<iframe style="width:120px;height:240px;" marginwidth="0" marginheight="0" scrolling="no" frameborder="0" src="//ws-na.amazon-adsystem.com/widgets/q?ServiceVersion=20070822&OneJS=1&Operation=GetAdHtml&MarketPlace=US&source=ss&ref=as_ss_li_til&ad_type=product_link&tracking_id=peaceinvesting-20&language=en_US&marketplace=amazon®ion=US&placement=0060555661&asins=0060555661&linkId=80f8e3b229e4b6fdde8abb238ddd5f6e&show_border=true&link_opens_in_new_window=true"></iframe>|<iframe style="width:120px;height:240px;" marginwidth="0" marginheight="0" scrolling="no" frameborder="0" src="//ws-na.amazon-adsystem.com/widgets/q?ServiceVersion=20070822&OneJS=1&Operation=GetAdHtml&MarketPlace=US&source=ss&ref=as_ss_li_til&ad_type=product_link&tracking_id=peaceinvesting-20&language=en_US&marketplace=amazon®ion=US&placement=1119404509&asins=1119404509&linkId=0beba130446bb217ea2d9cfdcf3b846b&show_border=true&link_opens_in_new_window=true"></iframe>|<iframe style="width:120px;height:240px;" marginwidth="0" marginheight="0" scrolling="no" frameborder="0" src="//ws-na.amazon-adsystem.com/widgets/q?ServiceVersion=20070822&OneJS=1&Operation=GetAdHtml&MarketPlace=US&source=ss&ref=as_ss_li_til&ad_type=product_link&tracking_id=peaceinvesting-20&language=en_US&marketplace=amazon®ion=US&placement=1119376629&asins=1119376629&linkId=2f1e6ff64e783437104d091faaedfec7&show_border=true&link_opens_in_new_window=true"></iframe>

By Josh Katzowitz, WCI Content Director

Money mistakes can affect you at any time in your investing career. Naturally, most white coat investors (and most investors, in general) will make bad decisions when they’re first getting financially literate. Dr. Jim Dahle made snafus when buying his first house and when he invested in loaded mutual funds early in his career.

In one of my first newspaper jobs, I took way too long to enroll in my company’s 401(k) and didn’t receive thousands in matching dollars, and WCI columnist Rikki Racela still bemoans the fact he lost tens of thousands of dollars on a whole life insurance policy sold him to by a salesman who he thought was a friend.

Even if you’ve become a smart(er) investor as you move into your mid- or late-career, you can still inflict painful wounds on your portfolio. Some would say I shouldn’t have bought a Tesla. Some might regret sending their kids to private school. Others might never start a Roth IRA, while others might pay high fees for terrible financial advice.

At WCICON23 last February, I corralled a number of attendees and asked them about their biggest money mistakes. Hopefully, you can either empathize with or learn from their financial boo-boos. I’ve kept them all anonymous so they could speak freely and be as honest as possible. Hopefully, their blunders can do all of us a little bit of good going forward.

Biggest Money Mistakes

OK, what was your biggest money mistake?

- “Before I went to medical school, I was an engineer. I worked at a coveted job and made a coveted salary (“Oh my God, you’re making $45,000 a year!”). I socked away the minimum for retirement. In 1995, I could have maxed it out, and it would have been worth so much money today. I put in the minimum just so I could get a match—the 3% of my salary or whatever it was. If I had been smart, I would have saved more than 25%. It might be worth as much as $500,000 today.”

- “Sending my kids to private school. It’s a money suck. It’s all post-tax, disposable income that you could do something else with. We’d have been retired now if we hadn’t sent our kids to private school. It’s not worth it. Maybe we should have moved to a neighborhood with a good school.”

- “Allowing Fidelity to send me the full payment of my non-governmental 457. I had asked for it over a period of five years, but they sent me the whole thing. When you’re making irrevocable decisions, you have to make sure it’s right. So, I had to take it all in one tax year, and it cost me about $14,000. Just be freaking careful with irrevocable decisions.”

- “Paying off debt too quickly. We have no debt now. We had a lot of debt with very low interest. I’m OK with it, but if I had known, I would have held onto the mortgage for a little longer. It’s a calculated decision, obviously. We probably would have bought real estate when it was a good deal. I should have leveraged the debt a little bit better.”

- “I bought a property that ended up having an environmental issue that was not disclosed, resulting in a year-and-a-half of litigation and lawsuits and hundreds of thousands of dollars of potential losses. It resolved OK for me, but it ended up with about a year-and-a-half of headaches. I trusted the real estate broker, but I didn’t verify anything. He told us there were no issues. But there were. I trusted but I didn’t verify.”

- “Starting too late with paying off student loans. We really didn’t figure out that we should be doing more than the minimum until about two years ago. My husband has been out of residency for seven years. We had the means to pay more. We just didn’t do it.”

- “Now that I’m getting long-term disability, I got cheap on the premiums, and I didn’t carry as much disability coverage as I could have or should have. In order to save $500 a year on premiums, I’m now not collecting $3,000 a month until I’m 65. I knew enough that I should have carried more, but I didn’t want to. The recommended ratio of coverage to income, I knew I was under that. If I had followed the doctrine, I would have increased it from $7,000 per month to $10,000. Writing that [premium] check for $2,800 instead of $2,100, it just hurt. It was the hubris of youth.”

- “I focused too much on my finances too early. I could have gone to Europe in my early 20s, but I was more focused on my Roth IRA.”

- “Not starting a Roth IRA when I was in college in 2008 and not earning a lot of money. I had four jobs: bartending, waiting tables, working in a research lab, and teaching for Kaplan. I probably could have maxed it out in those years. I was making a good bit of money, and I was on scholarship. It would have been easier to pay off some of those medical student loans. My parents said don’t worry about investing and that everything will work out.”

- “Going into medicine. It was a decade-and-a-half worth of training to make low six figures income. If you put that same amount of time or energy into another field—if I had gotten my certification for investment grade security, that’s a much more lucrative field—I could have made more money. Thinking about the cost-benefit with risk, it would have made much more sense to pursue something like that.”

More information here:

Should Doctors Be Organizing and Striking for Better Pay and Work Conditions?

Top 10 Financial Mistakes for New Attendings

What to Do After Making a Financial Mistake

You can’t let your mistakes define you and continue to weigh you down financially and emotionally. As Jim has written, you have to admit the miscue, minimize the damage, stop making the mistake, and then let it go.

As he previously wrote:

“The water is under the bridge and the milk is already spilled. If you let your financial mistakes paralyze you, you are likely to make more of them.”

There’s also this: a high income makes up for plenty of mistakes.

So, take it from Bram Stoker (who once said, “We learn from failure, not from success”) and Tallulah Bankhead (“If I had to live my life again, I’d make the same mistakes, only sooner”). You, too, could make all kinds of mistakes in your life and still go on to find the success of a Gothic horror writer or a 1930s movie star (or whatever the financial equivalents of those are).

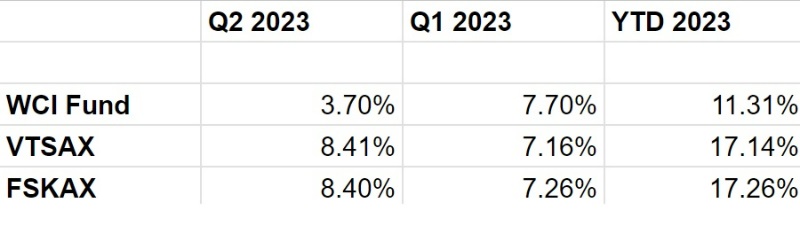

The WCI Fund 2023 Q2 Update

Remember how high we were riding after Q1 when the WCI Fund (the quasi-index (and completely made up) fund composed of the individual stocks picked by WCICON23 attendees) had beaten the performances of VTSAX and FSKAX? Yeah, that didn’t quite happen in Q2. In track and field parlance, we were like the rabbit/pace-setter for the first lap of the mile run. We ran a great first 400 meters, but we trailed off a little bit in the second lap. Now, everybody else has caught up to and surpassed us.

But it’s OK, because we’re still up on the year. Here's how WCIF compares to VTSAX and FSKAX.

Solid, but not as spectacular as we would have hoped. The S&P 500 dominated in the first half of 2023 with a 14% rise, and the NASDAQ had its best-ever first half of the year with a gargantuan gain of nearly 40%. Meanwhile, WCIF did fine in Q2, but we failed to keep pace with the two most popular total stock market index funds to which we are comparing ourselves.

As a reminder, here’s what’s inside WCIF.

- The Walt Disney Company (DIS)

- International Business Machines Corp. (IBM)

- New York Times Company (NYT)

- General Electric Company (GE)

- Lululemon Athletica Inc. (LULU)

- Masimo Corporation (MASI)

- Dick’s Sporting Goods Inc. (DKS)

- Target Corporation (TGT)

- Vail Resorts Inc. (MTN)

- Adverum Biotechnologies Inc. (ADVM)

- The Coca-Cola Company (KO)

- Moody’s Corporation (MCO)

- National Storage Affiliates Trust (NSA)

- Walmart Inc. (WMT)

- McKesson Corp (MCK)

- Paramount Global (PARA)

- Palantir Technologies (PLTR)

- Roblox Corporation (RBLX)

- Chewy, Inc. (CHWY):

- Peloton Interactive, Inc. (PTON)

Though artificial intelligence has given a boost to Palantir (which nearly doubled its price from Q1 to Q2) and the New York Times grew its digital subscriptions by hundreds of thousands of people, Disney and Target got pummeled. I’m not sure if that’s the result of the political culture wars that both have had to fight this year, but either way, both companies are some of our lowest performers of Q2.

That’s a little discouraging. Overall, though, we’re feeling good about WCIF—even if not everybody loves this version of the Stock Game.

Tweet of the Week

This is always a good reminder.

What were your biggest money mistakes? Can you relate to any of the mistakes made by our WCICON panel? Comment below!

[Editor's Note: For comments, complaints, suggestions, or plaudits, email Josh Katzowitz at [email protected].]

The post Your Biggest Money Mistakes appeared first on The White Coat Investor - Investing & Personal Finance for Doctors.

||

----------------------------

By: Josh Katzowitz

Title: Your Biggest Money Mistakes

Sourced From: www.whitecoatinvestor.com/your-biggest-money-mistakes/

Published Date: Sun, 30 Jul 2023 06:30:38 +0000

Read More

.png) InvestingStocksToolsClubsVideosPrivacy PolicyTerms And Conditions

InvestingStocksToolsClubsVideosPrivacy PolicyTerms And Conditions