<iframe style="width:120px;height:240px;" marginwidth="0" marginheight="0" scrolling="no" frameborder="0" src="//ws-na.amazon-adsystem.com/widgets/q?ServiceVersion=20070822&OneJS=1&Operation=GetAdHtml&MarketPlace=US&source=ss&ref=as_ss_li_til&ad_type=product_link&tracking_id=peaceinvesting-20&language=en_US&marketplace=amazon®ion=US&placement=0060555661&asins=0060555661&linkId=80f8e3b229e4b6fdde8abb238ddd5f6e&show_border=true&link_opens_in_new_window=true"></iframe>|<iframe style="width:120px;height:240px;" marginwidth="0" marginheight="0" scrolling="no" frameborder="0" src="//ws-na.amazon-adsystem.com/widgets/q?ServiceVersion=20070822&OneJS=1&Operation=GetAdHtml&MarketPlace=US&source=ss&ref=as_ss_li_til&ad_type=product_link&tracking_id=peaceinvesting-20&language=en_US&marketplace=amazon®ion=US&placement=1119404509&asins=1119404509&linkId=0beba130446bb217ea2d9cfdcf3b846b&show_border=true&link_opens_in_new_window=true"></iframe>|<iframe style="width:120px;height:240px;" marginwidth="0" marginheight="0" scrolling="no" frameborder="0" src="//ws-na.amazon-adsystem.com/widgets/q?ServiceVersion=20070822&OneJS=1&Operation=GetAdHtml&MarketPlace=US&source=ss&ref=as_ss_li_til&ad_type=product_link&tracking_id=peaceinvesting-20&language=en_US&marketplace=amazon®ion=US&placement=1119376629&asins=1119376629&linkId=2f1e6ff64e783437104d091faaedfec7&show_border=true&link_opens_in_new_window=true"></iframe>

By Josh Katzowitz, WCI Content Director

If my psychiatrist wife hadn’t begun taking care of our money and our investing strategy so many years ago and if I hadn’t made a New Year’s resolution in 2020 to dive into the world of finances, I shudder to think about where our retirement savings would be.

I’ve been thinking about that lately, especially after I read a recent Fidelity study about the retirement preparedness of Americans. If my wife hadn’t gotten financially literate, would we be maxing out our retirement accounts every year? Would we have started Roth IRAs and then learned how to squeeze through the backdoor? Would we be prepared? Thank goodness that her ingenuity and planning (and my eventual motivation to become financially literate) have brightened our future. But what about other white coat investors? What about the rest of America?

According to Fidelity in a study titled Retirement Preparedness During Uncertain Times, the news isn’t great.

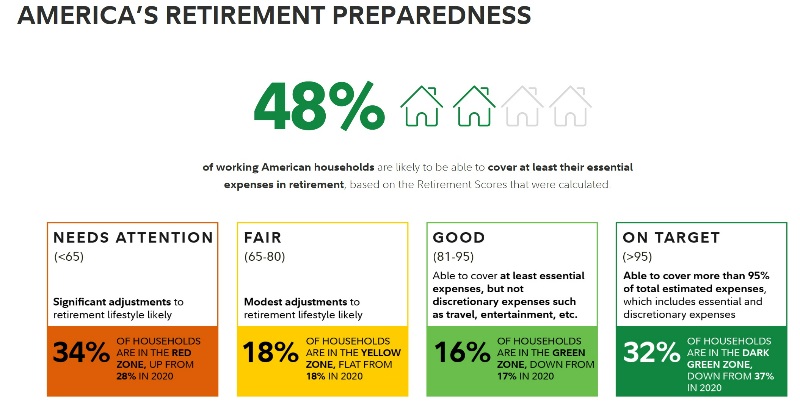

The survey included more than 3,500 responses, and it showed that in the post-pandemic world “amid continued volatility,” more than half of those who were surveyed are not on target and “face modest to significant adjustments to their planned retirement lifestyle if they don’t take action to make up for the shortfall.” The last time Fidelity put together a report like this, 46% of people weren’t ready for retirement. This year, it’s 52%.

Here's a breakdown, via Fidelity.

Yes, Americans seem less prepared for retirement than the last time their pulse was taken. But if you’re a high earner or have enough financial literacy to be reading this website, you’re probably in a better spot than most Americans.

“It is not even close; they are definitely in a better spot,” Konstantin Litovsky—the founder of WCI-recommended Litovsky Asset Management, which offers comprehensive retirement plan advisory and investment management services—told me last week. “But they face very different challenges. I may be biased since we mostly work with doctors and dentists who are in the 1%, but for them (at least in the first 10-15 years after graduation), the biggest concern is paying down debt—which includes student loans, real estate loans (including primary residence and/or office building where their practice is located), and practice loans (which is more of a concern for dentists). So, the biggest hurdle for doctors and dentists would be the high level of debt they have accumulated before they start to make good money.”

Doctors might not have the same money problems as those who earn less, but that doesn’t mean they’re 100% ready for their post-work lives either.

The Numbers for Retirement Preparedness Are Scary

The retirement numbers are concerning—and at the very least, it should cause you (like it’s caused me) to think about how to make sure you don’t fall into that 52% (or if you are there, how to escape that category).

According to Fidelity, the Baby Boomer generation (born between 1948-64), the last generation that could reliably rely on a defined benefit pension plan, is in a good spot. Generation X (born between 1965-80), which could still have decades of earning years but which has had to deal with the complexity and planning of more 401(k) style retirement plans, is not far behind the Baby Boomers. But the Millennial generation (born between 1981-96), with a savings rate of 9.5%, is struggling with its readiness.

Even with those alarming numbers, 83% of US workers are confident that their retirement goals will be met and 74% believe they’ll have “at least a somewhat comfortable lifestyle in retirement.” Interestingly, Gen Y and Z are more confident about that than either Gen X or Baby Boomers. While Gen X has a savings rate higher than either of the generations it’s sandwiched between, that number is still only 11.1%.

A National Institute on Retirement Security (NIRS) report on Gen X’s preparation says the retirement outlook is “dismal.” The bottom 50% of earners have “only a few thousand dollars saved for retirement,” and the median amount of retirement savings in the households from that generation is only $40,000. Even high earners might only have a few hundred thousand set aside for retirement.

“The data pretty clearly indicates that the system we have in place now will not provide adequate income for many workers,” Tyler Bond, the NIRS research director and a co-author of the study, said, via CNN.

Are those numbers scary and sobering? No doubt. But are they apocalyptic? Litovsky says no.

“While the numbers may seem concerning, the overall picture is most likely a lot less concerning if all of the details are taken into account,” he said. “The standard of living for those in the lower income brackets is also usually lower. Many people will end up with jobs in retirement, so there is really no such thing as fully retiring, even for those who may have pensions or other sources of income in addition to Social Security. We live in Sarasota, Florida—which has a higher proportion of retirees and older people—and while there are some who are happy living on a fixed income, many work part-time. There is also the family structure, which can help mitigate some of the issues related to lack of retirement assets. Family members tend to help each other, and assets are passed on over time. Social Security/Medicare will definitely help.”

More information here:

How to Build an Investment Portfolio for Long-Term Success

How to Start Saving for Retirement

Is Now a Good Time to Retire? Here’s What Christine Benz Thinks

What to Do If You’re Not on Track for Retirement

To increase Americans' preparedness, Fidelity recommends a trio of actions, including 1) aiming to save at least 15% of pre-tax income each year; 2) making sure you have the right asset allocation of stocks, bonds, and cash based on your comfort in taking portfolio risk; and 3) reevaluating your retirement plan and perhaps deciding to work past the median retirement age of 65.

Some of that advice fits into the well-established WCI philosophy espoused by Dr. Jim Dahle. He’s recommended saving 20% of your gross income (instead of 15%), but both goals are good. Asset allocation is awfully important (whether it’s the typical 60/40 stock-to-bond ratio or if you feel more comfortable having a higher percentage of equities or perhaps real estate). While WCI would rather you take Social Security at 70 instead of 62, we’d hate for high earners to have to work full-time past the date that they want to retire.

But if you earn a physician’s income, Litovsky has other tips if you’re worried about your retirement. He said:

“1) Prioritize repaying debt. If you are a small practice owner, work hard to increase your revenue and net profit so that you are not buried in debt. You might not need to work at this level for long, just long enough to pay down all debt fast and to put money away for retirement.

2) Avoid buying more house than necessary. This one can't be emphasized enough.

3) Start planning as soon as possible. This is especially true for those who may not feel comfortable managing their own finances. Reach out and get help if you need it. Learn as much as you can about the details so that you know what good advice looks like.”

As Litovsky notes, many WCI readers will have different challenges than most other Americans. They come out of medical school (or other kinds of graduate school) and could owe hundreds of thousands of dollars of student loans. They might contend with lifestyle creep. They live in high tax brackets. All of that can hinder their retirement savings.

“WCI readers have very different challenges than most other people,” Litovsky said. “They have to make good decisions with their money, as it is very easy to end up with high debts and an income that's not high enough. I've seen this happen, and it is a result of making poor financial decisions. The consequences for making bad financial decisions are a lot more severe for WCI readers, so it is even more important for them to be on top of their finances.”

Even with six- or seven-figure salaries, it’s imperative for high earners to plan for retirement. As Jim has pointed out repeatedly, one-fourth of doctors in their 60s aren’t even millionaires (and only about 1 in 6 have more than $5 million). Maybe picturing the struggle to scratch through retirement is only a fleeting thought for you and me. But that doesn’t mean it couldn’t one day become a reality.

Money Song of the Week

For some reason, I was thinking about Morphine this week. It was an interesting rock band (no guitar player; only a bassist/singer, drummer, and saxophonist who often played two instruments at once), and I became a fan when I saw Morphine play a side stage gig at the H.O.R.D.E. Festival in 1995. The band never got all that big commercially, and even nearly 25 years after the on-stage death of bassist/singer Mark Sandman (who died of a heart attack in Italy at the age of 47), the band’s legacy continues on with its existing fan base.

I always liked the “low rock” style of the band, and I liked Sandman’s laid-back baritone vocals (plus the fact he played a two-string slide bass was super cool). Listening to Morphine was like meandering through a modern-day jazz/blues daydream with the shrill sax acting as the sun constantly breaking through the clouds, whether you wanted it to or not.

Take, for instance, its 1995 song, “Free Love.” Sandman’s singing sits in the background, partially obscured by the soaring sax and the low rumbling of the rhythm section. Meanwhile, Sandman tries to make the point that there’s no free lunch when it comes to romance.

As Sandman sings,

“Free love, ow, I can't stand; it's a panic/Normally love costs a bundle and plenty of trouble/But you fooled me, you fooled me/You ran away to Italy/You fooled me.

“Yeah, you fooled me, you fooled me/You ran away to Italy/With your psychiatrist who's now a scientologist/Oh! I should have foreseen this/Business with your psychiatrist.”

Sandman goes on to sing that love is expensive, and if somebody offers it for free, you should “run for the cynical arms of a stranger” and “run for the open arms of an unknown tomorrow.”

And yes, beware of falling in love with and running away with a psychiatrist.

Tweet of the Week

A few months ago, we wrote about whether it’s OK for doctors to organize and strike. This week, the biggest healthcare strike in US history began when 75,000 Kaiser Permanente workers walked off the job and formed picket lines. Physicians were not involved in the three-day strike.

Are you worried about your retirement preparedness? Do the above statistics surprise you? How can you ease your mind about your future? Comment below!

[Editor's Note: For comments, complaints, suggestions, or plaudits, email Josh Katzowitz at [email protected].]

The post Some Sobering (and Scary) Statistics on People’s Retirement Preparedness appeared first on The White Coat Investor - Investing & Personal Finance for Doctors.

||

----------------------------

By: Josh Katzowitz

Title: Some Sobering (and Scary) Statistics on People’s Retirement Preparedness

Sourced From: www.whitecoatinvestor.com/american-retirement-preparedness-statistics/

Published Date: Sun, 08 Oct 2023 06:30:44 +0000

Read More

Did you miss our previous article...

https://peaceofmindinvesting.com/investing/what-is-your-annualized-real-return

.png) InvestingStocksToolsClubsVideosPrivacy PolicyTerms And Conditions

InvestingStocksToolsClubsVideosPrivacy PolicyTerms And Conditions