<iframe style="width:120px;height:240px;" marginwidth="0" marginheight="0" scrolling="no" frameborder="0" src="//ws-na.amazon-adsystem.com/widgets/q?ServiceVersion=20070822&OneJS=1&Operation=GetAdHtml&MarketPlace=US&source=ss&ref=as_ss_li_til&ad_type=product_link&tracking_id=peaceinvesting-20&language=en_US&marketplace=amazon®ion=US&placement=0060555661&asins=0060555661&linkId=80f8e3b229e4b6fdde8abb238ddd5f6e&show_border=true&link_opens_in_new_window=true"></iframe>|<iframe style="width:120px;height:240px;" marginwidth="0" marginheight="0" scrolling="no" frameborder="0" src="//ws-na.amazon-adsystem.com/widgets/q?ServiceVersion=20070822&OneJS=1&Operation=GetAdHtml&MarketPlace=US&source=ss&ref=as_ss_li_til&ad_type=product_link&tracking_id=peaceinvesting-20&language=en_US&marketplace=amazon®ion=US&placement=1119404509&asins=1119404509&linkId=0beba130446bb217ea2d9cfdcf3b846b&show_border=true&link_opens_in_new_window=true"></iframe>|<iframe style="width:120px;height:240px;" marginwidth="0" marginheight="0" scrolling="no" frameborder="0" src="//ws-na.amazon-adsystem.com/widgets/q?ServiceVersion=20070822&OneJS=1&Operation=GetAdHtml&MarketPlace=US&source=ss&ref=as_ss_li_til&ad_type=product_link&tracking_id=peaceinvesting-20&language=en_US&marketplace=amazon®ion=US&placement=1119376629&asins=1119376629&linkId=2f1e6ff64e783437104d091faaedfec7&show_border=true&link_opens_in_new_window=true"></iframe>

[Editor's Note: Deadline alert! Today is the last day to register for early-bird pricing for the Physician Wellness and Financial Literacy Conference (WCICON23). After midnight MT, the price to attend the best medical conference of the year will increase by $300. You already know that WCICON23 (March 1-4) will give you the tools to learn about financial freedom and burnout prevention—all while earning up to 17 hours of CME. Register today before early-bird pricing ends, and start saving before you even step into the conference center!]

By Dr. James M. Dahle, WCI Founder

Inflation should be a major consideration in portfolio design. Of the four “deep risks”

-

-

-

-

- Inflation,

- Deflation,

- Confiscation, and

- Devastation,

inflation is, by far, the most common. That's why, when I designed my own portfolio, it was designed first and foremost to best inflation in the long-term. Each component was designed to do reasonably well no matter what future inflation may be.

- 60% Stocks: Stocks are fractional ownership of the most profitable companies ever made in the history of the world. As inflation rises, these companies can charge more for their products and services, countering the effects of inflation in the long run.

- 20% Real Estate: Real estate goes up in value with inflation, since it can charge higher rents as inflation rises. Inflation also makes it easier to pay down the fixed leverage typically used in real estate ventures with less and less valuable dollars each year. Again, this is only in the long run. Rising inflation often triggers a recession that decreases the value of real estate in the short term.

- 10% Nominal Bonds: While nominal bonds are the asset class most heavily affected by inflation, the damage here can be mitigated by keeping the bonds short-term. My primary nominal bond holding over the years has been the TSP G Fund, the shortest duration bond fund on the planet. In more recent years, I have had to add bonds to my taxable account to maintain my desired asset allocation, but I still do not use bonds with long maturities. Short-term bonds can be reinvested at the new, higher interest rates much sooner than long-term bonds.

- 10% Inflation-Indexed Bonds: I Bonds and TIPS are designed to adjust upward with inflation, making them some of the safest bonds in the long run because they protect against the major risk of bonds—inflation.

Today, we're going to focus on that last category, the inflation-indexed bonds. We're going to see what's going on in today's markets, as of October 2022, and what you can do to protect your bond portfolio from inflation.

New I Bond Rate

I Bonds are a type of savings bond issued by the US government. The I stands for Inflation. The other type of savings bond, EE Bonds (don't ask me what EE stands for, but they're also called Patriot Bonds) are not indexed to inflation, but I Bonds are. I Bonds never go down in value, but how much they go up depends on two things: a fixed rate and the rate of inflation. Once issued, the fixed rate never changes. It is set for newly issued I Bonds every six months, in May and November. As the years go by, however, the rate of inflation changes and so does the yield on I Bonds to keep up with it. That inflation rate is only changed every May and November. Just to keep things confusing, when you buy an I bond, you get the inflation rate currently in effect for the next six months—even if you buy the I bond in March or September—and then it changes to the new rate for the next six months.

Since the origin of I Bonds in 1998, this fixed rate has varied from as high as 3.8% to as low as 0.0%, where it has been since the COVID-19 pandemic started.

Again, to keep things maximally confusing, this is the formula used for the composite rate:

Composite rate = Fixed rate + 2 x semi-annual inflation rate + fixed rate x semi-annual inflation rate

The composite rate for May 2022-October 2022 is 9.62%. The formula looks like this:

9.62% = 0.00% + 2 * 4.81% + 0 * 4.81%

The semi-annual inflation rate comes from the change in the CPI-U inflation index for the prior six months. The rate is easily calculated once the data is released. The latest data was released on November 1, and the semi-annual inflation rate is 3.24%.

When you combine the new fixed rate of 0.4% with the new inflation rate of 3.24%, you get:

6.89%

That's what I Bonds purchased during the next six months will yield for their first six months. Why is the rate lower now than it was earlier in 2022? Mostly because inflation, at least as measured by CPI-U, wasn't too bad the last few months. Here are the actual monthly numbers:

- May 1.10%

- June 1.37%

- July -0.01%

- August -0.04%

- September 0.22%

Current TIPS Rates

TIPS are a form of US Treasury Bond (TIPS = Treasury Inflation Protected Securities) that is also indexed to the CPI-U inflation index. New issues of TIPS are for five, 10, and 30 years, but TIPS of any maturity < 30 years can be purchased on the secondary market. At issue, the TIPS have a fixed “real” (after-inflation) yield that remains fixed for their entire life. Added to this is the inflation component, which is essentially added to the value of the bond periodically. So, if the bond had a value of $1,000 when you purchased it and inflation was 5% that first year, the bond will have a value of $1,050 at the end of the first year. The real yield will then be calculated using that new, higher value.

What has really changed in 2022 is not the I Bond yield, it's the TIPS yields. Since TIPS were first issued in 1997, the real yield on TIPS has varied from as high as 4.13% to as low as -1.6%, which is where it was in March 2022. In just a few months, from then until October, that yield skyrocketed. Here is the TIPS yield curve on October 19, 2022:

- 5-Year: 1.89%

- 7-Year: 1.78%

- 10-Year: 1.72%

- 20-Year: 1.74%

- 30-Year: 1.79%

Two things to notice there. First, it's very flat. In fact, it's even slightly inverted, which makes everyone worry about a recession since inverted yield curves have predicted something like the last 10 recessions. Second, the numbers are all just a whole lot bigger since March. Since March, the real yield on a 10-year TIPS has gone up by 3.3%! This is the largest and most rapid rise in TIPS yields EVER. Check out the chart for the 10-year:

Pretty cool right? In March 2022, everyone was climbing all over each other to buy I Bonds, but now just the opposite is happening. People are saying, “Why buy an I Bond with a tiny real rate when I can buy a TIPS with a 1.7% real rate?

How did TIPS yields get so juicy? Well, interest rates went up, both on a nominal basis and on a real basis. Those of us who have owned TIPS this year have really not enjoyed the experience. The Vanguard Inflation Protected Securities Fund is down 13.42% YTD as of October 19. When rates go up, the value of existing bonds goes down, but at least the future return on those bonds (as well as newly purchased ones) goes up. If you hold TIPS until maturity, you won't lose principal. But if you're buying and selling them (or investing via a fund that is buying and selling them), you can lose principal.

You can buy TIPS straight from the government at TreasuryDirect, or you can buy them via a fund such as the Vanguard Inflation Protected Securities Fund (VAIPX) or via ETFs such as the Schwab SCHP, the iShares TIP, or the Vanguard VTIP. The convenience and liquidity of the funds and ETFs will only cost you a few basis points, but it does introduce the risk of potential loss of principal.

Should I Buy I Bonds or TIPS?

Given current yields, as of late 2022, the answer is clearly TIPS. However, yields change frequently, and since both of these instruments are designed to be held for the long term, you will likely end up with a combination of both types of inflation-indexed bonds in your portfolio.

Comparing I Bonds to TIPS

Still don't get it? Don't worry, despite the simplicity of the proposition (bonds that keep up with inflation), these are investments that are some of the most difficult to understand. For example, most people thought TIPS would do great in a year of unexpectedly high inflation like 2022; yet they performed just as badly as other bonds. As William Bernstein likes to say, TIPS are a riskless asset in the long run, but a risky asset in the short run. Let me try to point out the important differences between the two types of bonds

Amount You Can Buy

An individual is only allowed to buy $10,000 a year of I Bonds but can buy an unlimited amount of TIPS. This is an important difference that introduces a lot of hassle if I Bonds are your preferred investment. You can also buy a TIPS fund or an ETF for convenience and liquidity, but there are no I Bond mutual funds. It is much easier to set up a TIPS ladder than an I Bonds ladder. For example, if you wanted a 20-year ladder, you could buy 20-year, 19-year, 18-year, etc. TIPS on the open market today. But if you wanted to build a 20-year I Bonds ladder, it would take you 20 years to do it. (See the discussion about gifting I Bonds to your spouse later for a possible exception).

Mechanism of Setting the Fixed Rates

While the inflation adjustment uses the same inflation index (CPI-U), the fixed portion varies. With an I Bond, it is set by the government every May and November. With a TIPS, it is set by the market; TIPS are auctioned off so there is a market mechanism determining their rates.

Mechanism of Setting the Inflation Rates

While both types of bonds use the same inflation index and should provide similar inflation protection in the long run, the mechanism by which the inflation portion of the interest rate is set is different and can result in some interesting and difficult-to-understand shorter-term effects.

Penalties

A TIPS, like any other treasury bond, can be sold (and bought) on the open market at any time with minimal spreads, small commissions, and plenty of liquidity. I Bonds can only be sold back to the government, which won't buy them back at all for the first year and then will assess a penalty (the last three months of interest) for the next four years after that.

Deflation Protection

I Bonds generally have better deflation protection than TIPS. The I Bond composite rate never goes below zero. You will get back at least what you paid for them in nominal and inflation-adjusted returns (and likely something better). With a TIPS, as we have seen recently, they can have negative real interest rates and, in fact, the value of the bond can go back to par, i.e. what it was originally issued at. So, even if a 30-year TIPS had gone up in value for 25 years, if serious deflation hits, it could go right back to its original value.

Unique Tax Breaks

Each type of inflation-indexed bond offers some unique tax rates. You don't have to pay any taxes on an I Bond until you sell it. That tax deferral reduces tax drag. TIPS yields get taxed as they go, and you can actually be taxed on income you don't even receive (phantom income)! Remember how the value of the TIPS goes up with inflation? Yeah, that increase in value is not actually paid out to you until the TIPS is redeemed, but you do have to pay taxes on it. This is one reason why people often prefer to use TIPS funds/ETFs inside their tax-protected retirement accounts rather than buying individual TIPS at TreasuryDirect. Aside from the fact that the government-provided TreasuryDirect is run like a bad EMR with a difficult interface, random shutdowns, and frequent glitches. TreasuryDirect makes the IT and customer service issues at Vanguard look trivial by comparison.

To be fair, you can buy individual TIPS on the secondary market inside a self-directed retirement account, an IRA, or a 401(k) with a brokerage window. I bonds can never be bought inside a retirement account. So, if all of your investments are in retirement accounts, your decision between these two has already been made for you.

The returns on I Bonds (like EE Savings Bonds) can be tax-free, so long as they are used for education. Note that this benefit is completely phased out for high earners (MAGI > $100,800 [$158,650 MFJ]) in 2022).

The income from I Bonds and TIPS is state and local tax-free, just like any other bond issued by the federal government.

How to Get Around the $10,000 Limit with I Bonds

I mentioned earlier that perhaps the greatest downside of I Bonds is the fact that an individual can only buy $10,000 per year of them. Thus, people spend a lot of time and effort trying to get around that rule. And there are several workarounds. First, if you're married, you just go open an account in your spouse's name: Voila! You're up to $20,000. Next January is a new year, and you can buy another $10,000 a piece. In addition, you can buy $10,000 a year for all of your other entities. This includes LLCs, corporations, and trusts. We have some trusts, so we figure why not buy some I Bonds in them? In fact, some people open multiple revocable trusts just to buy more I Bonds. That seems like kind of a pain, as does opening an account for each of our businesses. But you could do it.

Another workaround is to buy some I Bonds for your minor kids in your accounts (and gift them later) or open accounts for them. Be aware of gift tax laws as you do this (Note: in 2023, you can gift $17,000 without it counting against the gift tax laws).

You can also buy I Bonds as gifts for others that are not your kids. Lots of people were doing this in 2022 when I Bond composite rates were 9.62%. While someone cannot get more than $10,000 per year total between what they purchase and what they receive as a gift, the gift can remain in the “gift box” at TreasuryDirect for years. People basically pre-purchased the next five or 10 years worth of I Bond purchases for their spouse all at once in 2022 so they could collect that sweet 9.62% yield for six months. The risk, of course, is that I bond composite rates could fall before you are allowed to redeem the I Bonds at one year or before you are allowed to redeem them without penalty at five years. In addition, if future I bond fixed rates are greater than 0%, you would miss out on some of that return.

Finally, you can actually buy another $5,000 per year of I Bonds with your tax refund. Be aware that the IRS screws this up a lot. Even if you're filing Married Filing Jointly, you're still limited to just $5,000.

How to Pass I Bonds to Heirs

As mentioned above, you can gift $10,000 worth of I Bonds per year to anyone you want, including your heirs. The recipient will also need a TreasuryDirect account, but once they have it, the transfer from your “Gift Box” to their account is relatively straightforward. But what happens if you die with I Bonds? Just like a life insurance policy or a retirement account, you can name a beneficiary (or survivor) to receive your savings bonds if you die. If no beneficiary is named, the value of the bonds goes into the estate. If you inherit paper savings bonds where you are named as the beneficiary, you have a number of options including:

- Do nothing (i.e., cash it in later)

- Cash in the bond

- Have the bonds reissued in your name

If you inherit a TreasuryDirect account, you're supposed to contact it for directions about what to do. You should have similar options, though. If you don't want to cash them in, expect to have to open a TreasuryDirect account yourself and have the savings bonds put in there. Note that inherited savings bonds do not get a step up in basis at death like many other investments.

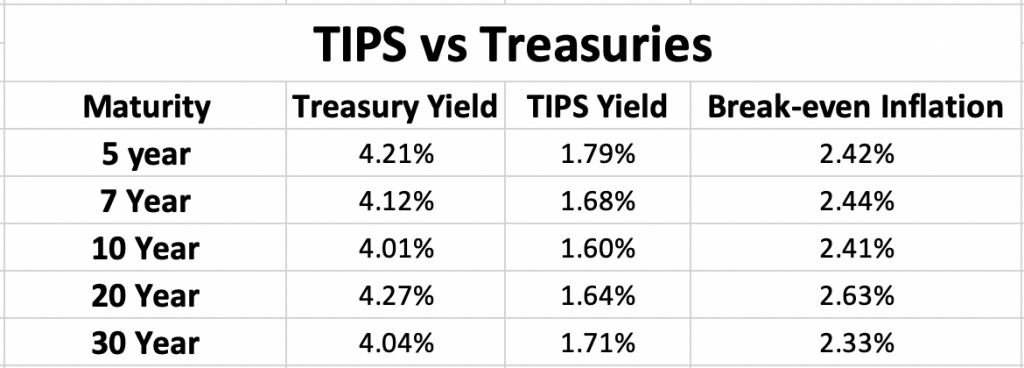

Using Treasury Bonds to Estimate Inflation

One can use the “yield curves” to determine what the market estimates inflation is going to be over any given time period (break-even inflation). Right now, this produces some pretty interesting data. Theoretically, the difference between the yield of a nominal treasury of a certain maturity and the real yield of a TIPS of the same maturity should provide an estimate of what the market expects inflation to be over that time period. For example, on October 18, 2022, the nominal yield of a five-year treasury was 4.21%, and the real yield of a five-year TIPS was 1.64%. So, the market expects inflation over the next five years to be 4.21% – 1.64% = 2.57%. Thus, if you think inflation is going to be greater than 2.57% over the next five years, you should preferentially buy TIPS instead of nominal treasuries. Here is a chart of this spread for bonds of various durations.

There are two other factors that affect this spread, but I suspect they are pretty small most of the time and they offset each other anyway. The first factor is a premium for taking inflation risk with a nominal treasury. Since the TIPS provides inflation protection in the event of unexpectedly high inflation, it should theoretically yield slightly less than you would expect from this calculation. That is to say that the TIPS provides insurance against unexpectedly high inflation.

However, the offsetting factor is that TIPS are less liquid than nominal treasuries, especially in really severe economic shocks. TIPS have wider bid-ask spreads and smaller lots. Normally, this liquidity premium is between 0.5%-1%, but it was as high as 3.25% in the 2008-2009 bear market.

Even if there wasn't a premium for taking on inflation with a nominal treasury, this calculation right now for a five-year TIPS still shows a break-even inflation rate of no more than 2.57% + 1% = 3.57%. Given that inflation is humming along at 8.2%, inflation would have to drop 4.63% before you would come out behind by buying a five-year TIPS instead of a five-year treasury. My crystal ball is cloudy as always, but that doesn't seem to be the worst bet in the world to take right now.

I Bonds and TIPS are inflation-indexed bonds that are a worthy addition to a portfolio. Which one to use depends on the accounts you are investing in, current rates, liquidity needs, and how much you need to invest. Most white coat investors who include this asset class in their portfolio are likely to eventually end up with some of both types of bonds.

What do you think? Do you own I Bonds, TIPS, both, or neither? Which do you see as more attractive right now? Do you expect to buy more I Bonds next year? Comment below!

The post I Bonds and TIPS: Which Inflation-Indexed Bond Should You Buy Now? appeared first on The White Coat Investor - Investing & Personal Finance for Doctors.

||

----------------------------

By: The White Coat Investor

Title: I Bonds and TIPS: Which Inflation-Indexed Bond Should You Buy Now?

Sourced From: www.whitecoatinvestor.com/i-bonds-and-tips/

Published Date: Mon, 07 Nov 2022 07:30:31 +0000

Read More

.png) InvestingStocksToolsClubsVideosPrivacy PolicyTerms And Conditions

InvestingStocksToolsClubsVideosPrivacy PolicyTerms And Conditions