<iframe style="width:120px;height:240px;" marginwidth="0" marginheight="0" scrolling="no" frameborder="0" src="//ws-na.amazon-adsystem.com/widgets/q?ServiceVersion=20070822&OneJS=1&Operation=GetAdHtml&MarketPlace=US&source=ss&ref=as_ss_li_til&ad_type=product_link&tracking_id=peaceinvesting-20&language=en_US&marketplace=amazon®ion=US&placement=0060555661&asins=0060555661&linkId=80f8e3b229e4b6fdde8abb238ddd5f6e&show_border=true&link_opens_in_new_window=true"></iframe>|<iframe style="width:120px;height:240px;" marginwidth="0" marginheight="0" scrolling="no" frameborder="0" src="//ws-na.amazon-adsystem.com/widgets/q?ServiceVersion=20070822&OneJS=1&Operation=GetAdHtml&MarketPlace=US&source=ss&ref=as_ss_li_til&ad_type=product_link&tracking_id=peaceinvesting-20&language=en_US&marketplace=amazon®ion=US&placement=1119404509&asins=1119404509&linkId=0beba130446bb217ea2d9cfdcf3b846b&show_border=true&link_opens_in_new_window=true"></iframe>|<iframe style="width:120px;height:240px;" marginwidth="0" marginheight="0" scrolling="no" frameborder="0" src="//ws-na.amazon-adsystem.com/widgets/q?ServiceVersion=20070822&OneJS=1&Operation=GetAdHtml&MarketPlace=US&source=ss&ref=as_ss_li_til&ad_type=product_link&tracking_id=peaceinvesting-20&language=en_US&marketplace=amazon®ion=US&placement=1119376629&asins=1119376629&linkId=2f1e6ff64e783437104d091faaedfec7&show_border=true&link_opens_in_new_window=true"></iframe>

[Editor's Note: WCI is proud to introduce a new community and webinar series, and the aim is to turn your financial life from a source of stress into a source of strength. The Financially Empowered Women (The FEW) is a newly created WCI community that supports women on their path to financial success. Make sure to join us on September 26 at 6pm MT for our free kickoff webinar on how to create an intentional financial life. We know that, as a woman, you wear many hats, and it’s easy to push financial education to the side. But you can change that now, and The FEW wants to be your catalyst!]

By Dr. Jim Dahle, WCI Founder

Long-term readers know that for the last six years, we have been investing a small portion (20%) of our portfolio into real estate and a fraction (25% or 5% of the whole portfolio) of that portion into private lending funds. I have written previously about these funds, but briefly, they collect money from investors and lend it out to real estate operators. They pay the operators' expenses, take their fees, and share the remainder of the profits with the investors. The investor gets a high-yielding, passive investment of dozens of real estate-backed loans.

As an investment, the returns tend to be relatively high (stock-like) and quite steady but terribly tax-inefficient. The main risk, besides manager risk, is simply that the debt fund becomes an equity fund in a terrible real estate downturn when the operators mail in the keys instead of the payments due.

Private or Public Real Estate Investments?

There are public companies and REITs that do the same thing and trade on the stock market. You can even buy an iShares ETF of these companies. Like anything traded on the stock market, the returns of these public investments tend to be more correlated with the overall market and display more volatility. While the underlying source of returns is the same, there is more of a speculative component introduced—at least in the short run—due to the company being marked to market each day. As I write this, the yield on this ETF is nearly 10%, but that's dramatically higher than it was before it lost more than 27% of its value in 2022. If you don't like that sort of volatility, you may prefer to invest on the private side.

More information here:

The Case for Private Real Estate

Comparing Private Real Estate Lending Funds

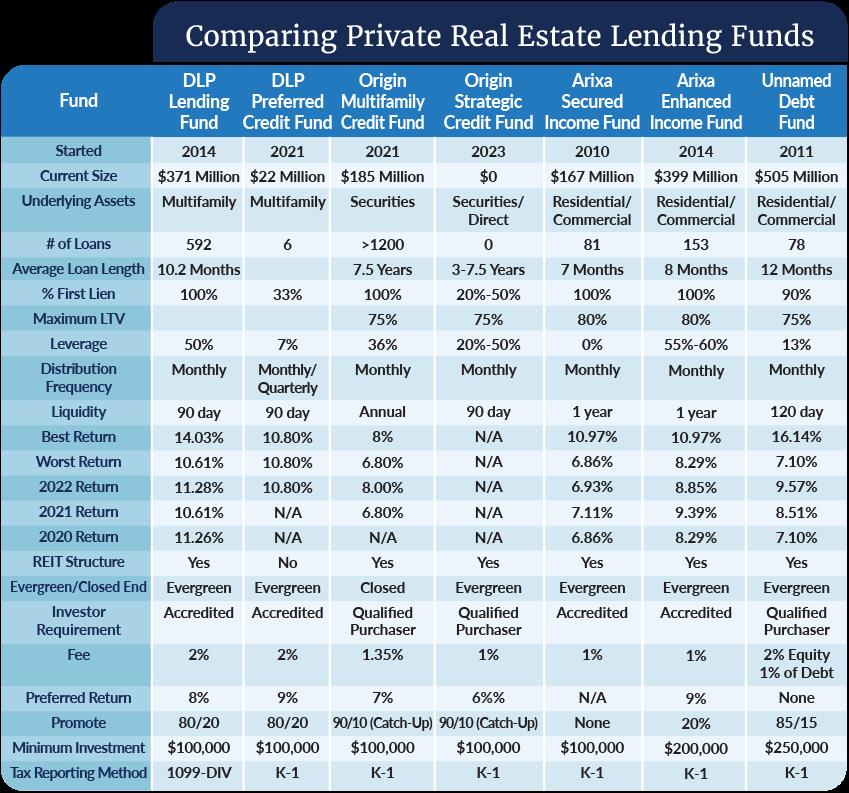

Today, I thought I would compare seven different private real estate lending funds from four different companies. This is not a comprehensive list of these funds. It is, however, a list that includes all of the funds I have invested in and the funds offered by our real estate partners (i.e. advertisers). One fund will remain unnamed at the request of the fund manager (don't ask me why). The funds we will be talking about include:

- DLP Lending Fund

- DLP Preferred Credit Fund

- Origin Multifamily Credit Fund

- Origin Strategic Credit Fund

- Arixa Secured Income Fund

- Arixa Enhanced Income Fund

- Unnamed Debt Fund

Here is a chart comparing the funds to each other, as of April 2023.

As you can see, there is a lot to know before you invest. However, given the straightforward nature of the business and the relatively high liquidity of these funds, they might be the easiest private investments on which to do due diligence.

None of these funds are particularly old. If you're looking for a track record similar to the 95-year-old Vanguard Wellington Fund, you can give up right now. Between 10-15 years is pretty good in this space. Most of the collateral for these loans is apartment buildings, no matter what fund you invest in. The funds all hold dozens but usually not hundreds of loans. You will find significant variation in the percentage of the fund that is invested in first lien position. That means you are the senior lender on a project, so if everything goes to Hades in a handbasket, you should be the first one to get your money back. The fund has the ability to foreclose on the property. Obviously, if you're going to take on the risk of not being in first lien position, you should get paid more to do that. The funds also have some variation in how much they will loan on a given project and how much leverage is used in the fund itself. That percentage of leverage used ranges from 0% to as much as 60% at times. The amount in the chart above is what they reported to me was actually being used in early 2023.

You may or may not care how often the fund pays you or how much liquidity it offers. Most of the funds have a 1-2 year lock-up but then will let you have your money back with 3-4 months of notice. Note that these partnership agreements usually include a provision that allows the fund to restrict withdrawals in exceptional circumstances (think Michael Burry in The Big Short).

Returns vary between 6%-16%, but they're pretty steady year to year. I generally expect 7%-11% out of these funds. Most of them have adopted a REIT structure, which allows you to deduct 20% of the income thanks to the Qualified Business Income (QBI) or 199A deduction through 2025, but they're still not particularly tax-efficient since the entire return is basically income distributed every year and taxed at ordinary income tax rates. While most (but not all) send you a K-1, I don't recall ever having to file in another state due to investing in a debt fund.

Most (but not all) of these funds are evergreen, and they require you to be an accredited investor to invest. Minimum investments range from $50,000-$250,000, making it challenging for anybody who is not rich yet to even get into the game, much less diversify between managers. For example, if you want 10% of your portfolio in this asset class but want at least three managers and you're looking at funds with $100,000 minimums, you're going to need a $3 million portfolio before you'll have your desired diversification.

The fee structure is also surprisingly variable. Some just charge a fee. Others charge a fee and a promote. Some charging a promote have a preferred return and others don't. One company pays you the preferred return before it even takes its fee.

DLP Lending Fund

This is one of the oldest funds from WCI sponsor DLP Capital. I've been investing in it (at first indirectly, now directly) since 2019. While it does use leverage, all of its loans are in first lien position (most with personal guarantees), and historically it has done very well. It is unique in that it offers a 1099 early in the year instead of a K-1 in the spring, although DLP has always been pretty prompt with its K-1s. It is a REIT, and it can offer a 199A deduction. But it doesn't really matter to me as we own this one in the WCI self-directed 401(k). The fee went up recently, but if you have $1 million+ in the fund, you can get a 0.5% discount on that. The 20% promote is only on profits above and beyond the 8% preferred return, which DLP pays prior to taking any of its own fees. The fund is 50% leveraged, and it has an average loan-to-value of 53%. Note that the $100,000 minimum is only available to white coat investors ($200,000 normally).

DLP Preferred Credit Fund

This is DLP's newest debt offering, rolled out in 2021. The main difference between this fund and the Lending Fund is that this fund has investments in it that are not in first lien position. DLP Capital CEO Don Wenner makes an argument that this fund is actually less risky than the Lending Fund because it only lends to DLP's highest-quality borrowers, and as evidence, he points to a track record of no delinquent loans ever in the fund. That argument will become more powerful as the years go by, I suppose. It offers a higher preferred return and a higher targeted return, but in its first full year (2022), it actually performed slightly worse than the Lending Fund. It is a much smaller fund with a lot fewer loans in it than the much older Lending Fund, but I expect that will grow with time. Still, it's a worthy option for those willing to hold a significant percentage of assets outside of first lien position. This fund uses minimal leverage, and its average loan-to-value of the loans (not the preferred equity in the fund) is just 40%. Note that the $100,000 minimum is only available to white coat investors ($200,000 normally).

Origin Multifamily Credit Fund

While I have been investing with Origin Investments since 2017, that has mostly been on the equity side (although its Income Plus fund does include a lot of debt-like preferred equity.) A dedicated debt fund is a relatively new offering for Origin, and this one is particularly unique. Rather than making loans directly to operators, this fund contains leveraged Freddie Mac “K-deal” and “SBL B-piece” securities. These mortgage-backed securities have low rates of default and have multifamily housing as the underlying asset. The fund targets an IRR of 8%-10% with a yield of 6%-8%. Unlike the other funds on this list, this is not an evergreen fund. It is a closed-end fund (and is now closed to new investors), and it will run for seven years before returning your capital (although it does offer liquidity annually).

Origin Strategic Credit Fund

This one is a brand new (April 2023) debt fund from Origin. Unlike the Multifamily Credit Fund, this one will be evergreen. It will invest in the securitized Freddie Mac products like the other fund, but it will also lend directly via mezzanine/preferred equity loans (i.e. not in first lien position). Origin has had lots of success with preferred equity in its Income Plus fund (which contains equity and preferred equity), and it expects this will be a $100 million+ fund by the end of the year. While Origin charges lower fees (and it's waiving that fee through November 2023) and a smaller promote percentage than DLP, its promote does use a 50/50 catch-up. Like DLP, fees drop the more you invest. The listed fees in the chart are the fees you would pay if you only invest the minimum.

Arixa Secured Income Fund

Arixa might be new to you, but it isn't new to us. We invested in this fund from 2018-2023. This fund uses no leverage and charges only 1% with no promote. It seems to be managed fairly conservatively. It's based out of California and primarily makes loans in California. The historical returns are not as high as some other companies despite having lower fees. That may just be a function of taking on less risk, however. Pretty much every other fund on this list is using at least some leverage, but this one does not. Both of the Arixa funds have a one-year lock-up and then can limit withdrawals to 25% per quarter for four quarters. But when I swapped from one to the other, I had full liquidity in less than 60 days.

Arixa Enhanced Income Fund

Do you like Arixa but are willing to take on some leverage to have higher returns? This is the fund for you. It does have a higher minimum investment, though. We owned the Secured Fund in taxable but swapped to this one when we moved this holding into the WCI self-directed 401(k). We figured it was most similar to the other two funds we own. Historically, the returns are about 2% higher.

Unnamed Debt Fund

We've been investing in this fund since 2020. The fees are relatively high (it even charges equity investors a fee on the debt the fund borrows to invest) but the returns historically have been reasonably good . . . right up until the time we invested. We think that is a short-term thing due to the pandemic, though, and the increasing returns over the last three years seem to bear that out. All returns in the chart, of course, are net of fees. This fund is the hardest one to invest in. Not only am I not telling you who runs it, but it requires a $250,000 minimum and qualification as a “Qualified Purchaser,” a higher standard than “Accredited Investor.”

More information here:

How Our Private Real Estate Investments Performed in 2022

What Should You Do?

If you want to invest in this asset class, I think you should limit it to a relatively small portion of your portfolio, perhaps something in the 5%-20% range. I like the asset class because of its steady returns, low correlation with the stock market, higher returns than the bond market, and real estate backing mostly in first lien position that makes it less likely to really be cleaned out (although the leverage does increase that risk.) The biggest issue in this asset class is the need to diversify against manager risk and the difficulty of doing that with such high minimum investments. I think using three managers is adequate diversification there, but which ones you use is up to you. I can introduce you to companies and I can tell you what I do, but I cannot provide formal investment advice to you.

A frequent question I get is, “Who should I invest with first if I can't afford to really be diversified yet?” My answer to that is that you probably shouldn't invest at all if that is the case, but I'll leave that decision up to you. You need to be a REAL accredited investor to invest in these sorts of investments. While the SEC will consider you an accredited investor just for earning the average physician income for each of the last two years, I think real accredited investors are people who can afford to lose their entire investment without having it affect their financial life AND who have the financial knowledge to evaluate the investment on its own merits without the aid of a financial advisor, attorney, accountant, or blogger.

What Do We Do?

We invest in the DLP Lending Fund in my 401(k), in the Arixa Enhanced Income Fund in Katie's 401(k), and in the Unnamed Fund in our SLAT taxable account in approximately equal amounts. Our preference is for evergreen funds and first lien position, and we are OK with the use of a reasonable amount of leverage.

When investing in private real estate lending funds, you need to do your due diligence. I hope this blog post can assist you with that process.

If you're interested in pursuing real estate investing and working with some of the WCI-vetted partners that I invest with, here are some of the best companies in the business.

Featured Real Estate Partners

DLP Capital

Type of Offering:

Fund

Primary Focus:

Multi-Family

Minimum Investment:

$100,000

Year Founded:

2008

Origin Investments

Type of Offering:

Fund

Primary Focus:

Multi-Family

Minimum Investment:

$50,000

Year Founded:

2007

37th Parallel

Type of Offering:

Fund / Syndication

Primary Focus:

Multi-Family

Minimum Investment:

$100,000

Year Founded:

2008

Southern Impression Homes

Type of Offering:

Turnkey

Primary Focus:

Single Family

Minimum Investment:

$60,000

Year Founded:

2017

Wellings Capital

Type of Offering:

Fund

Primary Focus:

Self-Storage / Mobile Homes

Minimum Investment:

$50,000

Year Founded:

2014

MLG Capital

Type of Offering:

Fund

Primary Focus:

Multi-Family

Minimum Investment:

$50,000

Year Founded:

1987

Mortar Group

Type of Offering:

Syndication

Primary Focus:

Multi-Family

Minimum Investment:

$50,000

Year Founded:

2001

AcreTrader

Type of Offering:

Platform

Primary Focus:

Farmland

Minimum Investment:

$15,000

Year Founded:

2017

* Please consider this an introduction to these companies and not a recommendation. You should do your own due diligence on any investment before investing. Most of these opportunities require accredited investor status.

What do you think? Do you invest in debt funds? Why or why not? Which ones do you invest in? Comment below!

The post Comparing Private Real Estate Lending Funds appeared first on The White Coat Investor - Investing & Personal Finance for Doctors.

||

----------------------------

By: The White Coat Investor

Title: Comparing Private Real Estate Lending Funds

Sourced From: www.whitecoatinvestor.com/comparing-private-real-estate-lending-funds/

Published Date: Tue, 12 Sep 2023 06:30:57 +0000

Read More

Did you miss our previous article...

https://peaceofmindinvesting.com/investing/inflation-hedges-the-real-side-hustle

.png) InvestingStocksToolsClubsVideosPrivacy PolicyTerms And Conditions

InvestingStocksToolsClubsVideosPrivacy PolicyTerms And Conditions