||

Modern Portfolio Theory (MPT), ever since its inception by Harry Markowitz in the early 1950s, has revolutionized the way investors and financial analysts perceive risk and return. As the financial world has continued to evolve, so too have the tenets of MPT. The evolution of MPT, its implications for asset allocation, and the challenges it faces in today’s financial landscape are all crucial to understanding contemporary portfolio management.

Historical Overview of MPT

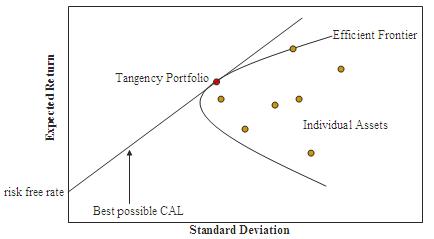

In the early 1950s, Harry Markowitz introduced the concept of MPT through his paper, “Portfolio Selection,” published in the Journal of Finance (Markowitz, 1952). The core premise of MPT is the optimization of portfolios to maximize expected return for a given level of risk. Markowitz proposed the idea that investors are not only concerned with returns but with the risk associated with those returns. He introduced the concept of an efficient frontier – a set of portfolios that offers the maximum expected return for a defined level of risk. The Capital Asset Pricing Model (CAPM) introduced by Sharpe (1964) and Lintner (1965) further expanded on MPT. It linked the expected return of an asset to its risk, measured by its beta with the market.

Efficient Frontier Graph

Implications of MPT for Asset Allocation

MPT suggests that by diversifying investments, specific risks can be mitigated without affecting potential returns. The diversification benefit arises because different assets don’t move exactly in tandem. The less correlated these assets are, the more the risk reduction potential; sort of like putting your eggs in more baskets.

Efficient Frontier and Asset Allocation

By plotting different combinations of assets on the risk-return plane, one can find the efficient frontier. For investors, this means pinpointing the desired level of risk and selecting the portfolio on the frontier that matches this risk level.

The Role of Beta in Asset Allocation

CAPM introduced the concept of beta – a measure of how much a particular asset’s returns move relative to the market. Assets with a beta greater than one are considered more volatile than the market, while those with a beta less than one are less volatile. By understanding an asset’s beta, investors can better align their portfolios with their risk tolerance.

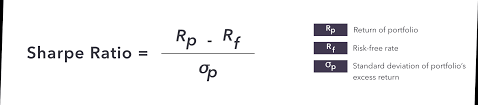

The Relevance of the Sharpe Ratio

Introduced by William Sharpe in 1966, the Sharpe Ratio measures the performance of an investment compared to a risk-free asset, after adjusting for its risk. It’s a crucial tool for comparing the risk-adjusted returns of different portfolios or assets. The Sharpe Ratio is calculated by subtracting the risk-free rate from the expected return of the investment and then dividing by the standard deviation of the investment’s returns. A higher Sharpe Ratio indicates better risk-adjusted performance, as it signifies that an investor is receiving more return per unit of risk taken.

Sharpe Ratio Formula

Modern Challenges to MPT

While MPT has been foundational in finance, it has not been without criticism and challenges, especially in the light of financial crises like that of 2008.

Non-Normal Distribution of Returns

MPT assumes that asset returns are normally distributed, which isn’t always the case. Events termed as “Black Swans” by Nassim Nicholas Taleb, signify extreme market events that are not predicted by standard financial models (Taleb, 2007). Black Swans are rare and unpredictable occurrences that have profound and widespread ramifications on financial markets, challenging traditional financial theories and exposing the limitations of relying solely on historical data for predicting future events.

Changing Correlations

MPT relies heavily on correlations between assets staying consistent over time. However, during financial crises, correlations can converge, reducing the benefits of diversification.

Emerging Behavioral Finance Theories

Behavioral finance, which studies the effects of psychological factors on financial markets, suggests that investors do not always act rationally, which can lead to market inefficiencies. Researchers like Shiller (2003) have argued that irrational exuberance and herd behavior can result in asset bubbles and their eventual bursts.

The Future of MPT and Implications for Asset Allocation

Given the aforementioned challenges, does MPT still hold relevance in today’s dynamic financial world?

Integration with Behavioral Finance

Merging the concepts of behavioral finance with MPT can lead to a more holistic understanding of market dynamics. By accounting for psychological factors, asset allocation strategies can be more resilient against irrational market behaviors.

Factor-Based Investing

Beyond the traditional beta, factor-based investing looks at multiple factors like size, value, momentum, etc., to explain asset returns. This multifactor approach can offer a more nuanced understanding of asset risk and potential returns.

Technological Advancements and MPT

With the rise of artificial intelligence and machine learning, there’s potential to refine asset allocation strategies by processing vast amounts of data to identify patterns and trends not immediately apparent through traditional analysis.

Wrapping Up: MPT in the 21st Century

Modern Portfolio Theory has undeniably shaped the way we approach investing. Its principles of diversification, risk optimization, and efficient frontier formation are foundational in finance. While challenges arise, especially during financial crises and market anomalies, MPT’s core concepts remain robust.The future of MPT, intertwined with behavioral finance, technological advancements, and new investment paradigms like factor-based investing, paints a promising picture. For investors and financial professionals, understanding MPT’s evolution and its implications ensures they’re equipped with the tools to navigate the ever-evolving financial landscape.

References

Markowitz, H. (1952). Portfolio Selection. Journal of Finance, 7(1), 77-91.

Sharpe, W. F. (1964). Capital asset prices: A theory of market equilibrium under conditions of risk. The Journal of Finance, 19(3), 425-442.

Lintner, J. (1965). The valuation of risk assets and the selection of risky investments in stock portfolios and capital budgets. The Review of Economics and Statistics, 47(1), 13-37.

Taleb, N. N. (2007). The black swan: The impact of the highly improbable. Random House.

Shiller, R. J. (2003). From efficient markets theory to behavioral finance. Journal of Economic Perspectives, 17(1), 83-104.

The Evolution of Modern Portfolio Theory and Its Implications for Asset Allocation

Modern Portfolio Theory (MPT), ever since its inception by Harry Markowitz in the early 1950s, has revolutionized the way investors and financial analysts perceive risk and return. As the financial world has continued to evolve, so too have the tenets of MPT. The evolution of MPT, its implications for asset allocation, and the challenges it faces in today’s financial landscape are all crucial to understanding contemporary portfolio management.

Historical Overview of MPT

In the early 1950s, Harry Markowitz introduced the concept of MPT through his paper, “Portfolio Selection,” published in the Journal of Finance (Markowitz, 1952). The core premise of MPT is the optimization of portfolios to maximize expected return for a given level of risk. Markowitz proposed the idea that investors are not only concerned with returns but with the risk associated with those returns. He introduced the concept of an efficient frontier – a set of portfolios that offers the maximum expected return for a defined level of risk. The Capital Asset Pricing Model (CAPM) introduced by Sharpe (1964) and Lintner (1965) further expanded on MPT. It linked the expected return of an asset to its risk, measured by its beta with the market.

Efficient Frontier Graph

Implications of MPT for Asset Allocation

MPT suggests that by diversifying investments, specific risks can be mitigated without affecting potential returns. The diversification benefit arises because different assets don’t move exactly in tandem. The less correlated these assets are, the more the risk reduction potential; sort of like putting your eggs in more baskets.

Efficient Frontier and Asset Allocation

By plotting different combinations of assets on the risk-return plane, one can find the efficient frontier. For investors, this means pinpointing the desired level of risk and selecting the portfolio on the frontier that matches this risk level.

The Role of Beta in Asset Allocation

CAPM introduced the concept of beta – a measure of how much a particular asset’s returns move relative to the market. Assets with a beta greater than one are considered more volatile than the market, while those with a beta less than one are less volatile. By understanding an asset’s beta, investors can better align their portfolios with their risk tolerance.

The Relevance of the Sharpe Ratio

Introduced by William Sharpe in 1966, the Sharpe Ratio measures the performance of an investment compared to a risk-free asset, after adjusting for its risk. It’s a crucial tool for comparing the risk-adjusted returns of different portfolios or assets. The Sharpe Ratio is calculated by subtracting the risk-free rate from the expected return of the investment and then dividing by the standard deviation of the investment’s returns. A higher Sharpe Ratio indicates better risk-adjusted performance, as it signifies that an investor is receiving more return per unit of risk taken.

Sharpe Ratio Formula

Modern Challenges to MPT

While MPT has been foundational in finance, it has not been without criticism and challenges, especially in the light of financial crises like that of 2008.

Non-Normal Distribution of Returns

MPT assumes that asset returns are normally distributed, which isn’t always the case. Events termed as “Black Swans” by Nassim Nicholas Taleb, signify extreme market events that are not predicted by standard financial models (Taleb, 2007). Black Swans are rare and unpredictable occurrences that have profound and widespread ramifications on financial markets, challenging traditional financial theories and exposing the limitations of relying solely on historical data for predicting future events.

Changing Correlations

MPT relies heavily on correlations between assets staying consistent over time. However, during financial crises, correlations can converge, reducing the benefits of diversification.

Emerging Behavioral Finance Theories

Behavioral finance, which studies the effects of psychological factors on financial markets, suggests that investors do not always act rationally, which can lead to market inefficiencies. Researchers like Shiller (2003) have argued that irrational exuberance and herd behavior can result in asset bubbles and their eventual bursts.

The Future of MPT and Implications for Asset Allocation

Given the aforementioned challenges, does MPT still hold relevance in today’s dynamic financial world?

Integration with Behavioral Finance

Merging the concepts of behavioral finance with MPT can lead to a more holistic understanding of market dynamics. By accounting for psychological factors, asset allocation strategies can be more resilient against irrational market behaviors.

Factor-Based Investing

Beyond the traditional beta, factor-based investing looks at multiple factors like size, value, momentum, etc., to explain asset returns. This multifactor approach can offer a more nuanced understanding of asset risk and potential returns.

Technological Advancements and MPT

With the rise of artificial intelligence and machine learning, there’s potential to refine asset allocation strategies by processing vast amounts of data to identify patterns and trends not immediately apparent through traditional analysis.

Wrapping Up: MPT in the 21st Century

Modern Portfolio Theory has undeniably shaped the way we approach investing. Its principles of diversification, risk optimization, and efficient frontier formation are foundational in finance. While challenges arise, especially during financial crises and market anomalies, MPT’s core concepts remain robust.The future of MPT, intertwined with behavioral finance, technological advancements, and new investment paradigms like factor-based investing, paints a promising picture. For investors and financial professionals, understanding MPT’s evolution and its implications ensures they’re equipped with the tools to navigate the ever-evolving financial landscape.

References

Markowitz, H. (1952). Portfolio Selection. Journal of Finance, 7(1), 77-91.

Sharpe, W. F. (1964). Capital asset prices: A theory of market equilibrium under conditions of risk. The Journal of Finance, 19(3), 425-442.

Lintner, J. (1965). The valuation of risk assets and the selection of risky investments in stock portfolios and capital budgets. The Review of Economics and Statistics, 47(1), 13-37.

Taleb, N. N. (2007). The black swan: The impact of the highly improbable. Random House.

Shiller, R. J. (2003). From efficient markets theory to behavioral finance. Journal of Economic Perspectives, 17(1), 83-104.

||

---------------------------

By: Abesalom Webb

Title: The Evolution of Modern Portfolio Theory and Its Implications for Asset Allocation

Sourced From: streetfins.com/the-evolution-of-modern-portfolio-theory-and-its-implications-for-asset-allocation/

Published Date: Sun, 27 Aug 2023 22:33:35 +0000

Read More

Did you miss our previous article...

https://peaceofmindinvesting.com/clubs/macroeconomic-models

.png) InvestingStocksToolsClubsVideosPrivacy PolicyTerms And Conditions

InvestingStocksToolsClubsVideosPrivacy PolicyTerms And Conditions