<iframe style="width:120px;height:240px;" marginwidth="0" marginheight="0" scrolling="no" frameborder="0" src="//ws-na.amazon-adsystem.com/widgets/q?ServiceVersion=20070822&OneJS=1&Operation=GetAdHtml&MarketPlace=US&source=ss&ref=as_ss_li_til&ad_type=product_link&tracking_id=peaceinvesting-20&language=en_US&marketplace=amazon®ion=US&placement=0060555661&asins=0060555661&linkId=80f8e3b229e4b6fdde8abb238ddd5f6e&show_border=true&link_opens_in_new_window=true"></iframe>|<iframe style="width:120px;height:240px;" marginwidth="0" marginheight="0" scrolling="no" frameborder="0" src="//ws-na.amazon-adsystem.com/widgets/q?ServiceVersion=20070822&OneJS=1&Operation=GetAdHtml&MarketPlace=US&source=ss&ref=as_ss_li_til&ad_type=product_link&tracking_id=peaceinvesting-20&language=en_US&marketplace=amazon®ion=US&placement=1119404509&asins=1119404509&linkId=0beba130446bb217ea2d9cfdcf3b846b&show_border=true&link_opens_in_new_window=true"></iframe>|<iframe style="width:120px;height:240px;" marginwidth="0" marginheight="0" scrolling="no" frameborder="0" src="//ws-na.amazon-adsystem.com/widgets/q?ServiceVersion=20070822&OneJS=1&Operation=GetAdHtml&MarketPlace=US&source=ss&ref=as_ss_li_til&ad_type=product_link&tracking_id=peaceinvesting-20&language=en_US&marketplace=amazon®ion=US&placement=1119376629&asins=1119376629&linkId=2f1e6ff64e783437104d091faaedfec7&show_border=true&link_opens_in_new_window=true"></iframe>

By Francis Bayes, WCI Columnist

When I started “investing” by buying index funds, my portfolio included VNQ: one of the low-cost, broad-market index ETFs of publicly traded REITs. I had public REITs, aka Real Estate Investment Trusts, because (1) I was excited about maximizing diversification, (2) I felt that I could not go wrong by imitating Dr. Jim Dahle's portfolio (he has 20% of his portfolio in real estate, including some in REITs); and (3) Rick Ferri’s All About Asset Allocation–one of the first investing books that I read–recommended the asset class.

But as I read more books and blogs on investing (like William Bernstein, JL Collins, and Mike Piper), I questioned the complexity of my asset allocation as I learned the value of simplicity. Each asset (or sub-asset) class came with a baggage of questions. Will this asset outperform a total stock market fund, like VTI? Am I buying the best ETF in its class? Should I over- or underweight it this year? After a few years, my own second-guessing annoyed me, and public REITs were the biggest culprit.

In January 2022, as I bought stocks in lump sum in our Roth IRAs, I shed public REITs from my portfolio (maybe I should have sold off crypto, too!)

Although I was selling them high (not low) relative to VTI, I replaced VNQ with VTI because of the following five reasons that I explain below. This column is for those who are writing their financial plan and deciding on the asset allocation for their retirement portfolio. If you own public REITs, you should buy them according to your financial plan because changing your asset allocation can be costly unless you are early in the accumulation phase. Many good portfolios include public REITs. If you don’t own public REITs, I hope my column is not counterproductive.

(Disclaimer: I have no disclosures, but The White Coat Investor has financial incentives to promote some of the real estate investments that I discuss later in the column. Here's what WCI's real estate partners can offer.)

Featured Real Estate Partners

RealtyMogul

Type of Offering:

Platform / REIT

Primary Focus:

Multi-Family

Minimum Investment:

$5,000

Year Founded:

2012

MLG Capital

Type of Offering:

Fund

Primary Focus:

Multi-Family

Minimum Investment:

$50,000

Year Founded:

1987

Origin Investments

Type of Offering:

Fund

Primary Focus:

Multi-Family

Minimum Investment:

$50,000

Year Founded:

2007

DLP Capital

Type of Offering:

Fund

Primary Focus:

Multi-Family

Minimum Investment:

$200,000

Year Founded:

2008

Wellings Capital

Type of Offering:

Fund

Primary Focus:

Self-Storage / Mobile Homes

Minimum Investment:

$50,000

Year Founded:

2014

Trion Properties

Type of Offering:

Fund

Primary Focus:

Multi-Family

Minimum Investment:

$50,000

Year Founded:

2005

The Peak Group

Type of Offering:

REIT

Primary Focus:

Single Family

Minimum Investment:

$25,000

Year Founded:

2000

JAX Wealth Investments

Type of Offering:

Fund / Turnkey

Primary Focus:

Single Family

Minimum Investment:

$100,000

Year Founded:

2017

* Please consider this an introduction to these companies and not a recommendation. You should do your own due diligence on any investment before investing. Most of these opportunities require accredited investor status.

#0 Public REITs Tilt Toward, Not Add, Real Estate in the Portfolio

In part because public REITs are so easy to buy, one thinks that buying more public REITs is akin to “adding real estate” to their portfolio. But most, if not all, of VNQ’s 167 companies are already a part of the total stock market (e.g., 3.85% of VTI). When one allocates 5%-25% of their portfolio to public REITs, they are “tilting,” not adding.

#1 Public REITs May Not Improve the Portfolio’s Return

To determine whether one should tilt toward public REITs, one often compares their past performance to that of the broader stock market even though “past performance does not guarantee future results.” They might compare 20-year returns or returns since 2000, both of which happen to start near the peak of the dot-com bubble. Or they might read about the outperformance of the Nareit REIT index relative to the S&P 500 since the former’s inception in 1972 (which was the year before the stock market had its worst decade since the Great Depression).

But how about 10-year returns? Why not compare the returns since the stock market bottom during the 2008 financial crisis? Different start dates can lead to opposing conclusions. Even Nareit, which is an industry group representing REITs, has the integrity to not mention their own index’s “outperformance” on its website.

I have no idea how public REITs will perform relative to the S&P 500 or a total stock market fund in the future. I continue to tilt toward small-cap value (SCV) stocks based on studies of past performance, as well, but I have more confidence in the SCV because the timeframe of such studies predates 1972 and one can explain the outperformance in different ways. If you think that public REITs will outperform, then I have neither the ability nor the will to convince you otherwise.

More information here:

Real Estate Investing 101

#2 Public REITs May Not Provide Diversification

When one considers adding real estate to their portfolio of stocks and bonds, they hope for two things: (1) a higher return than that of either asset; and/or (2) a positive return when both assets have negative or zero returns. If one wants to add public REITs for a negative or low correlation to stocks, then I have seen limited evidence. Similar to those of sub-asset classes within stocks (e.g., SCV, international stocks), the correlation of public REITs with large-cap stocks (essentially, S&P 500) has been increasing to around 0.75. Maybe the correlation of public REITs will decrease to near their historical average of 0.59. But buyers beware: when the stock market crashes, public REITs will likely crash as well.

#3 TBD: Public REITs May Not Outperform with Inflation

One year cannot tell the whole story, but so far in 2022, the YTD returns for ETFs of public REITs are either worse or nearly identical to that of the S&P 500. If one focuses on the years when inflation exceeded 4%, REITs outperformed stocks, so the pattern could continue in 2022—or in 2023 if inflation continues to exceed 4%. In his book, Rational Expectations, Bernstein suggests that the dividend yield of REITs, which predicts future returns, grows more slowly than inflation because REITs cannot reinvest more than 10% of their earnings.

#4 Public REITs Are Not Representative of ‘Real Estate'

Because we say that we own the entire stock market when we buy VTI or VTSAX, you might think that you own the entire real estate market when you buy public REIT ETFs, such as VNQ or FREL. But you only end up owning a slice. According to Nareit, the size of the professionally managed real estate market (including both residential and commercial) is approximately $4.5 trillion, of which publicly held REITs own around $3 trillion. In contrast, the size of the commercial real estate market exceeded $20 trillion in 2021, and the residential real estate market is also in the trillions. If we focus on “REIT-like properties” that Nareit defines as institutional-grade properties, then public REITs own about 20% of such commercial properties.

When one tilts toward public REITs, they concentrate in two ways: (1) 100-200 companies among thousands in the US and (2) less than 20% of the real estate market that such companies can own. By comparison, domestic small-cap value index funds own anywhere from 172 to more than 1,400 stocks. The risk of such concentration with public REIT ETFs is much greater than that of SCV.

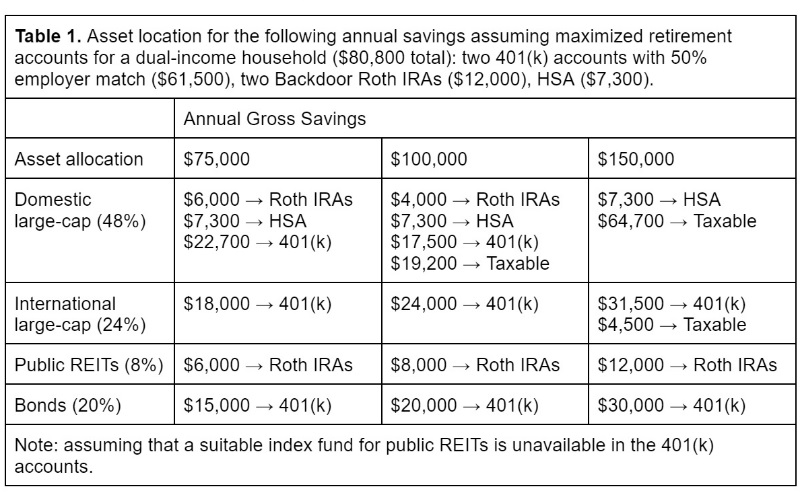

#5 Public REITs Create Asset Location Headaches

Public REITs are not tax-efficient, because they are required to distribute at least 90% of their income in the form of dividends. The dividends are nonqualified and subject to ordinary income tax. Thus, one should have public REITs in tax-sheltered accounts, such as a traditional/Roth IRA or a 401(k).

But for many savers, fitting their public REITs into their tax-sheltered accounts can become a headache (especially if a suitable index fund is not available in their 401(k) account). Public REITs should be the last asset class to be in a taxable account. Table 1 shows the asset location with Rick Ferri’s “Core-4 Portfolio” for a dual-income household that maximizes their retirement accounts. As one’s taxable savings increase, they need to have more of their large-cap stocks (e.g., VTI, VXUS), which are the most tax efficient, in their taxable account (unless they own bonds in taxable).

If they want to add asset classes that are less tax-efficient than large-cap stocks (like SCV stocks), then they may need to exchange the large-cap stocks in their tax-sheltered accounts for their less tax-efficient counterparts. In the above examples, adding just 8% of domestic SCV stocks would require one to own the asset class in multiple accounts: at $150,000 annual savings, one would have to figure out where $4,700 should belong (after buying $7,300 in their HSA). But given the reasons 1-4 above, any benefits of owning public REITs may not outweigh the hassle of optimizing tax efficiency.

What Are the Alternatives?

A detailed section on the alternatives to public REITs is beyond my level of expertise. The White Coat Investor website and other blogs have courses and mountains of content on real estate investing. Private REITs, funds, and syndications may have specific advantages in addition to the “illiquidity premium” (or illiquidity problem!) How about direct ownership and management of residential property? According to the Federal Reserve Bank of San Francisco (FRBSF), the returns on housing, if unleveraged, were as high as that of stocks with less volatility from 1950-2015 (not accounting for transaction costs, maintenance costs, and taxes). But the FRBSF’s study equally weighted the returns in 16 countries. The difference between the two total returns was the greatest in the US, as the mean real returns of equity and housing were 8.39% and 6.03%, respectively. When Big ERN used the source data to calculate the geometric means, the difference was 0.9% for 1870-2015 and 1.92% since 1950.

Unlike stocks and bonds, the alternatives to public REITs are not for every saver. All of the above also comes with additional hassles, whether it is K-1 tax forms or tenants. But most importantly, I want to stress that with any real estate investing—but especially with direct investing into residential real estate—one should beware of the survivorship bias when they hear about returns on real estate investing that exceed that of the stock market. One should not “add” real estate because of FOMO.

More information here:

Financial Products That Are Even Better Than Vanguard’s

‘No Called Strikes in Investing'

Only the likelihood of following a good financial plan matters, and a good financial plan does not need public REITs. One does not need public REITs to have a diversified portfolio, because if they own the total stock market, they already own some real estate. Adding an allocation to public REITs may not accelerate one’s journey to financial independence or achieve other objectives. The less stressful your financial plan, the more likely you are to follow it for 20-30 years, year after year. In the end, one should remember Warren Buffet’s advice: there are “no called strikes in investing.”

WCI’s No Hype Real Estate Investing is the best real estate course on the planet and the best way to get started in this exciting (and profitable) asset class. Taught by Dr. Jim Dahle and more than a dozen other experts, this course is packed with more than 25 hours of content, and it gives potential investors the foundation they need. If you’re interested in real estate investing, you can’t afford to miss the No Hype Real Estate Investing course!

Do you have public REITs in your portfolio? If so, what do you like about them? If not, why are you avoiding them? Are there other reasons not to own any public REITs? Comment below!

The post The Case Against Using Public REITs for Portfolio Diversification appeared first on The White Coat Investor - Investing & Personal Finance for Doctors.

||

----------------------------

By: Josh Katzowitz

Title: The Case Against Using Public REITs for Portfolio Diversification

Sourced From: www.whitecoatinvestor.com/the-case-against-using-public-reits-for-portfolio-diversification/

Published Date: Sat, 26 Nov 2022 07:30:58 +0000

Read More

.png) InvestingStocksToolsClubsVideosPrivacy PolicyTerms And Conditions

InvestingStocksToolsClubsVideosPrivacy PolicyTerms And Conditions