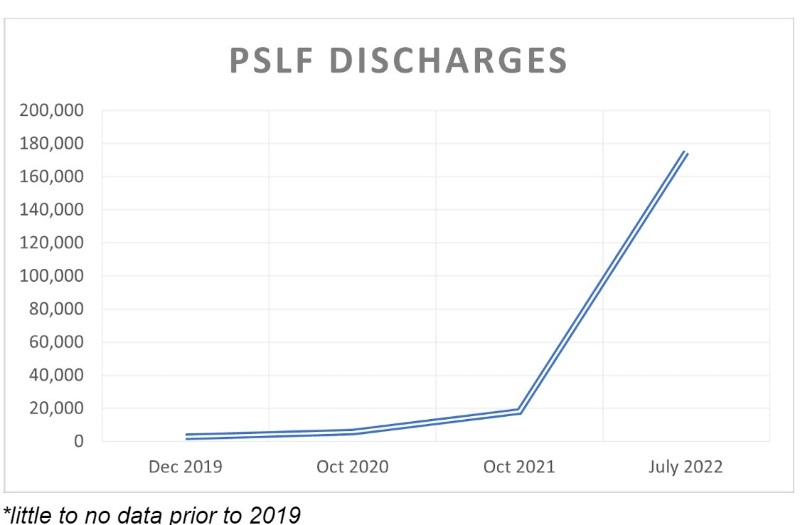

The first four years borrowers were eligible for PSLF, October 2017-October 2021, roughly 18,000 borrowers received it. Since July 2022, more than 175,000 have received it. People are getting their loans forgiven, and it’s mostly older borrowers with FFEL loans.

Is Now the Time to Private Refinance My Student Loans?

With the final payment pause set, it is time to get serious about private refinancing your student loans. Borrowers not pursuing a federal loan forgiveness program should give strong consideration to privately refinancing their loans. Recently, interest rates for refinancing have started to level out, and they might look favorable to what you're paying when payments and interest resume in January 2023. WCI, in partnership with our vetted private student loan lenders, has negotiated a cash bonus for any borrower who refinances their loans by December 31, 2022. And, if you refinance $60,000 or more, WCI will throw in our flagship financial course, Fire Your Financial Advisor: A Step by Step Guide to Creating Your Own Financial Plan, a $799 value.

Student loan programs will continue to change, and it is our hope this process will become easier. Until that time, I will continue to inform you about what you need to know and how to create your plan to tackle your student loans. If you need personalized advice, schedule an appointment with a member of our StudentLoanAdvice.com team.

What do you think about the student loan holiday pause? Does this help you or hurt you? Is this policy fair? Comment below!

The post The Latest Student Loan Holiday Extension: Here’s What to Know appeared first on The White Coat Investor - Investing & Personal Finance for Doctors.

||

----------------------------

By: Josh Katzowitz

Title: The Latest Student Loan Holiday Extension: Here’s What to Know

Sourced From: www.whitecoatinvestor.com/student-loan-holiday-pause-biden-forgiveness-plan/

Published Date: Fri, 26 Aug 2022 06:30:11 +0000

Read More

.png) InvestingStocksToolsClubsVideosPrivacy PolicyTerms And Conditions

InvestingStocksToolsClubsVideosPrivacy PolicyTerms And Conditions