<iframe style="width:120px;height:240px;" marginwidth="0" marginheight="0" scrolling="no" frameborder="0" src="//ws-na.amazon-adsystem.com/widgets/q?ServiceVersion=20070822&OneJS=1&Operation=GetAdHtml&MarketPlace=US&source=ss&ref=as_ss_li_til&ad_type=product_link&tracking_id=peaceinvesting-20&language=en_US&marketplace=amazon®ion=US&placement=0060555661&asins=0060555661&linkId=80f8e3b229e4b6fdde8abb238ddd5f6e&show_border=true&link_opens_in_new_window=true"></iframe>|<iframe style="width:120px;height:240px;" marginwidth="0" marginheight="0" scrolling="no" frameborder="0" src="//ws-na.amazon-adsystem.com/widgets/q?ServiceVersion=20070822&OneJS=1&Operation=GetAdHtml&MarketPlace=US&source=ss&ref=as_ss_li_til&ad_type=product_link&tracking_id=peaceinvesting-20&language=en_US&marketplace=amazon®ion=US&placement=1119404509&asins=1119404509&linkId=0beba130446bb217ea2d9cfdcf3b846b&show_border=true&link_opens_in_new_window=true"></iframe>|<iframe style="width:120px;height:240px;" marginwidth="0" marginheight="0" scrolling="no" frameborder="0" src="//ws-na.amazon-adsystem.com/widgets/q?ServiceVersion=20070822&OneJS=1&Operation=GetAdHtml&MarketPlace=US&source=ss&ref=as_ss_li_til&ad_type=product_link&tracking_id=peaceinvesting-20&language=en_US&marketplace=amazon®ion=US&placement=1119376629&asins=1119376629&linkId=2f1e6ff64e783437104d091faaedfec7&show_border=true&link_opens_in_new_window=true"></iframe>

By Dr. Zachary Zemore, Guest Writer

Being only a few years out of residency, I am deeply immersed in the accumulation phase of my financial journey. Like many readers, I have read all the old White Coat Investor blog posts and have a firm grasp on the financial essentials, such as establishing a proper budget, minimizing expenses, and paying off student debt in a timely fashion. At the same time, I am also maxing out my 401(k) and executing a Backdoor Roth IRA, and I have opened a brokerage account. Thanks to my low cost of living, even with these financial sinks, I still find myself with surplus funds which can be mobilized for actionable financial progress.

What, then, should a reasonable physician do? Certainly, risk tolerance and capacity for further work must be considered at this point. Many physicians elect to capitalize on surplus funds by further diversifying their portfolios with real estate investing. As someone who prefers less risk and desires more free time to be spent on family or long-lost hobbies, the idea of beginning a real estate venture or a similar process is completely unappealing. However, if you own a home, there is one real estate investment that makes sense and will almost always guarantee that you “beat the market:” Paying down the first half of your mortgage as quickly as possible.

Let me explain.

The Mortgage vs. The Market

Aside from student loans, which are typically higher in interest rate, the next most common debt is home mortgage debt. There are countless web articles that simply note the interest on a home mortgage is likely somewhere between 3%-5%, while the average annual stock market return is notably higher, around 8%. This leads many to the uninformed conclusion that investing that extra money into the stock market is more profitable than using it to pay down your mortgage to save that 3%-5% in interest. I would argue that this is a superficial analysis that gets turned onto its head when you consider mortgage amortization schedules.

What Is a Mortgage Amortization Schedule?

Let’s start back with the basics. When you purchase a home, you take out a loan from the bank. The bank charges an annual interest rate as a fee for this lending service. In this example, let’s say you purchase a home for $500,000 at 3.5% and get a standard 30-year mortgage. In simplest terms, you would pay 3.5% interest of the principal every year for 30 years. The principal payment would always remain the same, and your interest payments would decrease as the principal is reduced. Your total payment would be higher initially and then decrease over time. This is called straight-line amortization.

Unfortunately, it is not that simple, and this is NOT what banks do.

The disadvantages of straight-line amortization are that payments change on a monthly basis and that they are highest at the beginning of the loan. To counteract these negatives, banks created mortgage amortization. In this method, monthly payments are the same over the life of the loan. This means that interest fees are paid in higher proportion in the early years of the loan, while principal payments are weighted more highly in the later years of the loan. The result is that the customer pays the principal much more slowly at first, and total interest payments are higher over the life of the loan. While beneficial for the borrower to have consistent payments, mortgage amortization schedules were created with the lender’s profit in mind.

More information here:

How to Get a Mortgage with a Great Rate

Is Paying More Interest in the Early Years of Your Loan a Problem?

The result of a mortgage amortization schedule is that you end up paying approximately 15% more in total interest compared to a straight-line amortization. While paying more total interest is not ideal, the negative effects are further increased if you move before paying off your home. Think about it: how many people do you know who live in a home for 30 years these days? It’s very few, in fact. The average time spent in a home is only eight years, while the median is only 13 years. This results in a minimum amount of wealth accumulated as equity, while the highest amount of your money goes toward interest and lender profit.

After eight years, 60% of your mortgage payments would have gone to interest. Life and desires change quickly. Think back to when you were 20 years old. Did you guess correctly what your life would look like as a 35-year-old? I’m guessing not. Unless you live in your dream home, easily afford the payments, and plan to stay there for the remainder of your years, I would consider a closer analysis on the benefits of paying your mortgage early.

Mortgage Amortization Schedule Breakdown

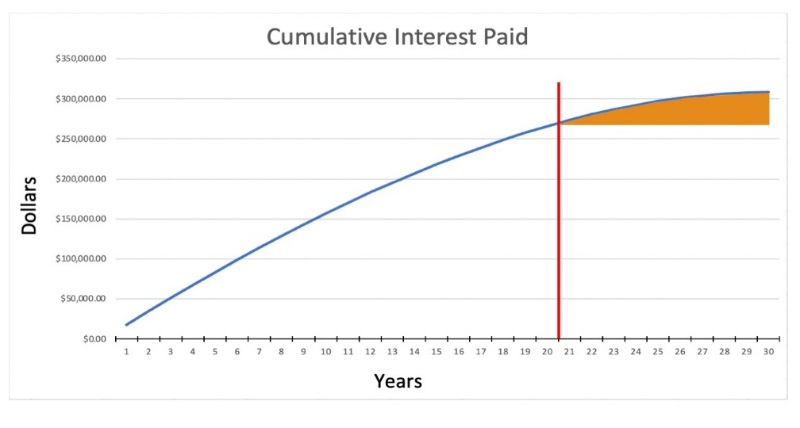

When you look at a standard mortgage amortization graph offered by banks, it can get quite confusing. They typically have multiple lines representing very different data all on one chart. While well-intentioned, this makes it difficult to isolate the important aspect: total interest paid. Below is a standard mortgage amortization graph from our example home, with the total interest payments isolated. When you take a closer look, you realize a few things. As previously noted, your interest payments are initially quite high. There are also very subtle inflection points, where your interest payments will begin to decrease significantly. As the slope of the line approaches zero, meaning the line becomes more horizontal, your interest payments are approaching zero. The line placed at the 20-year mark helps demonstrate truly how little interest is paid in the final decade of your loan (orange area under the curve).

To simply state that paying your mortgage early will earn you the interest rate charged for the loan is actually quite inaccurate, depending on the portion of the loan being analyzed. You must compare the return on investment among different strategies to truly compare them fairly. The same principles of compounding interest earned in a retirement account apply to interest saved on a mortgage amortization schedule.

It is for this reason that I say every physician should pay their mortgage early—to own at least half of their home. If you pay off the first 20 years of your mortgage within the first five years, you are almost assuredly beating out any investment that you would otherwise pick, while maintaining the month-to-month flexibility of low required monthly payments.

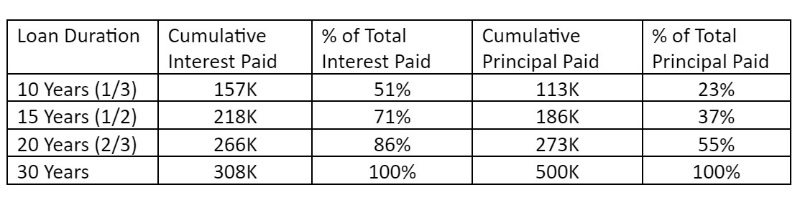

In our above example, a $500,000 home was purchased at 3.5% interest rate for 30 years. The table below shows various amounts of interest and principal paid at various points during the loan.

What you can see is the numerical representation of interest payments being front-loaded and principal payments being back-loaded. Half of your interest is paid in the first 10 years of the loan, while only a quarter of your principal is paid in the same decade-long timeframe. Therefore, if you were to pay off the first 20 years of this mortgage over five years, you would have a guaranteed return on investment of approximately 10%. This is incredible, and it rivals even the best stock market returns. What’s more, when you consider this is only over a five-year period and you compare that to the short-term volatility of the stock market, it becomes increasingly likely that you will beat out any and all plausible stock market returns.

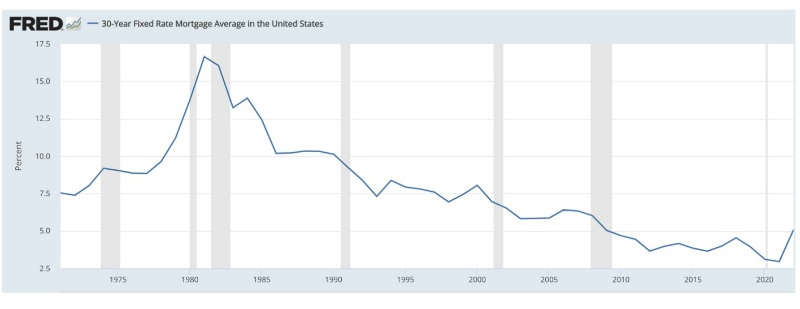

Additionally, the benefits will only increase as mortgage interest rates climb. Just as you can use historical data to determine stock market returns, you can also use historical data to estimate home mortgage interest rates. From the graph below, you can see the years where rates were less than 3.5% were truly remarkable, and they should not be counted on for future homebuyers.

Should You Pay Off the Entirety of Your Mortgage or Just Half?

As you approach the last one-third of the mortgage amortization schedule, your return on investment begins to diminish significantly. This can be exemplified by comparing the interest saved if you were to pay the first year or the last year of your loan early. During the first year, you would save $17,000 by paying it off early, which equates to an astounding return on investment of 180%. In the last year, you would only save $500 which is an ROI of a paltry 1.8%. Therefore, in the last one-third of the loan, it is increasingly wise to invest your money elsewhere.

In essence, this means you would pay your 30-year mortgage in roughly 15 years. For some, there can be emotional wins from completely eliminating debt, but by the numbers, this is technically not the most advantageous option. Some will argue that it would be wiser to simply get a 15-year mortgage and obtain a lower interest rate. This is certainly a valid argument, but for those of us with a lower net worth, erratic income, low starting equity, or many other scenarios, this does not afford the same flexibility that a 30-year mortgage does with its lower required payments. I, for example, am getting married in the fall of 2023, and I skipped three months of my extra principal payments to pay for the wedding. This is the type of flexibility I need at this point in my life, and I’m certain that anyone with a family or other source of unexpected expenses would agree.

More information here:

10 Ways to Pay Off a Mortgage Quickly

Things to Consider Before You Pay Off Your Mortgage Early

It is important to note a few caveats before using your surplus funds to pay down your mortgage.

- While your returns can be great, they do not trump the financial benefits of fully funding your 401(k)/IRA. You should only prioritize paying the first half of your mortgage after funding these accounts and having a student loan debt plan in place.

- Most home mortgages don’t penalize you for paying early, but it’s best to check the fine print first.

- When you do begin paying ahead, don’t recast your loan or the returns will diminish significantly.

- If ever refinancing, do not refinance for a period of time longer than your current position on the amortization schedule.

- And for those of you considering the tax implication in regards to mortgage interest deductions, the adage of spending more on your mortgage to save more on your taxes again does not hold true.

The net gain is always in favor of paying your mortgage early.

If you're interested in pursuing other kinds of real estate investing and working with some of the WCI-vetted partners that Dr. Jim Dahle invests with, here are some of the best companies in the business.

Featured Real Estate Partners

Southern Impression Homes

Type of Offering:

Turnkey

Primary Focus:

Single Family

Minimum Investment:

$65,000

Year Founded:

2017

MLG Capital

Type of Offering:

Fund

Primary Focus:

Multi-Family

Minimum Investment:

$50,000

Year Founded:

1987

DLP Capital

Type of Offering:

Fund

Primary Focus:

Multi-Family

Minimum Investment:

$100,000

Year Founded:

2008

37th Parallel

Type of Offering:

Fund / Syndication

Primary Focus:

Multi-Family

Minimum Investment:

$100,000

Year Founded:

2008

Origin Investments

Type of Offering:

Fund

Primary Focus:

Multi-Family

Minimum Investment:

$50,000

Year Founded:

2007

Wellings Capital

Type of Offering:

Fund

Primary Focus:

Self-Storage / Mobile Homes

Minimum Investment:

$50,000

Year Founded:

2014

AcreTrader

Type of Offering:

Platform

Primary Focus:

Farmland

Minimum Investment:

$5,000

Year Founded:

2017

Mortar Group

Type of Offering:

Syndication

Primary Focus:

Multi-Family

Minimum Investment:

$50,000

Year Founded:

2001

* Please consider this an introduction to these companies and not a recommendation. You should do your own due diligence on any investment before investing. Most of these opportunities require accredited investor status.

Does this kind of mortgage payment schedule make sense to you? If you could pay off the first half of your mortgage early, where else would you invest? What else could you do with that saved money? Comment below!

[Editor's Note: Dr. Zach Zemore is a graduate of a combined training program in Emergency Medicine and Internal Medicine who is currently expanding his personal and professional horizons in the big sky country of Montana. This article was submitted and approved according to our Guest Post Policy. We have no financial relationship.]

The post Why Every Doctor Should Own Half a Home appeared first on The White Coat Investor - Investing & Personal Finance for Doctors.

||

----------------------------

By: Lauren O'Brien

Title: Why Every Doctor Should Own Half a Home

Sourced From: www.whitecoatinvestor.com/pay-off-half-mortgage/

Published Date: Fri, 17 Mar 2023 06:30:07 +0000

Read More

.png) InvestingStocksToolsClubsVideosPrivacy PolicyTerms And Conditions

InvestingStocksToolsClubsVideosPrivacy PolicyTerms And Conditions