<iframe style="width:120px;height:240px;" marginwidth="0" marginheight="0" scrolling="no" frameborder="0" src="//ws-na.amazon-adsystem.com/widgets/q?ServiceVersion=20070822&OneJS=1&Operation=GetAdHtml&MarketPlace=US&source=ss&ref=as_ss_li_til&ad_type=product_link&tracking_id=peaceinvesting-20&language=en_US&marketplace=amazon®ion=US&placement=0060555661&asins=0060555661&linkId=80f8e3b229e4b6fdde8abb238ddd5f6e&show_border=true&link_opens_in_new_window=true"></iframe>|<iframe style="width:120px;height:240px;" marginwidth="0" marginheight="0" scrolling="no" frameborder="0" src="//ws-na.amazon-adsystem.com/widgets/q?ServiceVersion=20070822&OneJS=1&Operation=GetAdHtml&MarketPlace=US&source=ss&ref=as_ss_li_til&ad_type=product_link&tracking_id=peaceinvesting-20&language=en_US&marketplace=amazon®ion=US&placement=1119404509&asins=1119404509&linkId=0beba130446bb217ea2d9cfdcf3b846b&show_border=true&link_opens_in_new_window=true"></iframe>|<iframe style="width:120px;height:240px;" marginwidth="0" marginheight="0" scrolling="no" frameborder="0" src="//ws-na.amazon-adsystem.com/widgets/q?ServiceVersion=20070822&OneJS=1&Operation=GetAdHtml&MarketPlace=US&source=ss&ref=as_ss_li_til&ad_type=product_link&tracking_id=peaceinvesting-20&language=en_US&marketplace=amazon®ion=US&placement=1119376629&asins=1119376629&linkId=2f1e6ff64e783437104d091faaedfec7&show_border=true&link_opens_in_new_window=true"></iframe>

[Editor's Note: What exactly do you get when you sign up for the upcoming Zero To Freedom Through Cashflowing Rentals course? Dual physician couple Kenji and Leti will teach you all you need to know about direct real estate investing in this action-based seven-week course. They’ll walk you through the blueprint for how to crunch the numbers to see if a property will generate cash flow, how to know where and when to buy your first property, how to build the right team, and how to negotiate like a pro. Plus, if you sign up today, we’ll throw in a copy of the WCI Continuing Financial Education Las Vegas course (a $649 value!). Today is the day for you to discover why the Zero To Freedom Through Cashflowing Rentals course is a WCI favorite!]

By Dr. James M. Dahle, WCI Founder

If you're really interested in mortgage history, you know that the 30-year mortgage has really only been around since the post-WWII years. Going into the Great Depression, most mortgages required a 50% down payment, and they were interest-only (and variable) for 5-7 years. After that, a big balloon payment was due. Nevertheless, there is some wisdom in the 30-year mortgage. Since most careers last about 30 years after the time people traditionally buy a house, you will have your mortgage paid off right about retirement time (if you never move). However, there is nothing magic about the 30-year mortgage. As the cost of housing rises, 40- and even 50-year mortgages are becoming ever more popular.

Our European peers won't find this surprising. People have been using 50-year and even multi-generational mortgages there for years.

Today, let's talk about whether getting a super-lengthy mortgage is a good idea for you.

Why Get a 40-Year Mortgage?

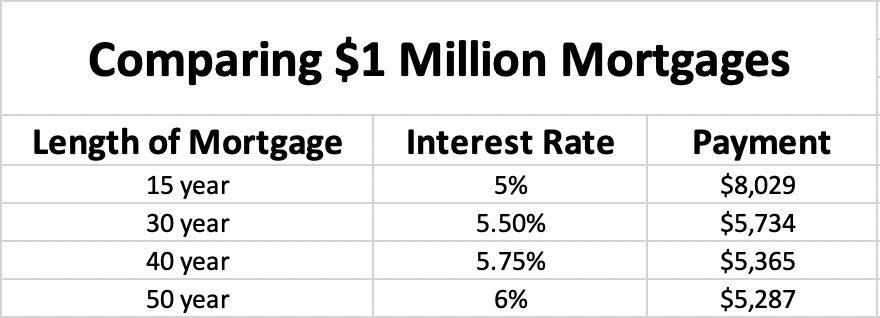

The main benefit of a 40- (or 50-) year mortgage is that the payments are lower than they would be on a 30-year mortgage and especially on a 15-year mortgage. This is just math. Let's assume a 15-year fixed mortgage is available at 5% and you can get a 30-year at 5.5%, a 40-year at 5.75%, and a 50-year at 6%. What do the payments look like on a $1 million mortgage?

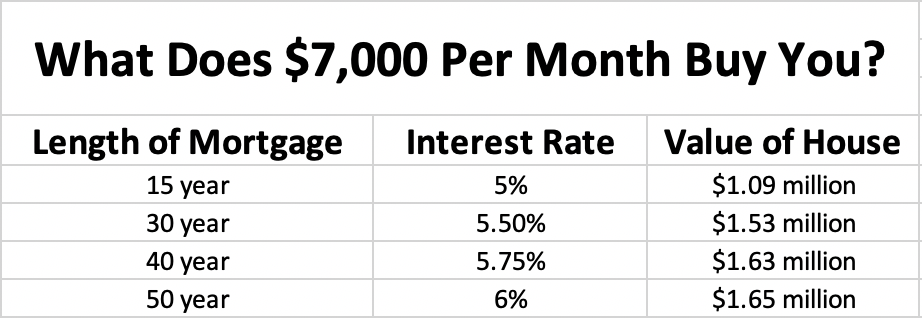

As you can see—even with a higher interest rate—the longer the mortgage, the lower the payments. If you reverse-engineer this equation, you can see that someone can afford more house if they take out a longer mortgage. Let's assume someone is going to put 20% down on their house and have $7,000 per month to spend on principal and interest. How expensive of a house can they buy, and how does that change if they use a longer mortgage? We'll assume the same mortgage rates as before (5%-6%).

Obviously, the larger the house, the larger that 20% down payment would be, too. But you can see why someone would consider a really long mortgage. It helps them to afford a house that is just a little bit nicer.

Should You Get a 40-Year Mortgage?

The short answer is easy: No. Are you nuts? Do you really want to be in debt for close to a half-century?

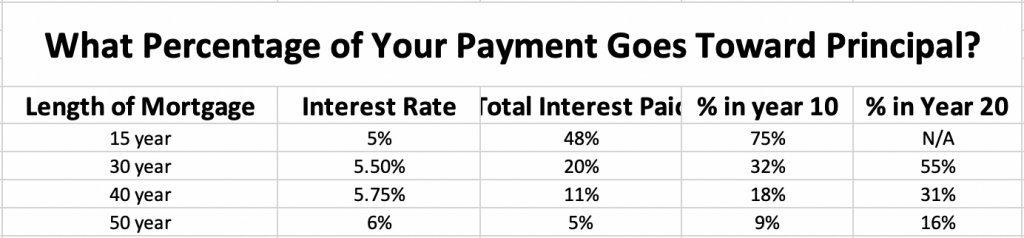

The long answer isn't all that much harder. Consider how much of your payment is going toward principal when you have a 40- or 50-year mortgage. Let's assume that $1 million mortgage we were using earlier, with those same 5%-6% interest rates. How much of that payment goes toward principal in year 1? How about year 10? Year 20?

As you can see, in that first year, only 5%-11% of your payment is going toward principal each month. Even after two decades on that 50-year, only 16% is going toward principal. There is very little difference between a 50-year mortgage payment and an interest-only mortgage payment!

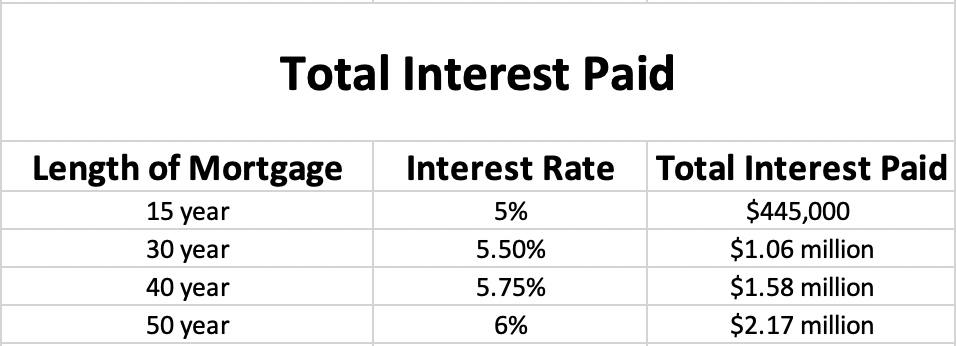

The main reason not to use a 40- or 50-year mortgage is because you'll (almost) never get it paid off. I guess if that doesn't really matter to you and if you can't get an interest-only mortgage for some bizarre reason, then sure, get a 40- or 50-year mortgage. But it certainly matters to me. When we moved into our “doctor house” in 2010, we took out a 15-year mortgage. Then, we paid it off in seven. That was back in 2017. We haven't regretted it yet. When I think I could have been in debt for this house for the next 35-45 years, I just about blow an aneurysm. Still not convinced? Well, how about we add up the interest you'll pay?

My goodness! How would you like to pay for your house not once, but three times! You will pay almost five times as much in interest with a 50-year as with a 15-year mortgage. Sure, there's an opportunity cost there, but just think about what you can do with those 35 years of payments that aren't going to the mortgage lender.

More information here:

6 Reasons the Rich Should Pay Off Their Mortgage Early

Alternatives to a 40-Year Mortgage

What other options do you have besides a 40-year mortgage? Well, I can come up with a decent list of other options.

#1 Get a 30-Year Mortgage

Even on a $1 million mortgage, it only costs you $69 more a month to have a 30-year instead of a 40-year. Find that $69 somewhere else in your budget.

#2 Buy a Less Expensive House

Heaven forbid you don't buy a house right at the limit of affordability for you. Just buy one that costs 7% less.

#3 Put Down More Money

You know what else helps you to keep your payments low? Put down more money. The larger your down payment, the smaller your mortgage and, thus, your mortgage payments. There's no rule that says you can only put down 20%. Maybe you have to wait a few more months to buy while you save up that down payment, but is that really the end of the world?

#4 Move

If you're really considering a 40- 0r 50-year mortgage, you should also be considering moving to a less expensive area of the country. There is a good chance that the cost of your house will go down and that your income taxes will also likely go down. Your income may even go up. The median cost of a house in the Bay Area is $996,000. You know what it is in Biloxi, Mississippi? About $207,000. And they're both on the water. Now I'm not going to pretend that Biloxi is the same as San Francisco. But is San Francisco really five times better (perhaps 10 times better after adjusting for tax and other costs)? Because you're spending like it is.

#5 ARM

An adjustable-rate mortgage often has a lower interest rate than a fixed-interest mortgage, at least for a few years and possibly for the entire length of the mortgage. This can help you to afford more house than you otherwise could with a fixed-rate mortgage. If it is a 5/1 ARM (meaning it is fixed for five years) and you're only going to be there for five years, this could be a no-brainer. Or perhaps you'll be in a dramatically better financial situation five years from now with much more income (like making partner) and fewer liabilities (like student loans.) And you might even refinance between now and then. At any rate, they would be risks that I would be willing to run to get out of debt a decade sooner.

#6 Interest-Only Mortgage

I don't know if this is necessarily better, but at least you're not trying to fool yourself that you're actually making progress on paying off your mortgage.

#7 Rent

Did you know there are many financially successful people who are long-term renters? Some of them even own property; they just don't live in it. While I think buying generally makes sense if you will be in a home for at least five years, it is certainly not mandatory for financial success.

More information here:

Is Renting Better Than Buying? Why We’re Financially Independent and Renting

#8 Use a Home Co-Investment Company

Now there is at least one co-investment company out there (Unison) that will give you 17.5% of your house in exchange for the appreciation on that 17.5% when you sell. I'm not a huge fan of this, but I think I'd still take it over a 40-year mortgage.

Forty- (and 50-) year mortgages might be appropriate for somebody out there. But I hope not, because that means they're in a pretty desperate housing situation. If you have been thinking about taking out a long mortgage like that, I would encourage you to at least consider the listed alternatives.

Don't forget to sign up for the free White Coat Investor Real Estate Newsletter that will alert you to opportunities to invest in private real estate syndications and funds, including most of those I invest in.

What do you think? Would you take out a 40- or 50-year mortgage? Why or why not? Comment below!

The post Should You Get a 40- (or 50-) Year Mortgage? appeared first on The White Coat Investor - Investing & Personal Finance for Doctors.

||

----------------------------

By: The White Coat Investor

Title: Should You Get a 40- (or 50-) Year Mortgage?

Sourced From: www.whitecoatinvestor.com/40-and-50-year-mortgages/

Published Date: Wed, 27 Jul 2022 06:30:46 +0000

Read More

.png) InvestingStocksToolsClubsVideosPrivacy PolicyTerms And Conditions

InvestingStocksToolsClubsVideosPrivacy PolicyTerms And Conditions