<iframe style="width:120px;height:240px;" marginwidth="0" marginheight="0" scrolling="no" frameborder="0" src="//ws-na.amazon-adsystem.com/widgets/q?ServiceVersion=20070822&OneJS=1&Operation=GetAdHtml&MarketPlace=US&source=ss&ref=as_ss_li_til&ad_type=product_link&tracking_id=peaceinvesting-20&language=en_US&marketplace=amazon®ion=US&placement=0060555661&asins=0060555661&linkId=80f8e3b229e4b6fdde8abb238ddd5f6e&show_border=true&link_opens_in_new_window=true"></iframe>|<iframe style="width:120px;height:240px;" marginwidth="0" marginheight="0" scrolling="no" frameborder="0" src="//ws-na.amazon-adsystem.com/widgets/q?ServiceVersion=20070822&OneJS=1&Operation=GetAdHtml&MarketPlace=US&source=ss&ref=as_ss_li_til&ad_type=product_link&tracking_id=peaceinvesting-20&language=en_US&marketplace=amazon®ion=US&placement=1119404509&asins=1119404509&linkId=0beba130446bb217ea2d9cfdcf3b846b&show_border=true&link_opens_in_new_window=true"></iframe>|<iframe style="width:120px;height:240px;" marginwidth="0" marginheight="0" scrolling="no" frameborder="0" src="//ws-na.amazon-adsystem.com/widgets/q?ServiceVersion=20070822&OneJS=1&Operation=GetAdHtml&MarketPlace=US&source=ss&ref=as_ss_li_til&ad_type=product_link&tracking_id=peaceinvesting-20&language=en_US&marketplace=amazon®ion=US&placement=1119376629&asins=1119376629&linkId=2f1e6ff64e783437104d091faaedfec7&show_border=true&link_opens_in_new_window=true"></iframe>

By Andrew Paulson, CSLP, Lead Student Loan Consultant and Co-Founder of our partner site StudentLoanAdvice.com

Yes, it’s true. The federal student loan pause that began during the COVID pandemic is ending, and after a three-and-a-half-year hiatus, loan payments and interest are beginning once again. Interest starts accruing in September 2023, and payments will be due in October. If you were in a repayment plan prior to the pause, you should still be in that repayment plan unless you’ve switched since then. If you have never entered a repayment plan or need to switch repayment plans, you should do so now.

In anticipation of the payment restart, here are a couple of things to consider to ensure you’re ready.

Create a Budget for Your Monthly Payments

The first thing you need to do is understand how much you can carve out of your monthly budget for your student loan payments. If you were making $5,000 per month as a resident and are now making $25,000 per month as an attending, there’s another $20,000 you could be throwing toward your loan. Of course, you want to put a little buffer in there for increased retirement contributions and lifestyle inflation in case you are buying a house, starting a family, or moving to a more expensive neighborhood.

Yes, you could double your monthly take-home pay and still have $15,000 to pay down your loans. But before you start paying off your loan like your hair is on fire, you need to consider what repayment track you are on.

Most high earners will pay down their student loans by one of two methods:

- Live Like a Resident (aka aggressive paydown) or

- Public Service Loan Forgiveness (PSLF)

Decide If You Should Refinance Your Student Loans

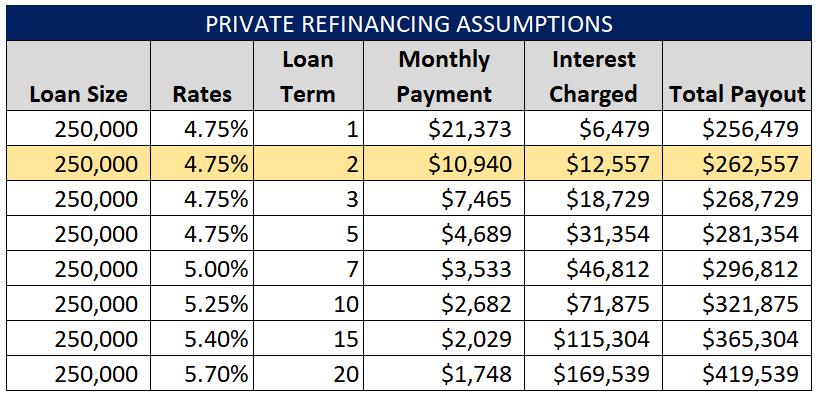

If you’re planning on aggressively paying down your loans, you should first consider private refinancing your student loans to see if you can obtain a lower interest rate. After you have secured a lower interest rate (if you were able to drop your interest rate at all), determine the term or length of repayment.

This table shows what the potential interest rates would be if you were to refinance $250,000 of student loans right now with an attending income and excellent credit. If you live like a resident, you could select a five-year term and be out of debt in five years. You could be debt free in TWO YEARS if you pay ~$11,000 per month. Sounds pretty enticing to be student debt free that soon.

The longer you keep your loan, the more interest you’ll likely have to pay. Unfortunately, rates in the 1%-2% range don’t exist with refinancing right now, but there’s still some value for those who plan to pay down their loans aggressively.

If you are planning on PSLF, your objective is to pay the least amount possible toward your student loans. Whatever balance you have forgiven after a decade is TAX-FREE so don’t put extra money into your student loans if you're on the PSLF track. Put it into retirement, real estate, college savings accounts, future vacations, etc. You can drop your monthly payments by contributing to pre-tax accounts or filing separately if you have a spouse that works.

In either case, you’ll likely be out of debt in a maximum of 10 years after you graduate from medical school.

More information here:

Student Loans 101: Ultimate Guide to Student Loans

Refinance Student Loans and Pay Off or Go for PSLF?

Consider a Loan Forgiveness Option

There are a number of federal loan forgiveness programs. PSLF is the most common we see with our audience, and it has increased in popularity due to its recent success. But, there’s also IDR forgiveness.

PSLF takes 10 years of payments in an income-driven repayment (IDR) plan, working at least 30 hours per week at a nonprofit. When you reach your forgiveness milestone, there are no taxes due on the balance forgiven.

IDR forgiveness is 20-25 years of payments in an IDR plan, and it doesn’t have any particular work requirement. That means you don’t even have to be employed to qualify for this plan. However, when you reach your forgiveness milestone, the balance is taxed. So, if you had $300,000 forgiven in 20 years, you could end up paying more than six figures in taxes that year.

Please note: Those who receive IDR forgiveness prior to 2026 will not be taxed on their debt balance forgiveness. This benefit of the American Rescue Plan Act of 2021 will sunset in 2026.

Those who make more money than they owe in loans should not consider loan forgiveness as an option. However, with the three years of payment pause, many have kept their loans federal and continued to receive forgiveness credit during the pause. If you’re only a couple of years away from either forgiveness milestone, you might be better off sticking with it since you haven’t paid a dime on these loans for 3+ years.

For our PSLF clients, we are seeing that they will only pay around one-third of what they borrowed for school—even if they go into a high-earning specialty. If you borrowed $300,000, you’d likely only have to pay $100,000 over a decade to reach PSLF. Not a bad deal for that expensive education. Of course, these numbers can change slightly if you only train for 3-4 years and start making more than you owe right away. PSLF generally favors those going into surgical specialties and fellowships because of the additional years at a lower income.

As a rule of thumb, if your debt-to-attending-income ratio is 1:1 or greater, you should consider PSLF. And if you have extended training of five-plus years, you should run the numbers. We’ve recently met with docs in orthopedics, ENT, and radiology who thought they made too much for PSLF before discovering they would actually benefit from it now.

Those not considering PSLF and wondering about eligibility for IDR forgiveness need to have a debt-to-attending-income ratio of roughly 2.5:1 or greater. Very few physicians will pursue this track unless they work part-time or are career changers. This track is more common for those who are dentists, attorneys, animal doctors (veterinarians), and chiropractors.

If you made any payments on direct loans during the pause, you can request your servicer refund you that money. This is a good idea if you are on forgiveness since non-payments during the pause count, and you can use those funds toward future monthly payments.

More information here:

Is Public Service Loan Forgiveness Worth It for Doctors?

12 Reasons I Hate Income Driven Repayment Forgiveness Programs

SAVE Plan Is Available When Payments Start

When President Joe Biden’s $10,000-$20,000 of forgiveness was blocked by the Supreme Court in June 2023, the administration announced Saving on a Valuable Education (SAVE) would be available for borrowers when payments resume this year. SAVE is an IDR plan that replaces the REPAYE payment program. It qualifies for the federal forgiveness programs discussed earlier. If you are already in the REPAYE plan, you will automatically be placed in the SAVE program.

The SAVE program is the most affordable program if you only borrowed for undergrad. If you borrowed for graduate school, it will be the most affordable option for many (but not all). Here are a couple of quick points on SAVE and changes in IDR plans going forward.

- In SAVE, monthly payments are calculated by taking 5% of discretionary income for undergraduate loans and 10% for graduate loans. When you have a combination of both, the weighted average of the two will be taken to calculate your monthly payments.

- Instead of taking 150% of the poverty line to calculate your discretionary income, SAVE will take 225%. This should drop your monthly payments. The larger your household, the larger the deduction for which you’ll be eligible.

- If you make your monthly payment, no accrued interest will be added to your loan balance. For example: If $500 in interest accumulates each month and you have a $200 payment, the remaining $300 would not be charged. In the past, the interest subsidy was not nearly as generous, usually covering one-half of unpaid interest.

- SAVE allows the exclusion of spousal income if you file taxes Married Filing Separately. In the past, this was not available to borrowers in REPAYE.

- PAYE and ICR will be phased out to new borrowers in July 2024 (ICR will still be available to Parent PLUS loan borrowers). If you’re considering either of those plans, make sure you’re in them before that date.

- If, as of July 1, 2024 (or beyond), you've made 60 or more payments under REPAYE, you may not switch to the Income-Based Repayment plan.

- Unlike the PAYE and IBR repayment plans, SAVE does not have a payment cap based on the standard 10-year repayment plan.

Here’s an example of a borrower who owes $250,000 from graduate school and makes $250,000 per year. They are married with a stay-at-home spouse and two kids.

Borrowers who make less than they owe in student loans should strongly consider switching into SAVE. Those who will make more than they owe should be wary of entering the SAVE program. You might be better off staying in IBR or PAYE. To see more scenarios, check out our recent post on SAVE.

Income Recertification

Income recertification is an annual requirement to stay current with your loan servicer if you’re in an IDR plan. Certification has been postponed during the student loan pause for more than three years. If you are already in an IDR plan, you shouldn’t have to recertify until around February/March 2024 at the earliest. Also, if you log into your servicer’s website and see a date before then, it will be pushed back an entire year. For example, if your recertification date is marked for November 2023, assume it will restart in November 2024. We are seeing lots of servicers tell borrowers they need to recertify now. This is not true unless you’ve never enrolled in a repayment plan.

For those who graduated during the payment pause, you’ll need to make sure you’re in a repayment plan when payments start in October. We strongly suggest enrolling into a repayment plan now.

If you’re enrolling for the first time, switching plans, or consolidating, you are required to submit income certification (a recent tax return or pay stub) to enroll in an IDR plan. Right now, borrowers can self-certify income. Yes, you read that right. No supporting income documentation is required. Also, beginning in 2024, you'll be allowed to automate your income recertification.

12-Month Onramp for Student Loan Repayment

To help borrowers move back into repayment, the Department of Education is giving borrowers a 12-month runway to resume repayment. This means you could extend forbearance until September 30, 2024. Those who miss a monthly payment during this time would not be considered delinquent or placed in default. Unlike the government-mandated pause from March 2020-September 2023, interest WILL accrue and non-payments WILL NOT be treated as qualifying months for either forgiveness track.

The student loan pause was a large benefit to many with mortgage-sized student loan balances, due to no payments and no interest. Despite the hardships of the pandemic, you hopefully moved closer to your financial goals through retirement savings, buying a home, etc.

With the imminent start of payments, make sure you’re signed up for the correct repayment plan and that you have an overall plan of attack to pay down your loans. If you need help running the numbers, StudentLoanAdvice.com has a team of student loan professionals who can help walk you through all the scenarios. StudentLoanAdvice.com will help you select the best way to pay down your debt.

What do you think? Are you going for PSLF or aggressively paying down your loans? What actions do you need to take before payments restart? Comment below!

The post Student Loan Payments Are Resuming — Now What? appeared first on The White Coat Investor - Investing & Personal Finance for Doctors.

||

----------------------------

By: Andrew StudentLoanAdvice

Title: Student Loan Payments Are Resuming — Now What?

Sourced From: www.whitecoatinvestor.com/student-loan-payments-resuming-now/

Published Date: Wed, 02 Aug 2023 06:30:06 +0000

Read More

Did you miss our previous article...

https://peaceofmindinvesting.com/investing/budgeting-for-a-new-doctor

.png) InvestingStocksToolsClubsVideosPrivacy PolicyTerms And Conditions

InvestingStocksToolsClubsVideosPrivacy PolicyTerms And Conditions