<iframe style="width:120px;height:240px;" marginwidth="0" marginheight="0" scrolling="no" frameborder="0" src="//ws-na.amazon-adsystem.com/widgets/q?ServiceVersion=20070822&OneJS=1&Operation=GetAdHtml&MarketPlace=US&source=ss&ref=as_ss_li_til&ad_type=product_link&tracking_id=peaceinvesting-20&language=en_US&marketplace=amazon®ion=US&placement=0060555661&asins=0060555661&linkId=80f8e3b229e4b6fdde8abb238ddd5f6e&show_border=true&link_opens_in_new_window=true"></iframe>|<iframe style="width:120px;height:240px;" marginwidth="0" marginheight="0" scrolling="no" frameborder="0" src="//ws-na.amazon-adsystem.com/widgets/q?ServiceVersion=20070822&OneJS=1&Operation=GetAdHtml&MarketPlace=US&source=ss&ref=as_ss_li_til&ad_type=product_link&tracking_id=peaceinvesting-20&language=en_US&marketplace=amazon®ion=US&placement=1119404509&asins=1119404509&linkId=0beba130446bb217ea2d9cfdcf3b846b&show_border=true&link_opens_in_new_window=true"></iframe>|<iframe style="width:120px;height:240px;" marginwidth="0" marginheight="0" scrolling="no" frameborder="0" src="//ws-na.amazon-adsystem.com/widgets/q?ServiceVersion=20070822&OneJS=1&Operation=GetAdHtml&MarketPlace=US&source=ss&ref=as_ss_li_til&ad_type=product_link&tracking_id=peaceinvesting-20&language=en_US&marketplace=amazon®ion=US&placement=1119376629&asins=1119376629&linkId=2f1e6ff64e783437104d091faaedfec7&show_border=true&link_opens_in_new_window=true"></iframe>

By Dr. Jim Dahle, WCI Founder

There is a lot of discussion out there these days about securities lending income programs being offered by major brokerages. Let's talk about what's going on so you can make an informed decision about whether you want to participate.

What Is Securities Lending?

Securities lending is exactly what it sounds like. The owner of a security—let's say a share of stock—lends it to a borrower. In exchange, the borrower posts collateral for the loan (shares of stock, bonds, or just cash) AND pays the lender a fee. The borrower is contractually obligated to return the borrowed security on demand. These shares can be in a tax-protected account or in a taxable account.

Why Would Someone Borrow a Security?

It's usually not some person. Instead, it's an institution, such as a mutual fund, hedge fund, brokerage, or pension. In fact, the lender is also usually an institution. But there are four main reasons why a security may be borrowed:

- Cover a short position

- Hedge an investment position

- Arbitrage

- Gain voting rights

My impression is that most securities lending/borrowing is done to support shorting the security.

More information here:

The Nuts and Bolts of Investing

The Ethics of Investing

How Does Shorting a Stock Work?

When you short a stock, you are betting that it will go down in value. You first sell the stock. But how do you sell something you don't even own yet? You borrow it. So, you borrow the share; then you sell it. You wait a little while for it to go down in value, and then you buy it and give it back to the lender. If you sell the share at $10 per share and then buy it at $7 a share, you're going to come out ahead, even after paying some interest to the lender.

Interestingly, short sellers are not entitled to the dividends of the stock. They have to pay them to the owner of the share, i.e. the person or institution they borrowed the shares from. That's an additional cost of short selling.

Why Would Someone Lend a Security?

The main reason someone would lend a security is to earn that extra income, i.e. the fees or interest that the borrower pays to the lender. Since they can demand the shares back at any time and they have collateral, there isn't a lot of risk there. They don't even lose the dividends.

You Mean There's No Risk to This at All?

There are no free lunches in life, and securities lending is no exception. There is counterparty risk there. That is the risk that the person who borrowed the shares from you cannot or will not pay them back to you. True, you have the collateral, but sometimes the collateral goes down in value. This happened quite a bit in 2008-2009.

Collateral reinvestment risk is generally considered to be much higher than counterparty risk due to the protections in place (often requiring more than 100% collateral). In addition, the Securities Investor Protection Corporation (SIPC) does not cover securities that are lent out. While that protection is not nearly as important as FDIC/NCUA protection at banks and credit unions, it's not worthless either. You also lose your voting rights on those shares. The dividends you receive are actually now called “cash-in-lieu” payments, and they may not get the same tax treatment. Basically, you pay ordinary income tax rates on cash-in-lieu payments, at least in a taxable account. However, there seems to be a trend where the brokerages make this up to you as the lender, although I'm sure they're not eating that cost.

Don't My Index Funds Already Do This?

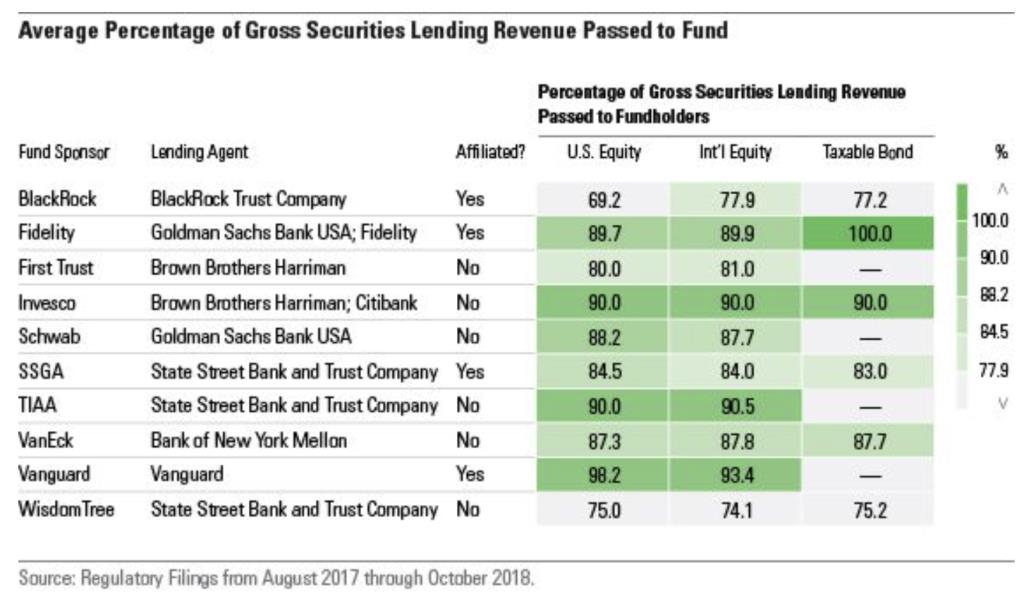

Absolutely they do. Most mutual funds, including Vanguard index funds, engage in securities lending. The extra income can be used to offset the expenses of running the fund or to boost profits for the mutual fund company. Interestingly, not every company passes all of that income along to the fund investors. Adam McCullough of Morningstar took a look at this in 2018, and this is what he found:

As you can see, there's a pretty wide variation. Vanguard passed along 98% of its securities lending income. Fidelity did 90%. Schwab 88%. State Street 85%. BlackRock 69%. Index funds and their ETF counterparts are not the same, and this is a significant difference. If this is what it looks like for the “good” fund companies out there, imagine what it looks like for all those companies offering loaded, high-expense ratio, actively managed funds. Interestingly, back in 2013, BlackRock was keeping 35% of the income and was sued for it for breach of fiduciary duty. BlackRock won the suit.

Is Vanguard Being Careful?

Mutual funds have regulations that require them to be careful.

The guidelines include:

-

- Limits on lending: The value of securities on loan at any one time may not represent more than one-third of the fund’s value. Separate analyses by the Investment Company Institute (ICI) and Rowley (2016) have found that, in practice, funds lend far less.

- Collateral: The borrower must pledge collateral equal to at least 100% of the security’s value. As noted on page 3, funds and other lenders generally demand collateral equal to 102% or 105% of the security’s value. The values are marked to market daily. If the value of the loaned securities rises, the borrower must provide additional collateral.

- Collateral reinvestment: The fund should reinvest cash collateral in securities that offer maximum liquidity and reasonable return. “In practice, US-regulated funds most often invest cash collateral in money market funds” (ICI, 2014).

- Loan termination: The loan is subject to termination by the fund at any time.

- Reasonable return: The fund must earn a reasonable return on the loan, including any distributions from the loaned security.

- Corporate governance: When the fund lends a security, its voting rights pass to the borrower. If fund management knows of a “material” vote, fund directors should recall the loaned securities to vote the proxies.

Vanguard also gives the following assurances:

“Our program seeks to capture the scarcity premium found in hard-to-borrow securities. We minimize risk in the reinvestment of cash collateral by investing in a money market fund managed by Vanguard Fixed Income Group. The fund’s average weighted maturity is capped at 60 days.

Outside the United States, Vanguard accepts sovereign debt as non-cash collateral and invests any cash collateral in overnight repurchase agreements, subject to daily monitoring by Vanguard’s Risk Management Group.

Vanguard has developed a monitoring program and lending limits for individual securities to ensure that any securities on loan can be recalled for important proxy votes. To reduce the risk of counterparty default, Vanguard lends to a limited number of preapproved broker-dealers and maintains strict internal guidelines on the aggregate dollar amount of loans to any one borrower.

In addition, Vanguard ensures proper collateral coverage by valuing the loaned securities on a daily basis—using current market prices—and by calling for additional collateral when necessary to bring the coverage up to the 102% or 105% floors for US or foreign securities, respectively. Vanguard’s agency agreement requires the lending agent to indemnify our fund in the case of a counterparty default by replacing either the security or the security’s current market value to the fund.

Consistent with Vanguard’s client-owned structure, Vanguard returns all net lending revenues—after subtracting program costs, agent fees (on non-US securities), and any broker rebates—to the funds. In 2015, program costs amounted to about 5% of gross revenue.”

Seems reasonable to me.

More information here:

Why Vanguard?

Securities Lending Programs

At least three popular brokerages offer programs where you can do this yourself above and beyond what your fund managers are doing.

- Charles Schwab

- Fidelity

- Interactive Brokers

How Does Securities Lending Work at Schwab?

At Schwab, you can lend your securities as long as you have at least $100,000 invested at Schwab. The collateral is in cash. There are no trading restrictions on the loaned security, and you split the income 50/50 with Schwab. This is not necessarily a new program. In 2022, Schwab reported in a letter to the SEC that it's been doing this since 2005 and that it has 25,000 clients with $40 billion in market value doing it. Schwab now owns TD Ameritrade, which has a similar program.

Some redditors who own difficult-to-borrow individual stocks report being paid as much as 300% in interest for a few days or months on stocks they have lent out. Schwab apparently approaches its investors who own these difficult-to-borrow shares to encourage them to enroll in the program. Presumably, the ETF shares that most white coat investors would own would not be nearly as difficult to borrow and, thus, would not pay nearly as much. The redditors did express concern about providing the shares to hedge funds that were helping to drive down the price of their investments and thought they might not actually be coming out ahead because of that.

How Does Securities Lending Work at Fidelity?

Fidelity has a lower minimum than Schwab, just $25,000 invested. The collateral is in cash held at a third-party bank. There are no trading restrictions. Interestingly, Fidelity tries to get your shares back to you before the ex-dividend dates so you don't get cash-in-lieu payments. If Fidelity can't, it'll pay you the difference. It was not clear to me what the split is of the income between you as the investor and Fidelity, but Fidelity is very clear that it's making money on this program. Redditors note that even though they may have 60 stocks in their account, only 1-3 of them are typically lent out at any given time. One redditor insightfully summed up all of these programs in one line:

“I started this recently. Just know that there aren't many major disadvantages, but the advantage is also very little because you get paid extremely little too.”

How Does Securities Lending Work at Interactive Brokers?

Interactive Brokers (IB) calls its program the “Stock Yield Enhancement Program.” Like Schwab, it supposedly splits the income with you 50/50 (although I have read accounts, including one below, where the split seemed to be 2/3 to IB, so watch that). It has a $50,000 minimum or margin account approval (which requires a $110,000 minimum). There are no trading restrictions. Redditors had all kinds of bad things to say about this program, although it doesn't appear to operate much differently from that of Fidelity or Schwab. In the past, IB did not make up the difference in taxes for those cash-in-lieu payments, but it appears that has been rectified. Here are some quotes from the redditors:

“I turned it off after I figured out the taxes on payments in lieu of dividends were costing me more than the interest received.”

“I’ve had it turned on for several months, but none of my stocks have ever been lent out. I have pretty common/high volume stocks.”

“I use it, the more common stock don't really get lent out. I currently got RIOT in my portfolio which is quite often lent out. But it's usually returned on the same day. On roughly 700 shares, I collect about $3-$4 a month.”

“If you make money with that, it means you have many crap stocks in your portfolio!”

“My annual yield is like 0.00025 lol but still free money.”

You can also find a Bogleheads thread or two on the subject, such as this one from 2020.

“The return is not magnificent: about 0.02% of my assets per annum, if I calculate correctly. Still, it is free money, and would add almost 1% to my safe withdrawal amount forever.”

“I don't hold any stocks, only ETFs. In that account I have EMGF, GSLC, IEMG, REET, RZV. I earn anywhere from $3 a month to $380 a month. But it depends massively on your portfolio size (obviously) and what you hold. I don't think my IEMG has ever been borrowed, for instance. What gets borrowed also changes substantially over time. From February to April, EMGF was borrowed heavily. But no one has borrowed any of it since September.”

“Well I had SYEP turned on for all of May and it earned me $17.14 on about a $70,000 investment. So that's ummm . . . pretty small . . . but it feels like free money. I hold NTSX, VXUS, and EDV. EDV was never lent out at all. VXUS was loaned out at least half the days, but earns IB only 1% and you 0.5%. NTSX was only loaned out four days but earns IB 7.5% and you 3.75% . . . so despite the infrequent lending, it accounted for at least two-thirds of the interest received.”

“Yes, that seems about right: somewhere around 0.3% return. The way I look at it, assuming the 0.3% holds steady (which I doubt, I think it is high now [this was 2020] due to all the volatility) and in retirement I withdraw 3% after taxes, this will let me withdraw an extra 10% indefinitely. That's not too bad. My Value ETFs got shorted a ton in the previous months, and it turned out that they were right.”

There is a cool link where you can see the securities that are most likely to be borrowed at ridiculously high interest rates.

Sure feels like a list of stocks not to own, though. Presumably, there is a reason people are shorting these stocks.

Is Securities Lending Worth It?

It seems to me that this is priced just about right. You get a little bit of extra income in exchange for taking on a little bit of extra risk. However, it doesn't seem to me that the extra complexity is worth it. I think the additional income from a portfolio like those I typically recommend is not going to add much to your retirement. I think I'm just going to let the experts at Vanguard do what they can in this regard and help use it to keep my expense ratios low. This is one more reason I prefer Vanguard index funds, though.

What do you think? Are you participating in one of these programs? Which one? What has your experience been like? Comment below!

The post Securities Lending — Extra Income or a Mirage? appeared first on The White Coat Investor - Investing & Personal Finance for Doctors.

||

----------------------------

By: The White Coat Investor

Title: Securities Lending — Extra Income or a Mirage?

Sourced From: www.whitecoatinvestor.com/securities-lending/

Published Date: Wed, 06 Dec 2023 07:30:50 +0000

Read More

Did you miss our previous article...

https://peaceofmindinvesting.com/investing/how-i-failed-and-then-mastered-the-backdoor-roth-ira

.png) InvestingStocksToolsClubsVideosPrivacy PolicyTerms And Conditions

InvestingStocksToolsClubsVideosPrivacy PolicyTerms And Conditions