<iframe style="width:120px;height:240px;" marginwidth="0" marginheight="0" scrolling="no" frameborder="0" src="//ws-na.amazon-adsystem.com/widgets/q?ServiceVersion=20070822&OneJS=1&Operation=GetAdHtml&MarketPlace=US&source=ss&ref=as_ss_li_til&ad_type=product_link&tracking_id=peaceinvesting-20&language=en_US&marketplace=amazon®ion=US&placement=0060555661&asins=0060555661&linkId=80f8e3b229e4b6fdde8abb238ddd5f6e&show_border=true&link_opens_in_new_window=true"></iframe>|<iframe style="width:120px;height:240px;" marginwidth="0" marginheight="0" scrolling="no" frameborder="0" src="//ws-na.amazon-adsystem.com/widgets/q?ServiceVersion=20070822&OneJS=1&Operation=GetAdHtml&MarketPlace=US&source=ss&ref=as_ss_li_til&ad_type=product_link&tracking_id=peaceinvesting-20&language=en_US&marketplace=amazon®ion=US&placement=1119404509&asins=1119404509&linkId=0beba130446bb217ea2d9cfdcf3b846b&show_border=true&link_opens_in_new_window=true"></iframe>|<iframe style="width:120px;height:240px;" marginwidth="0" marginheight="0" scrolling="no" frameborder="0" src="//ws-na.amazon-adsystem.com/widgets/q?ServiceVersion=20070822&OneJS=1&Operation=GetAdHtml&MarketPlace=US&source=ss&ref=as_ss_li_til&ad_type=product_link&tracking_id=peaceinvesting-20&language=en_US&marketplace=amazon®ion=US&placement=1119376629&asins=1119376629&linkId=2f1e6ff64e783437104d091faaedfec7&show_border=true&link_opens_in_new_window=true"></iframe>

[Editor's Note: Due to an overwhelming volume of WCI Scholarship applications, we’re coming to you with an urgent request: We need more scholarship judges! If you are a working or retired professional (no students or residents) and would be willing to read and rank a number of 1,000-word essays in a timely manner in September, send an email to [email protected] with “Volunteer Judge” in the subject line. Become a scholarship judge today and help WCI invest in the doctors of tomorrow!]

By Dr. Tyler Scott, WCI Columnist

When content director Josh Katzowitz approached me on a pickleball court last December to be a columnist here at WCI, I was excited and confused. My excitement stemmed from being a fan of the site for over 12 years, and my confusion was concerning what I could possibly write about.

He said he wanted more dental voices on the blog, and he thought my career transition was interesting—as was my ongoing disability insurance journey. Furthermore, one of the perspectives he thought I would bring to the blog is that of a “moderate earner.” He and I agreed that the blog can occasionally tilt toward the very high-earning demographic that Dr. Jim Dahle inhabits (which is both understandable and legitimate), and Josh and Jim want to make sure the blog is also consistently speaking to those of us who will likely never have $250,000 to invest in a private equity real estate fund.

Now, before making you read through the entire post to find out what my wife, Megan, and I make as “moderate earners,” let’s get that out of the way early. Our combined 2023 income will likely be just under $300,000.

The notion that $300,000 is a “moderate income” is ludicrous by any reasonable standard. Based on recent data from the Economic Policy Institute from 2020, our income puts us in the top 8%-10% of earners in 2023 when adjusted for inflation. It is only in the context of this readership that such numbers could possibly be considered moderate.

According to the most recent US Census data, the median household income in 2021 was $70,784, and in a recent Gallup poll, Americans said they believe that a family of four needs $85,000 of annual income to “get by.”

Three years ago, Megan was working for no monetary compensation as a stay-at-home-do-everything-domestic-volunteer, and I did not yet have a disability claim. Our household income then was $203,000. All that income came from my work at a public health dental clinic. Our spending was similar at that time, and so, the primary difference now is the increase in our savings rate.

Whether you're a pediatrician, a plastic surgeon, or anywhere in between, we can agree that whether our income then or now is moderate—even in the context of this blog—is highly debatable. Though that debate may be worthwhile, it’s not the purpose of this post.

Our Salaries as Moderate Earners

I have two objectives for putting our personal cash flow out into the world:

1) I’d like to see our culture normalize talking about money: Americans are famously uncomfortable talking about money, and that is often to our detriment. While we occasionally offer up casual reference points regarding our personal finances to our friends/family in the abstract (i.e., “that restaurant is a little pricey for us” or “we have to pass on that vacation; it’s out of our budget right now”), we rarely put specific dollar amounts into the arena for discussion. Specificity seems to bring out the most unpleasant of human emotions in some of us: shame, guilt, resentment, jealousy, fear, and judgment. But that need not be. Being transparent about our salary, how much we paid for our house, or how much the kids’ private school costs can put our financial life into perspective and help us know if we are getting a reasonable deal. Consider this post my first attempt to “be the change I want to see.”

2) I just want people to be happy: After doing financial planning full-time for over a year now, primarily for readers of this blog, I have learned that basically everyone feels the same. Whether they make $120,000 or $1.5 million, almost everyone feels like things are going pretty much OK and they wish they had a little more money to do or buy a few extra things or retire a few years earlier. There is a ubiquitous sense of “near happiness” with a chaser of scarcity that I hope we can all shake over time. Happiness is ultimately a choice we make, not a math equation we solve. Let’s make that choice sooner rather than later.

With that context and those objectives in mind, let’s first look at our household income, estimated taxes, big-picture spending projections, and expected savings rate for 2023.

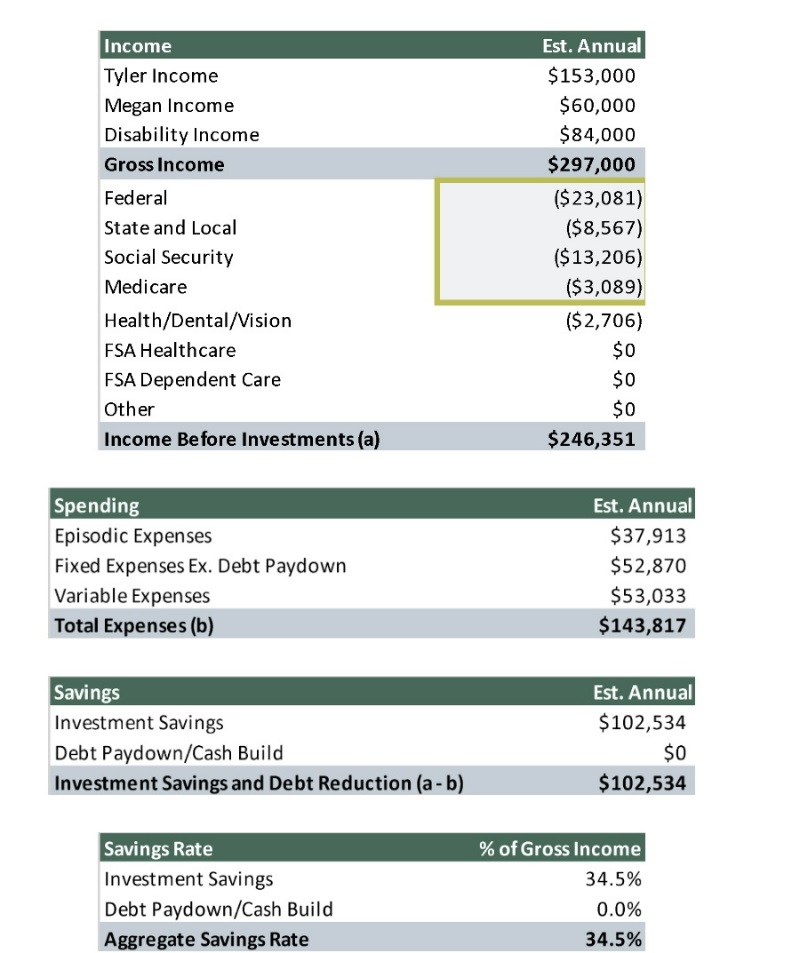

Here you see our various sources of income. While my pay is variable based on how many clients I serve in a given year, I expect to make ~$150,000 in 2023. Add in ~$3,000 for the few columns I write for WCI and a little work I do to help Andrew Paulson at StudentLoanAdvice.com (all you Kaiser docs in California that are suddenly eligible for PSLF are keeping SLA very busy right now), and, in total, I expect my income to be about $153,000 this year.

Megan’s salary as the WCI podcast producer is more predictable, though for reasons I’ll discuss later, her paychecks are $139 per month.

If you read my most recent column about how structural lower back problems and dentistry don’t play well together, you’ll know that I also receive $7,000 per month from my own occupation long-term disability insurance policy. If I hadn’t been cheap and short-sighted with my Future Benefit Increase rider, this amount could have been much higher. At the same time, we are very grateful for what we do receive.

This disability income is tax-free, which is why a savvy reader may have noted that our tax burden is remarkably low for our income level. For those who are interested, our effective tax rate is 21.5% and our marginal tax rate is 27%. More on how that impacts our retirement savings decisions in a moment.

Not included here is compensation that our culture sometimes forgets to consider but is worth pointing out. WCI pays for 80% of our medical insurance premiums ($13,530) and gives Megan a $6,500 match in her 401(k). I also receive a 4% match (~$6,000) and a $100 per month work-from-home stipend. Not to mention the FICA taxes paid on our behalf by our employers or the value of when Jim and Katie Dahle take the WCI employees on a team-building trip and the WCI conferences.

Overall, our 34.5% savings rate is respectable and puts us on pace to be “work optional” around age 60.

More information here:

The Moderate-Income Physician

How We're Spending Our Salaries

Now, let’s look at how we sliced up our $297,000 in 2023.

Deciding how to prioritize cash flow can be a difficult decision for families of any income. Finding the balance between eliminating debt, saving for retirement, and living a joyful life in the present is a challenging and dynamic process for many.

We have four stops on our cash flow train that help us determine how to slice up our income:

- Pay ourselves first.

- Save for future expenses.

- Pay the bills.

- Spend the rest.

#1 Pay Yourself First

By first making sure we are saving enough to retire at the age we want and doing that through automated contributions to various accounts, we protect ourselves from overspending and make the most of what economists have won Nobel Prizes for discovering regarding behavioral economics. In short, automate savings wherever possible and make incremental increases over time.

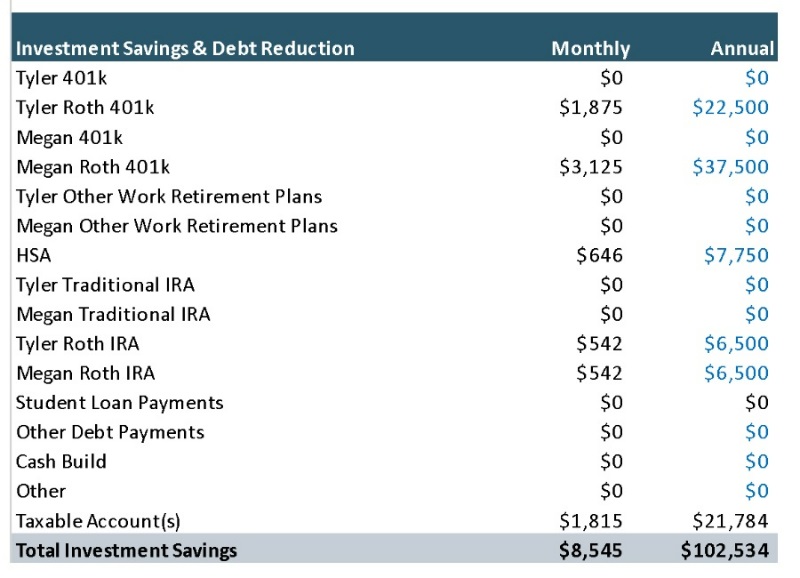

You will note that Megan and I both make Roth contributions to our 401(k). This goes against the smart and well-established rule of thumb consistently proffered by Jim to “make pre-tax 401(k) contributions in your peak earnings years.” Because of our unusual situation with my tax-free disability income, we are in the 22% federal tax bracket and feel that is a reasonable price to pay in exchange for not owing tax on that money or its growth ever again.

Also, because the disability income does not count toward AGI, we stay below the $218,000 income limit in 2023 (in 2024, the income limit will be $230,000), and we can make direct Roth IRA contributions each month rather than saving up throughout the year for a one-time Backdoor Roth IRA contribution.

You will also notice that Megan contributes an amount well above the IRS employee contribution limit of $22,500 for 2023 ($23,000 for 2024). Is this because Jim is so impressed with her podcast-producing skills that he made her a partner in WCI and so she gets to make employer contributions as well? No, but it is because WCI offers the world’s best 401(k). The WCI 401(k) allows employees to redirect a portion of their take-home salary to their 401(k) each year. By the time Megan contributes the annual family maximum to her HSA, pays for her portion of our family’s health insurance, redirects the allowable amount to her 401(k), and pays her portion of payroll taxes, she ends up with a take-home pay of $139 per month. I love this and the efficiency it represents; she loves it slightly less.

Finally, you will observe that paying off student loans or other high-interest debt counts as paying yourself first. Having $110,000 of my $280,000 dental school debt paid for by the NHSC (National Health Service Corp) loan repayment program was a critical step to wealth-building as a moderate earner.

#2 Save for Future Expenses

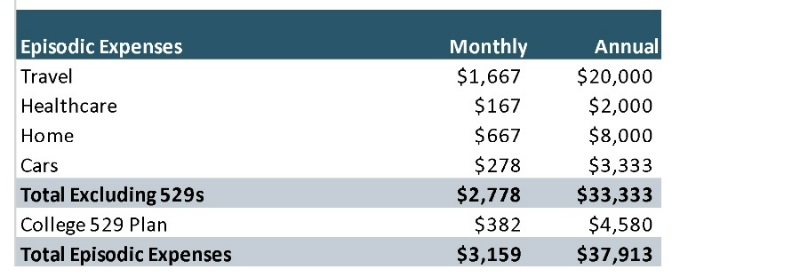

Next, we save for expenses that we know will happen, but we don’t know when they will occur. For example, we know we will need to replace our cars, our home will need updating and repairs, we will go on vacations, we will have out-of-pocket healthcare expenses, and our kids will (probably) go to college.

To prepare for these episodic expenses, we set up what a mentor of mine calls “squirrel funds” where we squirrel away a little bit of cash every month into our high yield savings account. Our HYSA has different buckets within the account that we deposit specific dollar amounts to every month via automatic transfer from our checking account. We also think of our monthly contributions to the kids’ 529s as a type of squirrel fund.

You may be wondering how we pick the amounts to squirrel away each month.

For travel, we pick an amount that is some combination of currently true and reasonably aspirational. We have three young kids so traveling too often or too far is hard right now. We live in a state with five national parks and where an $80 America the Beautiful annual pass goes a long way, but we also try to mix in some expensive Hawaii and Disneyland trips throughout the years. Megan and I hope to travel much more in the coming years as the kids get older and now that she and I can almost always work from anywhere. We don’t spend $20,000 every year but squirrel funds “roll over” year to year and give us a guiding light for an average annual spending target.

For out-of-pocket healthcare expenses, we pick the amount of our HSA per person deductible. Again, some years we use less, and some years we use more. But this is a decent rubric for our healthy family.

For home-related costs, we save between 1%-1.5% of the value of our home each year. This is meant to cover big repairs (our water heaters and entire HVAC system recently went out), upgrades (we all get sick of the carpet or color of the cabinets eventually), and sizeable furnishings (think of buying a new $11,000 sectional sofa). Obviously, this doesn’t get used every year, but when I got a bid for $46,000 last week to replace our water heaters and HVAC, I was glad I had my squirrel fund.

For cars, we take the number of vehicles in the family, the number of years we intend to keep each car, and the expected cost to replace those cars to come up with an annual savings target. We have two cars, plan to keep them for 15 years, and plan to spend $25,000 to replace them (we have a very utilitarian view on cars). That math produces a monthly savings target of $278.

For college, we contribute up to our state’s allowable tax deduction each year. This projects to cover about one-third of the future costs for our state university. Helping our kids with college costs is a goal for us but not one we are willing to compromise our retirement goals for. There are many ways to pay for college, and 529s are just a part of our family plan. We expect our kids to cover the other two-thirds from their own savings, their own cash flow, scholarships, financial aid, and/or loans. Future grandparent contributions are also likely though not assured.

Other possible squirrel funds that I’ve seen be useful for clients include future Backdoor Roth IRA contributions, annual disability insurance premiums (often you get a discount if you pay annually instead of monthly), weddings, big/expensive cultural celebrations (i.e., Bar/Bat Mitzvahs and quinceañeras), and a down payment for a future home.

The way squirrel funds work mechanically is that we pay for the expense on our credit card to get the 2% cash back, then we “reimburse ourselves” from the squirrel fund to our checking account, and then we pay the credit card bill from the checking account. Then, the squirrel fund begins to fill up again because of our automated contributions.

Having these squirrel funds allows us to automate our financial life and to be reasonably assured that any future expense will not disrupt our normal monthly cash flow.

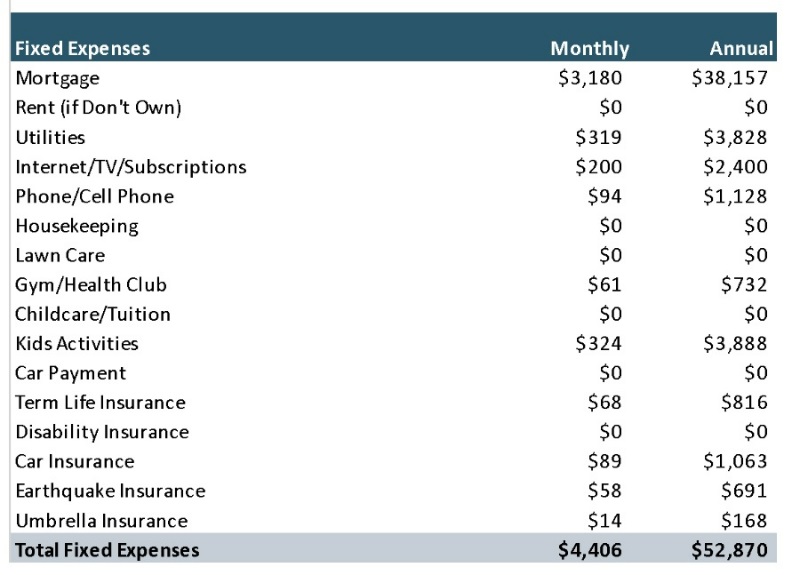

#3 Pay Your Bills

Next, we pay the bills, aka our fixed expenses. We put as many of these on autopay as possible (currently all of them). We use a credit card for any bills that don’t charge a fee for using a card.

We have a 15-year mortgage. There is proliferous debate online and over water coolers about whether a 15- or 30-year mortgage is optimal. I understand the arguments for the 30-year as it relates to inflation-adjusted, tax-adjusted, time value of money, etc. calculations. However, for us, knowing that we will save over $100,000 in interest over the life of the loan and increase our monthly cash flow substantially in half the time is compelling. The mortgage payment you see above includes taxes and insurance.

Ultimately, we aimed to keep our total housing costs (principal, interest, property taxes, utilities, repairs) at less than 20% of our annual gross income on a 15-year mortgage. This is not possible in all areas of the country—especially with today’s interest rates—and yet, I think it’s a worthy goal for the moderate-earning demographic.

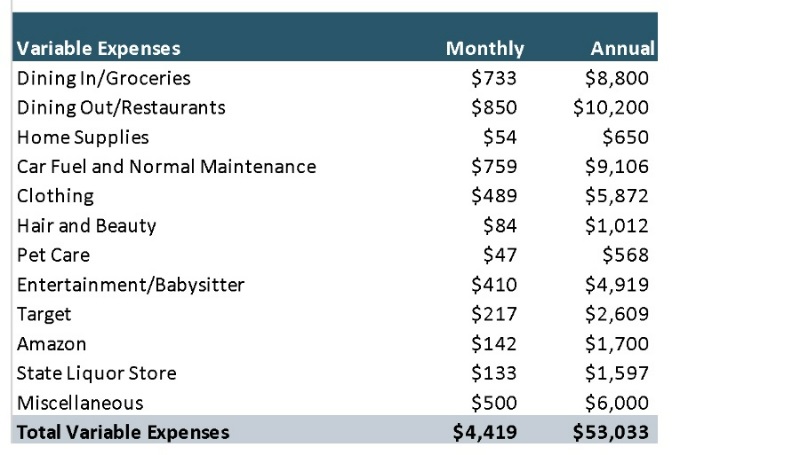

#4 Spend the Rest

Finally, we spend the rest. These are our variable or discretionary expenses. We update these numbers each year based on a rolling three-year look back. We use online software to track our expenses and that’s where we get our data.

We used to have a monthly meeting where we would review this data to ensure we were fairly close to our targets. Now that we have established spending habits based around these numbers, we review our spending annually. If we get more than 5% beyond our target, we identify why we believe that area has increased and make adjustments to our budget or to our behavior as needed.

That’s it. That’s how much we made and where we allocated it.

We find tremendous value in spending time each year to account for every dollar and to give every dollar a job. This level of organization and intention helps us feel in control of our finances, and feeling in control of our money is the only consistent thing we’ve noticed that brings us happiness as it relates to money.

Further, having this four-piece cash flow prioritization system in place creates a joyful relationship with our spending. At first, it may feel like a bummer to have spending come last in your financial plan. However, when we follow this system, whatever is earmarked to be spent is spent freely and without regret. This is because we know that everything else upstream has been taken care of already. We believe we will retire at the age we want. We are saving for future expenses. All the bills are paid. Now, spend the rest joyfully!

Most people have that gremlin who sits on our shoulder telling us we should not order the appetizer at dinner, we shouldn’t buy those cute shoes in the store window, or we shouldn’t enter a winner-take-all fantasy football league. Almost all of us went through many years of austerity in training and then several more years living like a resident to pay off our student loans. That gremlin played an important role, but, in time, we can get to a place where we thank him for his service and take our leave of his scarcity-minded hauntings. Having this kind of cash flow system operational in our lives helps make that possible.

It is worth noting that American culture goes exactly the opposite direction with their cash flow train. They buy whatever they want, try to pay their bills on time, and stick $100 under their mattress in case something “goes wrong.” And an alarmingly small number of people save adequately for retirement if they even save at all. As of 2022, the median retirement savings for those 55-64 was $89,714!

It is therefore no surprise why we have so much anxiety around money in our country. Prioritization is largely backward, and there is a dearth of organization and a paucity of intention. Then, we wonder why we are so stressed.

As a self-identified WCI moderate earner, I’m here to say I believe it is possible for nearly all “six-figure professionals” to feel wealthy, abundant, and joyful as it relates to their income. Let’s talk about it more, let’s celebrate our riches, and let’s choose happiness whenever and wherever we find it.

More information here:

A Dental Career Reimagined — I Thought I’d Be Rich But I Found Wealth in Another Way

The Bottom Line

Possible takeaways for moderate earners from this attempt at financial transparency:

- A great deal of attention needs to be paid to the “three big rocks.” Those three big rocks are housing, cars, and education. We made sure we could afford a home on a 15-year mortgage. We prioritize the maintenance and longevity of our cars (I drive a 1997 Camry, Megan drives a 2008 Acura; both have 240,000+ miles). We had someone else pay for a big chunk of my student loans. We send our kids to public school, and we intend to pay for one-third of their public university costs.

- Lifestyle creep and recurring costs can be sources of insidious erosion of wealth-building over time at more modest income levels. We mow our own lawn, shovel our own snow, clean our own house, and go to a cheap gym. We are thoughtful about which activities we enroll our children in (my sister-in-law pays $25,000 per year per daughter for dance class here in Utah; that’s not sustainable for us).

- Tracking spending may be more important compared to our high-earning peers. Jim often says something to the effect that “a high income erases a lot of spending mistakes.” A moderate earner can benefit greatly from keeping some kind of monitoring in place for monthly or annual spending.

- Roth 401(k) contributions may make sense in some cases. Marital status, state of residence, the capricious political environment, risk tolerance, and many other factors go into this decision. It’s worth taking a close look at it, depending on which federal tax bracket you are in currently.

- While it’s true that even a blind squirrel finds a nut once in a while, don’t be blindsided by unpredictable expenses. Set up squirrel funds and you don’t have to rely on luck.

- Pickleball creates jobs. Go to the court and see what good fortune awaits you.

Need to get your own financial plan in place? Check out the Fire Your Financial Advisor course! It's a step-by-step guide to creating your own path to financial freedom. Try it risk-free today!

If you're a moderate-income earner, what do you think about this example of earning, saving, and spending? Would you approach your finances in a different way? Comment below!

The post Here’s How Much We Make, Save, and Spend as ‘Moderate Earners’ appeared first on The White Coat Investor - Investing & Personal Finance for Doctors.

||

----------------------------

By: Josh Katzowitz

Title: Here’s How Much We Make, Save, and Spend as ‘Moderate Earners’

Sourced From: www.whitecoatinvestor.com/moderate-income-physician-cash-flow/

Published Date: Fri, 08 Sep 2023 06:30:43 +0000

Read More

.png) InvestingStocksToolsClubsVideosPrivacy PolicyTerms And Conditions

InvestingStocksToolsClubsVideosPrivacy PolicyTerms And Conditions