<iframe style="width:120px;height:240px;" marginwidth="0" marginheight="0" scrolling="no" frameborder="0" src="//ws-na.amazon-adsystem.com/widgets/q?ServiceVersion=20070822&OneJS=1&Operation=GetAdHtml&MarketPlace=US&source=ss&ref=as_ss_li_til&ad_type=product_link&tracking_id=peaceinvesting-20&language=en_US&marketplace=amazon®ion=US&placement=0060555661&asins=0060555661&linkId=80f8e3b229e4b6fdde8abb238ddd5f6e&show_border=true&link_opens_in_new_window=true"></iframe>|<iframe style="width:120px;height:240px;" marginwidth="0" marginheight="0" scrolling="no" frameborder="0" src="//ws-na.amazon-adsystem.com/widgets/q?ServiceVersion=20070822&OneJS=1&Operation=GetAdHtml&MarketPlace=US&source=ss&ref=as_ss_li_til&ad_type=product_link&tracking_id=peaceinvesting-20&language=en_US&marketplace=amazon®ion=US&placement=1119404509&asins=1119404509&linkId=0beba130446bb217ea2d9cfdcf3b846b&show_border=true&link_opens_in_new_window=true"></iframe>|<iframe style="width:120px;height:240px;" marginwidth="0" marginheight="0" scrolling="no" frameborder="0" src="//ws-na.amazon-adsystem.com/widgets/q?ServiceVersion=20070822&OneJS=1&Operation=GetAdHtml&MarketPlace=US&source=ss&ref=as_ss_li_til&ad_type=product_link&tracking_id=peaceinvesting-20&language=en_US&marketplace=amazon®ion=US&placement=1119376629&asins=1119376629&linkId=2f1e6ff64e783437104d091faaedfec7&show_border=true&link_opens_in_new_window=true"></iframe>

[Editor's Note: Here's an update on the Public Service Loan Forgiveness program (and this one is NOT an April Fools' Joke like Monday's post): PSLF certifications have been paused from May 2024 to July 2024. This should not affect people getting PSLF but rather just when they get notice that their student loans have been forgiven.]

By Dr. Jim Dahle, WCI Founder

I've written numerous times about the concept of a safe withdrawal rate (SWR), including these posts:

- The 4% Rule and Safe Withdrawal Rates

- 3% Is the New 4%? The Safe Withdrawal Retirement Rate

- How Much Will You Probably Die With?

However, the silliness of it all continues, and today I'm going to rant like never before on this topic in the hopes of realigning how people think about this concept.

What Is a Safe Withdrawal Rate?

The concept of a safe withdrawal rate is that a retiree can withdraw a certain amount of the portfolio value at retirement each year (usually indexed to inflation) with little risk of running out of money. That amount is the safe withdrawal rate. Note that it is NOT a GUARANTEED withdrawal rate. It is a SAFE withdrawal rate. If you want guarantees, look into insurance products such as Single Premium Immediate Annuities (SPIAs). Unfortunately, you can't really get inflation-indexed SPIAS anymore. Your best option there is to delay Social Security to 70.

Where Does the Safe Withdrawal Rate Concept Come From?

While not the first people to look at the concept, the SWR concept was popularized by the Trinity Study in the 1990s. Back then, financial advisors were telling their clients that if their portfolio was earning 8% a year on average, they could spend 8% a year without any fear of running out of money. Some were even more aggressive with spending because of the outsized equity returns of the late 1990s. However, the problem with this approach (aside from the fact that late 1990s equity returns were far above average) was that it did not address the problem of Sequence Of Returns Risk (SORR). In a nutshell, SORR is when, despite having adequate (again, let's say 8%) average portfolio returns throughout retirement, the portfolio will run out of money prior to death if the crummy returns show up first during early retirement. Withdrawing a large amount from a portfolio while it is falling in value can decimate a portfolio relatively quickly.

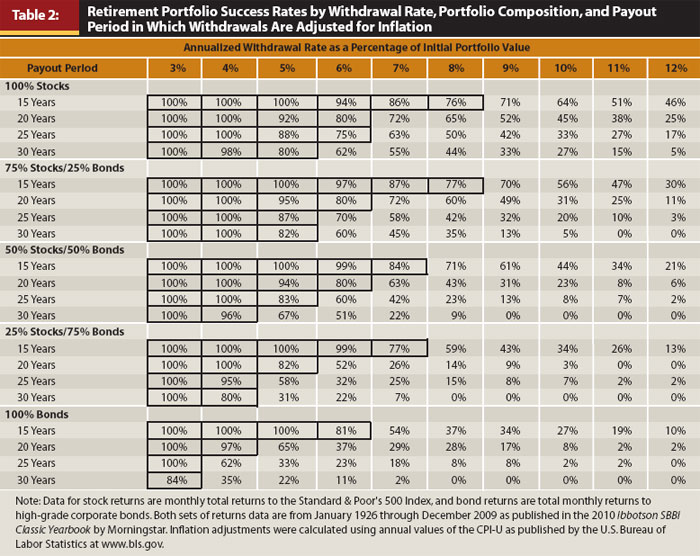

The Trinity researchers looked at the best database available (US stock and bond returns from 1927 on in rolling time periods), applied various time periods (15, 20, 25, and 30 years) and various asset allocations ranging from 100% bonds to 100% stocks, and then applied withdrawal rates from 3%-12% to see what percentage of the time the portfolio survived. This is what the data showed:

For a 30-year retirement with a 50/50 portfolio, a 3% withdrawal rate survived 100% of the time, a 4% withdrawal rate survived 96% of the time, a 5% withdrawal rate worked 2/3 of the time, a 6% withdrawal rate worked half the time, and an 8% withdrawal rate worked 10% of the time. Thus, advisors telling clients they could take out 8% were doing a huge disservice to them.

This is the birth of the 4% Rule. Four percent is a “safe withdrawal rate.” Maybe you could call 3% a “guaranteed withdrawal rate” (although there is never a guarantee in life, especially when it comes to market returns).

More information here:

4 Methods of Reducing Sequence of Returns Risk

What Is the Problem with the Safe Withdrawal Rate?

The problem with the SWR is engineers. What do I mean by that? Well, nothing too sinister. My father is an engineer. But engineers love to solve problems. And they love data. And they love spreadsheets. And they love planning way in advance. We need engineers for many things in life. But we don't need them when it comes to planning your retirement. What happens when you get engineers involved? You get people arguing about whether 3.67% or 3.74% is the correct safe withdrawal rate. Reminds me of the old joke:

“How do you know economists have a sense of humor?

They use decimal points.”

If you think economists use decimal points, you should check out engineers.

Injecting precision that doesn't exist into a process might make you feel better, but it certainly doesn't make the data any more useful. Consider the source of the data: less than 100 years of market returns in a single country. While there might be dozens of rolling 30-year time periods, there are fewer than four independent 30-year data points. You can't use a dataset like that and then pretend you can get some sort of precise answer out of it. The correct answer to “what is a safe withdrawal rate?” is “something around 4%, probably in the 3%-6% range.” Not 3.59% or 4.21%.

Pessimism Is Sexy

The other problem with the folks that get into this SWR stuff is that they like to look at all the possible reasons why a SWR could be much less than 4%. Maybe they project lower equity returns or bond yields are lower or the world seems scarier or whatever. They forget that the Trinity Study database (including updates) includes events such as:

- The Great Depression

- World War II

- The inflation of the 1940s

- The stagflation of the 1970s

- The Cold War

- October 19, 1987 (look it up)

- The Asian Contagion

- The meltdown of long-term capital management

- The dot.com bubble and bust

- The Global Financial Crisis

- Several cryptocurrency winters

- The COVID pandemic

That's a lot of bad stuff. So, when people are saying that the future will be worse, wow, that's pretty pessimistic. Especially since economic history should be titled “The Triumph of the Optimists.” But pessimism is sexy. In his excellent book “The Psychology of Money,” Morgan Housel wrote:

“Optimism sounds like a sales pitch. Pessimism sounds like someone trying to help you.”

“Pessimism just sounds smarter and more plausible than optimism.”

“Pessimism isn’t just more common than optimism. It also sounds smarter. It’s intellectually captivating, and it’s paid more attention than optimism, which is often viewed as being oblivious to risk.”

“It’s easier to create a narrative around pessimism because the story pieces tend to be fresher and more recent. Optimistic narratives require looking at a long stretch of history and developments, which people tend to forget and take more effort to piece together.”

“The intellectual allure of pessimism has been known for ages. John Stuart Mill wrote in the 1840s: ‘I have observed that not the man who hopes when others despair, but the man who despairs when others hope, is admired by a large class of persons as a sage.'”

Get a bunch of engineers cranking numbers using past data and current yields, and, all of a sudden, they start competing to see who can be the most pessimistic. Some small percentage of them might even be neurotic, maybe even a little OCD. But all of a sudden, people are talking about 2% being the safe withdrawal rate. Maybe 1.5% if you retire early. It's bonkers. That's what that is.

The Silliness of Safe Withdrawal Rates

If you go down this rabbit hole too far (and you don't have to go very far to go too far), you will meet a lot of strange people who try to convince you otherwise. They are mistaken. That's God's honest truth about withdrawal rates. Go back to that chart. Take a look at the 75/25 30-year line. It's 100%. In all of recorded financial history, a 4% (adjusted for inflation) withdrawal rate NEVER ran out of money. In fact, on average after 30 years. the portfolio was 2.7X the original portfolio value. Even if you decide you're going to do 5% of the original portfolio value (again, adjusted upward each year with inflation), it worked more than four out of five times.

How Long Is Retirement?

The average American retires at 64. The average life expectancy of a 64-year-old is 17 (male) to 20 (female) years. What's the table look like for a 20-year retirement? The 75/25 20-year line shows that you can withdraw 9% a year and only run out of money half the time. Nine percent! And you've got these crackpot engineers running around telling people they can only take out 2% a year. By the way, if you're a financial advisor and you're telling your 92-year-old client she can only spend 4% a year, you're a jerk. You can have very aggressive withdrawal rates for short time periods without any problem. There's a reason the RMD for a 92-year-old (9.8% of portfolio) is more than twice as large as that of a 75-year-old (4%).

More information here:

The Risk of Retirement

The TIPS SWR

Financial advisor Allan Roth took a look at a portfolio that was 100% TIPS at our current yields and determined that one could take out 4.36% a year, adjusted to inflation, and your money would be guaranteed to last 30 years. You don't even have to take any risk, and you can get 30 years of 4%+ inflation-adjusted withdrawals. You're not immortal. It's OK to spend some principal. Now, maybe you're retiring at 45, and 30 years isn't quite enough to feel comfortable. Fine. The difference in withdrawal rate between a portfolio that will last 30 years and a portfolio that will last forever is pretty trivial. Besides, how many 45-year-old retirees do you know who NEVER earn another dollar? There are not very many of them. Even the most diehard physician FIRE dude I know left medicine at 43, and he is still earning a little income.

Larimore vs. Pfau and Big ERN on SWR

I have three friends. We'll call the first one Taylor Larimore. Let's say he's a 100-year-old World War II vet who retired in 1980 at 55 on $1 million, and he has been living on it ever since. His philosophy on spending money in retirement is to “adjust as you go.” You simply take a look at how much you have and adjust how much you spend based on that. In a year when you earn a lot, you spend more. After a bad year or two, maybe you spend and give a little less. He bought a couple of SPIAs in his ninth decade of life and mostly lives off those and Social Security these days.

Let's call my second friend Wade Pfau. Let's just say he's a “retirement researcher” who makes his living off publishing study after study about safe withdrawal rates. Boy, does he ever like to get into the weeds on this stuff! Publish or perish you know, and this area of research has been fertile ground over the years. He has argued that the SWR is 2.4%.

Let's call my third friend Big ERN. While not an engineer (he's an economist by training), he has published a long, detailed blog series about safe withdrawal rates that rivals Pfau's work. He has also argued for a sub-4 % withdrawal rate.

Who's right and who's wrong? People say Taylor was just lucky. He retired at the beginning of the longest bull market in history. He won't be the last person who retires at the beginning of a bull market. If Pfau likes 2.4%, he's going to love the 0% withdrawal rate many retirees are currently using. Big ERN says adjusting as you go might mean a 15- or 20-year adjustment in spending, and he calls that “failure.” Calling having to make an adjustment “a failure” seems overly harsh to me. That's just how life works, both in accumulation and decumulation.

More information here:

Let’s Celebrate Taylor Larimore’s 100th Birthday by Asking Him 4 Questions About Money

SPIAs

If you go down the rabbit hole and end up with something like a 2% withdrawal rate, you need to seriously reconsider your approach. If you are so worried about running out of money that you are only willing to spend 2% a year, you should do something to reduce that anxiety. Here are some great options:

- Delay Social Security to age 70. This is the best deal out there for an inflation-indexed annuity.

- Buy a SPIA or two. Use these together with Social Security and any pensions to put a floor under your retirement. Even if your portfolio totally fails, you won't be eating Alpo.

- Ladder some TIPS. It's 4.36% for 30 years at today's yields. Yes, you could live longer than 30 years, I suppose. Maybe cut it back to 4% instead of 4.36%.

A Real Retirement Spending Plan

Few who have looked at this problem seriously actually advocate for a systematic withdrawal plan based solely on the initial portfolio value that never changes over the following decades. Most recommend a variable withdrawal plan based on returns as you go along. Whether you want to formalize that or just eyeball it like Taylor is up to you. In essence, the risk is SORR, i.e., the idea that you get terrible returns in the first few years of retirement. If that happens, you stick with something like 4% or even less. If it doesn't happen, you can spend 5%, 6%, or even more and be fine.

But you don't have to stick with the same stupid withdrawal rate for 30 years if your first three years go terribly. Just like you adjusted your spending to your income during your working years, you can do the same during your retirement years. If your retirement spending is 100% fixed and predetermined, you probably retired too early with too little money. It's one thing if you were forced to do that, but if you did that voluntarily, that's on you.

My advice on retirement spending is this:

Start at something around 4% of the portfolio value and adjust as you go.

That's it. It's that simple. The more uncomfortable you are with that plan, the more you should put into SPIAs and TIPS ladders. The more comfortable you are, the more you can leave in stocks and bonds and the more you can likely spend in retirement and leave to heirs.

Reverse Engineering

Perhaps the biggest benefit of the 4% Rule Guideline is figuring out how much you need to retire. For example, consider a doctor who needs $120,000 a year in today's dollars to retire and who saves $50,000 a year in today's dollars for retirement and earns 5% real (after inflation) on the investments. How long does this doctor need to work and save? It depends on the withdrawal rate.

- 5%: 25 years =NPER(5%,-50000,0,120000/5%)

- 4%: 28 years =NPER(5%,-50000,0,120000/4%)

- 3.5%: 30 years =NPER(5%,-50000,0,120000/3.5%)

- 3.33%: 31 years =NPER(5%,-50000,0,120000/3.33%)

- 3%: 33 years =NPER(5%,-50000,0,120000/3%)

- 2.5%: 36 years =NPER(5%,-50000,0,120000/2.5%)

That's an 11-year difference between someone willing to “risk it” with a 5% withdrawal rate (which will probably work, especially if you're willing to be flexible) and someone who went down Wade Pfau's rabbit hole. Maybe 11 years doesn't seem that long to you. But think about it this way.

Retirement is often divided into the “go-go years,” the “slow-go years,” and the “no-go years.” Perhaps, on average, it stacks up like this:

- Go-go years: Age 65-75

- Slow-go years: Age 75-85

- No-go years: Age 85+

Let's say you're a doctor who started saving upon exiting residency at age 33. Age 33 plus 36 years equals age 69. That leaves you six go-go years. On the other hand, if you retired after 25 years, you retired at 58. That leaves you 17 go-go years. That's almost three times as many of the best years of retirement. Does it matter? Absolutely it does.

More information here:

8 Ways to Spend More Money

Doesn't Matter for Many

For many white coat investors, however, the debate about safe withdrawal rates is purely academic. Because they enjoyed their work so much and were so talented at earning, saving, and investing, they hit FI long before they were actually ready to be done working. As you can see, it doesn't take that many years to go from a 4% withdrawal rate to a 2.5% withdrawal rate. Perhaps eight years. Maybe less with an inheritance or other windfall or a particularly high savings rate. If you were planning to retire at 55 but hit FI at 47, you now face an enviable dilemma. You can retire early. You can spend more money in retirement. You can give more money away during retirement. Or you can stress less about running out of money and probably give away more at death. I hope we all get to face THAT dilemma! You can whine about your RMD problem while you're at it.

Rich, Broke, or Dead

The SWR movement is composed of a lot of well-meaning but anxious people advocating for ridiculous less than ideal recommendations. Understand the concepts, but don't fall for their arguments. It's OK to spend your money. You're far more likely to end up dead with a huge portfolio than broke and wishing you had more. Don't forget the lessons of the Rich, Broke, or Dead graph. Green is rich. Red is broke. Black is dead. In the end, we're all dead, and most of us were rich right up until the end.

What do you think? Why do people get so pessimistic about withdrawal rates? What is your retirement spending plan? Comment below!

The post The Silliness of the Safe Withdrawal Rate Movement appeared first on The White Coat Investor - Investing & Personal Finance for Doctors.

||

----------------------------

By: The White Coat Investor

Title: The Silliness of the Safe Withdrawal Rate Movement

Sourced From: www.whitecoatinvestor.com/safe-withdrawal-rate-movement/

Published Date: Fri, 05 Apr 2024 06:30:41 +0000

Read More

.png) InvestingStocksToolsClubsVideosPrivacy PolicyTerms And Conditions

InvestingStocksToolsClubsVideosPrivacy PolicyTerms And Conditions