<iframe style="width:120px;height:240px;" marginwidth="0" marginheight="0" scrolling="no" frameborder="0" src="//ws-na.amazon-adsystem.com/widgets/q?ServiceVersion=20070822&OneJS=1&Operation=GetAdHtml&MarketPlace=US&source=ss&ref=as_ss_li_til&ad_type=product_link&tracking_id=peaceinvesting-20&language=en_US&marketplace=amazon®ion=US&placement=0060555661&asins=0060555661&linkId=80f8e3b229e4b6fdde8abb238ddd5f6e&show_border=true&link_opens_in_new_window=true"></iframe>|<iframe style="width:120px;height:240px;" marginwidth="0" marginheight="0" scrolling="no" frameborder="0" src="//ws-na.amazon-adsystem.com/widgets/q?ServiceVersion=20070822&OneJS=1&Operation=GetAdHtml&MarketPlace=US&source=ss&ref=as_ss_li_til&ad_type=product_link&tracking_id=peaceinvesting-20&language=en_US&marketplace=amazon®ion=US&placement=1119404509&asins=1119404509&linkId=0beba130446bb217ea2d9cfdcf3b846b&show_border=true&link_opens_in_new_window=true"></iframe>|<iframe style="width:120px;height:240px;" marginwidth="0" marginheight="0" scrolling="no" frameborder="0" src="//ws-na.amazon-adsystem.com/widgets/q?ServiceVersion=20070822&OneJS=1&Operation=GetAdHtml&MarketPlace=US&source=ss&ref=as_ss_li_til&ad_type=product_link&tracking_id=peaceinvesting-20&language=en_US&marketplace=amazon®ion=US&placement=1119376629&asins=1119376629&linkId=2f1e6ff64e783437104d091faaedfec7&show_border=true&link_opens_in_new_window=true"></iframe>

By Dr. Jim Dahle, WCI Founder

Settling up a Backdoor Roth IRA can be confusing, so I thought I’d put together a tutorial on the steps people can refer to when they go through this process. Let's get started.

Table of Contents

- What Is a Backdoor Roth IRA?

- Who Should Do a Backdoor Roth IRA?

- When to Do a Backdoor Roth IRA?

- Backdoor Roth IRA Pros and Cons

- Backdoor Roth IRA Tax Implications

- Backdoor Roth IRA Steps

- How to Fix and Prevent Backdoor Roth IRA Mistakes

- How to Report a Late Backdoor Roth (i.e., When You Contribute the Following Year)

- Recharacterizations: The Fix for When You Should Have Backdoor Rothed but Didn't

- Backdoor Roth IRA FAQs

What Is a Backdoor Roth IRA?

Despite its name, a Backdoor Roth IRA is not an account; it is a process with two steps:

- Contribute to a Traditional IRA.

- Complete a Roth conversion.

If you understand the rules of both of these steps, putting them together is no problem.

Who Should Do a Backdoor Roth IRA

Remember that if you are a low earner you can just contribute DIRECTLY to a Roth IRA and skip this Backdoor Roth IRA process.

Roth IRA Limits and Conversion Rules

Low earner is defined as a Modified Adjusted Gross Income (MAGI) under a phaseout range in 2024 of $146,000-$161,000 ($230,000-$240,000 Married Filing Jointly). Some docs—like residents, employee dentists, part-timers, and even some medical attendings in the lower-paying specialties who are married to a non-earner—can just contribute to a Roth IRA directly.

Anyone who earns at least $7,000 ($8,000 if 50+) can contribute $7,000 ($8,000 if 50+) to an IRA [2024]. If your income is below a MAGI of $146,000-$161,000 ($230,000-$240,000 Married Filing Jointly), you can contribute directly to a Roth IRA. If you have a retirement plan offered to you at work and your MAGI is below $77,000-$87,000 ($123,000-$143,000 Married Filing Jointly), you can deduct your traditional IRA contributions. Since most readers of this blog have a retirement plan through their job and have (or soon will have) a MAGI over $240,000, they will find that they can't make direct Roth IRA contributions or deduct their traditional IRA contributions. Thus, their best IRA option is the Backdoor Roth IRA process, i.e., an indirect Roth IRA contribution.

Spousal IRAs

Married physicians should be using a personal and a spousal Roth IRA, and you will usually need to fund both indirectly (i.e., through the Backdoor). This provides an additional $7,000 each ($8,000 for each spouse that is 50+) of tax-protected and (in most states) asset-protected space per tax year, and it allows for more tax diversification in retirement. Tax diversification allows you to determine your own tax rate as a retiree by deciding how much to take from tax-deferred (traditional) accounts and how much from tax-free (Roth) accounts. Remember that IRA stands for INDIVIDUAL Retirement Arrangement, so even if the pro-rata rule (discussed below) keeps you from doing the Backdoor Roth IRA, it doesn't necessarily keep your spouse from doing so. Each spouse reports their Backdoor Roth IRA on their own separate 8606, so the tax return for a married couple doing Backdoor Roth IRAs should always include two Form 8606s.

Married Filing Separately

The contribution and deduction income limits are particularly low if you are filing your taxes Married Filing Separately (MFS). Both the ability to contribute directly to a Roth IRA and the ability to deduct a traditional IRA contribution if you (or your spouse) are eligible for a retirement plan at work phase out between $0 and $10,000. Basically, the best option for anyone filing their taxes MFS is the Backdoor Roth IRA process, i.e., an indirect Roth IRA contribution.

There is an exception to these rules if you do not actually live with your spouse. In that case, your ability to contribute directly to a Roth IRA phases out between a MAGI of $146,000-$161,000 in 2024. If you live separately and are not covered by a retirement plan at work, you can deduct a traditional IRA contribution no matter your income. You can still do a Backdoor Roth IRA process in these situations where your IRA contribution is either partially or completely deductible. The tax bill will be precisely the same: $0 when done properly. However, instead of having no tax cost for either the contribution or the conversion, your deduction on the contribution will precisely equal the tax cost on the conversion, resulting in that same $0 tax bill for the entire process.

Mega Backdoor Roth IRA

A Mega Backdoor Roth IRA is completely different from a regular Backdoor Roth IRA. Despite its name, you actually do a Mega Backdoor Roth IRA with a 401(k), not an IRA. It requires a 401(k) that accepts both after-tax (not Roth) employee contributions and allows for either in-service withdrawals (and thus conversions to a Roth IRA) or, more commonly, in-plan conversions. Using the Mega Backdoor Roth IRA process, one could put as much as $69,000 ($76,500 if 50+) [2024] per year into a Roth 401(k) (or possibly a Roth IRA in addition to your usual $7,000-$8.000 contribution). However, this process has nothing to do with the Backdoor Roth IRA process we are discussing in this post.

When to Do a Backdoor Roth IRA

Lots of people wonder about the timing of a Backdoor Roth IRA.

IRA Contribution Deadline

There is really only one deadline to meet with the Backdoor Roth IRA process. IRA contributions for a given tax year must take place between January 1 of the tax year and April 15 (even if you file an extension) of the following year.

Backdoor Roth IRA Conversion Deadline

The conversion step may take place at any time. It can take place the next day or even the same day as the contribution. I don't recommend it, but you can wait months, years, or even decades between the contribution and the conversion step. There is no deadline for Roth conversions. If you need to perform a rollover or a conversion of a traditional, rollover, SEP, or SIMPLE IRA in order to avoid the pro-rata rule, you have until December 31 of the year you do the conversion step.

When Should You Contribute and Convert?

You should do both steps as soon as possible. Many white coat investors do the IRA contribution step and the Roth conversion step the first week of January each year. This maximizes the amount of tax-free compounding that can occur on those dollars. Minimizing the time between contribution and conversion and doing both steps within the calendar year is not required, but it certainly simplifies the paperwork.

Want to really make your paperwork complicated? Contribute to your IRA each month and convert it each month. Then, you have 12 contributions and 12 conversions to keep track of each year. Seriously, though, if you make enough money that you have to contribute to your Roth IRA(s) through the Backdoor Roth IRA process, you make enough to do it at one time each year.

Can I Do a Backdoor Roth IRA Every Year?

Yes. My wife and I have done one every year since 2010 and do not plan to stop until we no longer have any earned income. It is just one of the investment chores we perform once a year.

5-Year Rule

One factor that may push you to do a Backdoor Roth IRA earlier is the five-year rule. Now, there are at least three five-year rules related to IRAs, but the main one to pay attention to here is the five-year rule after a Roth conversion. This rule determines whether the withdrawal of principal from the account prior to age 59 1/2 will be penalty-free. The five-year period starts on January 1 of the year you do the conversion, so it could be a little less than five years. Roth IRA principal generally comes out tax- and penalty-free (it is only the earnings that may be subject to penalties), but that is only the case after the five-year rule has been fulfilled.

In essence, if you do a conversion of a Roth IRA at age 51, you can then withdraw the principal tax- and penalty-free starting at age 56 rather than age 59 1/2. This can provide funding for living expenses to early retirees. If you do a Roth conversion at age 57, you still get access to that principal (and earnings) tax- and penalty-free at age 59 1/2. So, it's five years or age 59 1/2, whichever comes first.

There is also a completely separate five-year rule on IRA contributions, but this starts from the time you make your very first IRA contribution, not every contribution, so it should not apply to most early retirees.

Backdoor Roth IRA Pros and Cons

There are a lot of great things about the Backdoor Roth IRA, but it isn't all peaches and cream.

Pros of Backdoor Roth IRA

The main benefit of a Backdoor Roth IRA is that it provides you with another retirement account. Via the Backdoor Roth IRA process, you can continue to contribute to a Roth IRA even after your earnings rise above the income limit for direct Roth IRA contributions. Retirement accounts eliminate the tax drag that applies in a taxable, or non-qualified account, reducing your taxes and allowing your investment to grow at a higher rate so you can reach your goals sooner.

How much can that tax protection be worth compared to a taxable account? It depends on the return of the underlying investment, its tax efficiency, and the amount of time the money is left in the account. At my marginal tax rate, $10,000 earning 8% in a tax-inefficient investment over 50 years would grow to $469,000 in a Roth IRA but only $88,000 in a taxable account. More realistically, over 30 years, the use of a Roth IRA vs. a taxable account for a tax-efficient investment would still result in 29% more money.

Retirement accounts ensure simple estate planning. By using beneficiaries, that money does not go through the probate process, so your heirs get it sooner with less hassle, more privacy, and no cost. They can even stretch the tax-protected growth benefit for another decade after they inherit the account. Retirement accounts like a Roth IRA also provide substantial asset protection in most states, meaning that in the admittedly very rare event of a dramatically above-policy limits judgment that isn't reduced on appeal, you can declare bankruptcy and still keep what is in your retirement accounts. Roth money is tax-free forever, so by continuing to contribute each year, you can increase tax diversification in retirement.

Cons of Backdoor Roth IRA

Roth IRAs, even when you contribute via the Backdoor Roth IRA process, are still retirement accounts with all of their downsides. Retirement accounts limit the investments you can put in them and prohibit the use of margin investing. If you withdraw Roth IRA earnings prior to age 59 1/2 without an approved exception, you will owe a 10% penalty.

Due to the pro-rata rule (see below), the Backdoor Roth IRA process requires you to either convert or roll over into a 401(k) any traditional IRAs, SEP-IRAs, and SIMPLE IRAs you may have. If you have self-employment income, you will need to use a solo 401(k) instead of a SEP-IRA to shelter that income from taxes. Doing Backdoor Roth IRAs each year also adds one form (IRS Form 8606) per spouse to your tax return. If preparing your own taxes using tax software, it can be tricky to ensure the software reports the process correctly. If you do a Backdoor Roth IRA instead of (rather than in addition to) maxing out your tax-deferred accounts during your peak earnings years, that can also be a mistake that results in the accumulation of less money.

Perhaps most significantly, there are now two steps to getting money into your Roth IRA each year instead of just one. While I think the process is pretty darn simple, I am continually amazed at all of the unique ways that doctors manage to screw it up. Later in this article, I'll show you how to fix all of those screwups.

Is a Backdoor Roth IRA Worth It?

Yes! Most of the time. It really is just a little bit of hassle to do each year, although there may be some additional hassle the first year if you need to take care of another IRA first to avoid the pro-rata rule. There may be times when someone has a large traditional IRA they cannot afford to convert to a Roth IRA and cannot roll over into a 401(k) because they don't have a 401(k) at all, their 401(k) charges high fees, or because the IRA assets are invested in something they cannot invest in within a 401(k). If your employer-provided retirement account is a SIMPLE IRA or a SEP-IRA, the Backdoor Roth IRA process is also probably not worth it. Finally, some multi-millionaires don't want to bother with even the minor hassle of the Backdoor Roth IRA process because getting an extra $7,000-$16,000 a year into Roth accounts just isn't going to move the needle for them.

Backdoor Roth IRA Tax Implications

Roth IRAs are all about avoiding taxation on earnings, so naturally, there are lots of tax implications of this process.

Pro-Rata Rule

The most important tax implication to be aware of is the pro-rata rule. I would estimate that 90%+ of Backdoor Roth IRA screwups involve the investor having his or her conversion pro-rated. When you report a Roth IRA conversion on IRS Form 8606 (see below), there is a pro-rata calculation made. The numerator is the amount converted. The denominator is the total of ALL traditional, rollover, SEP, and SIMPLE IRAs, but not 401(k)s, 403(b)s, 457(b)s, Roth IRAs, or inherited IRAs. Therefore, it is critical that you DO SOMETHING with any IRA balance you have PRIOR to December 31 of the year in which you do a Roth conversion of after-tax money. Later in this article, I'll describe the exact options you have for what to do with this money.

Tax on Backdoor Roth IRA Conversion

Done properly, there is NO tax on a Backdoor Roth IRA conversion. Zero. Nada. Zilch. While the money you put into a Roth IRA (indirectly via the Backdoor in this case) was taxed when you earned it, it is NOT taxed when you contribute it directly to a Roth IRA or when you contribute it as a non-deductible IRA conversion or when you subsequently convert that money to a Roth IRA. In fact, it is never taxed again.

Do I Need to Worry About the Step Transaction Doctrine?

There used to be a concern that the IRS would have a problem with the Backdoor Roth due to an IRS rule called The Step Transaction Doctrine. This rule basically says that if the sum of a bunch of legal steps is illegal, then you can’t do it. Some wondered if this Backdoor conversion from a Traditional IRA to Roth was a legal transaction considering this doctrine. Those concerns, valid or not, are no longer an issue. The IRS clarified in early 2018 that no waiting period is required between the contribution and conversion steps of the Backdoor Roth IRA. It has essentially given its blessing on the whole process. Waiting just makes things more complicated on the 8606, as discussed in Pennies and the Backdoor Roth IRA.

How to Report a Backdoor Roth IRA on TurboTax

Reporting the Backdoor Roth IRA properly on TurboTax is unfortunately even more complicated than filling out Form 8606 by hand. The key to doing it right is to recognize that you report the conversion step in the Income section but you report the contribution step in the Deductions and Credits section. Since you generally do the income section first, you report the conversion before you report the contribution, even though you actually did the contribution before the conversion. At the end, you want to look at the Form(s) 8606 that TurboTax generates, just like you would check up on one filled out by an accountant.

More information here:

How to Report a Backdoor Roth IRA on TurboTax

Backdoor Roth IRA Steps, Tutorials, and Walkthroughs

In this section, we'll explain exactly how to do the Backdoor Roth IRA process and how to report it on your tax return, whether you file on paper or using tax software. You can easily walk through these Backdoor Roth IRA steps at Vanguard, complete a Backdoor Roth at Fidelity, or knock out a Backdoor Roth IRA at Schwab, three of the most popular brokerage/mutual fund companies.

How to Perform and Report on Paper the Backdoor Roth IRA Process

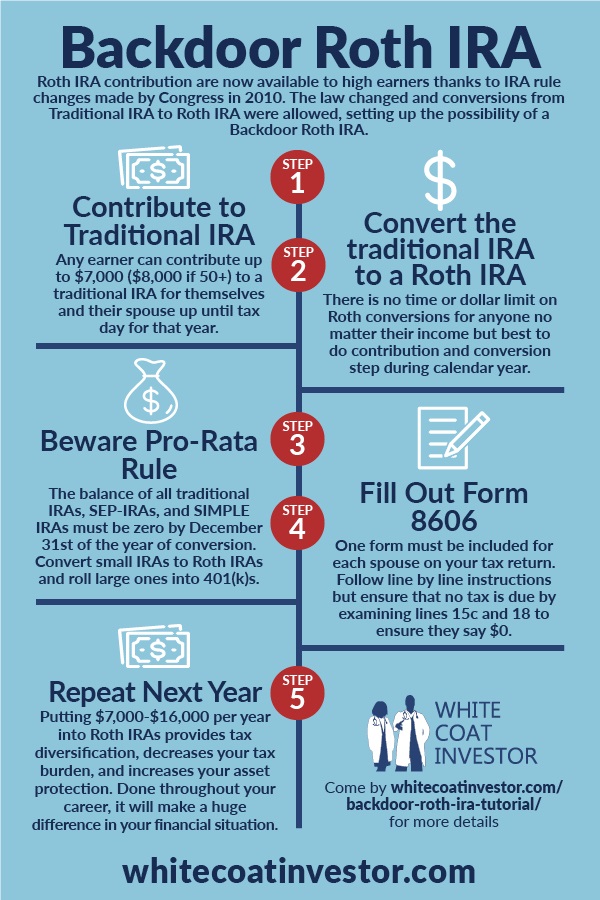

While it is really just a two-step process, it is best to think of it as a five-step process. These steps don't all have to be done in order (it might be easier to do Step 3 before Step 1), but they will all need to be done.

Step #1 Contribute to a Traditional IRA

Make a $7,000 ($8,000 if 50+) non-deductible traditional IRA contribution for yourself and one for your spouse. You can use the same traditional IRA accounts every year—they just spend most of the time with $0 in them. Most fund companies, including Vanguard, don’t close the account just because there is nothing in it. I do this every January 2.

Step #2 Leave the Money in Cash

An account like a traditional IRA is not an investment, of course; just like a suitcase isn't clothing. When putting money in a traditional IRA, you also have to tell the IRA provider how you want to invest. In this case, just leave the money in cash, whether a money market fund or a settlement fund. At Vanguard, the settlement fund is the Federal Money Market Fund. You really don't want to have any gains (or especially any losses) between the contribution and conversion step because it makes the paperwork more complicated. The best way to minimize the gains is to leave it in cash (and then of course to do the conversion as soon after contribution as possible to minimize the “pennies” issue).

Step #3 Convert the Traditional IRA to a Roth IRA

Next, convert the non-deductible traditional IRA to a Roth IRA by transferring the money from your traditional IRA into your Roth IRA at the same fund company. If you don’t already have a Roth IRA there, you’ll need to open one. This can be done in a minute or two online at Vanguard, and it is essentially the same process as opening the traditional IRA. I do this the very next day after I make the contribution. It is very straightforward. When you transfer the money, the website will throw up a scary banner saying something like “THIS IS A TAXABLE EVENT.” That’s true. It is taxable. But the tax bill will be zero since you’ve already paid taxes on the $7,000 and couldn’t claim your contribution as a deduction because you make too much money. You can do Step 3 basically immediately after Step 1. Some companies will let you do it the same day. Other companies will make you wait until the next day or even a week or so. But there is no reason to wait months to do it.

Step #4 Invest the Money

Now you will need to select an investment for the money in your Roth IRA. If you already have an investment in there, you can simply add $7,000 to it. Otherwise, you will need to select an investment in accordance with your written investing plan. If you do not have a written investing plan yet, you can leave the money in cash or put it into a Target Retirement 2050 fund or another lifecycle fund until you get that part of your financial plan worked out.

Step #5 Beware of the Pro-Rata Rule

Get rid of any SEP-IRA, SIMPLE IRA, traditional IRA, or rollover IRA money. The total sum of these accounts on December 31 of the year in which you do the conversion step (Step 2) must be zero to avoid a “pro-rata” calculation (see line 6 on Form 8606) that can eliminate most of the benefit of a Backdoor Roth IRA.

2024 contribution levels

You can get rid of these IRA accounts in three ways:

- Withdraw the money (not recommended, as the money would be subject to tax and/or penalties, not to mention DECREASING your tax-advantaged/asset-protected investment space).

- Convert the entire sum to a Roth IRA. Only recommended if it is a relatively small amount and you can afford to pay the taxes out of current earnings or taxable investments with relatively high basis.

- Roll the money over into a 401(k), 403(b), or individual 401(k). 401(k)s don’t count in the aforementioned pro-rata calculation. Some physicians even open an individual 401(k) at Fidelity, eTrade, or Vanguard (rollovers from traditional IRAs to solo 401(k)s is a recent addition to Vanguard) in order to facilitate a Backdoor Roth IRA.

Step #6 Fill Out IRS Form 8606 Correctly

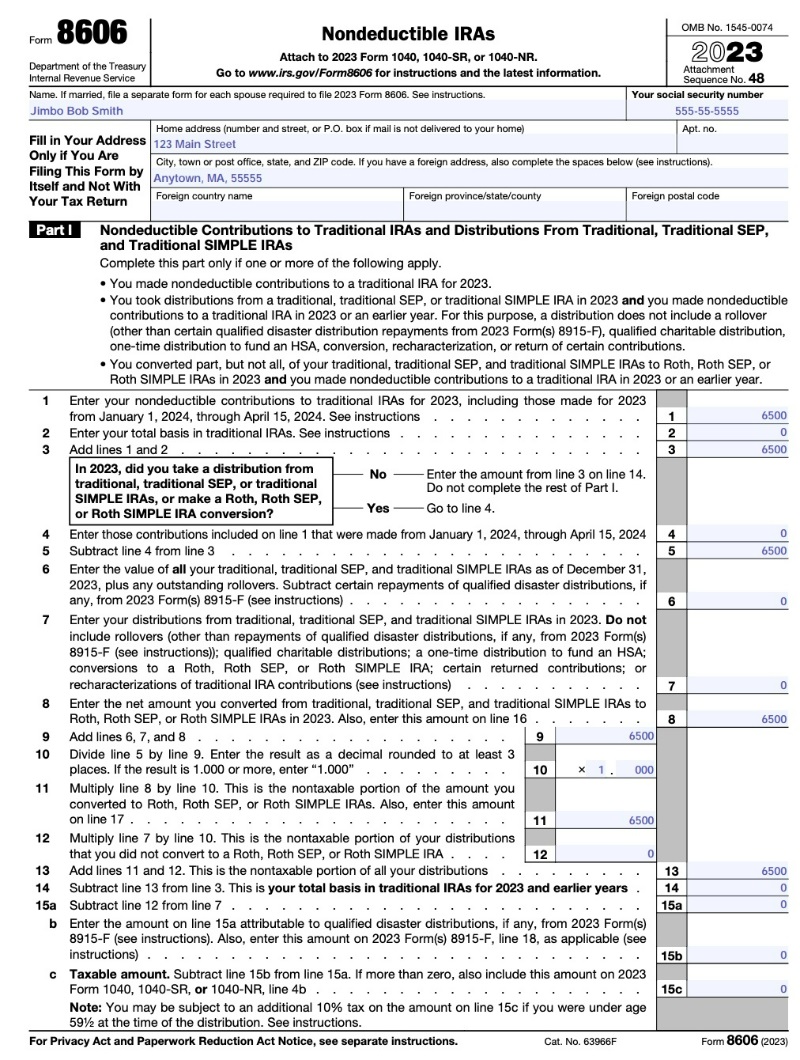

The next part of the Backdoor Roth IRA is done months later when you (or your accountant) fill out your IRS Form 8606 on your taxes. Don't forget to do it or there is a $50 penalty. Remember that you need one form for each spouse: INDIVIDUAL Retirement Arrangements. You need to double-check this to make sure it is done right, even if you hire a pro to avoid screwing up this part. Advisors have told me that they have had to help clients fix dozens of these that tax preparers have done improperly. If you don't do it right, you'll pay taxes twice on your Backdoor Roth IRA contribution.

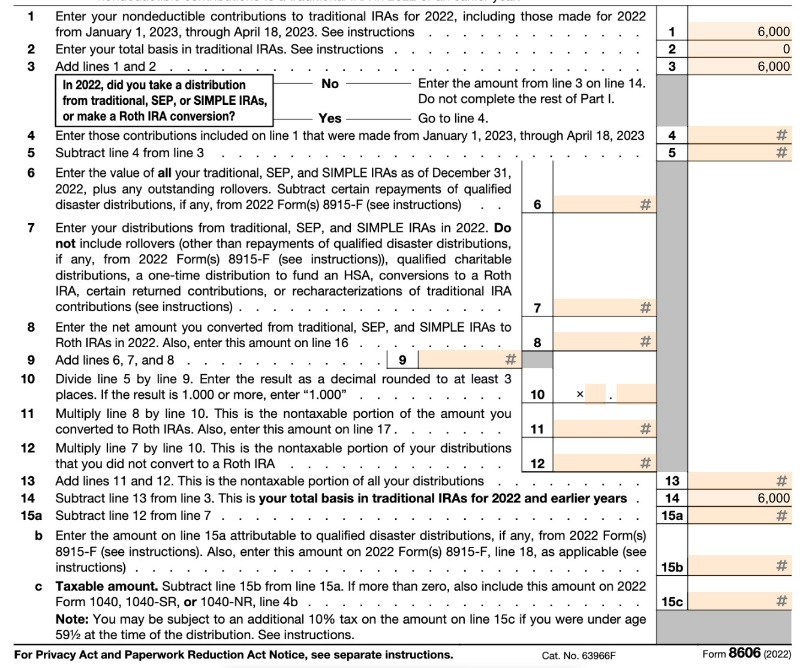

Page 1 (below) shows a “distribution” from your non-deductible IRA. Since the money was already taxed, the taxable amount on your distribution is zero. Line 1 is your non-deductible contribution. On Line 2, your basis is zero because you had no money in a traditional IRA on December 31 of last year (if you've been carrying a non-deductible IRA for years, this may not be zero). Line 6 is zero in a typical year. Note that TurboTax may fill this out a little differently (may leave lines 6-12 blank), but you end up with the same thing. Line 13 is the same as line 3, so the tax due is zero.

Here's an example from the 2023 version of Form 8606.

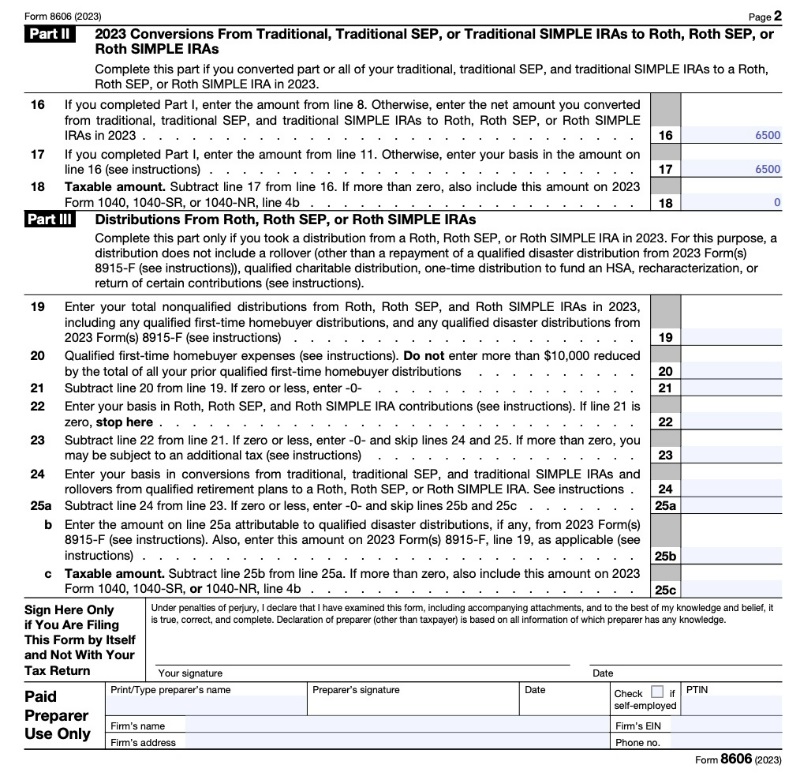

On page 2 (below), you are showing the Roth conversion. I'm not really sure why you have to do this twice (since you're just transferring the amounts from lines 8 and 11 and then subtracting them), but that's what the form calls for. As you can see, a Roth conversion of a non-deductible traditional IRA contribution without any gains is a taxable event; it's just that the tax bill is zero for it.

When double-checking your tax preparer's work, you want to concentrate on lines 2, 14, 15c, and 18, and make sure they're a very small amount, like zero, and not a very large amount, like $7,000. The form can get more complicated if you are doing other Roth conversions at the same time or if you made a contribution for the previous year (i.e., made your 2022 contribution in 2023). See below for more details.

Notice how there is no place on the form to put the date when you made the contribution or the date when you made the conversion. It isn't on the form your IRA custodian sends to the IRS (1099-R) either.

Do It All Again Next Year

You do not have to wait any period of time between the contribution and conversion. Each year, I make my Traditional IRA contribution on January 2, then convert it to a Roth IRA the next day or within a few days. That gets my investment money working as soon as possible and simplifies the record keeping. Vanguard won’t let you do it the same day (sometimes other providers will), so I have to wait one day anyway. Occasionally they'll make you wait up to a week. If you find you have a few pennies left in the account and are worried you'll get pro-rated, take a look at this post: Pennies and the Backdoor Roth IRA.

More information here:

How to Do a Backdoor Roth IRA with Vanguard

How to Do a Backdoor Roth IRA at Fidelity

How to Fix and Prevent Backdoor Roth IRA Mistakes

In this section, we're going to talk about how to fix and prevent common mistakes in the Backdoor Roth IRA process. To better organize these mistakes, we will break down the process into the six very clear steps used above and then will explain possible errors with each step and what to do about them.

6 Steps to Successfully Contribute to a Backdoor Roth IRA

- Step 1 – Contribute to traditional IRA ($7,000, $8,000 if 50+ for 2024).

- Step 2 – Invest the money in a money market fund.

- Step 3 – Move money from a Traditional IRA to a Roth IRA (i.e., a Roth conversion).

- Step 4 – Invest in your preferred investment (typically a stock, bond, or balanced index mutual fund).

- Step 5 – Ensure you have no money in a traditional IRA, SEP-IRA, or SIMPLE IRA on December 31 of the year you do the CONVERSION step.

- Step 6 – Report the transactions correctly on your taxes by filling out Form 8606.

Seriously. That's it. If you can do a cholecystectomy, you can do this. If you can work up a pulmonary embolus appropriately, you can do this. If you can manage hypertension well, you can do this. If you can fill a cavity, you can do this. Super easy.

However, people still manage to screw up on EACH of those six steps. Let's go through the mistakes people make, step by step.

How to Fix Backdoor Roth IRA Mistakes

Step 1 Error – Contributing Directly to a Roth IRA

An error that commonly occurs with a first Backdoor Roth IRA is that people simply don't realize that their income is too high to make a direct Roth IRA contribution. Instead of doing it indirectly (i.e., going through the Backdoor), which is no big deal even if you're under the limit, they contribute directly to a Roth IRA. Then they realize their Modified Adjusted Gross Income (MAGI) is over $146,000-$161,000 ($230,000-$240,000 Married Filing Jointly) for 2024. Now what?

Enter the Recharacterization

If you have made this error, now you have to recharacterize the Roth IRA contribution to a traditional IRA contribution. This basically makes it as though you never contributed to a Roth IRA but contributed to a traditional IRA instead. You usually have to call your IRA provider to get this done, but it's no big deal. In this section, I'll walk you through the details of how to do it.

You have until the due date of your tax return to do this (including extensions). So, if you made an IRA contribution in January of 2023 for the 2023 tax year, you have until October 15, 2024, to do a recharacterization. There's no penalty or anything to do it. You can do the opposite as well if you contributed to a traditional IRA but meant to contribute directly to a Roth IRA.

Bear in mind that starting in 2018, you can no longer do recharacterizations of Roth CONVERSIONS (not contributions). This eliminated the “Roth IRA Conversion Horserace” technique for tax reduction.

Until only a couple of years ago, I had thought there was a waiting period after a recharacterization to then reconvert the money to a Roth IRA. However, that rule was only for recharacterizations of conversions, not contributions. There has never been a waiting period for a recharacterization.

Any gains that occur before the final conversion are, of course, fully taxable at your ordinary income tax rate in the year of the final conversion.

The Income Limit

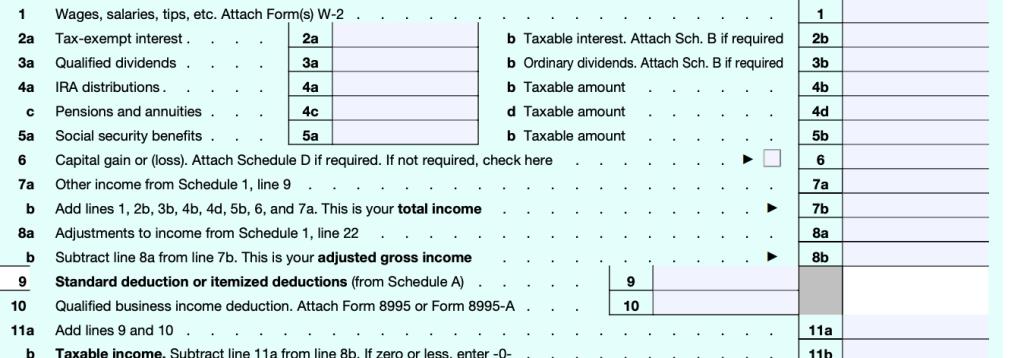

The first thing to determine is whether this post even applies to you. If your income is below a certain amount, you can just contribute directly to a Roth IRA. That amount depends on several things. First, it is a MODIFIED Adjusted Gross Income (MAGI). That number is very similar to your Adjusted Gross Income (AGI). Remember how tax Form 1040 works.

The first income line you come to is line 7b, your “Total Income.” When people think about income, this is generally what they think of. The third income line on the form is line 11b. This is your “Taxable Income.” This is what your tax bill is actually calculated from. It is basically your total income minus all of your deductions. In between those two, on line 8b, is another income, your “Adjusted Gross Income.” This is “the line” that people are talking about when they use the phrases “above-the-line deduction” and “below-the-line deduction.” If it comes out before your AGI is calculated, it is an above-the-line deduction. These are deductions such as self-employment tax, self-employed retirement plans, self-employed health insurance premiums, HSA contributions, student loan interest, alimony, tuition, and any IRA deductions. If it comes out after your AGI is calculated, it is a below-the-line deduction. These are EITHER your standard deduction OR your itemized deductions, like mortgage interest, state/local/property taxes, and charitable contributions. A MAGI is just a slight tweak to your AGI.

Below are the MAGI limits for direct Roth IRA contributions [2024]. If your MAGI is below the first number, you can just contribute to a Roth IRA directly. If your MAGI is over the second number, you cannot contribute at all. If your MAGI is between the two numbers, you can make a partial direct contribution (most shouldn't bother with this, just do it all through the Backdoor).

- Married Filing Separately (and lived with spouse for at least part of the year): $0-$10,000

- Married Filing Jointly: $230,000-$240,000

- Single or Head of Household: $146,000-$161,000

If you think you'll be anywhere close to that first number, do yourself a favor and just make your Roth IRA contribution indirectly, i.e., through the Backdoor (contribute to a traditional IRA and then convert that contribution to a Roth IRA). Since 2010, there has been no income limit on Roth conversions and there has never been an income limit on traditional IRA contributions, just your ability to deduct them.

How does a MAGI differ from an AGI? It's a very slight difference. Bear in mind that there are other MAGIs out there. We're only talking about the one that affects Roth IRA contributions here. But to get your MAGI, you simply take your AGI, subtract some income from it, and add back in some other income to it. The worksheet showing you how to do this is Worksheet 2-1 in Publication 590.

Basically, you subtract income from a Roth conversion and you add income from IRA deductions (not sure why you'd have this), student loan interest (if you are using this worksheet, you probably don't have this), tuition deduction (you probably don't have this), a couple of rare deductions for foreign income/deductions (you probably don't have these), some savings bond interest you probably don't have much of, and some employer-provided adoption benefits. For most people, your MAGI = your AGI since all of these deductions are pretty rare for the folks worried about this limit for direct Roth IRA contributions. So, focus on your AGI. That means if you contributed directly to a Roth IRA but late in the year realized you probably should not have, one easy fix is to get your AGI below that limit by contributing to an HSA or a self-employed retirement plan like an individual 401(k) or SEP-IRA. Note that giving a bunch of money to charity is NOT a solution to this problem because that is a below-the-line deduction.

How to Do an IRA Recharacterization

If you can't get your MAGI low enough, you will have to do an IRA recharacterization. As far as the IRS is concerned, a recharacterization is as though you never made the Roth IRA contribution at all but made a traditional IRA contribution instead. You don't report a recharacterization separately; you just report a traditional IRA contribution. Keep in mind as you read on the internet about recharacterizations that there used to be two types of them—a recharacterization of a Roth IRA CONTRIBUTION and a recharacterization of a Roth IRA CONVERSION. The second type was outlawed in 2018, but the first one, the one we're talking about today, is still perfectly legal. If you decide you want to undo a Roth conversion these days, you're simply out of luck. Here is how you do a recharacterization of a Roth IRA contribution:

- You tell Vanguard (or wherever your IRAs are) to recharacterize the Roth IRA contribution to a Traditional IRA contribution.

Yup. That's it. The brokerage takes care of the rest. You can read all about all of the rules in Publication 590 Chapter 1 if you want, but that's basically what they say. Don't believe me? Fine. Here are the IRS instructions:

How Do You Recharacterize a Contribution?

To recharacterize a contribution, you must notify both the trustee of the first IRA (the one to which the contribution was actually made) and the trustee of the second IRA (the one to which the contribution is being moved) that you have elected to treat the contribution as having been made to the second IRA rather than the first. You must make the notifications by the date of the transfer. Only one notification is required if both IRAs are maintained by the same trustee. The notification(s) must include all of the following information:

- The type and amount of the contribution to the first IRA that is to be recharacterized.

- The date on which the contribution was made to the first IRA and the year for which it was made.

- A direction to the trustee of the first IRA to transfer in a trustee-to-trustee transfer the amount of the contribution and any net income (or loss) allocable to the contribution to the trustee of the second IRA.

- The name of the trustee of the first IRA and the name of the trustee of the second IRA.

- Any additional information needed to make the transfer.

In most cases, the net income you must transfer is determined by your IRA trustee or custodian.

See what I mean? It's just a phone call. Any earnings that the account had in between the contribution and the recharacterization just go over with the contribution. No big deal.

You have until your tax filing date to do this. Most of the time, that's April 15 of the next year. However, the IRS is even more lenient than that. You actually can do this for an extra six months after your tax filing date, but you will have to refile your return.

Where Do You Report a Recharacterization?

If you hire somebody else to prepare your taxes, you can skip this section. If you do it yourself, you'll need to make sure you report this correctly. According to Pub 590, you report it on our old friend Form 8606.

Pub 590 says this:

Actually, that's really misleading. If you read Form 8606, you will see that the only time it ever mentions a recharacterization is to tell you NOT to put it on the form.

So, what is Pub 590 talking about? They're talking about this section in the 8606 instructions:

Reporting recharacterizations.

Treat any recharacterized IRA contribution as though the amount of the contribution was originally contributed to the second IRA, not the first IRA. For the recharacterization, you must transfer the amount of the original contribution plus any related earnings or less any related loss. In most cases, your IRA trustee or custodian figures the amount of the related earnings you must transfer. If you need to figure the related earnings, see How Do You Recharacterize a Contribution? in chapter 1 of Pub. 590-A. Treat any earnings or loss that occurred in the first IRA as having occurred in the second IRA. You can’t deduct any loss that occurred while the funds were in the first IRA . . . Report the nondeductible traditional IRA portion of the recharacterized contribution, if any, on Form 8606, Part I. Don’t report the Roth IRA contribution (whether or not you recharacterized all or part of it) on Form 8606. Attach a statement to your return explaining the recharacterization. If the recharacterization occurred in 2023, include the amount transferred from the traditional IRA on 2023 Form 1040, 1040-SR, or 1040-NR, line 4a. If the recharacterization occurred in 2024, report the amount transferred only in the attached statement, and not on your 2023 or 2024 tax return.

The bottom line is that you just report this recharacterized contribution on Form 8606 as if it were the regular old non-deductible traditional IRA contribution that you should have made in the first place. You also need to include a statement. What should your statement look like? I would write something like this:

“To whom it may concern:

I made a 2024 Roth IRA contribution of $7,000 on March 13, 2024, because I didn't know about the whole MAGI limit thing when I made the contribution. After becoming smarter, I recharacterized $7,137.14 (original contribution plus earnings) to a traditional IRA on November 4, 2024. Thank you for helping our country fund its government. You're the best.

Hugs and kisses from your favorite taxpayer,

James Dahle”

Seriously, it doesn't say what has to be on the statement, just that there is one “explaining the recharacterization.” You don't even have to tell them why you did the recharacterization. If you had a loss in the account between contribution and recharacterization, no big deal. It's still as though you made a $7,000 contribution to a traditional IRA and THEN it lost money. If you were able to deduct the contribution (you probably can't) you would get a $7,000 deduction. The IRA provider may also send you a Form 5498 (which has the recharacterized amount on line 4), but you don't actually do anything with it when you file your taxes. It's just an informational return.

Reconverting the IRA

Here is where it gets interesting. You've now fixed your mistake in the eyes of the IRS, going from an illegal Roth IRA contribution to a legal traditional IRA contribution (that is probably not deductible for you). But you aren't done with what you meant to do, which is put money into a Roth IRA. You now need to do a Roth conversion. You do it just like you normally would as if you had contributed originally to the Traditional IRA. You can do it the very next day if you like. You can probably even do it the same day; just make sure there is a paper trail showing the money was actually in the traditional IRA at some point. There used to be a waiting period after a recharacterization before you could do a Roth conversion on that money. But that waiting period only ever applied to the recharacterization of a Roth CONVERSION (which was no longer allowed starting in 2018) and NOT the recharacterization of a Roth CONTRIBUTION. So, there is no waiting period. Just reconvert convert it and go on your merry way.

I hope this information helps you fix your mistake. Just do your Roth IRA contributions through the Backdoor going forward, and you won't have this problem again.

Step 2 Error – Not Investing in a Money Market Fund in the Traditional IRA

What happens if you LOSE money in between the contribution and conversion step? This problem is easily avoided by using an investment like a money market fund that does not go down in value for that time period. But some people fail to do so and end up losing money. When they work their way through their IRS Form 8606, they discover they have basis left over that they can then carry forward indefinitely for years! No big deal; it just makes your paperwork more complicated. Perhaps at some point in the future, you'll do a Roth conversion of tax-deferred money and this carry-forward basis will reduce the tax on that event.

What if you MADE money in the account between contribution and conversion? This actually happens most of the time, so I wrote an entire post on it called Pennies and the Backdoor Roth IRA. Technically, any money earned between the contribution and conversion step is fully taxable at ordinary income tax rates in the year of the conversion. If it is less than 50 cents, you just ignore it. If it's more, you report it on your 8606 and pay taxes on it.

If it is still in the traditional IRA, either do another tiny Roth conversion or leave it there until you do next year's Backdoor Roth IRA process. Either is fine. If you were smart and just used a money market fund and did the conversion as soon as your IRA provider allowed it (usually less than a week and sometimes as early as the next day), this won't be much money and there won't be much tax due.

Step 3 Error – Forgetting to Do the Conversion

If you forgot to do the conversion step for eight months afterward, it could be a huge gain on which you're unnecessarily paying taxes. No way to fix this one, just pay your “stupid tax” and move on.

Step 4 Error – Forgetting to Invest the Roth IRA Money

Even worse than paying taxes on a huge gain is not getting the gain in the first place because you left the money sitting in cash for months. No way to fix this one either. Your “stupid tax” this time comes in the form of opportunity cost. Just get the money invested ASAP to stop the cash drag. Maybe you even got lucky and the market went down in between contribution and investment so now you get to buy low.

Step 5 Error – The Pro-Rata Rule

Some of the most common questions I get are from people who make a late contribution to a Backdoor Roth IRA. What do I mean by late? You are allowed to make an IRA contribution AFTER the calendar year ends. In fact, you have until Tax Day, usually April 15 unless you get an extension of up to six months. While it is to your advantage to contribute to retirement accounts as quickly as possible so that money can start compounding in a tax-protected way, I understand that we all have lots of good things to do with our money and sometimes this gets pushed back into the next calendar year. All it really does is complicate your paperwork a bit.

For example: if you made your 2023 IRA contribution in April 2024, instead of reporting both the contribution and the conversion on your 2023 taxes, you would report only the contribution there. The conversion would be reported on the taxes for the year you did the conversion, i.e., your 2024 tax return due in April 2025. Your 2023 IRS Form 8606 becomes a little simpler and your 2024 IRS Form 8606 becomes a little more complicated. Not a big deal if you can follow the simple instructions.

What confuses people, however, is the pro-rata rule. This is the rule that says you need to empty your traditional IRA by December 31 of the year you do the conversion. Since these folks have never filled out a Form 8606 (or apparently read the instructions), they assume that for a 2023 contribution they need to have a balance of $0 at the end of 2023, even if they didn't do the conversion step until 2024. That's simply not the case. The pro-rata rule isn't applied until the year of the conversion, i.e., December 31, 2024.

Emptying the IRAs

How do you empty those IRAs? You usually have two choices.

- Do a Roth conversion of the whole thing. This is what I generally recommend for small IRAs where the tax bill on the conversion would not be too onerous. It is quick and easy, and it increases the amount of tax-free assets you have.

- Roll the money into a 401(k) or 403(b), either that of your current employer, that of a past employer, or to your own individual 401(k) if you are self-employed. This is usually a better option if you have a large IRA where you would rather deal with the hassle than pay the tax bill during your peak earnings years.

How large is large and how small is small? It's going to vary by the person and how much disposable cash they have. Most would consider an IRA under $10,000 to be small and an IRA over $100,000 to be large. In between, it's a personal decision as to which would be better for you.

What If You Didn't Empty the IRA?

What if you screwed this one up? Your Backdoor Roth IRA conversion step just got pro-rata'd. There is a tax bill associated with that because most of your conversion was of tax-deferred money rather than post-tax money like it was supposed to be.

The fix for this is going to vary by the individual, but the easiest fix is to simply convert the entire IRA to a Roth IRA now, so you end up getting all your post-tax money into that Roth IRA. Another possible fix is to figure out a way to separate your basis in that IRA, roll the tax-deferred money into a 401(k), and then convert the basis left behind in the IRA.

Do yourself a favor and just empty the darn IRA by December 31. Keep in mind that this is usually not an instantaneous process, so don't put it off until you're on holiday break at the end of the year.

Step 6 Error – Screwing Up the Tax Forms

Both individual taxpayers and professional tax preparers screw up IRS Form 8606 all the time. In fact, some of them haven't even heard of a Backdoor Roth IRA. (Incidentally, this is one of the best questions to ask while interviewing a potential tax professional—”How many Backdoor Roth IRAs did you help last year?”)

The usual fix to this error is to file a 1040X (Amended Tax Return) and a new Form 8606. You can do this for the last three years if necessary. If you didn't file Form 8606 at all, you'll definitely want to do this. The key is to check lines 15c and 18 on Form 8606. They should both be a number very close to zero if the form is being completed correctly.

The tax preparer should NOT be filing Form 5439. If you did Steps 1-5 right, this form probably doesn't belong in your tax return.

A lot of people wonder about the 1099-R sent to them by their IRA provider and worry that it was done wrong and that it will cause them to pay taxes they shouldn't have to pay. Sometimes the form was filled out wrong, but mostly this is just a lot of anxiety. What gets people anxious is finding something on Line 2a “Taxable amount.” As long as the box on Line 2b is also checked “Taxable amount not determined,” you're golden. Don't worry about it. If it is not, have the IRA provider send you a new, correct form—either with $0 in 2a or the box in 2b checked (usually the latter). Here's what mine from a few years back looked like from Vanguard:

Note that Box 2b is checked, even though a taxable amount of $5,500.07 is being reported to the IRS.

Again, if you're not sure how to enter this into TurboTax, check out my TurboTax tutorial.

Still Confused About the Backdoor Roth?

Need more help with a Backdoor Roth IRA? I wish Congress would just lift the rule against direct Roth IRA contributions for high earners and save us all this hassle, but who knows if that will ever happen.

- If you made your contribution after the end of the year, check out Late Contributions to the Backdoor Roth IRA.

- Here's a step-by-step tutorial for doing a Backdoor Roth IRA at Vanguard.

- Here's a step-by-step tutorial for doing a Backdoor Roth IRA at Fidelity.

- Here is a step-by-step tutorial reporting the Backdoor Roth IRA in TurboTax.

- Here is my prior post on 17 Ways to Screw Up Your Backdoor Roth IRA.

- You can hire a professional to help you—either a good financial advisor or a good tax strategist can assist.

- You can also ask your peers for help on the WCI Forum, the Private WCI Facebook Group, and the WCI Subreddit.

Late Contributions to the Backdoor Roth IRA

While it is “cleaner” to make your contribution and your conversion all in the same calendar tax year, you can make your contribution up until your tax filing date of the next year. The key to filling out the 8606 correctly when you make a contribution after the calendar year is to recognize that the contribution step is reported for the tax year and the conversion step is reported for the calendar year. So imagine you did the following during the calendar year 2023:

- Made a 2022 IRA contribution (reported on 2022 8606)

- Did a Roth conversion of that contribution (reported on 2023 8606)

- Made a 2023 IRA contribution (reported on 2023 8606)

- Did a Roth conversion of that contribution (reported on 2023 8606)

Your forms would look like this:

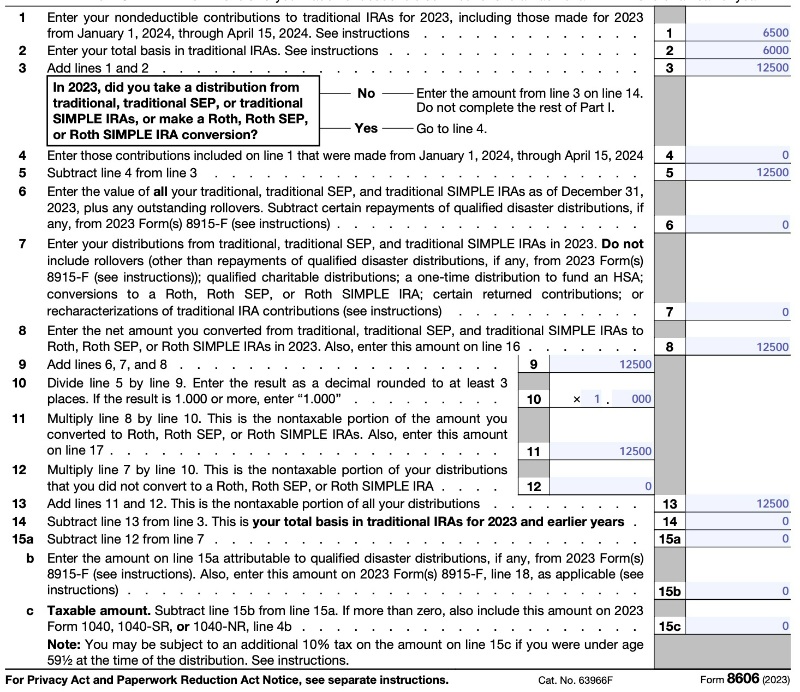

2023 Form 8606 (Only Have to Fill Out Part I)

Note that all this serves to do is report basis for the next year. No tax is due. Since no conversion step was done during the calendar year 2022, you only have to fill out lines 1-3 and 14.

2023 Form 8606 (Must Fill Out Parts I and II)

Note that you've got to do all of Part I plus Part II for this year because you did the conversion step, unlike last year (2022). Let's go through this line by line.

Your Roth IRA contributions will need to go through the “backdoor” many times as you build your portfolio.

Form 8606 – Part I

- Line 1 – That's the money you contributed for 2023 (which would be $6,500).

- Line 2 – This is your basis. Since you made a contribution for 2022 but didn't do a conversion during 2023, your basis is $6,000.

- Line 3 – $6,500 + $6,000 = $12,500.

- Line 4 – Remember this is asking about 2024, not 2023, and since you won't make the mistake of doing your contribution late again, this will be zero.

- Line 5 – $12,500 – $0 = $12,500.

- Line 6 – This is the line that triggers the pro-rata issue. Even though you made a 2022 contribution, you did so AFTER December 31, so this line would still be zero if you filled it out for 2022, which you didn't because you didn't do a conversion in 2022 and got to skip lines 4-13. But this is the 2023 form and since you converted your entire traditional IRA, this will be $0.

- Line 7 – This doesn't include conversions. Since you didn't take any money out of your traditional IRA this year except the conversion, this is $0.

- Line 8 – You converted a total of $12,500 this year to a Roth IRA, so $12,500.

- Line 9 – $0 + $0 + $12,500 = $12,500.

- Line 10 – $12,500/$12,500 = 1.

- Line 11 – $12,500 * 1 = $12,500.

- Line 12 – $0 * 1 = $0.

- Line 13 – $12,500 + $0 = $12,500.

- Line 14 – $12,500 – $12,500 = $0.

- Line 15a – $0 – $0 = $0.

- Line 15b – You didn't take money out of an IRA to help you survive a disaster, so $0.

- Line 15c – $0 – $0 = $0.

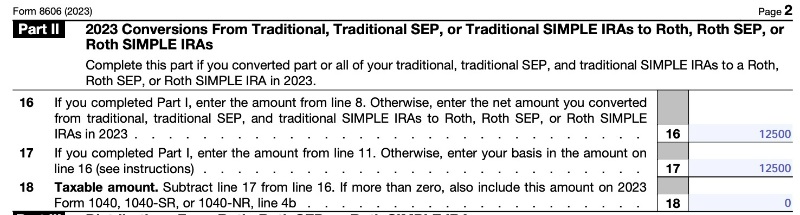

Part II

- Line 16 – Line 8 is $12,500 so $12,500.

- Line 17 – Line 11 is $12,500 so $12,500.

- Line 18 – $12,500 – $12,500 = $0.

Backdoor Roth IRA FAQs

You have until tax day (generally April 15, but as late as October 15 if you file an extension) of the following year to make your traditional IRA contribution. There is no deadline for the Roth conversion step; it can be done at anytime. Make sure you fill out the paperwork properly according to the section above about late contributions.

Yes. Just remember to report last year's contribution on last year's Form 8606 and this year's contribution and the conversion on this year's Form 8606.

No. Only traditional IRAs, rollover IRAs, SEP-IRAs, and SIMPLE IRAs count. See line 6 of Form 8606 for details.

Yes. All IRAs count toward the pro-rata calculation.

If it is small, convert it to a Roth IRA along with this year's traditional IRA contribution and pay the tax due on it. If large, try to roll it into your employer's 401(k) or if you have self-employment income, into your individual 401(k).

The easiest solution is to convert the entire IRA, SEP-IRA, or SIMPLE IRA that caused the pro-ration and is now composed of both pre-tax and after-tax money. That is also the most expensive solution. A harder solution that may save you some taxes involves isolating the basis in that IRA by rolling the rest of the account into a 401(k) and then convert just the basis to a Roth IRA.

If you put it into a traditional IRA it is going to cause any future Backdoor Roths to be pro-rated. Better options include leaving it where it is; rolling it into your new employer's 401(k) or 403(b); rolling it into your individual 401(k); or, if it is small, just converting the whole thing to a Roth IRA.

In 2024, you are allowed to contribute $7,000 ($8,000 if 50+) per year for you and $7,000 ($8,000 if 50+) for your spouse. This includes all contributions to traditional and Roth IRAs. Rollovers/transfers do not count toward the annual contribution limit.

While in the traditional IRA for a day or two, leave it in cash. Once it is in the Roth IRA, invest it according to your written investing plan. If you don't have one, get one, but in the meantime it would be a good idea to put it into a lifecycle fund such as a Vanguard Target Retirement Fund.

You can use the same ones each year.

The Backdoor Roth IRA process leads to more tax-free retirement account money for doctors and other high-income professionals. If you follow the simple steps outlined above, you will pay less in taxes, boost your returns, facilitate your estate planning, and increase your asset protection. Most members of The White Coat Investor community do these every year, and you should too.

What do you think? Are you doing Backdoor Roth IRAs? Why or why not? Any questions about it? Comment below!

[This updated post was originally published in 2014.]

The post How to Do a Backdoor Roth IRA appeared first on The White Coat Investor - Investing & Personal Finance for Doctors.

||

----------------------------

By: The White Coat Investor

Title: How to Do a Backdoor Roth IRA

Sourced From: www.whitecoatinvestor.com/backdoor-roth-ira-tutorial/

Published Date: Fri, 16 Feb 2024 07:30:13 +0000

Read More

.png) InvestingStocksToolsClubsVideosPrivacy PolicyTerms And Conditions

InvestingStocksToolsClubsVideosPrivacy PolicyTerms And Conditions