<iframe style="width:120px;height:240px;" marginwidth="0" marginheight="0" scrolling="no" frameborder="0" src="//ws-na.amazon-adsystem.com/widgets/q?ServiceVersion=20070822&OneJS=1&Operation=GetAdHtml&MarketPlace=US&source=ss&ref=as_ss_li_til&ad_type=product_link&tracking_id=peaceinvesting-20&language=en_US&marketplace=amazon®ion=US&placement=0060555661&asins=0060555661&linkId=80f8e3b229e4b6fdde8abb238ddd5f6e&show_border=true&link_opens_in_new_window=true"></iframe>|<iframe style="width:120px;height:240px;" marginwidth="0" marginheight="0" scrolling="no" frameborder="0" src="//ws-na.amazon-adsystem.com/widgets/q?ServiceVersion=20070822&OneJS=1&Operation=GetAdHtml&MarketPlace=US&source=ss&ref=as_ss_li_til&ad_type=product_link&tracking_id=peaceinvesting-20&language=en_US&marketplace=amazon®ion=US&placement=1119404509&asins=1119404509&linkId=0beba130446bb217ea2d9cfdcf3b846b&show_border=true&link_opens_in_new_window=true"></iframe>|<iframe style="width:120px;height:240px;" marginwidth="0" marginheight="0" scrolling="no" frameborder="0" src="//ws-na.amazon-adsystem.com/widgets/q?ServiceVersion=20070822&OneJS=1&Operation=GetAdHtml&MarketPlace=US&source=ss&ref=as_ss_li_til&ad_type=product_link&tracking_id=peaceinvesting-20&language=en_US&marketplace=amazon®ion=US&placement=1119376629&asins=1119376629&linkId=2f1e6ff64e783437104d091faaedfec7&show_border=true&link_opens_in_new_window=true"></iframe>

By Lawrence B. Keller, CFP®, CLU®, ChFC®, RHU®, LUFCF, A 2022 Platinum WCI Medical School Scholarship Sponsor

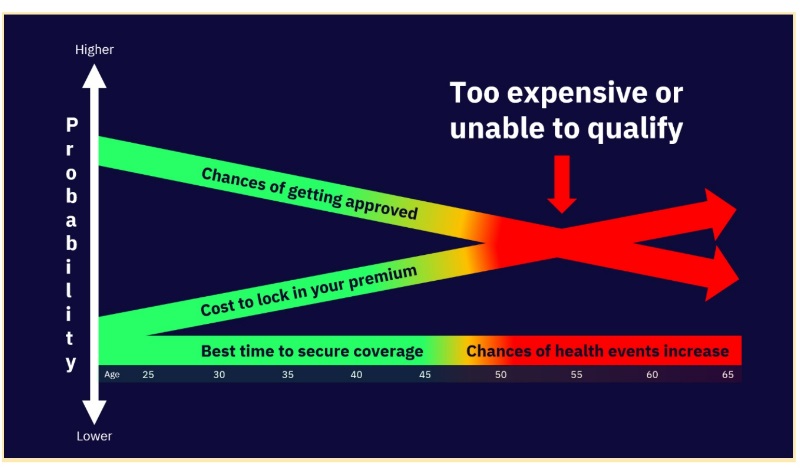

When it comes to insurance, most physicians don’t pay attention to details. They are more concerned with saving money in income taxes, investing in the stock market, or looking for new opportunities to increase their income beyond the practice of medicine. Unfortunately, this is the equivalent of putting the roof on a house before its foundation has been laid. That's why getting disability insurance early in your career is so important.

What’s at Stake?

If you complete your training at age 35, begin working with a salary of $200,000, and practice to age 65 with a 5% annual increase in income, you will earn approximately $14,152,144. If your starting salary is higher, you have that much more to potentially lose.

Note: Click on the charts to enlarge them.

Your Health Is Your Wealth

Let’s not forget that your health is what allows you to qualify to purchase disability insurance, and your ability to make the premium payment is what keeps the policy in force. While we are in good health, we often take this for granted and assume things will not change. I can assure you this is not always the case.

I receive calls on what seems like a daily basis from physicians who no longer qualify to purchase disability insurance for any number of reasons. The one thing they all seem to have in common is they know they should have already purchased it and that they had ample opportunity to do so.

Remember, while you might love what you do, the odds are that you are also working because you need to generate an income. If this is the case, you need to protect that income, and one of the most effective ways to do it is with disability insurance.

Employer-Provided/Sponsored Group Long-Term Disability Insurance

If you work for a large practice, a multi-specialty clinic, or a hospital, the odds are good you are provided with some type of Long-Term Disability (LTD) insurance coverage. While I do not typically recommend that it serves as the foundation of your disability income protection, due to the generally less favorable contractual provisions associated with it, there may be some significant benefits to having it—especially when supplemented with privately owned individual disability insurance.

Employer-provided or sponsored-group LTD plans will cover a percentage of your income up to a maximum monthly benefit or “cap.” For example, a typical LTD plan might provide coverage of 60% salary to a maximum of $10,000 or $15,000 per month. However, the percentage of income being replaced can vary along with the maximum monthly benefit.

Many physicians mistakenly believe that their group LTD plan will support their lifestyles in the event of a disability. This may not be the case for several reasons: group LTD plans may not cover all aspects of your earned income (such as overtime pay, shift differential, bonuses, and/or productivity or “incentive” pay) when calculating the monthly benefits payable.

As stated earlier, most LTD policies have a “cap” or maximum monthly benefit which may further limit the benefits one receives in the event of a claim. That means a physician earning $300,000 annually ($25,000 per month) assumes they will receive 60% of this amount ($180,000 annually or $15,000 per month). Yet in almost all situations, that will not be the case.

For example, this physician who earns $300,000 annually and who is insured under a group LTD plan that covers 60% income to a maximum of $10,000 per month would only be insured for $10,000 per month. This is significantly different from the $25,000 they were earning each month and much less than the $15,000 monthly benefit they thought they would receive from their group LTD plan.

In fact, the group LTD plan is only insuring them as if they were earning $200,000 (60% of $200,000 provides $120,000 annually or $10,000 per month, which is the plan’s maximum monthly benefit), leaving a significant amount of income unprotected!

Adding Individual Disability to Supplement a Group LTD Plan

Individual disability insurance policies will take all earned income into consideration when determining the amount of coverage available, and therefore, a larger amount of your income can be replaced. Most physicians may also not be aware that if their employer is paying the premium for their group LTD and not adding it back to their taxable income (including it in their W2), any benefits received from their LTD plan would be taxable, further reducing the amount of their income being replaced. In contrast, the monthly benefit from an individual disability insurance policy is typically received on an income tax-free basis when paid with personal post-tax dollars.

Group LTD policies typically do not have a true “Own Occupation” definition of disability. In fact, a well-known group LTD carrier’s policy states that, “You are disabled when due to your sickness or injury: You are unable to perform the material and substantial duties of your regular occupation and are not working in your regular occupation or any other occupation or, you are unable to perform one or more of the material and substantial duties of your regular occupation, and you have a 20% or more loss in your indexed monthly earnings while working in your regular occupation or in any occupation.”

While this policy protects a physician’s income, their monthly benefit may be reduced or potentially eliminated if they can no longer perform the duties of their medical specialty and choose to work in another occupation. As a result, supplementing a group LTD plan with an individual disability insurance policy can be very important.

Finally, group LTD plans typically offset for any benefits received for Social Security Disability, Worker’s Compensation, and other “deductible” sources of income. With the exception of the Social Insurance Substitute (SIS) Rider, which coordinates with payments received under Social Security and some other government programs, individual policies do not take these benefits into consideration.

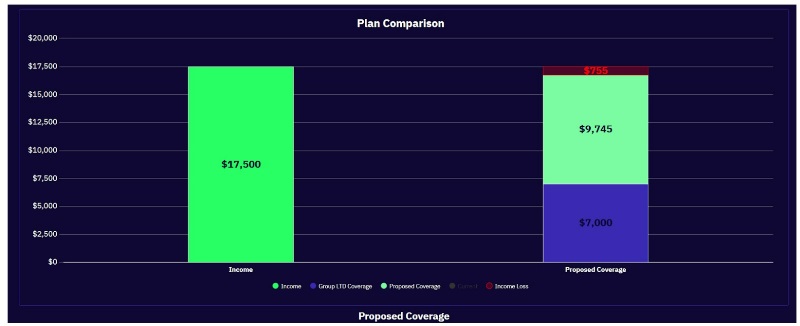

In this situation, a physician earning $300,000 ($25,000 per month) with employer-provided (taxable) group Long-Term Disability (LTD) coverage of $120,000 annually ($10,000 per month) would qualify to purchase up to $116,940 annually ($9,745 per month) of individual disability insurance ($140,340 annually).

Assuming a 30% tax on their group LTD coverage, they would “net” $200,940 annually or $16,745 per month ($7,000 per month of group LTD coverage and $9,745 per month of individual coverage), not including any Cost Of Living Adjustment (COLA). As a result, approximately 67% of their gross income would be replaced, as compared to the 40% that the group LTD plan alone would offer in this example.

One of my clients purchased his policy while he was completing his emergency medicine residency. At that time, his monthly benefit was $6,500 under the “New In Practice” limit. This amount was available to him regardless of his actual income or employer-provided group LTD coverage. He was earning approximately $64,000 and paying an annual premium of approximately $2,200, which represented 3.43% of his gross income. A few years later, he joined a practice that provided him with LTD coverage, and he sent an email to me stating, “I have a new employer that provides disability insurance. I would like to cancel my current policy as soon as possible.”

Here is an individual that was willing to pay almost 3.5% of his gross income for disability insurance on a resident’s salary, which demonstrated the value he saw in it—at least at that time. Now, three years later, he is earning a much larger salary and wants to cancel his individual disability insurance, because he has LTD from his new employer.

With the potential shortcomings outlined above, how does this make sense? What are the odds that he will even remain with this practice for the duration of his career?

What If You Have Medical Issues or Underwriting Concerns?

If you are a resident or a fellow and have pre-existing medical conditions or are concerned with medical underwriting, DO NOT apply for disability insurance coverage without checking into the availability of a Guaranteed Standard Issue (GSI) plan at your institution.

For those who are unaware, medical underwriting involves an application, a review of your medical records, a prescription drug check, questions related to your height/weight, and participation in “hazardous” activities.

If you are concerned about the outcome of a medically underwritten application, ask your insurance agent to speak with the underwriters or have your medical records reviewed informally—prior to applying for coverage. If this is not an option and one is available, secure the GSI plan first and then “shop around” to see if you can do “better” elsewhere.

Unfortunately, with most GSI plans, if you previously applied for medically underwritten coverage and were declined or offered a modified policy (a policy approved with an exclusion rider, limited benefit period, and/or a “rating” (additional sub-standard premium charge) to cover an adverse risk factor (like diabetes or obesity)), the GSI option may be off the table.

I should note that you do not need to provide your Social Security number, driver’s license number, or place of birth to obtain quotes. You also should not be signing anything—electronically or otherwise—that looks like or states it is an application for disability insurance (until you can confirm how your policy may potentially be issued based on your health, income, and lifestyle that you have disclosed to your agent). I cannot stress this enough.

Over the past few months, I have been contacted by several residents/fellows that wanted to purchase a GSI plan. Shortly after I submitted their applications, the insurance company came back asking about recent applications for disability insurance elsewhere. These clients were unaware that they had applied for medically underwritten coverage and were declined or offered modified coverage. As a result, they no longer qualify for the GSI plan they desired.

Different companies have different rules as to when you are ineligible for a GSI plan. For example, Berkshire (Guardian) GSI plans include a unique option for recent medical school and residency graduates that allows them to qualify—even if they were declined or offered modified coverage by another insurance company. That GSI plans state that the proposed insured not be determined to need modified coverage or have been declined by another disability insurance carrier more than nine months after their residency or fellowship hire date or in the past five years, whichever is shorter.

This means the “Endorsed” Agent has nine months to contact new residents/fellows to make them aware of their GSI program and the risk to their eligibility if they apply with another carrier. The nine months specifically was determined to be a reasonable time frame to give the agent running a GSI plan enough time to be in contact with them.

This provision was added after running into issues where a graduating medical student or resident was declined by another carrier before starting their residency or fellowship at a school with a GSI plan. These residents and fellows then subsequently learn they are not eligible for the GSI program because of a decline that occurred before they were even aware of the program.

Most GSI plans use the same policy that you would purchase on an individual basis, from the same companies, that require medical underwriting. However, if a GSI is offered at the hospital where you are doing your residency or fellowship (at the time of application), no medical underwriting is required. GSI plans are exclusive to specific agents, and only these “Endorsed” Agents can make the GSI plan available to residents/fellows at that specific institution. Often, agents that do not have access to them strongly discourage physicians from purchasing these plans, putting the client’s income protection needs at risk—especially when they may have existing health issues.

In theory, the additional risk the insurance company takes on from residents/fellows with pre-existing conditions is mitigated by the large volume of those applying for the GSI plan—many of whom do not have pre-existing health conditions and remain healthy long-term. In addition to volume, insurance companies protect themselves using a pre-existing condition limitation.

This states that disability due to a pre-existing condition is excluded from coverage for the first 12 months that the policy is in force. After the first 12 months, a pre-existing condition will be covered only if the pre-existing condition is not specifically excluded from coverage by amendment or endorsement.

A pre-existing condition is any mental or physical condition for which, during the three-month period preceding the policy’s effective date, you have consulted a physician, received medical treatment or services, or undergone diagnostic procedures—or for which a reasonably prudent person would have sought medical advice, care, or treatment.

There are exceptions to the pre-existing conditions limitation. For example, Berkshire (Guardian) GSI plans do not include one at all.

Who Benefits from a GSI Plan?

- Anyone with a pre-existing medical condition. These might include a chronic medical condition such as anxiety/depression, ADD/ADHD, surgery requiring the placement of hardware (pins, screws, anchors), sleep apnea, diabetes, and joint/spine disorders.

- Anyone who is “overweight” and may not qualify for standard coverage due to their build.

- Those that participate in “hazardous” activities such as mountain or rock climbing; martial arts; motorsports events or racing (auto, truck, cycle, boat, etc.); scuba diving; skydiving; hang gliding; parachuting; and/or paragliding.

- Those that self-prescribe. I saw more of this in the past academic year than ever before. While it may be OK to prescribe something like an antibiotic, it is unacceptable to prescribe medications, such as SSRIs, on a long-term basis with no supervision or official medical records that can be reviewed by an underwriter. Generally, insurance companies will not offer individual disability coverage to anyone who self-prescribes. Insurance companies routinely perform prescription drug checks and will find out. Furthermore, having a co-resident/fellow or your spouse prescribe medication(s) with no official medical records is not looked upon any more favorably. You have probably heard the adage, “The man who represents himself has a fool for a client.” This is no different when it comes to disability insurance.

- Females (healthy or otherwise) when unisex rates are available. This rate structure typically reduces their premium rates by 40%-50% off the normal female rates. Additionally, if the base policy includes an increase option, all increases made to their coverage using this rider will also include unisex rates. Currently, Standard, Ameritas, and MassMutual offer unisex rates as part of their GSI plans. Some but not all Ohio National GSI plans also include unisex rates.

While the insurance companies that offer GSI plans vary from one institution to another, at the time of this writing, here is a partial list of hospitals that offer them:

- NYU Langone Health

- Albany Medical Center

- Stony Brook University Hospital

- Johns Hopkins

- University of Maryland Medical Center

- Baylor College of Medicine

- University of Washington

- Medical University of South Carolina (MUSC)

- The University of Arizona – Tucson and Phoenix

- Eastern Virginia Medical School (EVMS)

- The Ohio State University Wexner Medical Center

- University of Louisville

- Duke University Medical Center

- Vanderbilt University Medical Center

- Washington University in St. Louis

- Medical College of Wisconsin

- University of Iowa

- University of Kentucky

- Rutgers University

- Mountain Area Health Education Center (MAHEC)

There are many others. It is wise to check with your insurance professional to see if one is available through your training program, as the GME office itself may not know they exist.

Agents that specialize in the “medical market” should be familiar with these offerings—even if they cannot offer them directly. They should be willing to refer you to the “Endorsed” Agent to request illustrations of coverage and/or start the application process.

GSI plans are available from 60-180 days after the completion of residency or fellowship. Therefore, even if you graduated, you may still be able to take advantage of this offering.

Are 2 Policies Better Than One?

If you are in a high-income specialty and your earning potential exceeds the maximum monthly benefit under a GSI plan, you may consider supplementing the GSI plan with another medically underwritten plan, if you qualify—even if it may contain exclusion riders based upon your medical history.

For example, if you are limited to a $5,000 monthly benefit as a resident/fellow and the GSI plan’s maximum monthly benefit is $10,000 ($5,000 base policy plus a $5,000 increase option), you may want to purchase $4,000 per month under the GSI plan and another policy for $1,000 per month using medical underwriting. In many cases, this $1,000-per-month policy can potentially reach $20,000-$30,000 per month on its own. This strategy will allow you to potentially replace a larger percentage of your income in the future.

Understanding the Definition of Total Disability

Typically, “total disability” or “totally disabled” means that, due to an accident or illness, you are not able to perform the “material and substantial” duties of your occupation. Some companies—including Berkshire, Standard, Ameritas, and Ohio National—will even go so far as to state that if you have limited your practice to a single medical specialty, that specialty will be deemed to be your occupation. This definition of total disability makes it possible for you to work in another occupation or medical specialty and still receive your full disability benefits—even if you are earning the same or more income than you were prior to your disability.

Understanding Berkshire’s (Guardian) Enhanced True Own Occupation Definition

Many physicians do not understand Berkshire’s Enhanced Medical Specialty definition of total disability. In fact, I receive large numbers of calls and emails from those in certain medical specialties—such as Pathology, Pain Management, and Gastroenterology—asking if it even applies to them.

The first thing to remember is that Enhanced True Own Occupation protection for medical doctors (MDs) and doctors of osteopathy (DOs) starts with a true Own Occupation definition of Total Disability. That means that if the policyholder is deemed totally disabled, they would receive their full disability benefits even if they are gainfully employed in another occupation or capacity.

More Ways to Qualify for Benefits

While totally disabled in your own occupation, there may be instances where you can even work in your own business or practice and still collect a full benefit if:

More than 50% of your income is earned from performing surgical procedures, you will be considered totally disabled even if you are gainfully employed in your practice or another occupation so long as, solely due to injury or sickness, you are not able to perform surgical procedures

OR

more than 50% of your income is earned from performing hands-on patient care, you will be considered totally disabled even if you are gainfully employed in your practice or another occupation so long as, solely due to injury or sickness, you are not able to perform hands-on patient care.

For example, if you are an Orthopedic Surgeon and you see patients in clinic, read X-rays, interpret data, promote referrals, perform surgery and post-op follow-up, you would be deemed to be a surgeon by all the carriers above if your primary office duties are incidental to the fact that you are a surgeon.

However, let's say you were in a hybrid specialty like Ophthalmology, Urology, OB/GYN, and Otolaryngology, where you saw patients for both medical management and surgery. Now, it becomes more complicated as you are really acting as both a clinician and a surgeon. Here is where Berkshire's Enhanced Medical Specialty Definition may work well.

In these situations, if at the time of disability more than 50% of your income is earned from performing surgical procedures, you may be considered totally (and not partially) disabled if you could no longer perform those procedures.

The same might be true of a Surgical Critical Care Physician that can no longer perform surgery due to an accident or sickness and now works full-time as a Critical Care Physician. If more than 50% of your income is earned from performing surgical procedures, the insured may be considered totally (and not partially) disabled if they could no longer perform those procedures.

This might work for those who are working as a physician but also have side gigs. For example, you're an Emergency Medicine Physician and a blogger. If more than 50% of your income was derived from emergency medicine (performing “hands on” patient care) and you could no longer practice medicine but subsequently blogged on a full-time basis, even if you earned more income than you did as an Emergency Medicine Physician, you would still be deemed totally disabled.

All other carriers would have paid partial benefits unless the loss of income in any given month was more than 75% or 80% compared to your pre-disability income. The same is true for those that might lecture for pharmaceutical companies, be the director of a medical spa, or do consulting and/or medical/legal work.

In summary, the Enhanced Medical Specialty Definition of total disability can only help and never hurt an insured. However, if the sole reason someone is considering the purchase of Berkshire (Guardian) is for this definition, I suggest they consider the overall cost and benefits of how Berkshire's policy compares to others.

Short of what I described above, unless the cost difference was minimal, I would find it difficult to justify the purchase of their policy solely based upon their Enhanced Medical Specialty definition of total disability.

The More Things Change, the More They Stay the Same

Several years ago, a well-known mutual insurance company introduced the Medical Occupation Definition (MOD) of total disability. A few years later, that same carrier revised it and created the Medical Own Occupation Definition of total disability (MOOD). The bottom line is that despite how either definition reads on the surface, if you worked in another occupation, any earnings would be taken into consideration. A calculation is then made by the insurance company to determine the benefit that may be payable, if any.

This same company recently announced it will be changing things again later this year. While the base policy will contain a Modified Own Occupation definition, the policyowner can select a buy-up option to include a True Own Occupation definition of total disability or a Medical True Own Occupation definition of total disability.

So, why the change of heart—after 25 years?

The Medical Own Occupation definition caps the benefit payable for total disability at the insured’s loss of earned income when the insured is working in an occupation other than the regular occupation.

To illustrate this point, here's an example of an Orthopedic Specialist earning $500,000 annually ($41,667 per month) that purchased a policy with a monthly benefit of $15,000. This physician is subsequently disabled and unable to do any physician duties but chooses to work in a new (non-medical) field.

As a result, they earn $400,000 ($33,333 month) and their monthly benefit is reduced from $15,000 to $8,334 ($41,667 per month minus $33,333) since loss of income is < full benefit (post-disability earnings plus monthly benefit cannot exceed pre-disability income).

To further prove their point, it states that while totally disabled, you would need to earn at least $320,000 of annual income in a new occupation ($26,667 per month plus the $15,000 per month benefit = $41,667 per month) to receive more benefits under a True Own Occupation definition compared to a policy with a Medical Own Occupation Definition (MOOD) of total disability and that 50% of all medical specialties pay less than $320,000.

Finally, it asks, “How likely are you to earn among the highest of incomes in a different specialty or occupation while totally disabled from your specialty” (naming the Medscape Physician Compensation Report 2018 as its source)?

If the above example seems complicated, it is! Why would you want to purchase a policy with a definition of total disability with this many moving parts requiring ongoing calculations?

True Own Occupation and Medical True Own Occupation do not include this cap. The removal of this cap is the only difference between the currently available Medical Own Occupation definition and the new Medical True Own Occupation definition.

True Own Occupation Option

Total Disability or Totally Disabled

The words “Total Disability” or “Totally Disabled” mean the Insured is unable to perform the substantial and material duties of the Regular Occupation. If the Insured can perform one or more of the substantial and material duties of the Regular Occupation, the Insured is not Totally Disabled; however, the Insured may qualify as Partially Disabled.

Medical True Own Occupation Option

Total Disability or Totally Disabled

The words “Total Disability” or “Totally Disabled” mean the Insured is unable to perform the substantial and material duties of the Regular Occupation. If the Insured can perform one or more of the substantial and material duties of the Regular Occupation, the Insured will be considered Totally Disabled if:

- The Insured is not gainfully employed in an occupation;

- More than 50% of the Insured's time in the Regular Occupation at the time Disability began was devoted to providing direct patient care and services; and

- The Insured is unable to perform the substantial and material duties which accounted for more than 50% of the Insured's charges for direct patient care and services as evidenced by the billing codes for the 12 months before the Disability began.

If the Insured can perform one or more of the substantial and material duties of the Regular Occupation and is not considered Totally Disabled, the Insured may qualify as Partially Disabled.

Billing codes mean codes that are generally accepted by the healthcare and insurance industries, such as the Current Procedural Terminology (CPT) or American Dental Association (ADA), that are used to identify and describe medical, surgical, diagnostic, or dental services directly performed by the Insured.

If the Medical Occupation Definition of total disability (MOD) or the Medical Own Occupation Definition (MOOD) was far superior to what the other carriers offered, why introduce something thought to be inferior? Is something old suddenly something new again?

After all, the marketing materials stated that they provided more flexibility to qualify for benefits in more situations because you can continue working or stop working and be eligible to receive benefits. By contrast, typical partial disability definitions include a work requirement to be considered eligible to receive benefits.

The Bottom Line

In my opinion, you should not only look at the definition of total disability but other areas and potential pitfalls this policy may still contain. These might include the following:

- It is Guaranteed Renewable (not Non-Cancellable and Guaranteed Renewable)

- It has a limited Transition Benefit (Recovery Benefit) of only 12 months

- It has a limitation for claims resulting from mental/nervous and substance abuse disorders

Dividends, which are not guaranteed, are being touted to reduce the cost since, in many cases, it is more expensive compared to other companies. In the past, this insurance company has reduced or even eliminated dividends for those in certain medical occupations or states. Therefore, when comparing it to other policies, it is best to focus on the guaranteed premium, not taking the dividends into consideration at all.

Disability Insurance for an Independent Contractor or When Starting Your Own Practice

If you previously worked for a large practice, a multi-specialty clinic, or a hospital, you were likely provided with or offered some type of Long-Term Disability (LTD) insurance coverage. However, as an independent contractor, you are responsible for your own benefits including disability insurance, health insurance, and retirement benefits.

Without a guaranteed salary, insurance companies have no way of knowing what you will earn initially and what your expenses will be for running your practice. Without one year of earnings history, insurance companies will typically use 75% of your prior income when you were an employee and allow you to purchase up to a maximum of $7,500 or $10,000 per month.

However, once you can document a larger income (after expenses but before taxes), you can then increase your coverage. This is typically done using a recent CPA-prepared Profit & Loss Statement or a federal income tax return.

Protect Your Practice and Yourself

In addition to disability insurance to protect your income if you are unable to work, there are other coverages available to protect you as a business owner.

Business Overhead Expense (BOE) Disability Insurance

If you are in private practice, and responsible for some or all the monthly expenses to keep your office open, you should strongly consider purchasing a Business Overhead Expense (BOE) disability insurance policy. BOE insurance is a cost-effective way to ensure that your business can meet its ongoing expenses during a period of disability by reimbursing the owner(s) up to 100% of the normal ongoing business expenses incurred during a disability, including items such as:

- Rent

- Electricity

- Telephone

- Heat

- Water

- Laundry, janitorial, and maintenance services

- Employee salaries

- Employee benefits

- Real estate taxes

- Property, liability, and malpractice insurance

- Interest on debt

- Depreciation

- Rent or lease expense of furniture or equipment

- Legal and professional services

- Professional, trade, and association dues

- Licensing fees

- Billing and collection fees

- Other tax-deductible business expenses

- Salary for your replacement (depending upon insurance carrier)

In addition, some policies may even offer riders to help cover the salary of a replacement hired to continue the services of a disabled physician or to cover business loans.

Business Loan Protection Rider

The Business Loan Protection (BLP) Rider provides reimbursement for a monthly business-related loan obligation in the event of an insured’s total disability.

Items commonly covered include:

- Purchase of a practice or existing business

- Purchase of expensive equipment

- Expansion of the business of practice

- Facility renovations and improvements

- Purchase of a disability used solely for the business

For example, Principal’s BLP Rider termination date is based upon the end of the financial obligation with a minimum of three years, up to a 30-year maximum, but it may not exceed the loan termination date or the age 65 policy anniversary of the Disability Overhead Expense policy.

Since the BLP coverage can be issued on a stand-alone basis or in conjunction with a Disability Overhead Expense policy, it can be a great way to purchase a higher level of overall coverage. It can also work well when a bank requires this type of coverage prior to being approved for a loan.

Types of loans typically not covered are investment loans (loans taken out solely to finance an investment; they are not eligible loans because the proposed insured is not actively working on a full-time basis in the business), lines of credit, credit cards, revolving lines of credit, and interest only or family loans.

Most insurance companies will cover monthly expenses up to $50,000 and will pay for up to 30 months. The rationale is that after 30 months, if you are not back to work, you would look to sell or close the practice and no longer have ongoing expenses. There is coverage available above $50,000 with special risk insurers, like Lloyd’s of London, to supplement the traditional market with monthly benefits of more than $250,000.

Premium payments for Overhead Expense insurance are tax-deductible as a reasonable and necessary business expense (Rev. Rul 55-264, 1955-1 C.B. 11). As such, benefits received during disability, while taxable upon receipt, are used to pay practice-related expenses, which are tax-deductible. The net tax result is a “wash,” so the net tax impact is neutral.

All Agents Are Not Created Equal

There is no shortage of insurance agents and/or financial advisors who want to work with physicians. Unlike medicine—which has a standardized path that physicians must take to gain the education, training, and experience requirements necessary to obtain board certification—the insurance and financial services industry does not. Since the industry is heavily regulated, you will not be paying anything more by purchasing your policy from an “experienced” insurance agent than you will be by purchasing your policy from a newly licensed or “inexperienced” agent.

No Hippocratic Oath

In its original form, the Hippocratic Oath requires new physicians to swear, by several healing gods, to uphold specific ethical standards. Unlike medicine, the insurance and financial services industry does not have something similar.

One approach the industry uses is the CFP Board’s Code and Standards, which became effective on October 1, 2019, and has been enforced by the CFP Board of Ethics since June 30, 2020. If you are dealing with a CERTIFIED FINANCIAL PLANNER™ professional, a CFP® professional makes a commitment to the CFP Board to act in the best interest of their clients—not just during the financial planning process but at all times when providing financial advice.

Keep in mind, the CFP® Board is not a regulatory body and the CFP® professional himself/herself makes the commitment and not the insurance companies. This is different compared to being governed by a regulatory body—such as Financial Industry Regulatory Authority (FINRA), a self-regulatory organization (SRO) that operates under the U.S. Securities and Exchange Commission (SEC), which is a federal government agency. While both agencies protect investors, FINRA primarily regulates broker-dealers and their agents. The SEC regulates Registered Investment Adviser firms and their investment adviser representatives, and it has broad authority over securities markets.

Those who conform to the suitability standard are required to make a suitable recommendation, given the client’s age, goals, resources, and other factors. The concept of a fiduciary standard is to help protect consumers who make important financial and life decisions with the assistance of individuals who are contractually held to the standard. The fiduciary duty in the Code and Standards is designed to help raise the bar for the profession and benefit the public. If you are dealing with an insurance agent who also has their CFP® certification, this might help you feel more confident in any decisions you might make.

Requesting Illustrations of Coverage from Multiple Agents

Doing your due diligence prior to purchasing disability insurance is important. While contacting multiple agents makes sense as their personalities and experience levels may vary, requesting illustrations from every agent on WCI's Recommended Agent List is extreme.

While you might think competition is good and agents will be excited to compete for your business, the opposite is probably true. In fact, if agents are aware of this, they may become discouraged from working with you at all or they will simply provide illustrations of coverage with stripped-down benefits to make their premium rates appear lower.

In my opinion, you will be much better served by contacting one or two agents you might want to work with and allow them to put together a customized plan for you based on your individual needs, goals, budget, and specific situation. Limiting your choice of agents will also save you (and them) a substantial amount of time and effort.

When interviewing them, you should immediately ask if they have access to unisex rates, exclusive discounts, and/or Guaranteed Standard Issue (GSI) plans where you work.

At the end of the day, if all agents design the policies the same way, the pricing will be the same.

Parting Thoughts

Your ability to earn an income is your most valuable asset. It allows you to repay your debt, accumulate wealth, and create a lifestyle for yourself and your family. With significant income potential at risk, a long-term disability may leave you financially devasted. Don’t take the purchase of disability insurance lightly—your entire financial future may one day depend on it.

1 Not available for policies with a Graded Lifetime Rider or that do not include a partial disability rider. These are the personal views of the author and may not represent the views and opinions of The Guardian Life Insurance Company of America or its subsidiaries or affiliates thereof. Material discussed is meant for general informational purposes only and is not to be construed as tax, legal, or investment advice. Although the information has been gathered from sources believed to be reliable, please note that individual situations can vary. Therefore, the information should be relied upon only when coordinated with individual professional advice. Individual disability income products underwritten and issued by Berkshire Life Insurance Company of America (BLICOA), Pittsfield, MA. BLICOA is a wholly owned stock subsidiary of The Guardian Life Insurance Company of America (Guardian), New York, NY. Product provisions and availability may vary by state. Optional riders are available for an additional premium. Some policy benefits and features are not available to all occupations. Guardian, its subsidiaries, agents, and employees do not provide tax, legal, or accounting advice. Consult your tax, legal, or accounting professional regarding your individual situation.

Registered Representative and Financial Advisor of Park Avenue Securities LLC (PAS), 355 Lexington Avenue, 9th Floor, New York, NY 10017-6603, 212-541-8800. Securities products and advisory services are offered through PAS, 1-516-677-6200. Financial Representative, The Guardian Life Insurance Company of America, New York, NY (Guardian). PAS is a wholly owned subsidiary of Guardian. Physician Financial Services is not an affiliate or subsidiary of PAS or Guardian. AR Insurance License #1057229, CA Insurance License #0C37340. PAS is a member FINRA, SIPC. 2022-143645 Exp. 09/2024

[Editor's Note: Many thanks to Larry Keller of Physician Family Services, one of our Platinum Level (contributing $8,000+) Sponsors, and his long-time relationship with WCI supporting the scholarship and helping physicians secure the best DI policies for their unique needs. Larry is a long-time advertiser and is on our list of Recommended Insurance Agents, and he's been helping physicians with their DI needs since 1990. Physician Family Services is a New York-based firm specializing in income protection and wealth accumulation strategies for physicians. Larry can be reached at (516) 677-6211 or by email at [email protected] with comments or questions. This is the fourth of our five scholarship-sponsored posts for 2022. Thank you for supporting those who support this site and especially the scholarship. All proceeds go to the scholarship winners.]

The post Disability Insurance: Your Health Is Your Wealth appeared first on The White Coat Investor - Investing & Personal Finance for Doctors.

||

----------------------------

By: Josh Katzowitz

Title: Disability Insurance: Your Health Is Your Wealth

Sourced From: www.whitecoatinvestor.com/disability-insurance-your-health-is-your-wealth/

Published Date: Sat, 24 Sep 2022 06:30:19 +0000

Read More

.png) InvestingStocksToolsClubsVideosPrivacy PolicyTerms And Conditions

InvestingStocksToolsClubsVideosPrivacy PolicyTerms And Conditions