<iframe style="width:120px;height:240px;" marginwidth="0" marginheight="0" scrolling="no" frameborder="0" src="//ws-na.amazon-adsystem.com/widgets/q?ServiceVersion=20070822&OneJS=1&Operation=GetAdHtml&MarketPlace=US&source=ss&ref=as_ss_li_til&ad_type=product_link&tracking_id=peaceinvesting-20&language=en_US&marketplace=amazon®ion=US&placement=0060555661&asins=0060555661&linkId=80f8e3b229e4b6fdde8abb238ddd5f6e&show_border=true&link_opens_in_new_window=true"></iframe>|<iframe style="width:120px;height:240px;" marginwidth="0" marginheight="0" scrolling="no" frameborder="0" src="//ws-na.amazon-adsystem.com/widgets/q?ServiceVersion=20070822&OneJS=1&Operation=GetAdHtml&MarketPlace=US&source=ss&ref=as_ss_li_til&ad_type=product_link&tracking_id=peaceinvesting-20&language=en_US&marketplace=amazon®ion=US&placement=1119404509&asins=1119404509&linkId=0beba130446bb217ea2d9cfdcf3b846b&show_border=true&link_opens_in_new_window=true"></iframe>|<iframe style="width:120px;height:240px;" marginwidth="0" marginheight="0" scrolling="no" frameborder="0" src="//ws-na.amazon-adsystem.com/widgets/q?ServiceVersion=20070822&OneJS=1&Operation=GetAdHtml&MarketPlace=US&source=ss&ref=as_ss_li_til&ad_type=product_link&tracking_id=peaceinvesting-20&language=en_US&marketplace=amazon®ion=US&placement=1119376629&asins=1119376629&linkId=2f1e6ff64e783437104d091faaedfec7&show_border=true&link_opens_in_new_window=true"></iframe>

[Editor's Note: The IDR waiver deadline has been extended once again, and it's now set for June 30, 2024. This extension applies to borrowers with FFEL, HEAL, LDS, or Perkins Loans who are seeking loan forgiveness. To apply, you must consolidate your federal student loans by June 30, 2024. To learn more, see our guide on the IDR waiver.]

By Alaina Trivax, WCI Columnist

After more than three years of allocating all our extra money toward student loans, we quit making extra payments on my husband’s medical school loans in the fall of 2023. When Brandon, a PM&R doctor now working in private practice, was in residency, we just paid the minimums on his student loans—and while doing so, watched the interest rack up. We refinanced during his fellowship year to get a lower payment. Laurel Road, I think it was, offered us a “training rate” of $100 per month, which got us through that expensive final year of training. We refinanced again in 2022 and now have an interest rate of 2.05%, down from 4.2%.

He started as an associate partner in July 2020 and entered a full-time partnership contract in January 2024. We began our student loan payoff journey with a balance of over $330,000, and despite stopping those extra payments, we’re hopefully just a couple of months away from paying them off in full!

Our Goals

Paying off our student loans is listed as one of our top priorities in our financial plan, just below maxing out our retirement accounts and HSA/FSA options. When Brandon started as an attending, we used his expected salary numbers and calculated our other expenses, estimating that we could pay off the loans in about five years.

Believe me, we have plenty of other things we’d like to do with our money. We want to move to a bigger home with an acre or two of land; Brandon wants to upgrade his Jeep Compass to a full-size pickup truck; we want to get a side-by-side ATV to help us do farm chores at my mom’s property. And we want to travel more—though, that’s the one thing we’re not delaying as much. We have decided to prioritize that regardless of the student loan situation; we can always buy more things, but there will only be so much time to make memories.

We’re actually tracking ahead of our five-year payoff goal. The loans will be paid off by the of summer 2024, despite having stopped making extra payments this past fall.

More information here:

Are Student Loans the New Mortgage for My Generation?

Should You Pay Off Debt or Invest?

Why We Pivoted

For the first three years of Brandon’s time as an attending, we kept a detailed budget and totaled up any extra money each month to send as an additional student loan payment. The monthly amount varied slightly as our family grew (and childcare expenses increased!). Still, we nickel-and-dimed every line item to find extra money to pay down those student loans as quickly as possible.

Brandon approached me last summer and suggested we stop making these extra payments and send the money to a high-interest savings account instead. We had a whole sit-down meeting about this. I’m talking hired-a-babysitter-and-took-our-laptops-to-Panera meeting. Brandon had researched a few savings and money market accounts and came prepared to discuss how much we could earn in interest by doing this.

Our student loan interest rate is around 2%, while the money market account currently yields 4.4%. But please forgive the clickbaity headline. Technically, the funds are still allocated for student loan payoff. We’re just trying to make some extra money on them while accumulating the total payoff amount. The fact that got me on board: we could earn enough interest to reduce our repayment timeline by a month or two. That’s compelling.

I Don’t Really Like It

Honestly, I am not the biggest fan of the plan. I don’t like that we’re not sending this money directly to the loans. It seems like we’re overcomplicating the process. The money market account is separate from our regular checking account; after I close out our monthly budget and tell Brandon how much extra money is available for student loans, he sets up a bank-to-bank transfer. I suppose it’s not much more work than setting up an additional payment to the student loan provider (and it is not one of my financial duties in our family anyway, so I guess it’s not my problem). It just seems like another account to manage and more opportunity for complications.

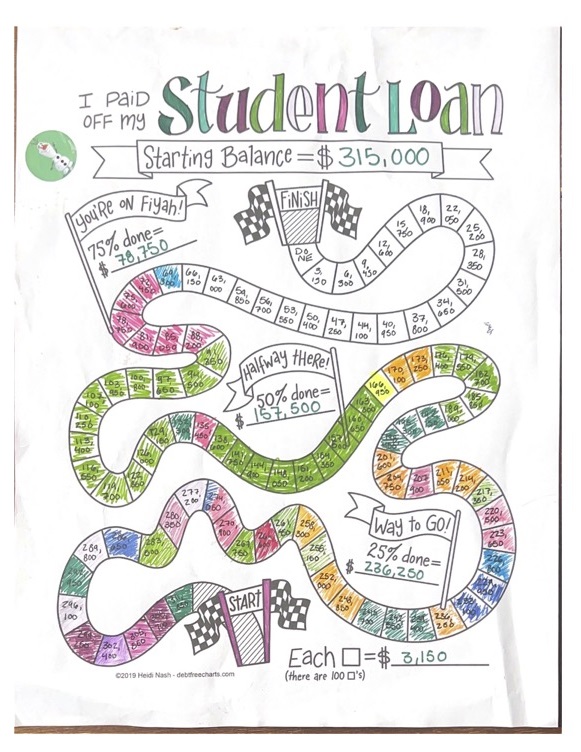

We have a chart on our fridge where we cross off student loan payments as they are completed. It’s set up as a game board with 100 squares, each equaling $3,150. I was not pleased the first time Brandon crossed off some squares to account for cash that we had set aside in that money market account and allocated for student loans. No payment had been made yet! In my mind, the money doesn’t “count” as a student loan payment (and should not be crossed off the chart) until it’s been used to actually PAY the student loan!

This is what hangs on our refrigerator.

Coloring in a chart on our fridge like it's a game obviously isn’t the important thing here; rather, I worry that having the funds on hand makes it too easy to use the money for other purposes. We talked a little about this when we first established the plan, and we already have had a few instances of needing to use the money. Brandon’s practice is pursuing a real estate investment for the company and he can buy in as a partner; we’re using some of the money we had set aside for student loans to join that real estate venture. We now have a specific amount in that account earmarked for that purpose.

We’ve also had to exercise some discipline to avoid viewing the account as a sort of slush fund for unexpected purchases and expenses. After Brandon’s first year as an attending, we miscalculated our tax bill and had to take out an advance on his bonus. Since then, we’ve worked closely with our accountant to ensure our withholdings are correct. But we’re still a little scared. The backup plan for this coming year is to use some of the funds from that account if needed. We’re also prioritizing travel with our family—taking a family trip to Mexico this winter and then planning a few beach trips with extended family for next summer. We are setting aside a little money for these and expect to cash flow the balance of these trips. We do have a separate emergency fund for the more day-to-day emergencies and big expenses—appliance repairs and replacement, unexpected vet bills, etc. Still, we are getting pretty comfortable knowing that extra money is there “just in case” we need it for these trips or for emergency expenses.

I’m not sure I like that.

That account is earning a good deal of interest, though—enough to shorten our student loan payoff timeline by a few months. That fact is really the only reason I’m willing to stick with this plan. We are ready to be done with these loans. With the money in that account, an upcoming bonus, and our regular monthly payments, we can probably pay them off by July 2024.

More information here:

What Happens When You Actually Have to Use Your Emergency Fund?

With Our Expanding Family, We’ve Had to Break Our Financial Plan – Twice

A Good Excercise in Disagreement

Brandon and I are usually on the same page regarding financial management, so this has been a new experience to navigate. I can only think of one other issue where we couldn't get on the same page: establishing sinking funds for recurring household expenses.

During his training and early attending years—when our budget was tighter—I would save a little money each month for expected but infrequent household expenses. Things like annual insurance policy renewals, household appliance repairs, and upcoming vacations—expenses that we knew were coming and we knew would be more than a few hundred dollars at once. For example, cash-flowing our $450 umbrella insurance policy renewal wasn’t feasible during his fellowship year. We needed to be saving for that in advance. And if the dryer needed repairs that same month? We’d have been air-drying our clothes for a little while.

I never could get Brandon to understand the rationale of this savings strategy. I’m not sure if it’s his background coming into play—the first time he ever experienced significant financial scarcity was his fellowship year, so the idea of not having enough money to pay the bills isn’t something he thinks about often. Now that he is more established in his career and we have greater financial flexibility, these sinking funds aren’t as necessary. We really can cash flow most of these unexpected or recurring household expenses.

We’ve learned that it’s OK to disagree with each other about financial matters as long as our family’s overall financial health isn’t being harmed. As far as our choice to quit paying extra on our student loans and send the money to a savings account instead, we’ll stick with that plan for now. Using the money as a cash account for something other than our student loans, the real estate opportunity, or a tax bill will be a major red flag to reassess.

And When They’re Gone . . .

Once those student loans are gone, we’ll convert the account into a savings account for a down payment on a house or property. We’ve looked at a few pieces of land in the past few months—we’re not quite ready financially but want to see what’s out there. I’m sure buying a new home (or building one!) will bring at least one new disagreement for us to explore.

Either way, we won’t have to play this student loan game ever again.

Is it the right move to not pay extra on the student loans and instead send those funds to our savings account? What other strategies could you use? Comment below!

The post We Quit Paying Extra on Our Student Loans (and Why It Feels Dangerous) appeared first on The White Coat Investor - Investing & Personal Finance for Doctors.

||

----------------------------

By: Josh Katzowitz

Title: We Quit Paying Extra on Our Student Loans (and Why It Feels Dangerous)

Sourced From: www.whitecoatinvestor.com/we-quit-paying-extra-on-our-student-loans/

Published Date: Fri, 24 May 2024 06:30:32 +0000

Read More

Did you miss our previous article...

https://peaceofmindinvesting.com/investing/what-is-the-best-degree

.png) InvestingStocksToolsClubsVideosPrivacy PolicyTerms And Conditions

InvestingStocksToolsClubsVideosPrivacy PolicyTerms And Conditions