<iframe style="width:120px;height:240px;" marginwidth="0" marginheight="0" scrolling="no" frameborder="0" src="//ws-na.amazon-adsystem.com/widgets/q?ServiceVersion=20070822&OneJS=1&Operation=GetAdHtml&MarketPlace=US&source=ss&ref=as_ss_li_til&ad_type=product_link&tracking_id=peaceinvesting-20&language=en_US&marketplace=amazon®ion=US&placement=0060555661&asins=0060555661&linkId=80f8e3b229e4b6fdde8abb238ddd5f6e&show_border=true&link_opens_in_new_window=true"></iframe>|<iframe style="width:120px;height:240px;" marginwidth="0" marginheight="0" scrolling="no" frameborder="0" src="//ws-na.amazon-adsystem.com/widgets/q?ServiceVersion=20070822&OneJS=1&Operation=GetAdHtml&MarketPlace=US&source=ss&ref=as_ss_li_til&ad_type=product_link&tracking_id=peaceinvesting-20&language=en_US&marketplace=amazon®ion=US&placement=1119404509&asins=1119404509&linkId=0beba130446bb217ea2d9cfdcf3b846b&show_border=true&link_opens_in_new_window=true"></iframe>|<iframe style="width:120px;height:240px;" marginwidth="0" marginheight="0" scrolling="no" frameborder="0" src="//ws-na.amazon-adsystem.com/widgets/q?ServiceVersion=20070822&OneJS=1&Operation=GetAdHtml&MarketPlace=US&source=ss&ref=as_ss_li_til&ad_type=product_link&tracking_id=peaceinvesting-20&language=en_US&marketplace=amazon®ion=US&placement=1119376629&asins=1119376629&linkId=2f1e6ff64e783437104d091faaedfec7&show_border=true&link_opens_in_new_window=true"></iframe>

By Dr. Hamik Martirosyan

Risk and return are inextricably tied together. They form the basic elements required to make successful investment decisions. Though risk is just as important as returns, most investors are typically more focused on the returns and underestimate the importance of risk.

In researching equity or fund literature, the returns are easily found; however, finding risk metrics requires more digging. Even when risk metrics are found, they will have their limitations. Given the lack of clarity and the lack of importance assigned to risk, how can an individual investor think about risk to make better investment decisions? A healthy appreciation of risk will differentiate investors from speculators.

What Is Risk?

To begin with, we must consider what exactly is risk.

In the investment world, risk is defined as volatility. It is measured by the Standard Deviation (SD) of returns over a specified time frame. This is helpful in that it provides a quantitative measure of risk, and it's what is used in models to assess risk. However, this is an imperfect definition of risk, and it comes with significant limitations. This definition is made under the assumption that the investing world operates in a normal distribution (bell curve) world. In his book The Black Swan, Nassim Taleb explains how investment returns do not follow a bell curve. If you plot biological variables—such as people’s heights, ambient temperatures, etc.—they will follow a normal distribution of the bell curve. However, investment returns are too complex and variable to follow a normal distribution. It will approximate a normal distribution but imprecisely so.

Also. importantly, investments can have fat tails. These represent a higher risk of rarer events occurring than would be predicted by the bell curve. Events that may be predicted to happen every 100 years may instead occur every few decades. Rarer events, being rare and less anticipated, can potentially have a more devastating effect on your portfolio. Models based on volatility alone will not address this important point sufficiently. Lastly, another important limitation of volatility is that it is completely backward-looking.

Instead, Howard Marks, the former CEO of Oak Tree, thinks of volatility as an indicator or symptom of risk, but it is far from the definition of risk. He describes risk as the possibility of permanent loss. This is what investors fear and demand compensation for. This is something that cannot be easily quantifiable. As a result, he argues that risk by necessity will be subjective, imprecise, and qualitative. That is what makes successful investing so hard. Risk cannot be easily measured and quantified. Models of risk management may prove to be illusory.

More information here:

The Risk of Retirement

Compensated vs. Uncompensated Investment Risk

A Brief History of Risk

A review of financial history shows that the most overarching theme in investor behavior is speculation and the attempts to make a quick buck. The concept of risk is typically ignored or minimized. It is only recognized after the fact when an investment idea collapses and principal is lost. This is evidenced by the South Sea bubble, the Tulip Craze, and the roaring '20s to name a few moments of speculative excess. In these cases, speculation drove up prices. Increased prices and returns fueled further speculation and further drove up prices. Risk was relegated to the sidelines or ignored altogether. The use of leverage and option-type products provides further evidence of the avoidance of risk assessment. With time, these investments collapsed onto themselves as they were based on an investment structure and price that were not sustainable. Only then, in retrospect, did risk become clearly apparent to all.

Even at the professional level, risk was not formally adapted until after Harry Markowitz’s Portfolio Theory in 1952. Prior to that, risk was not quantitatively considered when making investments. Markowitz’s key insight was that risk is central to the investment process. This is when volatility was introduced to the concept of risk.

However, despite the introduction of quantitative measures of risk, we continue to see episodes of speculative excess with little emphasis placed on risk. The most recent examples include the dot.com era of the early 2000s, the Great Financial Recession of 2008, and cryptocurrencies. With the dot.com era, Nasdaq’s PE ratio rose to 200 (the historical average is in the 20s), and anything with a dot.com after its name effortlessly raised money. With cryptocurrencies, funds were flowing easily into any fund that was crypto-related. To date, we’ve seen crypto funds/companies collapse due to poor structure or outright fraud. FTX and Binance are a couple of examples. In addition, the high volatility of crypto prices also adds evidence to the lack of risk aversiveness from its investors.

Qualitative Aspects of Risk

So far, I’ve told you that true risk is subjective and cannot be reliably quantitated. You may wonder how I would formulate my thoughts on risk. Howard Marks’ excellent newsletter goes into multiple ways to qualitatively think about risk. This may be used as a cornerstone of your investment philosophy and help guide your decision-making. Some important aspects he discusses about risk include:

- Risk means more things can happen than will happen, and you don’t know with certainty which event will happen. The future is not a destined outcome but a probability distribution of possible outcomes. Even if you know the probabilities, it does not mean you know what is going to happen. Just like in poker, you may know its strategy and the odds inside out, but you still do not know which cards will be dealt. You only know the probabilities of a certain card being dealt. The inherent uncertainty of the draw will always remain.

- Risk is not quantifiable in advance. Not only that, it is also not quantifiable in hindsight. The investment result by itself is not an indicator of how well risk was managed. This is because risk is hidden and deceptive. An investment can be risky and still not show losses as long the environment remains salutary. Only during tough times do we find out how much risk was taken. As it's been said, “When the tide goes out, you know who’s swimming naked.” Risk control is a hidden accomplishment since losses happen intermittently.

- Risk is counterintuitive. Risk of an activity lies not in the activity but in the behavior of the participants. Risk is low when investors behave prudently and high when they don’t. Risk is highest when we are lulled into believing that risk has disappeared and lowest after a crash when we think an investment is too risky to even think about. An example is the housing crisis of 2008, when investors were flipping houses without regard to risk. Given the continued rise in real estate prices, ebullience led to the belief that risk in real estate was low (or non-existent) and that house prices never fall. The risk was highest when investors thought that it was the lowest. This became clear soon after the collapse of the housing market. Conversely, post-collapse, investors felt that investing in real estate was high risk and avoided the asset class altogether. Again counterintuitively, this is when risk was lowest (when investors thought it was the highest).

- Risk is not a function of asset quality. A high-quality asset can be risky because it’s been priced so high. A low-quality asset can be priced cheap enough that it is not risky. It’s not what you buy; it’s what you pay that determines risk. Buying blue chip stocks may seem safe; instead, it may carry significant risk based on the price you paid and the exuberance of the markets at the time. Low-quality assets may have a large enough margin of safety to cover the risk associated with it.

- Risk is the possibility of a bad outcome materializing from a range of possibilities. It can lead to either loss of capital or missing out on gains. Both can be considered negative outcomes, not just losses. However, you don't become poor from not investing enough or missing out on gains. Principal loss seems to be the more serious offense.

- Risk occurs sporadically. It does not gradually build up for an investor to recognize and adjust appropriately and judiciously. Rather it shows up in paroxysms.

Taleb gives an example of how the White House turkey is nurtured for years. Every morning, the turkey is accustomed to its daily feed as it occurs regularly and without fail. However, on one morning in the third week of November, the turkey is met with the guillotene rather than its typical feed. This is a perfect example of the dangers of chasing after a few extra points of yield without researching how that extra yield is obtained. You might obtain regularly scheduled dividends and feel confident they will continue. But if that extra yield is due to increased risk-taking, the dividends may stop abruptly and may also include loss of capital.

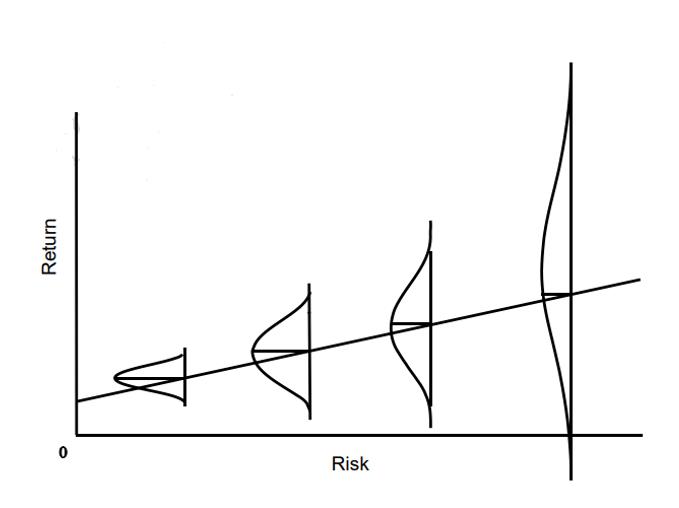

Lastly, think of the Risk/Reward graph below as not a linear relationship but more like a probability distribution of losses which is increased as more risk is taken. It's best illustrated by Marks’ graph, Figure 1.

Figure 1: Risk-Return Distribution, Howard Marks, Oaktree Newsletter

How Should You Handle Risk?

The essence of risk management lies in maximizing the areas where we have some control over the outcome while minimizing the areas where we have absolutely no control over the outcome and where the linkage between effect and cause is hidden from us.

The first step in managing risk is to remember not to ignore it. It is something that must be managed and controlled, not avoided. It must be dealt with consistently, not sporadically. You do not know when negative outcomes will happen. Even during the good times, risk assessment should be central to investing. In fact, especially during good times, risk assessments should be central. This is when risk is the highest due to investor overconfidence and behavior.

Secondly, think of risk in its truest sense. Investing is like pulling one ticket from a bowlful of tickets (possible outcomes). Superior investors have a better sense of what is in the bowl, but they still don’t know the outcome (or what ticket will be pulled). They make their investments based on what is in the bowl and what is the probability of each ticket becoming reality. This requires us to perform adequate due diligence prior to investing, and after investing, having the humility to know that the outcome remains uncertain. Superior investors have a better sense of the probability distribution that governs future events and for whether the potential returns compensate for the risk in the distribution's negative left-handed tail—and to make decisions based on this knowledge. This would be a goal to aim for in your investment journey.

You can bear risk prudently if it's:

- Risk you are aware of

- Risk that can be analyzed

- Risk that can be diversified

- Risk you are paid well to bear

Each of these would be a discussion among itself.

Rather than specific strategies, I’ve laid the foundation of how to think about risk in formulating an intelligent investing plan—a plan based on a high savings rate, diversification, low costs, and hedging against known risks.

More information here:

Yes, Risk Tolerance Can Be Modified: You Just Have to Rewire Your Brain

The Bottom Line

Risk is an underappreciated pillar of investing. Volatility is a crude and insufficient marker for it. Risk can be nothing more than a subjective assessment with some objective, though imperfect, data. This is what makes investing hard and lies at the heart of the Charlie Munger quote: “Investing is hard, and anyone who tells you different is stupid.”

The details above give some guidance about how to think about and how to approach risk to help formulate your investment policy plan.

Let's end with the quote below from writer and philosopher G.K. Chesterton which beautifully encapsulates the genesis of risk and its complexity. The problem is that our world is not completely illogical or logical; it is somewhat logical. It is logical enough for us to believe that it is completely logical, but the illogicality lies in wait and surfaces periodically to devastate portfolios.

“The real trouble with this world of ours is not that it is an unreasonable world, nor even that it is a reasonable one. The commonest kind of trouble is that it is nearly reasonable, but not quite. Life is not an illogicality; yet it is a trap for logicians. It looks just a little more mathematical and regular than it is; its exactitude is obvious, but its inexactitude is hidden; its wildness lies in wait.”

How do you think about risk? Do you feel like you can adequately measure how much risk you're taking? Do you take too much risk? Not enough? Comment below!

[Editor's Note: Dr. Hamik Martirosyan is a nephrologist in southern California with an active interest in investing and personal finance. This article was submitted and approved according to our Guest Post Policy. We have no financial relationship.]

The post How to Think About Risk and Why It’s So Hard to Quantify appeared first on The White Coat Investor - Investing & Personal Finance for Doctors.

||

----------------------------

By: Lauren O'Brien

Title: How to Think About Risk and Why It’s So Hard to Quantify

Sourced From: www.whitecoatinvestor.com/quantify-risk/

Published Date: Mon, 20 Nov 2023 07:30:38 +0000

Read More

.png) InvestingStocksToolsClubsVideosPrivacy PolicyTerms And Conditions

InvestingStocksToolsClubsVideosPrivacy PolicyTerms And Conditions