<iframe style="width:120px;height:240px;" marginwidth="0" marginheight="0" scrolling="no" frameborder="0" src="//ws-na.amazon-adsystem.com/widgets/q?ServiceVersion=20070822&OneJS=1&Operation=GetAdHtml&MarketPlace=US&source=ss&ref=as_ss_li_til&ad_type=product_link&tracking_id=peaceinvesting-20&language=en_US&marketplace=amazon®ion=US&placement=0060555661&asins=0060555661&linkId=80f8e3b229e4b6fdde8abb238ddd5f6e&show_border=true&link_opens_in_new_window=true"></iframe>|<iframe style="width:120px;height:240px;" marginwidth="0" marginheight="0" scrolling="no" frameborder="0" src="//ws-na.amazon-adsystem.com/widgets/q?ServiceVersion=20070822&OneJS=1&Operation=GetAdHtml&MarketPlace=US&source=ss&ref=as_ss_li_til&ad_type=product_link&tracking_id=peaceinvesting-20&language=en_US&marketplace=amazon®ion=US&placement=1119404509&asins=1119404509&linkId=0beba130446bb217ea2d9cfdcf3b846b&show_border=true&link_opens_in_new_window=true"></iframe>|<iframe style="width:120px;height:240px;" marginwidth="0" marginheight="0" scrolling="no" frameborder="0" src="//ws-na.amazon-adsystem.com/widgets/q?ServiceVersion=20070822&OneJS=1&Operation=GetAdHtml&MarketPlace=US&source=ss&ref=as_ss_li_til&ad_type=product_link&tracking_id=peaceinvesting-20&language=en_US&marketplace=amazon®ion=US&placement=1119376629&asins=1119376629&linkId=2f1e6ff64e783437104d091faaedfec7&show_border=true&link_opens_in_new_window=true"></iframe>

[Editor's Note: You want to know what’s so valuable about working with Jax Wealth Investments? It allows you to invest in new construction in high-growth, desirable neighborhoods that provide a great home for the tenant while also maximizing landlord profit. The Jax Wealth Investments turnkey system walks you through each step of the process of becoming a direct real estate investor without the headaches of managing a property by yourself. Do you want an alternative to the volatile stock market while also hedging against high inflation? Then, check out Jax Wealth Investments today!]

By Dr. James M. Dahle, WCI Founder

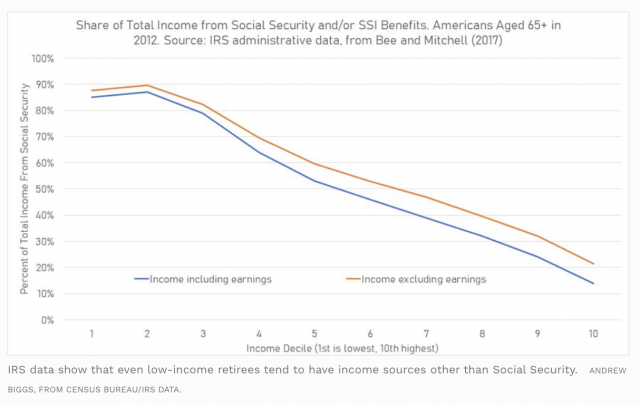

Social Security benefits pay for the lion's share of the retirement of most Americans. According to Forbes contributor Andrew Biggs, a significant number of Americans rely on Social Security for 90% or more of their retirement income.

Even for high-income professionals, the target audience of this blog, Social Security will be a significant portion of retirement spending. For example, if I quit working today and began taking Social Security at age 70, I would get a benefit of about $2,600 a month. If I continue to work until age 70, that benefit will increase to perhaps $3,700 a month. In addition, my wife will be eligible for at least 50% of my benefit. That equals $5,550 per month or $66,600 a year, more than the median American household income.

If a typical physician retires with a $2 million nest egg, that would only support retirement spending of perhaps $80,000 per year. In that sort of scenario, the Social Security income would account for 45% of retirement spending!

How Does Social Security Work?

Since Social Security will make up at least a significant minority of our retirement income, it is important to understand how it works.

Social Security has two progressive features and one regressive feature. The regressive feature is that a high earner only has to pay Social Security taxes (12.4% of earned income—6.2% from the employee and 6.2% from the employer) on a certain amount of earned income. In 2022, that amount is $147,000.

The first progressive feature is that up to 85% of Social Security income is taxed in retirement, but only if you have significant other income (defined as $34,000 single or $44,000 married filing jointly in total income, including the Social Security benefit).

The second progressive feature—the one that says that additional payments result in less and less Social Security benefits—is the one we're going to talk about today.

More information here:

The Consequences of Ignoring Social Security

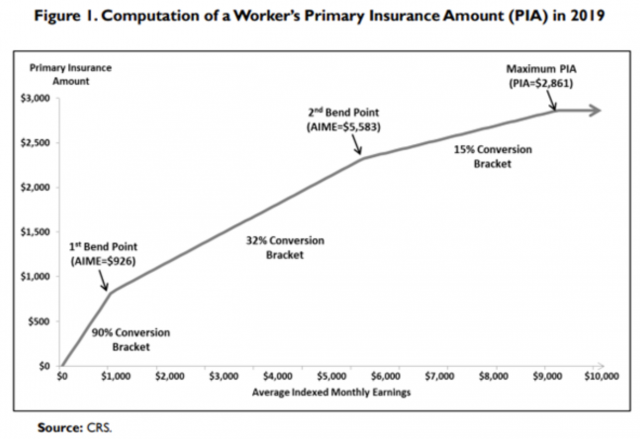

What Are Social Security Bend Points?

While progressive, the additional benefit you get from additional Social Security taxes paid is not a continuous curve. It has two bend points and looks like this chart, via Covisum:

Don't pay too much attention to the numbers on the chart, as they go up each year with inflation. I want you to pay attention to the general shape of the chart and to the axes.

Primary Insurance Amount (PIA): Shown on the Y axis, this is basically the Social Security benefit you will receive.

Average Indexed Monthly Earnings (AIME): Shown on the X axis, the more you earn (and pay SS taxes on), the higher your Social Security benefit.

As you can see, the chart starts out pretty steep. For a while (up to the first bend point), your PIA goes up by 90 cents for every extra dollar of earnings you pay SS taxes on. This is a fantastic investment. Basically, if you are below this bend point and retiring next year, earning an extra $100 a month (and paying 12.4% in SS tax on it) means you (and your employer) are “investing” $100 * 12 * 12.4% = $148.80 in exchange for an annual benefit of $100*12*90% = $1,080! Investing $149 and getting $1,080 EVERY YEAR FOR THE REST OF YOUR LIFE is an incredible investment.

Most Social Security “investments” aren't nearly this good, primarily because you don't make them the year before you start receiving the benefit. But they're still very good, especially below that first break point. Retiring before reaching that first bend point is actually pretty dumb given how awesome of an investment it is.

After your AIME gets past the first bend point, the deal is not nearly as good. Instead of getting credit for 90% of what you earned, you now get credit for only 32% of what you earned. Eventually, you reach the second bend point, where that figure drops even further, to 15% of what you earned.

How Much Do You Have to Earn to Get to the First Bend Point?

Where is that first bend point anyway? Well, it's not very far at all. But to understand exactly where it is, you have to understand how your AIME is calculated.

The first principle to know is that you must work and pay into Social Security for at least 40 quarters (10 years) to get anything from Social Security. Only 39 quarters? Too bad, so sad. Even if you earn and pay SS taxes on a ton of money for nine years, you're not getting squat.

The second principle to understand is that you must earn at least $1,510 (in 2022) per quarter to get credit for it. If you earn at least $1,510 x 4 = $6,040 in a year, you get credit for four quarters that year.

The third principle is that Social Security only counts your best 35 years (420 months). If you didn't earn for at least 35 years, the calculation uses $0 for all of the years you did not earn anything. In that respect, it doesn't matter if you earned just a little for many years or a lot for a few years (as long as it was at least 10 years). It all gets added together.

The fourth principle is that all of your earnings are adjusted for inflation. So, earnings made many years ago are worth more than earnings made in the last few years.

Got all that? OK, let's get started then.

It turns out that in 2022 the first bend point comes at an AIME of $1,024. You must earn and pay taxes on $1,024 per month * 420 months = $430,080 in today's dollars over 35 years to get there, or about $12,288 per year. Alternatively, you could get there in just 10 years if you earned $43,080 per year.

Good news! Most of you aren't going to have any trouble at all reaching the first bend point.

How Much Do You Have to Earn to Get to the Second Bend Point?

We can repeat the exercise for the second bend point. In 2022, the second bend point comes at an AIME of $6,172 in today's dollars. To get there, you're going to have to make a lot more money, and you probably won't do it in just 10 years.

$6,172 per month * 420 months = $2,592,240

You're going to have to earn millions over your career to get to the second bend point, but if you work a full 35 years, that's just $2,592,240/35 = $74,064 per year, certainly not out of reach for a professional who works a full career. What's the fastest you can get there? In 2022, the Social Security wage limit is $147,000. $2,592,240/$147,000 = 17.6 years. You'll basically need to earn at least the Social Security Wage Limit for 18 years.

If you're a physician interested in FIRE but want to make sure you hit that second bend point, you should plan on working at least a decade and a half or so out of training. Remember, you'll get some credit for your work prior to becoming an attending physician.

Maximizing Social Security Benefits

There is actually a third bend point, although few reach it. If you pay SS taxes on the Social Security wage limit every year for 35 years, you get zero credit for any additional earnings. It goes from 90% credit to 32% credit to 15% credit to 0% credit. Where is that point? In 2022, the wage limit is $147,000. Multiply that by 35 years and you get $5,145,000. Divide by 420 and you get an AIME of $12,250. What benefit would you get for that?

Well, you'd get 90% on the first $1,024, 32% on the next $6,172 – $1,024 = $5,148, and 15% on the next $12,250 – $5,785 = $6,465 so

- $1,024 * 90% = $922

- $5,148 * 32% = $1,647

- $6,465 * 15% = $970

- Total = $922 + $1,647 + 970 = $3,539 per month or $42,468 per year

If you're married, your spouse will qualify for at least 50% of your benefit, for a total of $63,702. Now, if you delayed to age 70 instead of taking it at the full retirement age of 67, it would be 24% larger, or $52,660 ($78,990 married).

Yes, that's correct. Earning and paying the exact same tax rate on your last $6,465 only gives you a little bit more than paying on your first $960.

More information here:

10 Reasons NOT to Take Social Security Early

Social Security Calculator: Am I There Yet?

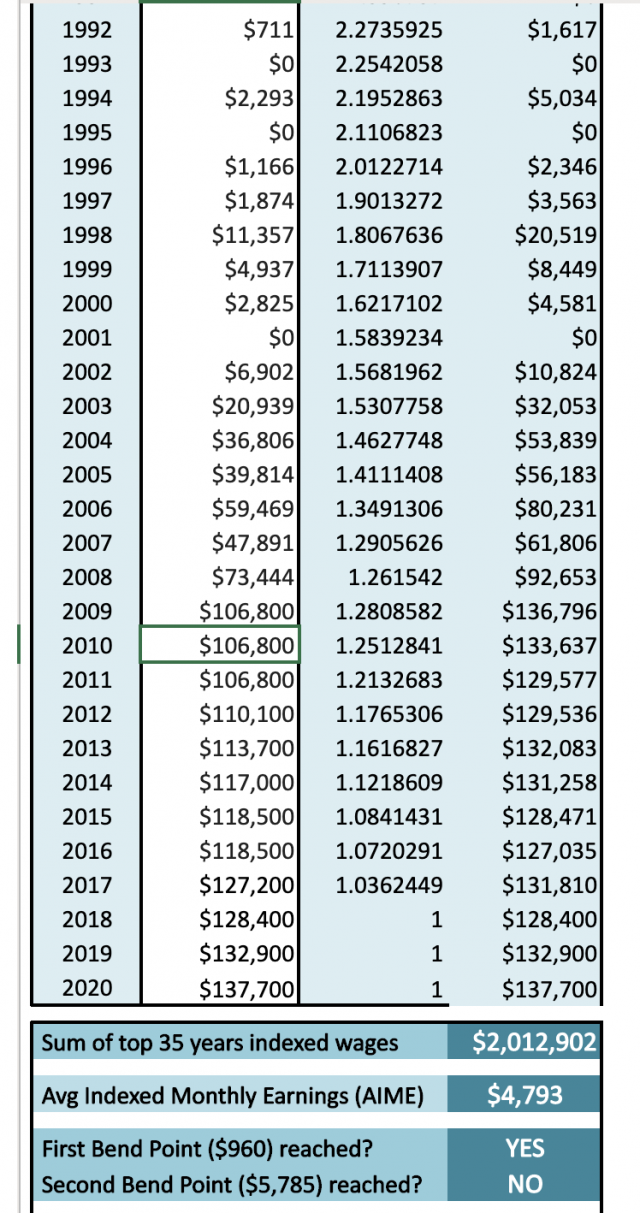

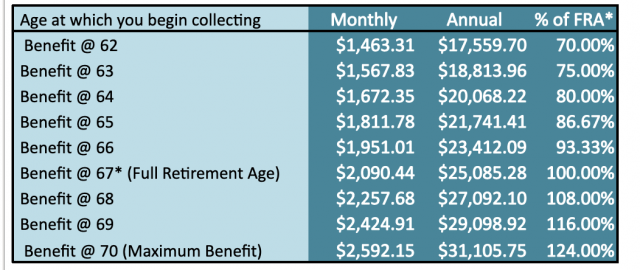

Unsurprisingly, the Physician on FIRE has spent some time thinking about this and has even developed a calculator to help you know when you reach each of the bend points. Just for fun, I put my earnings numbers (get them from your latest Social Security statement available at My Social Security) into his calculator. It spit this out when I first did this in 2020. Keep in mind that the figures for the bend points are slightly lower in this exercise than they are in 2022, but I think it's worth showing you this anyway:

As you can see, my AIME at the time was $4,793, so I was still a little bit below the second bend point of $5,875 and a long way away from maxing out my Social Security benefit. How many years of away was I (assuming I continue to earn more than the Social Security wage limit)? Well, you can get a quick estimate simply by taking $5,785 * 420 = $2,467,500 and subtracting my 35 years of indexed wages ($2,012,902) to get $454,598. Now, divide that by $137,700 and you'll get 3.3 years, about 17-18 years out of residency in my case.

Likewise, I could see how long it would take to maximize my Social Security benefit ($4,819,500 – $2,012,902 = $2,806,598 / $137,700 = Another 20 years and 16-17 years between that second bend point and the maximum level). Feels like a long time to work for not that much more benefit. Maybe there is another way to increase that benefit that doesn't involve working more.

What About My Spouse?

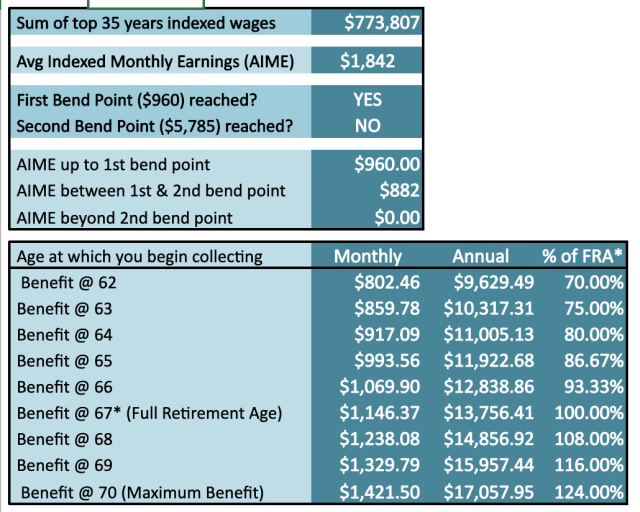

After many years without earnings while we were raising our children, Katie started working for The White Coat Investor a few years ago, allowing her to get to her 40 required quarters. She is now eligible for her own Social Security benefit. But I wondered where she was at in relation to the bend points and especially whether her benefit was higher than 50% of mine. I pulled her Social Security statement and plugged the numbers into the POF calculator, and this is what we ended up with:

As you can see, her AIME was $1,842 and her benefit at 67 would have been $1,146.37. That puts her well past the first bend point but still a long way from the second bend point. My benefit at the time was $2,090.44. Her benefit is now higher than 50% of mine, so at least we're getting something for those additional taxes we're paying.

Knowing where you are in relationship to the Social Security bend points may incentivize you to work a little longer or to retire a little sooner. Either way, it is good to know where you stand.

What do you think? Where are you in relation to the bend points? Will it change how much or how long you work? Comment below!

The post Social Security Bend Points — Maximizing Your Benefit appeared first on The White Coat Investor - Investing & Personal Finance for Doctors.

||

----------------------------

By: The White Coat Investor

Title: Social Security Bend Points — Maximizing Your Benefit

Sourced From: www.whitecoatinvestor.com/social-security-bend-points/

Published Date: Sat, 20 Aug 2022 06:30:08 +0000

Read More

.png) InvestingStocksToolsClubsVideosPrivacy PolicyTerms And Conditions

InvestingStocksToolsClubsVideosPrivacy PolicyTerms And Conditions