<iframe style="width:120px;height:240px;" marginwidth="0" marginheight="0" scrolling="no" frameborder="0" src="//ws-na.amazon-adsystem.com/widgets/q?ServiceVersion=20070822&OneJS=1&Operation=GetAdHtml&MarketPlace=US&source=ss&ref=as_ss_li_til&ad_type=product_link&tracking_id=peaceinvesting-20&language=en_US&marketplace=amazon®ion=US&placement=0060555661&asins=0060555661&linkId=80f8e3b229e4b6fdde8abb238ddd5f6e&show_border=true&link_opens_in_new_window=true"></iframe>|<iframe style="width:120px;height:240px;" marginwidth="0" marginheight="0" scrolling="no" frameborder="0" src="//ws-na.amazon-adsystem.com/widgets/q?ServiceVersion=20070822&OneJS=1&Operation=GetAdHtml&MarketPlace=US&source=ss&ref=as_ss_li_til&ad_type=product_link&tracking_id=peaceinvesting-20&language=en_US&marketplace=amazon®ion=US&placement=1119404509&asins=1119404509&linkId=0beba130446bb217ea2d9cfdcf3b846b&show_border=true&link_opens_in_new_window=true"></iframe>|<iframe style="width:120px;height:240px;" marginwidth="0" marginheight="0" scrolling="no" frameborder="0" src="//ws-na.amazon-adsystem.com/widgets/q?ServiceVersion=20070822&OneJS=1&Operation=GetAdHtml&MarketPlace=US&source=ss&ref=as_ss_li_til&ad_type=product_link&tracking_id=peaceinvesting-20&language=en_US&marketplace=amazon®ion=US&placement=1119376629&asins=1119376629&linkId=2f1e6ff64e783437104d091faaedfec7&show_border=true&link_opens_in_new_window=true"></iframe>

[Editor's Note: Want to make a huge impact in the lives of your medical school classmates while also earning some free gear? Become a WCI Champion today and be the financial hero your med school colleagues deserve by passing out free copies of The White Coat Investor's Guide for Students book. If you’re a first-year student (whether you’re MD, DO, DDS, Pharmacy, NP, or PA), sign up here to get started. If you complete the mission, you’ll get a free WCI T-shirt, and if you take a photo of you and your classmates with the book, you’ll get even more merch. Register today to become a Champion and help generate millions of dollars for your classmates!]

By Dr. Julie Alonso, WCI Columnist

It has been an exciting and eventful year for my family. My twin children came of age and celebrated their B’nai Mitzvah (plural of Bar or Bat Mitzvah), a Jewish ceremony that marks the start of the transition to adulthood. They worked hard for years studying Hebrew, attending religious school, and working with a mentor and a tutor to arrive at this accomplishment. These kinds of special occasions that give us the opportunity to experience so much pride and joy in our lives do not come along often. So, my husband and I decided to throw a big celebration. Suffice it to say that 2023 has been an expensive year for us!

This column is NOT about whether you should throw a large event, whether it be a wedding, reunion, Sweet 16, Quinceañera, retirement party, anniversary celebration, etc. That decision needs to be made with intention, taking into account a lot of individual factors and aligning with your values and budget. Some people will never be convinced that throwing a big event like this is worthwhile. Some may consider it a complete and frivolous waste of money, and that’s OK. I’m not here to convince you otherwise.

However, the opportunity to see our dearest friends and family from all over the country (and even the world) was something that we did not want to pass up. I’ve always emphasized to my children that the things that matter most in life are relationships and experiences. We try to live by these values and set an example. We’ve often given them experience gifts instead of toys, and we have done donation drives in lieu of gifts at many birthday parties. We prioritize travel experiences, and we will buy tickets for a concert, show, or event as a family “gift” instead of giving individual presents.

How did I justify throwing such a costly event, though? I am in a moderately paid specialty as a psychiatrist, but I make more than enough to live comfortably and support my family. I am fortunate that I only had minimal student loans and have paid those off, have a very low monthly mortgage payment ($1,810 thanks to a 15-year refi of 2.375% during the pandemic), and have no other debt besides a small car loan. My children attend public school. We are meeting all of our goals in maximizing retirement savings (employer-sponsored 401(k)s, solo 401(k)s, Backdoor Roth IRAs), 529 savings, taxable investment accounts, emergency fund, etc.

Bar or Bat Mitzvah celebrations, like any coming-of-age ceremony or wedding, can vary greatly by region, budget, and personal preference. We’ve been to some that are simple backyard parties and others that are over-the-top affairs. We wanted to have a bigger celebration so we could include more friends and family in this special moment. Here’s how we could throw a (relatively) lavish B’nai Mitzvah celebration weekend while keeping it within reason of our budget.

Setting Your Mindset

I have been a WCI reader since about 2016, and the information I’ve learned has helped me reconceptualize my approach to personal finance, including saving for retirement, investing, paying down debt, and the often not-as-lauded word of spending. I had read Dr. Jim Dahle’s article on spending intentionally that cited the following advice:

“Be generally frugal and selectively extravagant. Figure out what you really value, and spend your money on that, guilt-free. This is called intentional spending.”

His keynote speech at WCICON23 also talked about not being afraid of meaningful spending and, dare I say, allowing oneself to spend if you are meeting your financial goals in the pursuit of enjoying life in the present. I often have trouble pulling the trigger on large purchases. I did not grow up in a wealthy household, and my parents carefully considered purchases and rarely splurged on themselves. Consequently, I had to come to terms with planning and paying for such a large event.

We had saved a small amount of money earmarked for the celebration weekend (thanks Ally savings buckets!), but my plan was to largely cash-flow it, continue to meet my financial goals, and avoid taking out any other money from savings. With that being said, I framed my mindset in the context of this being a much more expensive year than average and allowed myself to accept that idea. A “selective extravagance,” if you will, that aligns with our life goals. I had to psychologically accept the thought that it was OK to spend on something that was a once-in-a-lifetime event (the advantage of having twins who went through this process at the same time was not lost on me).

It aligns with the adage, “You can have anything you want but not everything you want.” I try to live a balanced life of saving for the future but not with such austerity that it impacts the present. So, how did we approach paying for such a large expense while reconciling it with our financial principles and goals?

More information here:

From Wedding Planning to Owning 16 Credit Cards

From Fourth Year to the Real World: An $80,000 Wedding Causes a Downward Spiral

Defining a Budget

I found it helpful to define a budgetary range instead of a single fixed amount. It helped to feel some flexibility in the planning and not having such a rigid focus on a single number. I set my ideal budget but with a maximum budget in mind that I did not feel comfortable going over. This could be a range of 5%-15%, as an example.

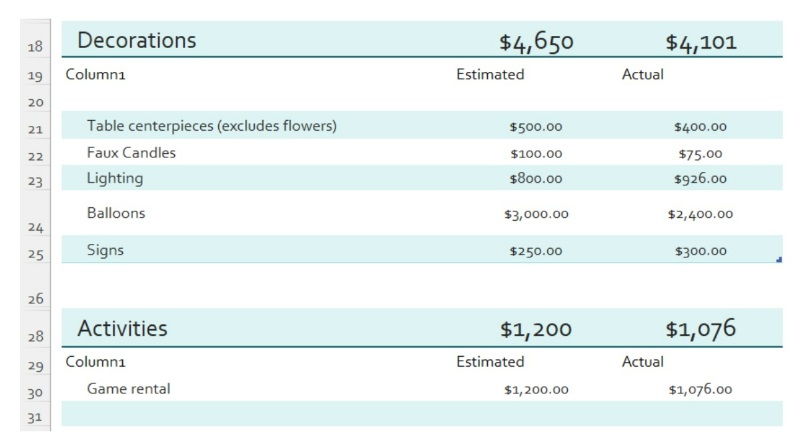

Our budget for the entire weekend of events was $50,000-$60,000. I’m happy to say that we ended up in the middle of the budget range and below our max, but this took continually checking in on the budget and my mega-Excel spreadsheet which tracked estimated and actual expenses along the way. I adjusted things as needed. If something ended up costing less, it gave us some more wiggle room for unexpected expenses (which definitely popped up). I had a spending log where I tracked EVERY penny I spent.

Here's a small snippet of my spreadsheet.

Reducing Personal Expenses and Increasing Cash Flow

I looked at areas where we could temporarily cut back on some spending. Dining out, purchasing clothing, or paying for electronics are some easy areas. Reducing overpayments on a mortgage or loan temporarily can free up some funds to avoid dipping into savings. We still paid for a scheduled Disney cruise and for airfare and a tour package for our summer vacation, so we did not scrimp completely. But we had planned for these things in advance. We cut back slightly on eating out and other expendable purchases in the months leading up to the event.

We also had to consider fully funding my husband’s 401(k) over the final four months of 2022 ($5,000+/month) since that is when he became eligible at the one-year anniversary of his job. With the big event being just a few months later in February 2023, this was not ideal timing. But since we did not want to miss out on maxing out the tax-advantaged retirement savings, we made it work. We also pushed out our Backdoor Roth IRA contributions to later in 2023 instead of at the beginning.

More information here:

With Our Expanding Family, We’ve Had to Break Our Financial Plan – Twice

Planning Over Time

Many of the vendors for the B'nai Mitzvah offered installment payments at the same total cost. I took advantage of those that did. Most of the bookings included a deposit that ranged from a nominal amount to a sizeable chunk of the cost, but many of them allowed us to pay over two or three installments that were spread out over months to a year plus. I knew that the final installments would all be due around the same time—a few weeks to a month out from the event—so I planned accordingly with the bucket of money we had earmarked. Also, I read the cancellation policies carefully before signing any contracts.

If you have the luxury of having a long runway to plan, this can also help with cash-flowing the event. We got the date for the ceremony over two years in advance, so I could start booking things over a longer period of time. I booked our top-choice venue 18 months out (on the day the reservations opened) with a small deposit. I booked the catering and entertainment more than a year ahead as well. On a side note, I got some better deals booking a DJ and caterer in late 2021 while the pandemic was still ongoing (nobody was booking large events, imagine that!) and before many of the vendors raised their rates in the setting of post-pandemic inflation.

Increasing Side Income

I took on some extra hours of telepsychiatry work after hours when some of the big payments were due but not too much that it greatly impacted my schedule or well-being. I cut back to my usual schedule as the event got closer. Other thoughts would be to moonlight extra hours within your medical field or increase your work in a non-medical side gig.

More information here:

The Gender Role Reversal: Being the High Earner of My Family as a Woman

Go High-Low

High-low is in style in the fashion world, meaning you wear some items that are high-end and mix them with other less luxurious items. I took this approach with our event. I focused on the food, venue, and entertainment (the big three of event planning) but bought a lot of the decorations on my own. I found savings in other areas, such as lighting. With a bit of extra legwork, I found an online vendor that shipped the lights both ways for free. This was over 50% less than what the DJ wanted to charge for the same lighting package, and it took only a little additional effort. Since I enjoy planning and crafts, I did not hire an event planner and took on the planning myself, which saved plenty of money. I made and designed all of the favors, signs, and decorations. I bought many of the décor items in bulk online (like votives, faux candles, bud vases, party favors, faux florals, DJ giveaways), and I took advantage of Black Friday sales.

We threw a dinner for out-of-town guests on the evening prior, sponsored a lunch after the ceremony, and hosted a brunch the next morning as well. My focus was on the main party, so I was able to seek out affordable deals and reasonable costs with these other events.

Since the event was in late February, just before spring break in Texas, we decided to forego a trip after the party was over (plus we had to go to WCICON!). It was really a nice break with some downtime after such a busy period in our lives and gave our children some time to relax. Although my husband and I were still working, it allowed us to avoid the stress of last-minute tasks and packing for a trip.

I’m happy to say that the celebration, and the whole weekend, were truly one of the most special times in our lives. We were surrounded by loved ones in beautiful and meaningful ways. We could physically see and feel the support of so many friends and family who came from near and far to be with us. I feel comfortable with the decisions we made in throwing and cash-flowing a large event, and I know that we were intentional with our planning, budgeting, and spending. The warm memories and photographs will last a lifetime—and that’s a great return on investment.

Have you had to throw a big event? How did you save for it? Did you cash-flow it? Was it worth it in the end? Comment below!

The post Justifying and Cash-Flowing a ‘Selective Extravagance’ appeared first on The White Coat Investor - Investing & Personal Finance for Doctors.

||

----------------------------

By: Josh Katzowitz

Title: Justifying and Cash-Flowing a ‘Selective Extravagance’

Sourced From: www.whitecoatinvestor.com/cash-flowing-big-event/

Published Date: Tue, 28 Nov 2023 07:30:05 +0000

Read More

.png) InvestingStocksToolsClubsVideosPrivacy PolicyTerms And Conditions

InvestingStocksToolsClubsVideosPrivacy PolicyTerms And Conditions