<iframe style="width:120px;height:240px;" marginwidth="0" marginheight="0" scrolling="no" frameborder="0" src="//ws-na.amazon-adsystem.com/widgets/q?ServiceVersion=20070822&OneJS=1&Operation=GetAdHtml&MarketPlace=US&source=ss&ref=as_ss_li_til&ad_type=product_link&tracking_id=peaceinvesting-20&language=en_US&marketplace=amazon®ion=US&placement=0060555661&asins=0060555661&linkId=80f8e3b229e4b6fdde8abb238ddd5f6e&show_border=true&link_opens_in_new_window=true"></iframe>|<iframe style="width:120px;height:240px;" marginwidth="0" marginheight="0" scrolling="no" frameborder="0" src="//ws-na.amazon-adsystem.com/widgets/q?ServiceVersion=20070822&OneJS=1&Operation=GetAdHtml&MarketPlace=US&source=ss&ref=as_ss_li_til&ad_type=product_link&tracking_id=peaceinvesting-20&language=en_US&marketplace=amazon®ion=US&placement=1119404509&asins=1119404509&linkId=0beba130446bb217ea2d9cfdcf3b846b&show_border=true&link_opens_in_new_window=true"></iframe>|<iframe style="width:120px;height:240px;" marginwidth="0" marginheight="0" scrolling="no" frameborder="0" src="//ws-na.amazon-adsystem.com/widgets/q?ServiceVersion=20070822&OneJS=1&Operation=GetAdHtml&MarketPlace=US&source=ss&ref=as_ss_li_til&ad_type=product_link&tracking_id=peaceinvesting-20&language=en_US&marketplace=amazon®ion=US&placement=1119376629&asins=1119376629&linkId=2f1e6ff64e783437104d091faaedfec7&show_border=true&link_opens_in_new_window=true"></iframe>

By Dr. Jim Dahle, WCI Founder

The Florida home insurance market has been a huge mess in 2022 and 2023. It's a real crisis. The cause is that insurance companies there are hemorrhaging money, over $1 billion a year for two consecutive years. It seems Florida is somewhat unique among the states in this regard. Not only do they have hurricanes, which damage many homes all at the same time, but there is a claims problem and, especially, a litigation problem. Florida accounts for 9% of homeowner's claims. That's a lot considering it only accounts for 6.6% of the US population. But amazingly, Florida accounts for 79% of home insurance lawsuits, many of which are fraudulent. That litigation costs the insurance companies a lot—in payouts and defense costs.

It's like a scam industry. Here's how it works, according to Bankrate:

-

- First, roofers canvas neighborhoods and offer inspections to unsuspecting homeowners. These contractors inevitably “find damage” on the roof and often promise a “free roof” to the homeowner, claiming they can have the home insurance deductible waived.

- Homeowners are pressured to sign an assignment of benefits form, giving contractors the right to file an insurance claim on their behalf.

- A claims adjuster from the insurance company inspects the alleged damage. The adjuster either finds no damage or far more minimal damage than the contractor found, and the claim payout is less than what the contractor demanded.

- The contractor brings legal action against the insurance company, demanding a claim payout for the contractor’s original quote. Remember, the homeowner signed the benefits of the policy to the contractor, so the contractor doesn’t need the homeowner’s permission to do this.

- The insurance company now has a choice: it can pay the legal costs to fight the lawsuit or pay the costs to settle out of court. Either way, the insurance company loses money due to the legal action.

As a result of the crisis, six insurance companies in Florida liquidated between 2017 and 2021, and there were five more in the process in 2022. Other companies simply left the state. Others are not renewing policies in large parts of Florida, raising prices, or tightening eligibility requirements.

Florida government officials are well aware of this problem and are trying to solve it. They passed new bills in July 2021, May 2022, and December 2022. The first was meant to reduce the number of fraudulent claims. The second set up the My Safe Florida Home program (which provides grants to make homes less likely to be damaged), prevented insurance companies from being able to deny coverage just because a home has an older roof, and limited how much attorneys could charge on property claim cases. The third law got rid of “one-way attorney fees” and assignment of benefit forms. Despite these changes, getting insurance is still a huge challenge.

The crisis means lots of people in Florida can't get homeowner's insurance at all. This also happens in other states, although in a more contained way. California fires have been causing some companies to quit writing policies there, as well.

What are your options if you are one of these people living in one of these states?

More information here:

How Much Homeowners Insurance Do I Need?

An Unsung Benefit of Insurance

My Emergency Fund in Action

#1 Sell the Home

You can always just sell the home. You can buy another home in an area that may be insurable. You could leave the area and buy a home. You could rent instead. Lots of options. The real downside here is that selling an uninsurable home probably limits your number of buyers and the price you can get for it.

#2 Go Bare

Some people choose not to have homeowner's insurance. That seems like a terrible idea unless you can afford to self-insure. That means lots of wealth and a relatively inexpensive home. If it burns to the ground or it's leveled by a hurricane, you lose. But otherwise, you actually come out ahead financially, especially if the alternative is to fire-sale the house at a ridiculously low price. However, if your home has a mortgage, this probably isn't really an option for you. Most mortgage companies require your home to be insured.

#3 Make Your House Insurable

Maybe your house is uninsurable because it has a terribly old roof or is in some other way exposed to more risk. Maybe you can replace the roof, and it will then be insurable. Or put in a sump pump. Or install hurricane straps or other roof-bracing measures. Maybe get rid of big trees overhanging your house. Or do some other modification that will now make the home insurable.

#4 Shop Harder

Maybe you just haven't called enough insurance companies. Try harder. Call more. Until you have called all of them, you don't really know you can't get insurance.

#5 Use a Broker

You can save time and can even be more likely to get coverage if you use a professional. An insurance broker will know the market much better than you, and they may qualify you for coverage that you can't get yourself. They can often find enough savings to more than make up for their cost.

#6 Call Citizens

Apparently, Citizens Property Insurance Corporation is the “only game in town” in many parts of the state. The nonprofit company has been taking over for other companies in large parts of Florida. Note that Citizens requires flood insurance with its policies.

#7 Call Tailrow

There's a new company writing business in the state called Tailrow. Call them, too.

#8 Check for Other Causes of Uninsurability

Moving away from the Florida-specific situation, consider other causes of not being insurable. These are generally broken down into the following categories:

- Occupancy issues

- Business use

- Structure

- Location

- Past claims

- Miscellaneous

Let's break down these issues a little more.

Occupancy Issues

Insurance companies don't like unoccupied homes. Even a second home can be tough to insure. Get someone in the house, and it might be easier to insure it.

Business Use

Insurance companies like homes that are just used by regular old homeowners eating dinner, sleeping, and watching TV. They don't like you running a business out of your home. An incidental business may be fine, but if you're making more than $10,000 or so, it could cause insurance problems. Same thing if you're running a ranch or farm. Those barns can be expensive to replace. Daycare introduces additional risk, and nobody wants to insure a frat house. Airbnb'ing your home or running a bed and breakfast can also cause issues with getting homeowner's insurance. However, one option to get insured is to just quit doing whatever it is you're doing—at least at that location. You can also look for specific farm or short-term rental policies.

Structure

The structure of your home could also cause insurability issues. Older homes have worn-out electrical features that might not be up to code, and they are more likely to burn down. Trampolines, pools, and other “attractive nuisances” can also increase the price of your insurance or make you uninsurable. Weird houses (tiny homes, DIY homes, domes, etc.) and historically important houses can also cause insurance issues. If your house is under construction, under renovation, or being remodeled, that can be an issue. Houses on stilts and wood-burning stoves are also problematic. Basically, before buying or building a home, make sure you can actually get it insured.

Location

If first responders can't find or get to your home easily, that could be a problem. Just being further from a fire station increases your costs. If the area is at high risk for forest fires or floods, you could be uninsurable. Landfills, steep hillsides, commercial neighborhoods, and mobile homes where you do not own the lot can also cause uninsurability problems. Check for insurance before buying.

Past Claims

If you're putting in a homeowner's claim every year for five years, don't be surprised when you can no longer get insurance. Better to get a higher deductible, self-insure a bit, and make fewer claims if possible. One is fine. Two is bad luck. Three in a short period of time is a problem client or a problem house.

Miscellaneous

Dogs, tigers, and snakes can all cause insurability problems. You can also be the problem, especially if you have a history of fraud, foreclosure, or arson. A bad neighborhood or an obvious lack of maintenance on your home can also be an issue. Find somewhere else to house your exotic pets, maintain your house, and encourage your neighbors to do the same.

#9 Ask Your Neighbors

They're probably insured by somebody. Call their company.

#10 Ask Why You're Being Denied

If every company is giving you the same story, see if you can fix the issue.

#11 Call the Consumer Division of the State Department of Insurance

This could get you help quickly, but if not, at least it'll be aware of the problem so maybe you'll only be uninsured for a few months or years.

#12 Ask for a ‘High-Risk' Policy

A high-risk policy obviously is going to cost more, but at least you can get it. It may be a completely different department at the insurance company, just like there is a different department for luxury homes (as many doctors buying doctor homes have discovered). These can also be called “surplus lines policies,” although that is typically used with separate insurance companies (often in Great Britain) so try both terms when asking about them. Surplus lines policies are not as subject to state oversight as regular policies.

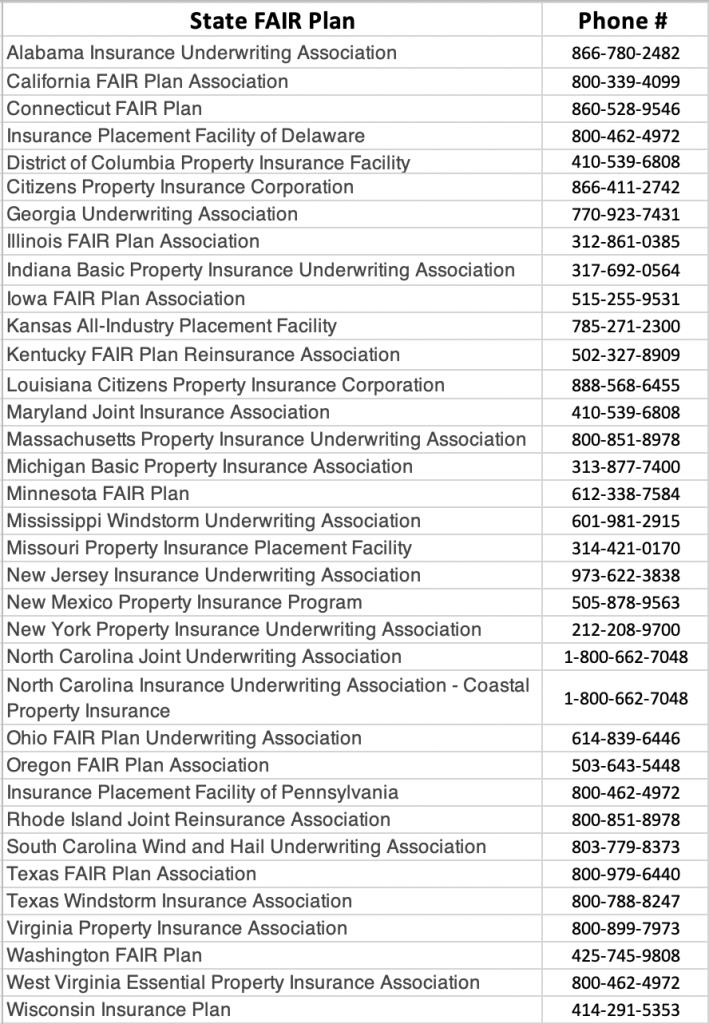

#13 Look into FAIR Plans

Thirty states, plus Washington DC, have Fair Access to Insurance Requirement (FAIR) plans in place. Unsurprisingly, Florida does not (but California does). They are bare-bones policies, but they're better than nothing. It is a state-mandated policy provided by multiple insurance companies (a shared market plan) on the same home. It may only cover fire, vandalism, wind, and riot risks, but it varies by state. They often do NOT include personal liability, an important consideration. Here are the names and phone numbers of the various programs. If the number doesn't work, try Google.

Homeowner's insurance is one of the policies we absolutely recommend here at WCI (along with disability insurance, term life insurance, health insurance, and liability insurance). However, you may have to work extra hard to get this coverage, especially in Florida or California.

What do you think? Have you had your policy denied or not renewed? What did you do? Comment below!

The post What Happens If You Can’t Get Homeowner’s Insurance in Your State? appeared first on The White Coat Investor - Investing & Personal Finance for Doctors.

||

----------------------------

By: The White Coat Investor

Title: What Happens If You Can’t Get Homeowner’s Insurance in Your State?

Sourced From: www.whitecoatinvestor.com/what-happens-if-you-cant-get-homeowners-insurance/

Published Date: Mon, 07 Aug 2023 06:30:11 +0000

Read More

.png) InvestingStocksToolsClubsVideosPrivacy PolicyTerms And Conditions

InvestingStocksToolsClubsVideosPrivacy PolicyTerms And Conditions