I am bullish on Taiwan Semiconductor Manufacturing Company or TSMC (TSM). It is the world’s largest manufacturer of semiconductor products.

There is a prevailing shortage of chips because the factories of TSMC cannot keep up with the growing $47.2 billion per month semiconductor business.

This company’s stock is trading at 21.7% discount to its 52-week high of $142.19. (See Analysts’ Top Stocks on TipRanks)

Top Foundry Service Provider

Most fabless semiconductor firms like Advanced Micro Devices (AMD), Nvidia, (NVDA), Marvell (MRVL), and Broadcom (AVGO) are dependent on TSMC’s factories.

Even Intel (INTC) has hired TSMC to manufacture its upcoming discrete ARC Alchemist GPUs. Total foundry services revenue in 2020 was $85.1 billion and TSMC took 63% of that. Samsung, TSMC’s closest rival, only has 17% share of the foundry manufacturing industry.

The demand for semiconductor parts is so strong that foundry customers do not mind TSMC’s up-to-20% price hike on foundry manufacturing fees. This price increase will help finance the $100-billion three-year plan to expand manufacturing capacity.

No Threat from Intel and Samsung

GlobalFoundries and Intel still has no 5nm or 3nm process node manufacturing capability for the next two to three years. TSMC is already coming out with 3nm next year.

The 2nm production capability will launch by 2023. Intel’s $20-billion Fab52 and Fab62 chip factories in Arizona are just holes in the ground.

It will take around four to five years before they could be operational. The same thing could be said for Samsung’s future $17-billion Texas chip factory.

Without those new factories by Intel and Samsung, TSMC will remain as the go-to foundry service provider.

Affordable Valuation Ratios

The 10.9% three-month decline of TSMC’s stock has made it more affordable. Its forward P/E is only 25.4x, and its TTM Price/Sales is 10.1x. These ratios are much lower than Nvidia’s 49.3x and 23.4x.

This market bias is temporary., reflecting a geopolitical fear that China might invade Taiwan. TSMC is a Taiwan company with expanding factories in China. The success of Nvidia is partly thanks to the manufacturing prowess of TSMC.

Nvidia’s stock will lose its luster should TSMC relegate it to the low priority list for foundry services. Nvidia’s consumer and data center GPUs are mostly manufactured by TSMC.

The other remarkable traits of TSM are its 22.9% forward revenue growth rate, and its TTM net income margin of 38.2%.

Wall Street’s Take

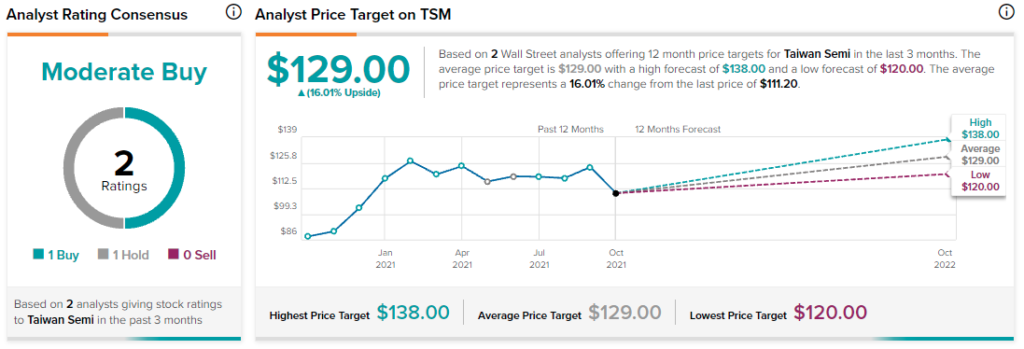

The consensus among Wall Street analysts is that TSM is a Moderate Buy, based on one Buy recommendation, and one Hold recommendation. The average TSMC price target is $129, implying 16% upside potential.

Conclusion

TSMC’s massive lead in semiconductor contract manufacturing fuels its high profitability, and double-digit revenue growth rate. It could be a worthy investment if you like the booming semiconductor industry.

Disclosure: At the time of publication, Motek Moyen did not have a position in any of the securities mentioned in this article.

Disclaimer: The information contained in this article represents the views and opinion of the writer only, and not the views or opinion of TipRanks or its affiliates, and should be considered for informational purposes only. TipRanks makes no warranties about the completeness, accuracy or reliability of such information. Nothing in this article should be taken as a recommendation or solicitation to purchase or sell securities. Nothing in the article constitutes legal, professional, investment and/or financial advice and/or takes into account the specific needs and/or requirements of an individual, nor does any information in the article constitute a comprehensive or complete statement of the matters or subject discussed therein. TipRanks and its affiliates disclaim all liability or responsibility with respect to the content of the article, and any action taken upon the information in the article is at your own and sole risk. The link to this article does not constitute an endorsement or recommendation by TipRanks or its affiliates. Past performance is not indicative of future results, prices or performance.

The post Why TSMC Stock Might Be Worth a Look appeared first on TipRanks Financial Blog.

----------------------------

By: Motek Moyen

Title: Why TSMC Stock Might Be Worth a Look

Sourced From: blog.tipranks.com/why-tsmc-stock-might-be-worth-a-look/

Published Date: Mon, 11 Oct 2021 16:07:47 +0000

Read More

Did you miss our previous article...

https://peaceofmindinvesting.com/investing/crowdstrike-finding-the-right-chords

.png) InvestingStocksToolsClubsVideosPrivacy PolicyTerms And Conditions

InvestingStocksToolsClubsVideosPrivacy PolicyTerms And Conditions