||

Hi to all English speaking investors. I want to start this 4th edition by apologizing to you twice: First for taking a 2 months long break between newsletters and second for making you wait for the English translation. Please get in touch with me so that I know if there is real demand for the English version or not – please also consider supporting me on Patreon as that is the ultimate form of letting me know – you’re here and need this service. Now on to some personal news: I reached a sort of financial independence, quit my job as of 1 of January 2021, travelled to beautiful Costa Rica for one month and am now enjoying my new jobs: As a father and husband. 8 years ago when I first read about the Financial Independence and Early Retirement movement I couldn’t have known that this could be us too. Our story with extra income from Airbnb-ing a part of our house, small investments and our salaries – is very typical in the FIRE community 🎉. I may return to work, but I’m not in a rush.

Second of all, in the last 2 months, inside the original Investment Club (6 members) we analyzed and discussed hundreds of hours of podcasts, videos, PDFs and annual reports. We spend so much time learning that our brains are fried every single day. This means that this issue of the Newsletter will be filled with links to external content – podcasts, videos and annual reports that I highly encourage you to read. Otherwise you’re just going to have to take my word that what I say is true. My patreon supporters also get more frequent updates any time I change my portfolio (Like the recent sale of 10% of my TSLA shares while it was at all time highs). All Patreon income is going towards improving the investment advice I give in this newsletter and I cannot wait for the next improvement. I hope you will notice it in the next newsletters.

So what will the 4th issue of the Newsletter be about?

- I will explain why as I previously wrote in the 2nd and 3rd issues, Bitcoin keeps going up and why it’s heading towards 100.000$-600.000$ per Bitcoin. Why Tesla purchased 1.5Billion USD worth of Bitcoin and why banks are now rushing in.

- For those that already purchased Bitcoin I will explain how to earn 6% interest on their Bitcoin and how this is paying for half of my mortgage now.

- The discovery that you can make 8.6% interest on the cash that you have in your bank accounts, why the risks are small and how to do it.

- We will look at the recent stock market correction and the triggers that led to it.

- And last but not least – going back to our original format – talk about Tesla, Berkshire and Square and their financial results for 2020 as well as Warren Buffet’s juicy annual letter to investors.

So why does Bitcoin keep appreciating in US dollar terms?

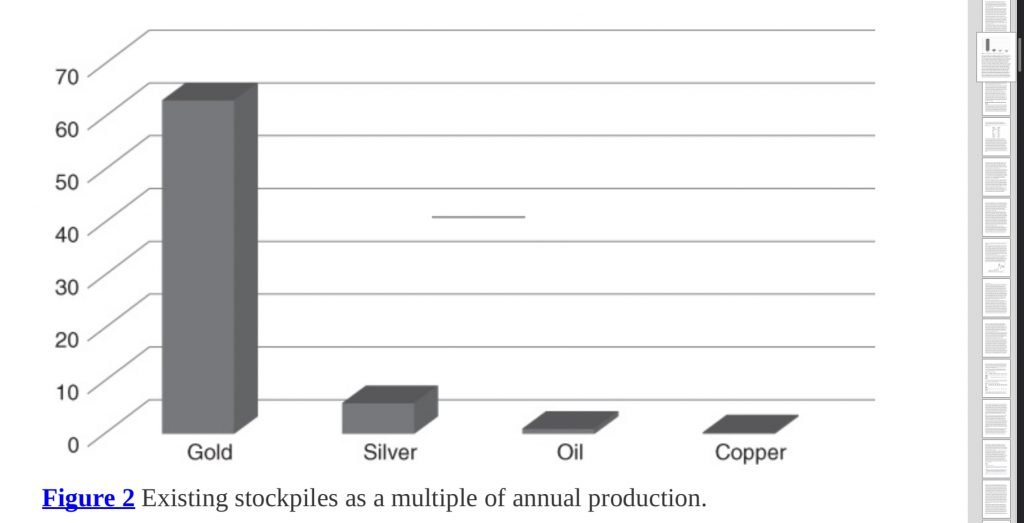

There are many explanations but if we go back to the basics – The Bitcoin Standard book by Saifedean Ammous will explain a lot. In it, the author goes through every form of money humanity ever used. From rocks and shells which didn’t hold value well because they were easy to replicate to copper and silver coins. Even silver didn’t last and didn’t do a great job as money. That’s because Silver could be easily mined – having a total stock at the earth’s surface of only 6 times larger than the yearly mined silver. Below – a small chart from the book with different commodities and their Stock to Flow:

Gold at a 60 StockToFlow, Silver at 6, Oil and Cooper at 1

What this chart tells us is that Silver has a stock to flow of 6 or in other words, that miners can extract 1/6 more silver every year or that it would take them 6 years to double the total extracted silver above ground. Cooper has a stock to flow of 1 so storing your wealth in Cooper is a really poor idea as miners can flood the market with more cooper. Gold has a very high stock to flow of 60. This means it would take gold miners 60 years to double the gold we have above ground. Or that the gold stock grows very slowly, 1.6% every year and it takes 60 years to double in quantity because gold is very difficult to mine. This is what makes gold a good store of value – governments can’t print it and miners can’t flood the market with it – being hard to extract. Gold had a high stock to flow throughout history and to this day continues to serve as a store of wealth.

This also means that every time a country tried to use Cooper or Silver as money (Even the US tried to monetize silver in the 19th century), the miners would not wait long and start flooding the market with the easy-to-mine metal. This would mean they could devalue the money used by a country with a cheap metal. In the case of African tribes using glass beads as money , European colonialists figured out they counterfeit their money and used it to enslave and steal the riches of the tribes. Now that we understand why having hard money (high stock to flow) is important we are ready to look at what this tells us about the price of Bitcoin:

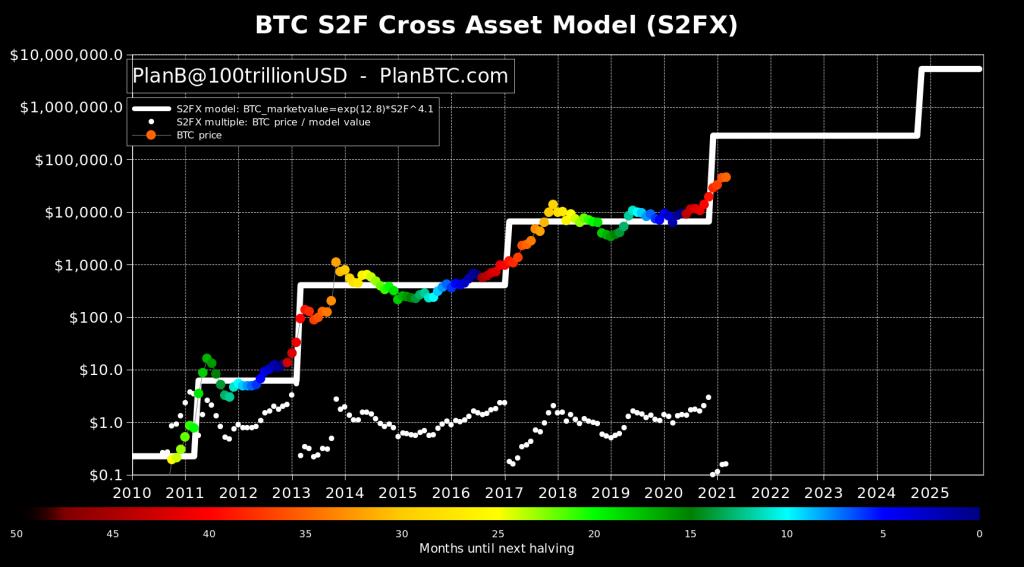

If you remember, in the 3rd issue I was writing that I finally discovered a valuation model for Bitcoin, one that isn’t – the price will go up. The model said that you can look at Bitcoin through a couple of it’s uses and estimate it’s value: It might be a bubble (0$/Bitcoin), It might be a niche currency (10.000$/Bitcoin), it may be a replacement of gold(100.000$-600.000$/Bitcoin just to rival gold’s market cap) and it may end up being the world’s reserve currency (Above 10.000.000$/Bitcoin). I liked this theory as it finally provided some anchor points. However at the same time, a Dutch gentleman, who had been working in the banking industry for 25 years had published another valuation model for Bitcoin 18 months earlier, called the Stock-To-Flow model. This man going by the name of PlanB@100TrillionUSD made an important discovery: By charting the scarcity of Bitcoin which gets halved every 4 years, he modeled the price of Bitcoin:

Stock to flow model created by PlanB. With every halving Bitcoin price increases 10x

This chart shows us how the price of a Bitcoin since 2009 onward is completely tied and explained by its scarcity – how much bitcoin miners get as a reward. Here’s a easier to read version of this same chart: Take note that the chart explains the price of bitcoin since 2009 virtually perfectly:

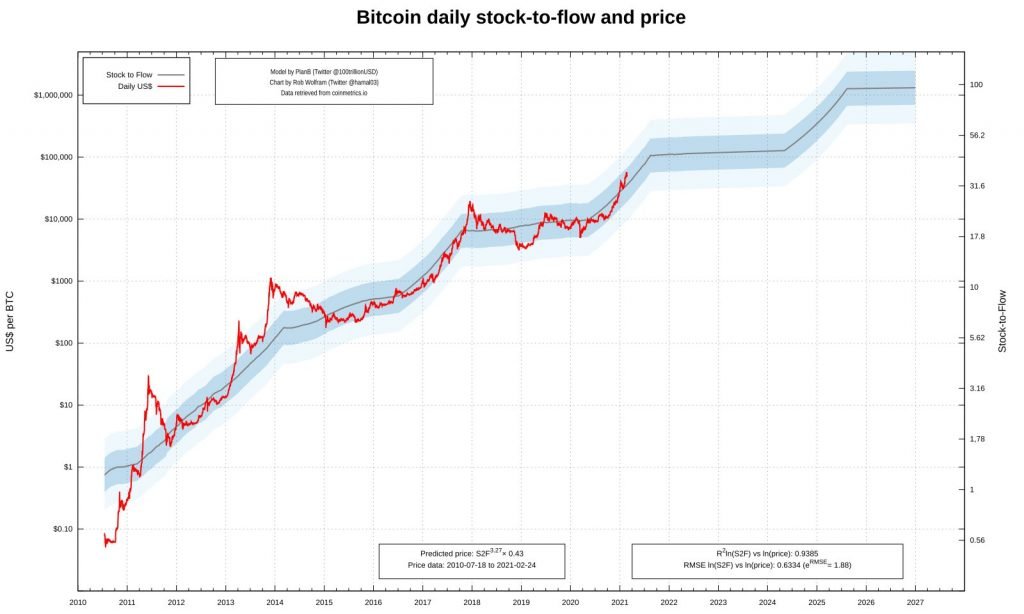

Another chart showing that Bitcoin 10x’s every 4 years

PlanB goes on to explain in this excellent interview that the first time he saw this chart he though he had made a mistake. Could it really be true that the only thing the price of Bitcoin depends on is its scarcity? PlanB goes on in that interview to predict many things that are quite frankly mind bending: That Bitcoin will reach 288.000$ in this cycle (2020-2024), that it will rival the market capitalization of gold and that after the next halving (2024) at a stock to flow of almost 100, the price will go up to several million dollars per Bitcoin. His model is so accurate that it could have been applied before Bitcoin was created, say in 2005, and it would have predicted the price in the last 12 years exactly. Mind blowing as I said. You can listen to PlanB in different interviews on YouTube as well as Spotify, to understand how serious and scientific his approach is and the growing community of researchers who are now studying his model to understand why it is so accurate.

I spilled enough ink over this topic – the conclusion is clear: both PlanB’s model and the simple theory that Bitcoin will act as a gold replacement leads us to a price of anywhere between 100.000$ and 600.000$ per Bitcoin in this cycle(2020-2024) and a couple million dollars per Bitcoin in the 2025-2029 cycle. Of course it wont be a straight line up, as it goes from euphoria to despair. It’s no wonder then that my favorite macro-economist, Lyn Alden, keeps on writing about Bitcoin and debunking myths and educating people both on this topic as well as the dollar devaluation we’ve been experiencing for the past century that is currently pushing people into Bitcoin. The 25$ a month I pay for my premium subscription to Lyn’s content has multiplied 480 times 🙂

Other than that, Tesla has converted 1.5Billion USD of their existing 20 Billion cash pile into Bitcoin after Elon teased us multiple times on Twitter, peaking with his now famous tweet, “In retrospect, it was inevitable”. The reason for this move? Protecting their cash from devaluation. Tesla is now up 70% on this investment alone. Michael Saylor encouraged Elon Musk to do this after his own company, Microstrategy, converted all of its cash to bitcoin. This triggered an avalanche of companies converting their cash and Michael Saylor has become a sort of a hero of the Bitcoin community after organizing an event for 7000 companies to teach them how to do the same for their treasury. Tesla & SpaceX attended this event too – which meant it was fairly obvious what they were about to do. Michael Saylor, however, did not stop here. He issued an additional 1 Billion dollars of debt at 0% interest rates (meaning the debt holders get no interest) – just to buy more Bitcoin. If this sounds like he is exploiting the low interest rates and pushing it all into Bitcoin which is the antidote for low interest rates and money printing – it is because he is. Some people call it a “speculative attack on the US dollar”. I just call it common sense. Just listen to Michael talk and you will understand he knows what he is talking about. ARK invest is estimating that the price per Bitcoin could go to 80.000$ if only 1% of the cash of all S&P500 companies is converted to Bitcoin. In other words, the printing of US dollars has led to inevitable abandonment of the currency by it’s citizens and this is starting to catch the eye of those who favor money printing yet are not willing to accept that this does more damage than good. Here is the US treasury secretary’s FUD, Janet Yellen. Inside the US central banks there must be heated discussion about what can be done to discourage the release valve that Bitcoin is – certainly banning it is too late as it’s legal in multiple US States now.

Ok, How do I make 6% interest from my Bitcoin holdings?

I discovered the platform that I’m going to describe below in the autumn of 2020. I had a bit of Bitcoin already and kept hearing about this platform on the Investors Podcast – my favorite value investing podcast. The idea of the platform being that you deposit your Bitcoin into their interest account and they pay you 6% for it (yearly) and an up to 250$ sign up bonus. You can withdraw your Bitcoin at any time. So how are they able to offer 6% in a super low interest rate world?

The way they achieve it is by lending your Bitcoin to institutional borrowers who use it like so:

- Arbitrage – selling your bitcoin and instantly buying it somewhere else cheaper.

- They use it for liquidity purposes – for example their own clients withdrawing Bitcoin and they don’t want to sell their holdings.

- Other trading strategies that require borrowing and returning Bitcoin quickly thereafter.

- Other similar strategies

I would later find out from the same BlockFi Interview on The Investors Podcast that institutional investors need this service from BlockFI because traditional banks don’t offer it – and that’s how the platform was born. Why institutional investors? Because although they borrow Bitcoin they deposit an even larger amount as collateral – Overcollaterization. Now on to the risks – your deposit is not insured like a typical bank account, but BlockFi is monitored and regulated by different US government agencies, has a good reputation and works, among others with Gemini – which is one of most reputable players in this space. Sure a paranoid investor could assume they don’t really lend your Bitcoin to institutional investors, maybe they don’t require enough collateral and maybe they even bribe their regulator. All highly unlikely – but there are some risks that are not paranoid that we can and will talk about in a few paragraphs.

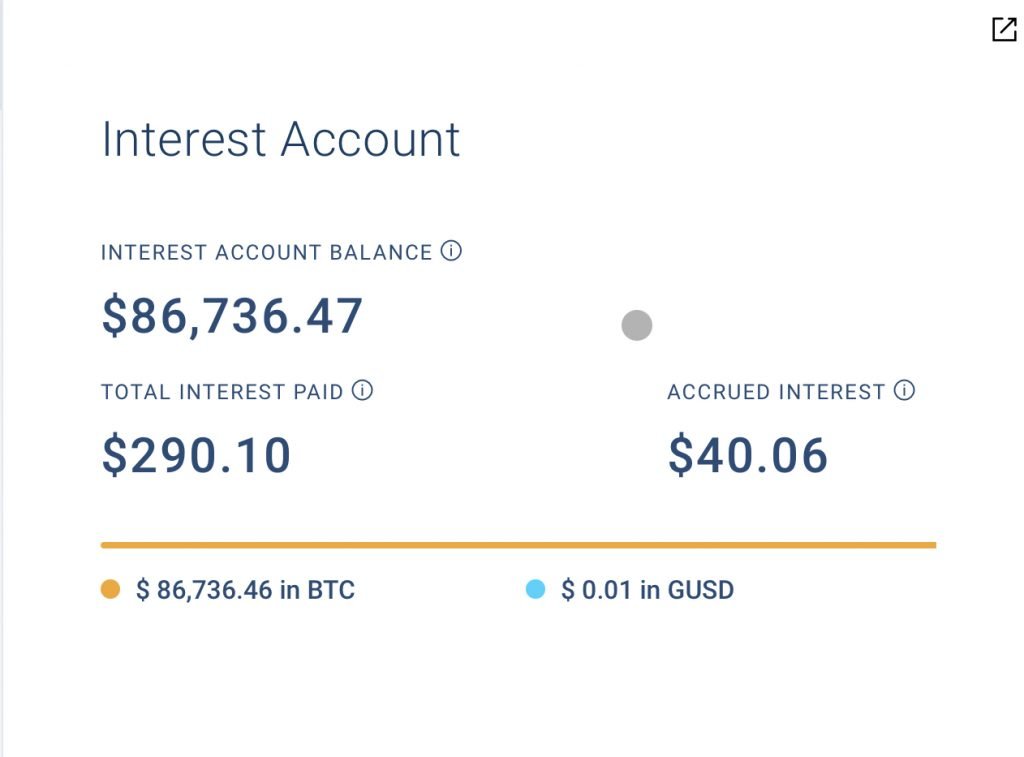

I started by depositing a small portion of my Bitcoin at 6% interest just to test the platform and once I received my first interest payment and ensured I can withdraw my Bitcoin:

First monthly interest payment from BlockFi

In my head there was a light bulb moment. If I can deposit 10.000$ and make 50$ a month in interest (enough to pay for Spotify, Netflix and one Phone subscription), I wonder how much could I make if I deposited a significant amount (but still not more than half) of my Bitcoin here. Here it is after I gained confidence:

Deposited a total of 1.8 BTC into BlockFI

At 1.8 BTC deposited into BlockFi means that at 6% interest I make at current market prices, 450$ a month or 0.009BTC. That’s enough to pay for half of my mortgage payment. And if I dont sell it it appreciates in value as Bitcoin goes up in price. That’s quite a feat. To quote one of the investors in the original investment club: “If I had purchased 3 Bitcoins for 10.000$ in March of 2020, I would have 150.000$ now and receive interest of 1000$ monthly. That would mean I could just retire?”. Yes, pretty much. But it gets better. Because you can actually make 8.6% interest on your cash without being exposed to Bitcoin’s volatility. How? Good that you asked:

How do I make 8.6% interest on the cash I have?

As I started to use BlockFi more and more I discovered they offer interest not just on Bitcoin but other crypto currencies and Stablecoins. Now stablecoins are an interesting variety of crypto-currencies. What makes them stable is that their value is pegged 1-1 with the US dollar. One of them is GUSD, the Gemini US Dollar. For every GUSD created on the blockchain there is 1 US dollar in their bank reserves. It’s stable because it’s price doesn’t fluctuate and equals one dollar. The advantage? You can send someone dollars across the globe without a 3 day settlement period like traditional banks require. BlockFI offers 8.6% interest on GUSD deposits and I found this out from Preston Pysh – one of the hosts over at The Investors Podcast and a very competent investor and educator in this space:

In other words what Preston is saying on twitter is that you can convert your US Dollars or Euros to GUSD (backed 1-1 with real dollars) and deposit that at 8.6% interest, a couple hundred times more than your traditional bank account offers. However I was upset because it turns out you can’t buy Gemini Dollars from Europe or Switzerland – so I couldn’t simply convert my cash to GUSD. It took a while but I found an alternative by accident:

You can buy Bitcoin and deposit it immediately on BlockFi, where you can convert it to GUSD. To withdraw your money you would sell your GUSD, buy Bitcoin and sell it for cash. As you can see, although it’s a 8.6% interest on GUSD the process to deposit it will take a while , and getting your money back will also take a few days. The advantage is that the value of your GUSD deposit doesn’t fluctuate, unlike the price of Bitcoin. Additionally you incur a loss when converting Bitcoin to GUSD and back of about 2%. That means the first 3 months of your interest are eaten away by conversion fees but you can earn it back with their referral programs that awards up to 250$ in BTC if you deposit Bitcoin and hold it in BlockFI for at least 2 months. I recently became an affiliate of this platform, yet I’ve been recommending it for the past months for free. It’s great wether or not you my referral code.

Here are the risks:

- BlockFi could lend our Bitcoin and GUSD too aggressively and not be able to get it back. Probability – low. BlockFi is asking for a large collateral and have a solid risk management approach.

- GUSD is based on the Etherium protocol and network which is centralized and not censorship resistant. It could be banned. Probability – low. GUSD is legal and approved by the US Government.

- The 8.6% interest earned is in US dollars which are losing value faster than the Euro is. When withdrawing your money you may end up with less Euros despite this high interest. Probability – high. This is a risk EU investors take with all US securities especially in the short term.

- BlockFi could lose investors’ Bitcoin through human error – and my account is not insured like a typical bank account. Probability – low but indeed you account is not insured or backed by US or EU governments.

I recently started using the GUSD interest account too at 8.6% interest and I cant wait to see how this goes too – again I can withdraw the money at any time making it virtually equivalent to holding cash on my bank account. I think there’s a high chance that my mortgage is paid entirely from the interest collected from them. Especially if Bitcoin continues to appreciate in price as the models above predict. Unlike classical p2p lending platforms, BlockFi makes everything simple for you – just deposit your money and earn interest. Behind the scenes they do the work and keep the difference in profit for themselves.

What is happening on the stock market?

Interest for US government bonds (US treasuries 10 year) have been spiking from 0.7% to 1.6% recently. This means investors prefer to earn money from safe government treasuries when compared to risky stocks, many of which do not make even that 1.6% interest on an annual basis. So for example if you own Apple stock which has a PE ratio of 35, or in other words earns about 3% per share yearly but could drop at any time, wouldn’t you much rather own treasuries at 1.6% risk free? As a result of this spike in treasuries many of the high growth stocks valued richly have come down 20-40%, especially tech stocks and will continue dropping with every significant upwards move of the 10 year treasury:

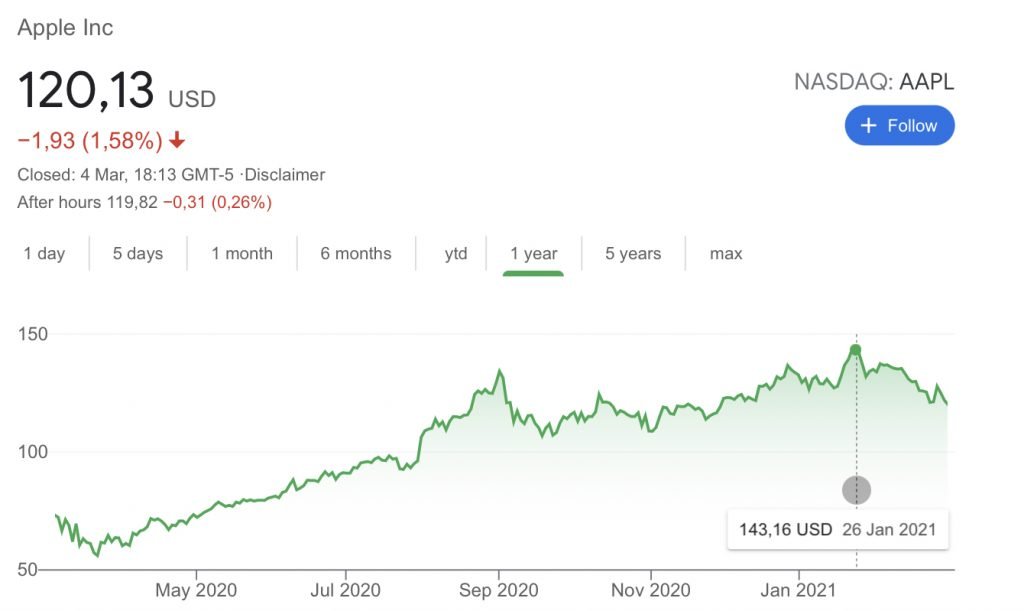

Apple dropped 16% in this correction

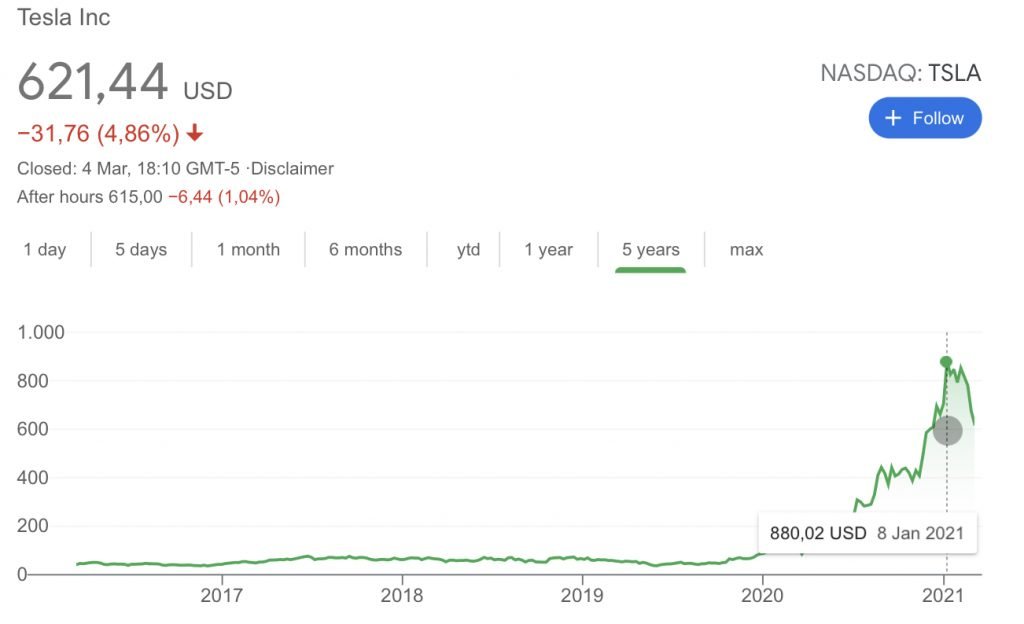

Tesla stock dropped 27%

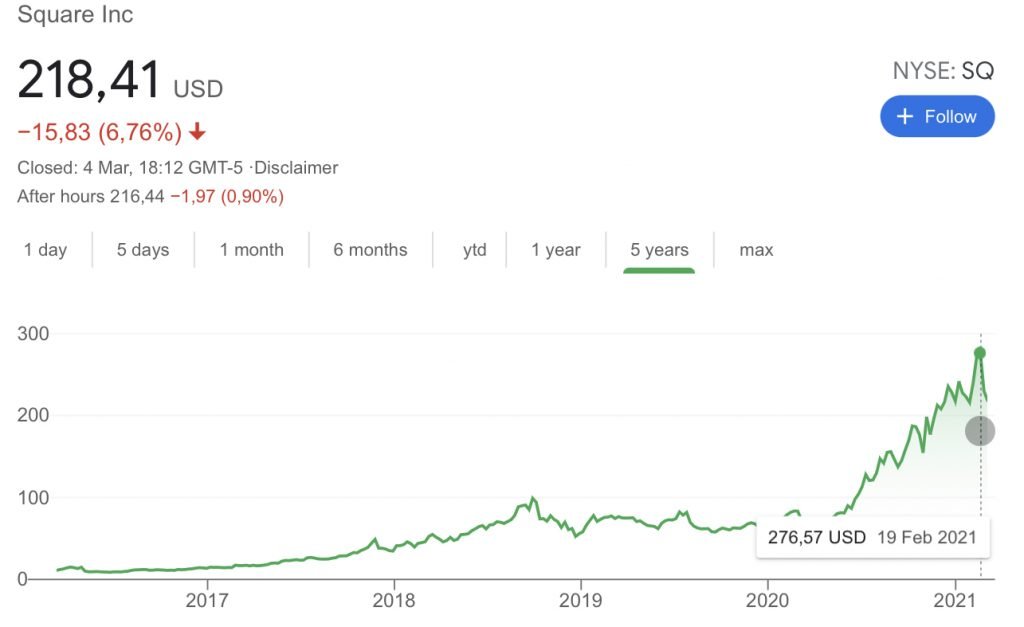

Square dropped 19%

While we’re comparing interest rates with stock prices, if interest rates were allowed to go to their natural level at around 5% like they are in the Bitcoin universe – all investors would prefer to earn 5% guaranteed interest income, versus 3%, which is what the average company in the S&P500 is earning (at a P/E ratio of 33, it means they make 3$ in earnings for every 100$ you pay per share). The entire S&P500 index and companies in it would have to be re-priced if interest rates would increase to 5%. In other words interest rates act like gravity for stocks. Although they are not my favorite here is how ARK Invest explains this very same drop. They have been buying Square and Tesla in the last few days. You can subscribe to their daily trading notifications here.

Investors that used all their cash to enter the stock market in January in hopes of a quick profit are quickly discovering the value of dollar cost averaging. As I said many times in the past – short term profits are an illusion and the only way to make money in the stock market as a retail investor is long term investment. Even if this correction continues for a significant period of time, I am sure that between 2025 and 2030 the companies we invest in will be much, much more valuable. The same investors who regret buying Tesla today and want to sell it at a loss will regret doing so in 2025. For investors in the original club and followers of this newsletter – it just means you keep dollar cost averaging into the stock market. Tesla at under 600$ a share? Yes please, and make it a double portion! Can it drop any lower? Yes it can. We hope it does.

There’s a deeper moral behind this story – of losing money in the hopes of making a quick buck. You should never expect too much of life and never put your hopes in a short term swing. A slow and sure approach will beat someone who is trying to borrow money to buy stocks and trade them in hopes of profit. I find it ironic that an investor starting out with 100$ would have better returns today than someone who started with 10.000$ and maybe even borrowed money and invested it all at once just to make more profit. As Charlie Munger, W Buffet’s partner would say – dont expect to much from life and when hard times come, expect to get your fair share. Keep your head down, keep working and keep investing. There are no shortcuts.

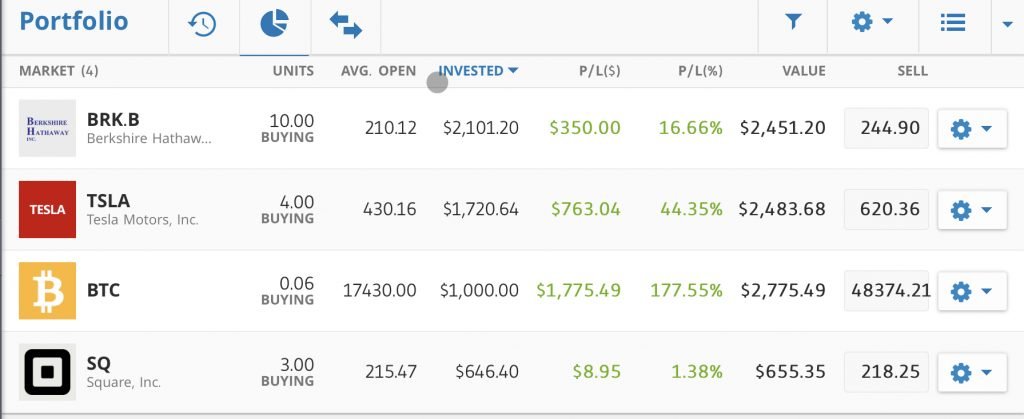

Coming back to our returns, if you’re wondering how the newsletter portfolio is doing, it’s doing 60-80% returns and that’s quite remarkable since it only exists for 5 months and we’re in a correction. Unfortunately eToro no longer allows me to add to the Bitcoin position in this virtual portfolio or we would be well above 100% profits:

Etoro virtual portfolio: +16% BRK.B, +44% TSLA, +177% Bitcoin, +1% SQ

What’s happening to our companies?

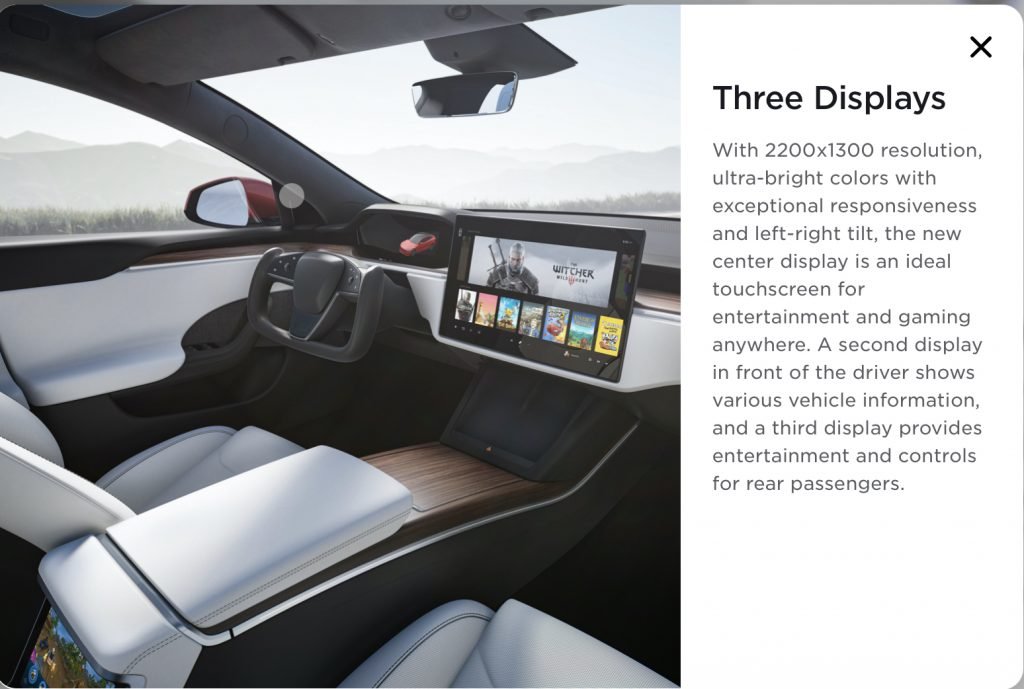

Tesla($TSLA) has finished 2020 with a record amount 20 Billion USD in its cash reserves (1.5Billion of which is already in Bitcoin) and the company delivered 499,500 thousand cars. That’s half a million. The press of course focused on Tesla missing it’s original target by 500 cars ignoring the fact that deliveries grew 60% in a pandemic year, while every other car brand had a contraction. The press and Wall Street continue to underestimate Tesla and not understand how fast the company is growing: From launching the Model 2 at 25-30 thousand dollars, to the Tesla Semi, Roadster, battery production, solar roof, the Berlin and Texas factories and the new Model S with a 800KM battery and the equivalent of a PS4/Xbox integrated into the car for gaming:

Another one of the fields in which Tesla is making progress is Full Self Driving. They plan on launching a FSD subscription in 2021 for about 200$/month the rumors say , which will essentially double Tesla’s profitability. Personally I cant wait for it as I don’t want to buy the FSD option upfront for 10.000$. I can cancel the subscription any time. Still, looking at FSD Beta videos online you can see how close Tesla really is to solving the autonomous car problem (I estimate 1 year to a working solution and 5 years to a nearly-perfect system). Tesla continues to be a company you want to own well into 2030 even if in the short term the stock ran ahead of the company.

Berkshire Hathaway($BRK.B):

Had a good year and altough profits are down 9% due to the pandemic, Berkshire repurchased 25 Billion worth of it’s own shares. That means that just by removing shares from the market Berkshire’s stock value increased 5%. Other than that it also had to admit a mistake when purchasing a company called Precision castparts which results in a 11 Billion accounting loss. The remainder of Berkshire’s businesses are humming alone just fine as they have been for half a century – profitably. Warren Buffet’s annual letter to shareholders is full of wise advice including my favorite: “owning a non-controlling portion of a wonderful business is more profitable, more enjoyable and far less work than struggling with 100% of a marginal enterprise”. Among other interesting facts in this letter Warren recognizes there is a group of shareholders(like me) who park their money in Berkshire for slow growth and are willing to take it out if better opportunities present themselves. Although that’s not the ideal Berkshire shareholder I’m glad he recognizes this reality. And speaking of interesting opportunities, Berkshire invested a couple of Billions in 2020 in Chevron(Oil, gas, refineries) and Verizon(Telecommunications). Although I’m sure their dividends and numbers are good I’m not sure these two companies will perform well going into the next decade of green technology, electric cars and revolutions in satellite communications as evidenced by Starlink, subsidiary of SpaceX which beams down internet from space. In my opinion this continues to showcase Berkshire’s lack of knack for Technology and these are not the companies I would be putting money behind. We may part with our Berkshire shares profitably one day – if these trends continue.

Square($SQ) finished 2020 on a positive note, with record Bitcoin profits, 36 million active Cash App users and many new initiatives to strengthen the bond between these users and Cash App. Unfortunately, Square also announced that they purchased Tidal – a music streaming service. Their entry into the music streaming space doesn’t Square(haha) up with my theory that they will become the leading Digital bank for the new generation offering loans, insurance, investments and Bitcoin custody and services to their users. Here is the CEO of Square and Twitter, Jack Dorsey explaining this move. The truth is that Square’s annual and quarterly reports are full of detail yet lack the same vision and focus we see lacking here. I’m sure Square can solve the streaming industry’s problems but I’m not sure that’s where the core expertise and focus of the company should be. Banking is a far worse offender with hundreds of countries excluded from proper financial access. This is a far greater challenge and opportunity and I’m afraid Square doesn’t have the focus to execute on it. I will review our position in Square this year again – although its small in our portfolio.

Last but not least I want to give a massive shoutout to Gheorghe, one of the original investors in the Club because he spends hours on end learning about Bitcoin and economics. Many of his ideas are spread throughout this newsletter and you can read his juicy replies in our facebook group (See issue #1 of the newsletter for details on it). Because many of us are aged 25-40 we are enjoying our newborn babies, investing as much as we can and living the most productive years of our lives. Couldn’t have found a better moment to start investing, either. .

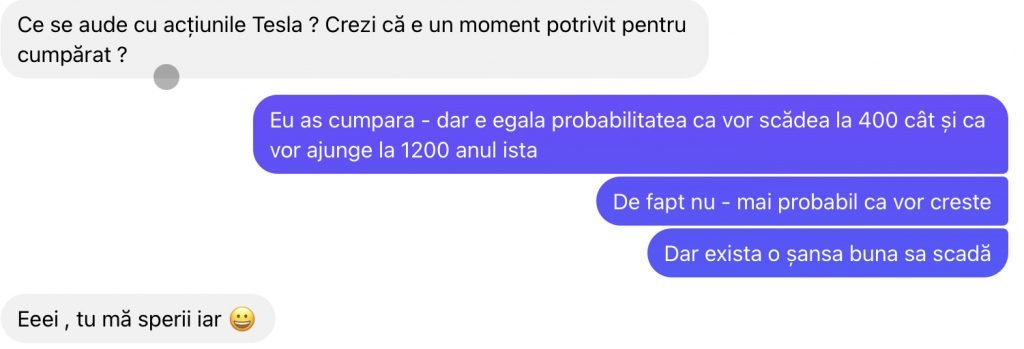

Finally, a bit of humor and fireworks if you missed the $GME saga but still like to hear about a good speculative move. In January someone reached out to me asking if they should invest in $TSLA at 870$ a share just for 6 months – when they need the money back. I said it could go up or down, and invest carefully:

“Hey, don’t scare me”

“Heey, you’re scaring me”

Our anonymous investor

Despite my warnings they went ahead an invested. And not just one investor but a few others like them – everything in one go in $TSLA. Even worse some of them invested in companies they had only heard about the day before. Here’s what they had to say when the correction came (it’s Romanian but I translate the funny parts):

I want to sell 6 TSLA stocks and buy Bitcoin. I’m tired of Tesla. Lost 600$

“I want to sell 6 TSLA stocks and buy Bitcoin. I’m tired of Tesla. Lost 600$“ . To which I say, get out of the stock market and stop speculating please on the short term moves:

Heey, you’re scaring me again!

Anonymous investor.

As you can see the Buy High Sell Low strategy is up for display here. This natural reaction to a big drop in the market is why this newsletter exists. Investments require common sense and as Charlie Munger puts it “Common sense is not so common”.

PS: If you follow the content I linked in this issue(31 links) you will find hundreds of hours of informative podcasts and videos you can listen to at will

||

---------------------------

By: [email protected]

Title: EN: #4 Investment club Newsletter – Bitcoin and earning 8.6% Interest on cash

Sourced From: danursu.com/en-4-investment-club-newsletter-bitcoin-and-earning-8-6-interest-on-cash/

Published Date: Mon, 08 Mar 2021 23:23:26 +0000

Read More

.png) InvestingStocksToolsClubsVideosPrivacy PolicyTerms And Conditions

InvestingStocksToolsClubsVideosPrivacy PolicyTerms And Conditions