<iframe style="width:120px;height:240px;" marginwidth="0" marginheight="0" scrolling="no" frameborder="0" src="//ws-na.amazon-adsystem.com/widgets/q?ServiceVersion=20070822&OneJS=1&Operation=GetAdHtml&MarketPlace=US&source=ss&ref=as_ss_li_til&ad_type=product_link&tracking_id=peaceinvesting-20&language=en_US&marketplace=amazon®ion=US&placement=0060555661&asins=0060555661&linkId=80f8e3b229e4b6fdde8abb238ddd5f6e&show_border=true&link_opens_in_new_window=true"></iframe>|<iframe style="width:120px;height:240px;" marginwidth="0" marginheight="0" scrolling="no" frameborder="0" src="//ws-na.amazon-adsystem.com/widgets/q?ServiceVersion=20070822&OneJS=1&Operation=GetAdHtml&MarketPlace=US&source=ss&ref=as_ss_li_til&ad_type=product_link&tracking_id=peaceinvesting-20&language=en_US&marketplace=amazon®ion=US&placement=1119404509&asins=1119404509&linkId=0beba130446bb217ea2d9cfdcf3b846b&show_border=true&link_opens_in_new_window=true"></iframe>|<iframe style="width:120px;height:240px;" marginwidth="0" marginheight="0" scrolling="no" frameborder="0" src="//ws-na.amazon-adsystem.com/widgets/q?ServiceVersion=20070822&OneJS=1&Operation=GetAdHtml&MarketPlace=US&source=ss&ref=as_ss_li_til&ad_type=product_link&tracking_id=peaceinvesting-20&language=en_US&marketplace=amazon®ion=US&placement=1119376629&asins=1119376629&linkId=2f1e6ff64e783437104d091faaedfec7&show_border=true&link_opens_in_new_window=true"></iframe>

By Dr. James M. Dahle, WCI Founder

In some ways, the decumulation phase can be a lot more complicated than the accumulation phase as you head into retirement. Lots of retirees get confused when they start thinking about how to spend in retirement. At times it can be complicated, although for most people it doesn't end up being as tricky as you might think. While there are exceptions to every rule of thumb, these guidelines will work for most people most of the time.

There are really three issues that retirees face when deciding how to spend in retirement:

- Which accounts to spend from first

- Which assets to spend first

- How much to spend

The first of these is the most complicated and the one we will spend the most time on today. But before we get into it, I wanted to make a couple of brief comments about the other two.

First, about which assets to spend: as a general rule, you spend from all of your assets, rebalancing as you go just like you did in the accumulation phase. If stocks had a banner year, you're going to spend mostly stocks this year. Bear market yet? You may be spending cash or bonds to bring the portfolio back into balance.

Second, about how much to spend: the answer is about 4% of your initial retirement portfolio, adjusted upward with inflation each year. You can spend a little more if you're willing to be flexible and take a little risk in your life. If you cannot be flexible or are not comfortable with risk, spend a little less. Adjust as you go.

Now, let's get into some guidelines about which accounts to spend from first.

#1 Spend Income First

Most retirees will have some sort of taxable income every year. Since you have to pay taxes on this income already, you might as well spend it. In fact, most retirees will never get past this step. They get enough income here to cover all of their spending wants and needs. These sources of income include:

-

- Pension distributions

- Interest

- Dividends

- Capital gains distributions from mutual funds or those generated by mandatory activities like rebalancing

- Social Security (up to 85% taxable)

- Any required minimum distributions (RMD) from tax-deferred accounts or Roth 401(k)s

- Rent from investments in real estate

- “Retirement job” income

- Annuity distributions

Note that Roth 401(k)s can be rolled over into a Roth IRA and avoid those RMDs, but if you're going to leave it in a Roth 401(k) and thus have to make RMDs from it starting at age 73, you might as well spend it before withdrawing from some other account.

More information here:

How to Access Your Retirement Money When Retiring Early

7 Principles of Withdrawing Money in Retirement

#2 Consider Your Estate Planning Goals

Before you move on to the next step, you really need to consider your estate planning goals. They will have an effect on every decision beyond this one. Do you plan to “Die with Zero?” Do you plan to leave everything that is left to your children? What tax bracket will they be in compared to yours? Do you plan to leave everything to charity? Will you be splitting what you leave behind between heirs and charity? How long is your spouse likely to live compared to you? Are you married in a community property state? What is the basis of your taxable assets (i.e. how much you paid for them)? You will need to consider each of these questions before we can really make any rules of thumb.

#3(a) Die With Zero Plan

It actually really simplifies your estate planning and retirement spending if you just want to maximize your own spending. All you have to avoid is running out of money. The best way to do that is to convert most or all of your assets into an income stream and then spend the income stream. You have to be aware of the effects of inflation on your income stream, though. That's trickier now than it used to be since you can no longer buy inflation-indexed annuities. But here are the guidelines.

- Delay Social Security as long as possible (assuming reasonably good health). This is the best-priced “annuity” you can buy. Plus, it's indexed to inflation.

- Get a reverse mortgage on your home.

- Exchange any cash value life insurance policies into Single Premium Immediate Annuities (SPIAs)

- Annuitize the majority of your taxable and retirement assets at retirement

- Periodically annuitize remaining assets to counter inflation—slower if in good health, faster if in bad

- Spend HSA on healthcare preferentially, but feel free to spend on anything after age 65

If you're married/partnered, these annuities need to pay out until the second person dies.

More information here:

A New Way of Doing Business (and Saving Tons of Money) in My Retirement

Functional Longevity: What Use Is Retirement If You Can’t Move and Think?

#3(b) Leave the Remainder To Heirs

In this common scenario, you want to spend freely from your assets, but whatever you don't need or want will go to your children. You'd like to leave them as much as possible but don't want to cramp your own style to do it. Since annuities and reverse mortgages turn potential inheritances into income streams, you will generally avoid them with most of your assets. Permanent life insurance policies will be left in place to pass the death benefit on to the heirs. Here's how to think about spending.

- HSA for any healthcare expenses

- High-basis taxable assets (mostly spending basis/principal to minimize taxes)

- HSA dollars unlikely to be used for healthcare (Yes, I know this can be hard to determine, but HSAs make for lousy inheritances)

- Low-basis taxable assets (at least until life expectancy < five years)

Now, here is where it gets complicated. The good news is when the answer is not clear cut, it probably doesn't matter all that much what you do.

If your heirs are likely to be in a similar or higher tax bracket than you are, then you want to preferentially leave them Roth assets. If they are likely to be in a lower tax bracket than you are, then you should spend the Roth assets yourself and leave them tax-deferred assets. As a general rule, once you are close to death, you should avoid selling low-basis taxable assets so the capital gains taxes are avoided completely due to the step up in basis at death. Over long periods of time, the tax-protected growth inside retirement accounts will have a larger effect than that of tax savings, but over short periods of time, the tax savings matters more.

How long is long and how long is short? It depends. But a life expectancy under 5-7 years seems appropriate. That means that even if you are in good health in your mid to late 80s, it's probably time to spend tax-deferred money instead of the low-basis taxable assets. And if you ever get a serious diagnosis with less than five years life expectancy, that should trigger a shift as well. This rule applies even if you are the first to die in a community property state but only if you are second to die in non-community property states (surviving spouses get a step up in basis). Also, if one spouse is likely to live for a long time after the first dies, it's nice to leave them more Roth assets since they'll be in the higher single tax brackets.

See, I told you it was complicated. Anyone who tells you to “spend taxable, then tax-deferred, then tax-free” has made things too simple.

If you burn through all of your other assets, you can look into doing partial surrenders and borrowing against cash value life insurance policies and reverse mortgages. The more of your assets that you use, the less your heirs will get, so it can be a bit of a balancing act.

#3(c) Leave the Rest to Charity

Similar to 3(b), you want to spend whatever you want to spend, but then you want to leave the rest to charity. In this situation, if you are willing to consider annuitizing some of your nest egg, be sure to take a look at a Charitable Remainder Annuity Trust (CRAT)—which provides you an income and some pretty good tax breaks before leaving the rest to charity at your death or after a certain number of years. You would think that you would be likely to leave more to charity by not annuitizing, just like you'd be likely to leave more to your heirs. However, the difference is that if you leave everything to charity at death, you're likely not getting the full tax benefit of that donation. A CRAT allows you to get those benefits—it is actually possible to leave more to charity using a CRAT simply because you paid less in taxes.

You can also make the charity the beneficiary of any cash-value life insurance policies you may have and leave your house to charity in your will. Here's how to spend.

- HSA for any healthcare expenses

- High-basis taxable assets (mostly spending basis/principal to minimize taxes)

- Low-basis taxable assets (at least until life expectancy < five years)

- Roth assets

- Tax-deferred assets and HSA for non-healthcare expenses

Remember that whether you leave a $100,000 IRA or a $100,000 Roth IRA to a charity, the charity gets $100,000. But if you spend a $100,000 IRA, you may only get to spend $70,000-$85,000. Spend the Roth money first.

More information here:

You Can’t Make Your Great Grandchildren Rich

#3(d) Split the Rest Between Heirs and Charity

Naturally, this is going to be the most complicated scenario (and unfortunately the one Katie and I will find ourselves in.) As you make decisions, you need to have this continuum crystal clear in your mind.

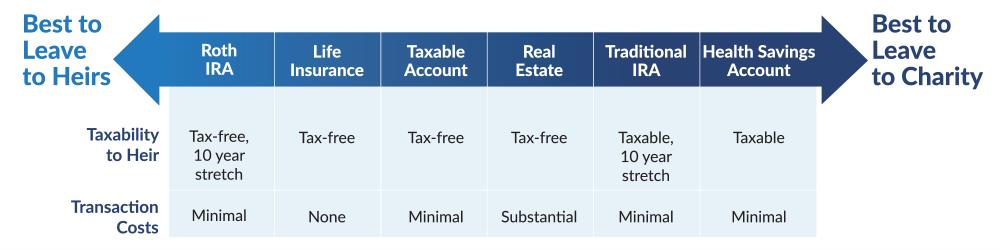

The general principle here is that your heirs prefer a tax-free inheritance and your favorite charities don't care since it is all tax-free to them. The worst things to inherit should go to the charity, and the best things to inherit should go to your heirs. Given that tax-deferred accounts can only be stretched for 10 years now, your heirs are almost always going to be better off inheriting a taxable account rather than a tax-deferred retirement account.

When splitting what you leave behind between heirs and charities, how you spend down your assets not only depends on the tax consequences to you during your life but also the relative sizes of each account and the relative amounts that you wish to leave to heirs and charities. Because of this, there are no reasonably accurate rules of thumb that can be applied. I recommend that you spend down your assets in a way that maximizes the total amount that can be spent by you, your heirs, and the charities. That primarily means spending in a way that minimizes your tax burden, knowing that anything with really nasty tax consequences can just be left to charity. Here's the best list I could come up with.

- HSA for any healthcare expenses

- High-basis taxable assets

- Low-basis taxable assets

- Tax-deferred assets if you have more in tax-deferred/HSA than you wish to leave to charity. Tax-free assets if you have less in tax-deferred/HSA than you wish to leave to charity.

The good news? You're probably not in this situation. If you have so much wealth that you're afraid to leave it all to your kids lest you ruin them, you're probably never spending more than your income anyway.

The decumulation years can be complicated. They are made more so by conflicting desires to spend more, to leave more to heirs, and to leave more to charity. The fact that our mental acuity tends to worsen over time doesn't help either. If you find that you are needing help to sort this all out, consider meeting with one of our recommended financial advisors. They can help send you on the right path.

Want to learn even more about How to Spend Your Money in Retirement? Watch the presentation that Dr. Dahle gave at WCICON23 in the just-released Continuing Financial Education 2023 course!

What do you think? What is your retirement spending plan? Has it been difficult to come up with a deaccumulation strategy? Comment below!

The post How to Spend in Retirement appeared first on The White Coat Investor - Investing & Personal Finance for Doctors.

||

----------------------------

By: The White Coat Investor

Title: How to Spend in Retirement

Sourced From: www.whitecoatinvestor.com/how-to-spend-in-retirement/

Published Date: Wed, 05 Apr 2023 06:30:41 +0000

Read More

.png) InvestingStocksToolsClubsVideosPrivacy PolicyTerms And Conditions

InvestingStocksToolsClubsVideosPrivacy PolicyTerms And Conditions