<iframe style="width:120px;height:240px;" marginwidth="0" marginheight="0" scrolling="no" frameborder="0" src="//ws-na.amazon-adsystem.com/widgets/q?ServiceVersion=20070822&OneJS=1&Operation=GetAdHtml&MarketPlace=US&source=ss&ref=as_ss_li_til&ad_type=product_link&tracking_id=peaceinvesting-20&language=en_US&marketplace=amazon®ion=US&placement=0060555661&asins=0060555661&linkId=80f8e3b229e4b6fdde8abb238ddd5f6e&show_border=true&link_opens_in_new_window=true"></iframe>|<iframe style="width:120px;height:240px;" marginwidth="0" marginheight="0" scrolling="no" frameborder="0" src="//ws-na.amazon-adsystem.com/widgets/q?ServiceVersion=20070822&OneJS=1&Operation=GetAdHtml&MarketPlace=US&source=ss&ref=as_ss_li_til&ad_type=product_link&tracking_id=peaceinvesting-20&language=en_US&marketplace=amazon®ion=US&placement=1119404509&asins=1119404509&linkId=0beba130446bb217ea2d9cfdcf3b846b&show_border=true&link_opens_in_new_window=true"></iframe>|<iframe style="width:120px;height:240px;" marginwidth="0" marginheight="0" scrolling="no" frameborder="0" src="//ws-na.amazon-adsystem.com/widgets/q?ServiceVersion=20070822&OneJS=1&Operation=GetAdHtml&MarketPlace=US&source=ss&ref=as_ss_li_til&ad_type=product_link&tracking_id=peaceinvesting-20&language=en_US&marketplace=amazon®ion=US&placement=1119376629&asins=1119376629&linkId=2f1e6ff64e783437104d091faaedfec7&show_border=true&link_opens_in_new_window=true"></iframe>

By Dr. James M. Dahle, WCI Founder

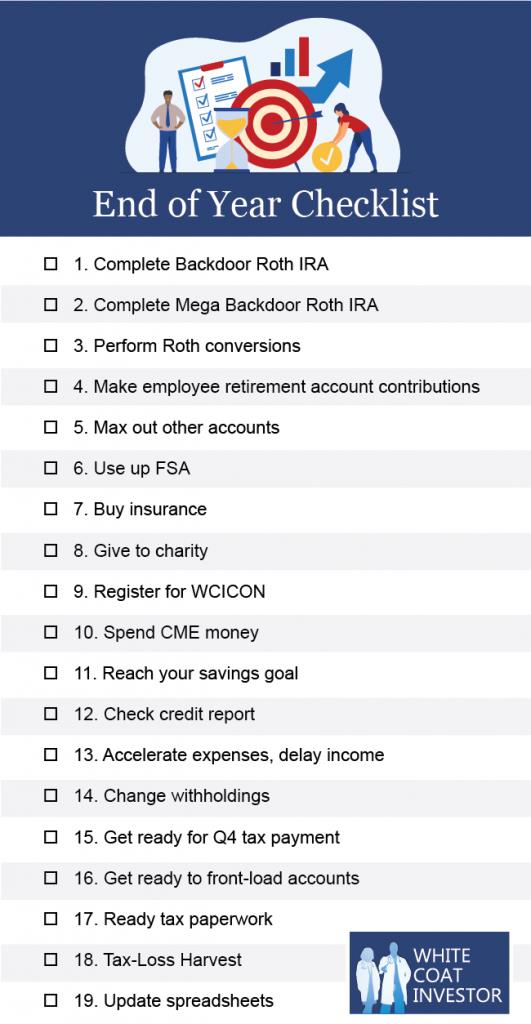

Another year in your financial life has almost come and gone. As has become a tradition at The White Coat Investor, we're unveiling (and updating) an end-of-the-year financial checklist, so that you can take care of everything that needs to be done before the calendar year is out. While every item may not apply to your situation, it's still worth a few minutes to make sure you have not forgotten anything you will regret.

#1 Complete Backdoor Roth IRA Process

Near the end of 2021, Congress was talking about eliminating the ability to do the Backdoor Roth, but that never came to pass. It has always been a smart move to complete both the contribution step and the conversion step within the calendar year. Some like to knock out this task early in the year. But if you are one who has been procrastinating it to the following calendar year or if you simply forgot to do the conversion step, be sure to get it done before year's end.

More information here:

- Backdoor Roth IRA Step-by-Step Guide

#2 Mega Backdoor Roth IRA

The Mega Backdoor Roth IRA is when you make after-tax (not Roth) contributions to your 401(k) and then immediately convert them either within the plan to a Roth 401(k) or by withdrawing them from the plan and converting them directly into a Roth IRA. If this is part of your plan, make sure you complete both steps before the end of the year.

More information here:

- The Mega Backdoor Roth IRA

#3 Roth Conversions

While a Roth conversion of after-tax money is part of both the Backdoor Roth IRA and the Mega Backdoor Roth IRA processes, that's not what I'm talking about here. I'm talking about converting pre-tax money to Roth money, essentially pre-paying the taxes on your retirement savings. This is not always a good idea, but if it is for you and you want to pay the tax bill for it on your 2022 taxes, you need to do the conversion before the end of the year.

More information here:

#4 ‘Employee' Retirement Plan Contributions

Whether you are employed and dealing with an employer 401(k)/403(b)/457(b) or you are self-employed and use an individual 401(k), you need to make the entire “employee” contribution ($20,500 for those under 50) by the last paycheck of the year. Your employer (or you, if you are the employer) has a few more months to make the employer portion of the contribution, and SEP IRA contributions can be made until you file your taxes. But your money needs to get in there now if you want to max out that account for the year.

More information here:

- Multiple 401(k) Contribution Rules

- SEP IRA vs Solo 401(k)

#5 Max Out 529s, ESAs, ABLEs, and UTMAs

Aside from your retirement accounts and an HSA, all of your other investing accounts require contributions to be made during the calendar year. If you're planning to put more in there this year, get it done. This includes college savings accounts such as 529s and Coverdell Education Savings Accounts (ESAs), an ABLE account for your disabled child, and Uniform Transfer to Minors (UTMA) accounts if you are providing a “20s fund” for your kids, like we are. Even though you can contribute to HSAs until Tax Day, the earlier the better.

More information here:

- 7 Reasons an HSA Should Be Your Favorite Investing Account

- Best 529 Plans: Reviews, Rankings, and Ratings

- ABLE: A Tax-Protected Investing Account for Your Special Child

- How Your Kids Can Lower Your Taxes

#6 Use Up Your Flexible Spending Account (FSA)

Health Savings Account (HSA) balances are carried over from year to year. That is not the case with any money you or your employer have put into a Flexible Spending Account (FSA). You need to use up that money before the end of the year, or you will lose it completely.

More information here:

- Optimize Tax Savings from Dependent Care FSA

#7 Get Insurance in Place

This one does not technically have a year-end deadline—the price actually goes up either on your birthday or six months before your birthday. However, if you and/or someone else depend on your income, you need to buy disability +/- term life insurance ASAP. This is so important I made it Chapters 1 and 2 in The White Coat Investor's Financial Boot Camp.

More information here:

- Recommended Insurance Agents

- Physician Disability Insurance

- How to Buy Life Insurance

#8 Give to Charity

Giving to charity is always a wonderful thing, but if you itemize, it is far better to give on December 31 than on January 1, at least from a tax perspective. If you're not yet sure what charity or charities you want to support, consider contributing to a Donor Advised Fund to get the tax break now and designate the recipient charities later.

More information here:

- Tax Benefits of Donating to Charity

- Donor Advised Fund

#9 Register for WCICON

The annual WCI Conference, aka The Physician Wellness and Financial Literacy Conference, is coming up on March 1-4. If you want to attend in person, you should register ASAP. If you are coming, you also need to register for the room block before the hotel releases those rooms for other guests. You can register for the virtual version right up until the day of the conference. Either way, WCICON is a great value, where you can learn about financial literacy, hear from some wonderful speakers, mingle with your fellow physicians, and enjoy some downtime in the warm Phoenix sun.

More information here:

WCICON23 Registration

#10 Spend CME Money

Like FSA money, many people have designated CME funds that are use-it-or-lose-it at year's end. Be sure to spend that money on books, computers, courses, or conferences. Remember that WCICON and many WCI courses are eligible for CME including:

- Financial Wellness and Burnout Prevention for Medical Professionals (Fire Your Financial Advisor, plus eight hours of wellness material)

- Continuing Financial Education 2022 (All the material from WCICON22, plus additional material—over 50+ hours of content!)

Even if you are self-employed and don't have a CME fund, courses and conferences that qualify for CME are deductible business expenses.

More information here:

- The Best Way to Use CME Money

#11 Hit Your Savings Goal

I hope you have a savings goal every year, something like 20% of your gross income toward retirement. How are you doing? Are you behind? If so, put some money toward that goal before the end of the year. If you've already maxed out your retirement accounts, invest it in a taxable account. There is no contribution limit there.

More information here:

- The Taxable Investing Account

- 6 Reasons to Have a High Early Savings Rate

- Safe Savings Rate — How Much Do I Need to Save for Retirement?

- 7 Ways to Increase Your Savings Rate

#12 Get Free Annual Credit Reports

This one doesn't have to be done at the end of the year, but it's definitely worth doing once a year. Why not now? Just go to AnnualCreditReport.com and download all three reports for you and your spouse. They don't give you a credit score, but it's important to make sure there's nothing on those reports that you either don't recognize or had forgotten about.

More information here:

- 10 Benefits of Keeping Your Credit Score in Good Health

- Why My Credit Score Is Higher Than Jim Dahle’s

#13 Accelerate Expenses, Delay Income

There is a general rule in tax planning to accelerate (front-load) your expenses and delay (back-load) your income. Assuming that you aren't changing tax brackets between years and that the tax brackets themselves are not changing in the new year, it makes sense for you personally or for your business to pay as much as you can in the old year and to get paid in the new year. Although the federal income tax system is a “pay-as-you-go” system, this could potentially allow you to delay the payment of taxes by as much as a year. In states that are not pay-as-you-go (like Utah), it would be like getting a 12-month interest-free loan from the state tax commission.

A related technique is “bunching” of itemized deductions. Some people don't have enough itemized deductions to bother itemizing, but if they bunch two years' worth of deductions into one year, then it makes sense to itemize. So, they itemize every other year, taking the standard deductions in the opposite years. This might mean making charitable contributions (especially if using a Donor-Advised Fund (DAF)) on January 1 and December 31 of one year, and then none in the next year. You could possibly do this with property/income tax payments or even medical expenses.

This strategy can also be profitably used in years in which your tax bracket or the tax bracket themselves are changing; just make sure you bunch into the right year (the one when you're in a higher bracket)! Businesses routinely do this as well, preferentially paying accounts due while allowing accounts receivable to pile up a bit. A medical practice might actually do the opposite knowing that bills are more likely to be paid by the insurance company at year's end, while bills at the beginning of the year might be sent primarily to the patients themselves (who are less likely to pay) since they have not yet met their deductible.

More information here:

- What You Need to Know About Schedule A

#14 Change Withholdings

Do you get huge tax refunds? You probably shouldn't be happy about that. You can adjust your withholdings to minimize how much you are loaning tax-free to the IRS each year. Get your money throughout the year instead of the next April. You can also play games using your withholdings if you make estimated tax payments. All withheld money is treated the same, whether withheld in January or December. That's not the case with quarterly estimated payments.

More information here:

- Estimated Taxes and the Safe Harbor Rule

#15 Get Ready for Q4 Estimated Tax Payment

If you are an independent contractor, make sure you have the cash flow to make that fourth-quarter estimated tax payment by January 15.

More information here:

- Financial Planning for 1099 Independent Contractors

#16 Get Ready to Front-Load Accounts

OK, this one is for the real money nerds out there. Some of us front-load our accounts, including HSA, Backdoor Roth IRAs, 529s, and even 401(k)s, completely funding them the first week of the year. If you are one of those folks, make sure you are planning for the cash flow to do so. You can't invest the same money into a taxable account on December 20 that will be needed for those contributions.

More information here:

- 5 Reasons Why I Don’t Regret Lump-Sum Investing in January 2022

#17 Make Sure Tax Paperwork Is Ready

While most of your tax paperwork doesn't start coming in until the last week of January, you can go ahead and get the parts that you prepare ready now. That might include:

- Pulling money out of 529s equal to receipts and possibly scholarships received

- Storing receipts to justify 529 withdrawals

- Pulling money out of HSA equal to receipts

- Storing receipts to justify HSA withdrawals (especially important to have durable storage if you're doing the “save receipts strategy”)

- Making sure your business or charitable mileage logs are up-to-date

- Gathering documentation for charitable gifts

- Updating contracts and timesheets if your business is paying your kids

It's just a good idea to do all this stuff while it is fresh in your mind, rather than next April when you file your taxes (or two years from now when you face an audit).

More information here:

- 2022 Tax Preparation Checklist

- Business Mileage Deduction

#18 Tax-Loss Harvest

If you invest in a taxable account, you might as well check for tax losses. It's a better habit to check after a big market decline, but December isn't a bad time to compare the basis to the value of your investments. If you have significant losses, why not tax-loss harvest them? You can use up to $3,000 in capital losses every year against your ordinary income and an unlimited amount against your capital gains. There are investors out there (like me) who simply don't pay capital gains taxes, thanks to lots of tax losses saved up over years.

More information here:

- A Step-by-Step Tax-Loss Harvesting Guide

#19 Update Your Spreadsheets

If you use a spreadsheet to track your net worth, your savings rate, or your investment return, get it updated. I measure each of these things once a year as a year-end chore. You might also want to make sure your investing plan is on track by measuring progress toward your goals and making sure it does not need to be rebalanced.

More information here:

- Doctor Net Worth: How to Calculate It and What Is the Physician Average Net Worth

- Calculate Compound Interest with the Future Value Calculation

- Excel XIRR: How to Calculate Your Return

- Portfolio Rebalancing Spreadsheet/Tool

Whew! You made it. That was a lot of chores. Hopefully, you didn't still have to do all of them. But if you have a bunch, here's a checklist you can print out and use for 2022 and beyond:

What do you think? What else would you put on your end-of-year checklist? How many of these chores have you still not completed? Comment below!

[This updated post was originally published in 2020.]

The post End of Year Financial Checklist for 2022 appeared first on The White Coat Investor - Investing & Personal Finance for Doctors.

||

----------------------------

By: Emily

Title: End of Year Financial Checklist for 2022

Sourced From: www.whitecoatinvestor.com/end-of-year-financial-checklist/

Published Date: Sat, 10 Dec 2022 07:30:36 +0000

Read More

.png) InvestingStocksToolsClubsVideosPrivacy PolicyTerms And Conditions

InvestingStocksToolsClubsVideosPrivacy PolicyTerms And Conditions